In s titu tio n a l E q u itie s

Initiating Coverage

Paint Sector

The sector which keeps on giving growth

In recent times, growth in India’s paint sector has been an outlier in the overall domestic

consumer space. The industry has been witnessing a gradual shift in terms of consumer

preferences from the traditional whitewash to better quality paints. Besides, it is also witnessing

healthy competitive environment, where players are applying different strategies to tap the

growing demand in the market for a larger regional share. Additionally, rise in disposable income

of the average middle class, urbanization, growing rural market, shortening of repainting cycle,

upgradation, increase in sale of premium-end products and launch of many innovative products

are the major drivers that are pushing the growth of the organized paint industry. Within the

Indian decorative paint segment, Asian Paints (APNT) and Berger Paints (BRGR) are the two

largest players with more than 80% of their overall revenues coming from the segment and within

the industrial paints segment, Kansai Nerolac (KNPL) is the leader (segment contributes ~45% to

its revenue). Since in the current environment there is a preference for businesses that are

relatively more resilient, sector multiples at current levels in near term will look expensive. We

initiate coverage on APNT (Accumulate rating) and BRGR (Sell rating), as we believe that Indian

decorative paints will continue to witness higher demand within this space, majorly led by steady

shift from unorganized to organized players with bigger players gaining further share.

Leaders continue to maintain share even as new players have entered in an oligopolistic market:

Organized domestic decorative paints industry is a comfortable oligopoly with a few big players (Asian

Paints, Berger, Kansai Nerolac and Akzo Nobel), constituting bulk of the segment, with strong entry

barriers such as distribution network and brand equity. The industry has demonstrated consistent pricing

discipline and has not seen mutually destructive price wars, discounting etc. Thus, every company has

co-existed with its own specific niche – regional strength, expertise in particular product sub-segment etc.

Although new players have entered the market over the last decade, existing players have strengthened

their distribution network, focused on capacity building and introduced innovative products & services to

help them fortify their market standing across regions.

Domestic decorative paints putting on a good show in a tough environment: Over the years, the

segment has been driven by urbanization, shortening of re-painting cycle and industry initiatives in terms

of reach expansion and introduction of variety of products. In recent times, the industry has been

witnessing a gradual shift in consumer’s preference from the traditional whitewash to better quality ‘value

for money (VFM)’/’bottom of pyramid (BOP)’ paints, especially in the tier II/III/IV cities. Growth prospect

for these products (mainly putty, distemper, lower end enamels) is strong in the near term for the listed

paint majors. Besides, the industry is witnessing healthy competitive environment, where players are

applying different strategies to tap the growing demand in the market for a larger regional share.

Additionally, rise in disposable income of the average middle class, urbanization, growing rural market

and launch of many innovative products (like eco-friendly, odour free and dust & water-resistant paints)

are other major drivers that are propelling the organized industry growth.

Benign cost environment in near term: The Indian paint industry is a raw-material oriented industry.

The primary cost being crude and its derivatives. Amid the tight business conditions, the soft price trend

in raw materials has been a beneficial factor for companies. Notwithstanding the sharp depreciation in

the exchange rate, overall material prices have been lower even on a sequential basis. This has helped

improve the gross margins for the entire coatings business in India as well as the International markets.

In addition, the cost control measures, especially in the area of selling & distribution and admin expenses

should help negate some of the adverse impact of lower topline in FY21 for Indian paint companies.

Sector view: Demand conditions for the industry has improved progressively since May’20 driven by

demand in upcountry markets, but sporadic lockdowns in various states might cause some hiccups. Tier

II/III/IV cities will continue to do well and even metros and tier I cities are expected to bounce back both

for decorative and other segments as well. Since in the current environment there is a preference for

businesses that are relatively more resilient, sector multiples at current levels in near term will look

expensive. We initiate coverage on APNT (Accumulate rating) and BRGR (Sell rating) as we believe

these are fundamentally strong businesses in the domestic decorative space.

Vishal Punmiya

Research Analyst

vishal.punmiya@nirmalbang.com

+91-22-6273 8064

Company

Rating

Mcap

CMP (Rs)

TP (Rs)

Upside/

Downside

(%)

P/E (x)

EV/EBITDA (x)

RoE (%)

Rsbn

$bn

FY21E

FY22E

FY23E

FY21E

FY22E

FY23E

FY21E

FY22E

FY23E

APNT

Accumulate

1,822

25

1,899

2,080

10

68

51

44

42

34

30

24

28

29

BRGR

Sell

522

7

538

500

-7

76

57

48

46

36

31

24

27

28

Source: Companies, Nirmal Bang Institutional Equities Research

1 September 2020

In s titu tio n a l E q u itie s

Paints Sector

2

Table of Content

Industry overview …………………..….……..………………………..….……..………...03

Demand drivers of decorative segment…………….…………………..….…………….11

Key players in the decorative segment...…………..………………..…….……….……18

Foraying into adjacencies…………….…..……..……….………………….……….……20

Raw material centricity…….…….…….…….……..……………………..….……………22

Capacity expansion during the recent years.…..…......…......…......…......…..........…24

Key risks to the sector…………..……………………..….……….…….…….…….…….25

Key highlights from recent channel checks.......……….………………….……….……26

Comparison of top paint companies in decorative segment.…………….……….……27

Sector view....……….…..……………………..…………..……….…….…….…….…….28

Companies

Asian Paints Ltd…. ………………………………………………………………..………33

Berger Paints Ltd..………………………………………….……...………………………63

In s titu tio n a l E q u itie s

Paints Sector

3

Industry overview

I. Global picture

As against the global paints and coatings industry, which generates revenue of ~US$160bn, the Indian paint

industry is valued at ~US$7.1bn as on FY20. Asia Pacific (APAC), the world’s largest coatings market with

45% market share and valued at US$71bn+ in 2019, has been growing faster than the global and matured

markets on account of relatively higher growth in the economy, especially in China and India. China is the

largest part of the APAC market, comprising nearly 60% of volume and value. Including the next two largest

markets, India and Japan, the top three markets account for over 80% of the volume and value of the APAC

region.

Exhibit 1: Global: APAC shares 45% of market share

Exhibit 2: APAC: Top 3 countries demand 80% of market share

Asia Pacific

45%

EMEA 30%

US and

Canada 18%

Latin America 7%

China 60%

India 12%

Japan 8%

Korea 6%

Others 14%

Source: PPG investor presentation, Nirmal Bang Institutional Equities Research

Source: Industry, Nirmal Bang Institutional Equities Research

India, APAC’s second largest coatings market, is dominated by the decorative segment with ~75% market

share. This is unlike the global and APAC markets’ structure where decorative segment (architectural)

contributes less than 40%. Industrial paint’s lower contribution in India’s overall paint market is probably

attributable to lower industrial and infrastructure development compared to other matured countries and

developing countries like China, and higher technical know-how required in the industrial paint segment,

which in turn leads to negligible involvement of unorganized players and thus a lower market size.

Globally, the top 10 companies dominate the market with more than 50% market share. However, APAC and

China remain fragmented with regional and international players co-existing in these markets. The Indian

paint market, unlike APAC and China, is an oligopolistic market with the top 4 players controlling a little less

than 70% market share of the overall domestic paint industry.

Exhibit 3: Industrial paints contribute >60% to the demand

globally….

Exhibit 4: ….as well as in APAC….

Architectural

39%

OEM and Special Purpose

(incl. general industrial, auto

oem, wood, protective,

marine etc). 61%

Decorative

36%

Industrial (incl. general

industrial, protective, powder,

wood, auto oem, marine etc).

64%

Source: Sherwin Williams investor presentation, Nirmal Bang Institutional Equities

Research

Source: Coatings World, Industry, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

4

Exhibit 5:… unlike in India where decorative paints have 75%

demand

Exhibit 6: Top 10 players have >50% share across the globe

Decorative

75%

Industrial (incl. automotive and

general oem, protective, powder

coatings etc.) 25%

Sherwin-

Williams

13%

PPG 11%

Akzo Nobel 7%

Nippon 4%

RPM 4%

Axalta 3%

BASF

3%

Kansai 3%

Asian Paints 2%

Jotun 1%

Other (>5,000

firms) 49%

Source: Company, Industry, Nirmal Bang Institutional Equities Research

Source: Sherwin Williams investor presentation, Nirmal Bang Institutional Equities

Research

Exhibit 7: APAC’s paint market is highly fragmented as

compared to…..

Exhibit 8: ….India’s market which is oligopolistic with top 4

players commanding nearly 70% market share

Nippon

8%

Akzo

Nobel

7%

Asian Paints

5%

Kansai 3%

KCC 2%

Sherwin-Williams 2%

Jotun 2%

Berger 2%

Axalta 2%

Others 55%

BASF, Noroo, TOA,Hempel,

SKShu, Carpoly, Chugoku

each have 1% share

Asian Paints

39%

Berger

Paints

12%

Kansai

Nerolac

11%

Akzo Nobel

6%

Others 32%

Source: PPG investor presentation, Nirmal Bang Institutional Equities Research

Source: Company, Industry, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

5

II. Constituents of the Indian paint industry

The domestic paint industry has grown at a rate of 10.4% from FY08, when the market was valued at

Rs159bn, to FY20, when the market size reached ~Rs520bn. Over the years, the decorative paint segment

(market share of ~75-80%) has grown at a CAGR of 11.4% against the industrial segment (market share of

~20-25%), which has grown at a CAGR of 7.9%.

Within the industry, the organized sector has been commanding ~70% market share and the balance 30% is

accounted by the unorganized sector. Till the first half of 2010s, the unorganized sector had ~35% market

share, but with demonetisation and implementation of GST, the organized players have been able to capture

market share from the unorganized players.

Exhibit 9: Indian paint industry has grown at 10.4% CAGR over 12 years

107 185 322 390

52

76

113

130

-

100

200

300

400

500

600

FY08 FY12 FY16 FY20

Decorative paint segment

(Rsbn)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

Exhibit 10: Contribution of decorative paints in the overall Indian paint industry has evidently

increased over the years

67 71 74 75

33

29

26

25

-

10

20

30

40

50

60

70

80

90

100

FY08 FY12 FY16 FY20

Decorative paint segment Industrial paint segment

(%)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

6

Exhibit 11: Paints industry in India

Decorative (75%-

80%)

Interior

Paints/emulsions

/enamels

Exterior

Paint/emulsions

/enamels

Distemper

Putty

Wood coatings

Cement paints

Primers and

thinners

Industrial (20%-

25%)

General Industrial

Automative

coating

Protective coating

Powder coating

Glass coating

Pipe coating

Niche segments

viz. coil, marine,

refinish coatings

Source: Company, Industry, Nirmal Bang Institutional Equities Research

A. Decorative paint industry in India

The decorative paint segment includes multiple categories depending on the nature of the surface like interior

wall paints, exterior wall paints, wood finishes, enamels as well as ancillary products like primers, putties etc.

Many factors have contributed to the faster growth of the decorative paint segment compared to the

industrial segment (and will continue to do so in the medium term). They include: (a) rapid scale of

urbanization and increase in nuclearization of families (b) rising disposable income (c) reduction in repainting

cycle (d) government boost for housing (e) upgradation and growth of top-end products and (f) slowdown in

the auto industry and infrastructure development in the recent years.

In s titu tio n a l E q u itie s

Paints Sector

7

Exhibit 12: Domestic decorative segment grows at 11.4% CAGR over the last 12 years

107

185

322

390

-

50

100

150

200

250

300

350

400

450

FY08 FY12 FY16 FY20

Decorative paint segment

(Rsbn)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

Interior/exterior paints/emulsions/enamels: Under the decorative paint segment, emulsion paints

(water-based paints) have been growing at a fast pace on account of their durability, washability and

superior aesthetics. Moreover, manufacturers have forayed into providing a wider choice to customers

with introduction of plastic, acrylic and textured emulsions, each having their unique properties to meet

the unique demand of the customers. Enamel paints (oil/solvent-based paints) can be used on a wide

variety of surfaces including metals, glass, wood and masonry surfaces, because of their hard, durable

and washable features.

Distemper: Distemper paints are water-based paints. They are also known as cement paints as they

can be applied directly on walls with plaster finish without using the primer. Considered as a better

version of whitewash, distemper paints are a cheaper option for emulsions and even last for more than 4

years. The major constituents of distemper are chalk, lime, water and some coloring pigments and are

available in powder and paste form. The distemper market, valued at ~Rs120-150bn, is highly

fragmented. The unorganized players’ share in distemper is substantially higher at 40-45% compared to

the overall share of the unorganized sector, which is at ~30% of the paint industry. Substantial increase

in the usage of distemper in smaller markets and market share gain from the unorganized sector have

boosted volume growth for the organized paint industry.

Putty: Putty, generally applied after primer, ensures smooth and even finish before painting and

increases longevity of the paint. Growing population, improving standard of living, rise in income levels,

changing lifestyles, rising urbanization and government’s infrastructure plans are some of the vital

factors driving growth of this product category. The putty market, valued at ~Rs50-60bn, is highly

fragmented as well. While preferred brands like UltraTech and JK Cement have the highest share,

followed by all four major paint companies, the share of the unorganized sector is still high.

Cement paints: Cement paints can be applied on the exterior as well as interior walls. It is essentially

applied on the exterior wall surface for preventing water penetration and reducing dirt collection. It is

suitable for coating concrete as well as decorating indoor and outdoor walls.

Wood coatings: These are primarily used on sidings, windows, doors, with stains and sealers used on

cabinets, furniture, flooring and decks, in order to increase durability, resistance to moisture and improve

aesthetics.

Primers and thinners: A primer (undercoat) is a layer of coating put on materials before painting to give

them a smooth finish by leveling out the surface. It ensures better adhesion of paint to the surface,

shields the material from paint and increases paint’s durability. Thinners are used to reduce the viscosity

of paint for its application. It is also used to clean painting equipment such as brushes, rollers and

containers used during painting.

In s titu tio n a l E q u itie s

Paints Sector

8

B. Industrial paint indutry in India

The industrial paint segment includes automotive and auto refinish coating, general industrial (GI) paints,

protective coatings, powder coatings and other niche segments like coil coatings, marine coatings etc. This

segment is dependent on business cycles and economic conditions. Growth of the industrial paint segment,

which accounts for 20-25% of the market, is highly dependent on the automotive sector. The auto sector has

been the leading consumer of industrial paints with 40-50% of the demand coming from it.

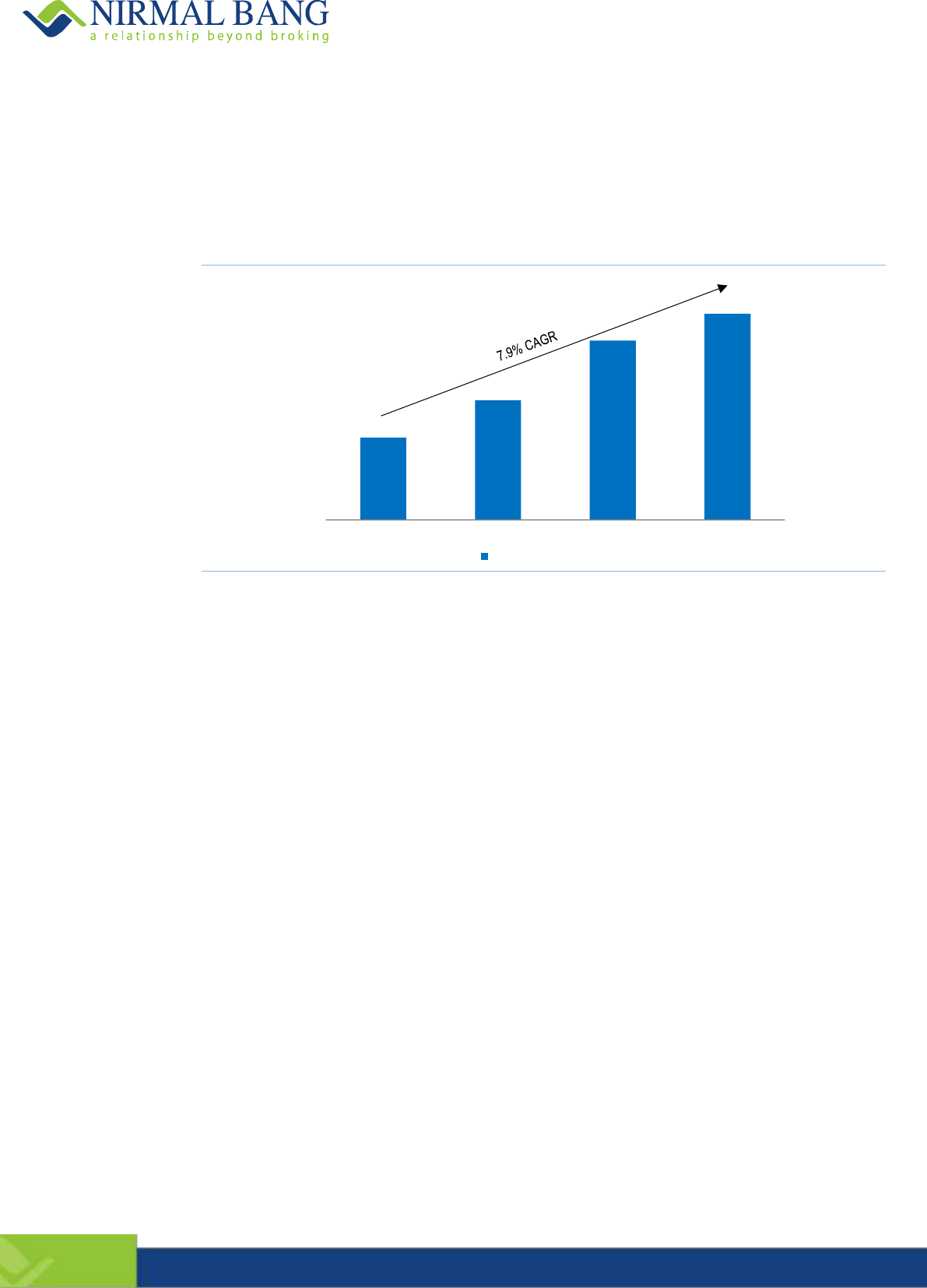

Exhibit 13: Domestic industrial paint segment grows at 7.9% CAGR over the last 12 years

52

76

113

130

-

20

40

60

80

100

120

140

FY08 FY12 FY16 FY20

Industrial paint segment

(Rsbn)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

Automotive and refinish coating: A direct function of the automotive industry of a country, the

automotive coatings segment has been facing challenging times due to the slowdown faced by the auto

industry over the last one and a half to two years. India’s automotive refinish market is valued at

~Rs20bn.

Due to automotive coating’s high contribution to industrial paints, there is direct positive correlation

between the growth of the auto industry and growth of industrial paints. During the 8-year period from

FY08 to FY16, when auto volumes grew at a CAGR of 9.8%, the industrial paint segment grew at a rate

of 10.2%. However, given the slowdown in the auto industry in the recent years, the 12-year auto

volume CAGR (from FY08-FY20) recorded at lower 6.9%, has in turn slowed down growth in industrial

paints during the same duration which was recorded at 7.9%.

KNPL is the leader in the automotive space and APNT is the leader in the auto refinish market.

GI coating: KNPL is the leader in the GI coatings category, which is used primarily for construction,

heavy engineering and agricultural equipment etc. Industrial coating space has been facing challenging

times on account of continued slowdown in overall investments in the manufacturing sector and tight

liquidity conditions for the small to mid-size companies

Protective coating: Protective coatings are thin layers of solid material applied to a substrate, with the

coating acting as a barrier to inhibit or prevent corrosion. BRGR is the leader in this category.

Powder coatings: Powder coatings are usually used for coating metals to prevent corrosion and for

finishing applications. They are superior to liquid coating as they are free from VOC (volatile organic

compounds) unlike liquid coatings. Powder coating is gaining increasing importance in the automotive,

furniture, appliances and others, as powders are an essential part of a construction that experiences

damage such as spillage, abrasion and exposure to dust, chemicals, heavy load and UV light. India’s

powder coating market is valued at ~Rs63bn. In powder coatings, KNPL is the leader followed by

BRGR.

In s titu tio n a l E q u itie s

Paints Sector

9

Exhibit 14: Auto sector slowdown in the recent years

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

2Ws 3Ws PVs CVs

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research

III. Rise in per capital consumption of paints

India’s per capita consumption of paints has increased at a CAGR of 7.0% over 7 years, from 2.6kgs in FY12

to 4.1 kgs in FY19. However, compared to the global average of ~13-15 kgs per capita consumption, India’s

per capita consumption of paints is far behind despite the huge size of the market. Thus, there is immense

headroom for the domestic market to grow in the long term given that structural drivers of the industry and

economy are in place.

Exhibit 15: India’s per capita consumption of paints far less

vis a vis global average

Exhibit 16: Growing per capita consumption in India

20+ 13-15 4

0

5

10

15

20

25

Developed countries Global average India

(kgs)

2.6 3.3 4.1

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY12 FY15 FY19

(kgs)

Source: Company, Industry, Nirmal Bang Institutional Equities Research

Source: Company, Industry, Nirmal Bang Institutional Equities Research

IV. Correlation of industry with GDP growth

In line with the global paint industry, growth of the domestic paint industry is closely linked to GDP growth.

The paint industry’s volume growth tends to be between 1.5x and 2x GDP growth. The strong positive

correlation between growth of the industry and GDP growth is a given since demand for paints tends to

follow overall economic activity, including income levels, industrial production and construction spending.

However, FY20 has been an exceptional year where the correlation has been relatively lower on account of

the Covid-19 pandemic hitting the industry towards the end of the year. Commenting on impact of Covid-19

induced lockdown on the industry, Mr. S Mahesh Anand, President, Indian Paint Association (IPA) stated

that “FY20 sales had been moderate and have ended flat, if not negative.”

In s titu tio n a l E q u itie s

Paints Sector

10

Exhibit 17: The industry’s value growth is positively correlated with the GDP growth

Source: Akzo Nobel India Presentation, Nirmal Bang Institutional Equities Research

Exhibit 18: Correlation of industry volumes with real GDP growth

12.1

14.8

14.5

15.5

12.2

11.8

12.0

5.5

6.4

7.4

8.0

8.3

7.0

6.1

2.2

2.3

2.0

1.9

1.5

1.7

2.0

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

0.0

3.0

6.0

9.0

12.0

15.0

18.0

FY13

FY14

FY15

FY16

FY17

FY18

FY19

Paint industry volume growth (%) Real GDP growth (%) Correlation (x)

(%)

(x)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

Exhibit 19: Correlation of industry volumes with nominal GDP growth

12.1

14.8

14.5

15.5

12.2

11.8

12.0

13.8

13.0

11.0

10.5

11.8

11.1

11.0

0.9

1.1

1.3

1.5

1.0

1.1

1.1

0.0

0.4

0.8

1.2

1.6

0.0

3.0

6.0

9.0

12.0

15.0

18.0

FY13

FY14

FY15

FY16

FY17

FY18

FY19

Paint industry volume growth (%) Nominal GDP growth (%) Correlation (x)

(%)

(x)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

11

Demand drivers of decorative segment

Exhibit 20: Decorative paints remain an attractive and high growth segment in the Asian markets

Source: Akzo Nobel N.V. presentation, Nirmal Bang Institutional Equities Research

I. Urbanization and nuclearization of families:

Industry’s long-term growth is attributable to many macro-economic and demographic factors, including rise

in gross household income, increasing urbanization and rising nuclearization of families.

Gross household income has been continuously increasing, albeit at a slower pace in the recent years.

Consequent to the rise in disposable income, consumer spends have also been rising. However, the

propensity to save (level of savings as a percentage of disposable income) has been gradually declining,

thereby reflecting consumers’ willingness to spend more than what they used to.

India’s urbanization trajectory has shaped well from 25.6% in 1990 to 34.5% in 2019 (34.9% 2020P). Rising

urbanisation, supported by real estate demand and improving infrastructure, have been boosting paint

demand. The UN expects ~40% of India’s population to reside in urban areas by 2030. Thus, even going

ahead, increasing urbanization will aid the growth of the decorative paint industry. Rising number of

households (on account of increasing nuclearization of families) has also been driving demand for housing.

Another factor that partially corroborates increase in housing over the years is the rise in home loans. As on

FY20, retail housing loans have grown at a 10-year CAGR of more than 16%, which shows consumer’s

growing aspiration to own a house.

While the real estate sector has seen a slowdown in the last two years and may continue to be under stress

in the near term, we believe that over the medium to long term the sector’s outlook is positive.

In s titu tio n a l E q u itie s

Paints Sector

12

Exhibit 21: Household disposable income has been increasing, although at a slower rate

26,638

30,107

34,606

39,150

47,084

53,716

62,052

67,083

75,930

85,746

93,680

1,02,847

1,14,261

1,26,049

1,41,946

12.3

13.0

14.9

13.1

20.3

14.1

15.5

8.1

13.2

12.9

9.3

9.8

11.1

10.3

12.6

0.0

5.0

10.0

15.0

20.0

25.0

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

Household disposable income % growth

(Rsbn)

(%)

Source: MOSPI, Nirmal Bang Institutional Equities Research

Exhibit 22: Propensity to save has been declining thereby reflecting increase in spends

7,637

8,690

9,944

11,183

13,309

16,390

17,493

20,656

22,353

22,853

24,391

24,749

27,871

32,773

34,468

15.8

13.8

14.4

12.5

19.0

23.2

6.7

18.1

8.2

2.2

6.7

1.5

12.6

17.6

5.2

28.7

28.9

28.7

28.6

28.3

30.5

28.2

30.8

29.4

26.7

26.0

24.1

24.4

26.0

24.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

Gross household savings % growth as a % of disposable income

(Rsbn)

(%)

Source: MOSPI, Nirmal Bang Institutional Equities Research

Exhibit 23: Percentage of population residing in urban areas expected to increase to 40% in 2030

25.6

27.7

30.9

32.8

34.9

40.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

1990

2000

2010

2015

2020P

2030F

Percentage of residing in urban areas

(%)

Source: MOHUA (Handbook of Urban Statistics 2019), UN, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

13

II. Value migration

The eminent players in the industry have been focusing on growing the bottom of the pyramid space, which

is far broader in terms of volume vis a vis the top-end and mid segments, through continuous new offerings

and focused advertising and marketing. Further, companies have been reiterating that while the premium

range continues to grow, the economy range (including emulsions, distempers and putties) have been

growing at a much faster rate. Increased awareness among rural households about applying lower/under-

coat (putty and primer) before applying final coat (distempers) has aided demand for low-end products. Paint

companies have been gaining market share from the unorganized players post regulatory reforms like GST

and have also resorted to competitive pricing to gain market share. Given that the presence of the

unorganized sector in the lower-end paint segment is much higher than the overall industry and general

growth in usage of paints, there is still headroom for paint companies to grow within the bottom of the

pyramid space.

Exhibit 24: Bottom of the pyramid offerings of APNT/BRGR/KNPL over the recent years

Source: Company, Nirmal Bang Institutional Equities Research

Putty: The putty market, valued at ~Rs50-60bn, is highly fragmented. While preferred brands like UltraTech

and JK Cement have the highest share, followed by all four major paint companies, the share of the

unorganized sector is still high.

Distemper: The distemper market, valued at ~Rs120-150bn, is also highly fragmented. The unorganized

players’ share in distemper is substantially higher at 40-45% compared to the overall share of the

unorganized sector, which is at ~30% of the paint industry. Substantial increase in usage of distemper in

smaller markets and market share gain from the unorganized sector have boosted volume growth for the

organized paint industry. This product is sold largely in the pre-Diwali period on account of higher demand

from the smaller towns/rural areas during the festive season.

Exhibit 25: Unorganized segment has a higher share in

distemper market vs….

Exhibit 26: ….. overall paints industry

Unorganized

40-45%

Organized 55-60%

Unorganized

30%

Organized 70%

Source: Company, Industry, Nirmal Bang Institutional Equities Research

Source: Company, Industry, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

14

III. Shortening of re-painting cycle over the last decade

Re-painting constitutes ~70% of the decorative segment demand in India and globally. While re-painting is a

function of various factors (including income levels, festive & marriage season and lifestyle improvement),

fresh construction is a function of improvement in real estate and infrastructure development, which depends

on the overall economic growth.

Re-painting cycle in India has reduced significantly from 7-8 years till early 2010s to 4-5 years now. Factors

that have influenced reduction in the re-painting cycle are: the rise in income levels, increase in number of

rented houses (where the owners prefer re-painting to attract tenants) and significant ease of the painting

process. The reduction of the re-painting cycle is despite the increase in the life of paints as consumers have

been giving importance to aesthetics, change in looks and appearance of their premises.

One of major issues impacting the timely repainting of homes was the hassle involved in the painting

process, including disruption to daily life, smell of fresh paint, cleaning after the painters left etc. To address

these issues, many companies have been successfully venturing into express painting services as well as

offering consultancies to their customers. These steps have led to the easing of the painting process as well

as avoidance of delay in the re-painting activity.

Exhibit 27: Mix of repainting and fresh painting in the global

market similar to…..

Exhibit 28: ….the mix in India

Fresh

painting 30%

Re-painting 70%

Fresh

painting 30%

Re-painting 70%

Source: Sherwin Williams investor presentation, Nirmal Bang Institutional Equities

Research

Source: Company,Industry, Nirmal Bang Institutional Equities Research

Exhibit 29: Re-painting cycle has reduced over the years; We do not expect any major reduction in re-

painting cycle further in the medium term

7-8 4-5

0

1

2

3

4

5

6

7

8

2010 2019

(yrs)

Source: Industry, Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

15

IV. Growing demand from smaller towns and rural areas

For the industry, metros and tier I areas contribute ~25% in value terms with the smaller towns (tier II/III/IV

cities) and rural areas contributing the balance 75%. For the past few years, demand in smaller cities and

towns has been growing at a faster pace than metro and tier I cities. Rise in disposable income, incremental

consumption expenditure, increase in awareness, development of rural markets and various launches have

fuelled the paint industry’s growth.

Paint companies have been proactively expanding their dealer base in newer geographies, especially tier

II/II/IV cities and rural areas, to ensure adequate presence. This has also led to some market share gain from

the informal sector. Further, many people have been entering the paint cycle, which has boosted growth in

these regions.

Even once the pandemic led lockdown was lifted, rural areas have been able to sustain demand on the back

of a good monsoon, good crop year, government support and lower penetration of the pandemic compared

to urban areas. Even in case of many smaller towns, demand has returned to pre-COVID levels. We have

highlighted management commentary of the top three players, showcasing the relatively better scenario in

smaller/rural markets in recent earnings call:

Management commentary from latest earnings call and interviews on demand scenario:

APNT:

Business picked up in tier II/III/IV cities where the demand conditions were better, while in metro and

tier I cities the business was slower.

Tier III and tier IV cities have outgrown metro and tier I cities.

Western region, including Mumbai and hinterlands, is far more affected. Across India, metros like

Chennai, Kolkata, Bengaluru and Delhi have been affected and tier I cities like Ahmedabad, Surat are

also affected.

Dealer expansion has happened in the months of May and June, especially in tier III and tier IV cities.

BRGR:

Upcountry and non-metro markets are witnessing a quick rebound with pent-up demand streaming in.

Specific micro-markets and regions such as the agriculture belts in North and Central India — that

include states such as Uttar Pradesh — and non-industry regions in Eastern India are doing well. In the

South, there is good demand from Karnataka.

Decorative paints, driven by repainting demand, are doing better, primarily in upcountry terrains. After a

washout in April, there was good demand in May and the same improved further in June. If the current

trend (in demand) continues, June 2020 will see us do better than last year and demand will be even

higher than pre-COVID levels.

There is a high probability of demand extending all the way up to July-September periods this year,

banking on agri-reforms and recovery in rural markets post a good monsoon.

KNPL:

Return of demand was better than expected and was driven by rural and small towns, partly attributable

to pent up demand and partly to regular demand.

Smaller towns across the country, except those in Western regions, have recovered. Recovery is the

highest in North, followed by East, then South and West.

V. Housing for all/affordable housing measures by the government has aided fresh painting

demand and will aid repainting demand in the future

The government has been pushing for affordable housing across the country. Certain measures taken by the

government in the recent years include:

Pradhan Mantri Awas Yojana - Housing for All (Urban) Mission was launched in 2015 to provide

housing for all in urban areas by 2022. As on CY19, 10.3mn houses were sanctioned and 3.2mn

houses were completed and delivered against the target of 20mn.

In line with the Housing for All mission, the Pradhan Mantri Awas Yojana Gramin aims at providing a

pucca house, with basic amenities, to all houseless people and those households living in kutcha and

dilapidated houses, by 2022. Of the revised target of constructing 40mn pucca houses across India by

2022, 15.4mn houses have been completed.

In s titu tio n a l E q u itie s

Paints Sector

16

Smart City Mission: Also introduced in 2015, this mission aims to promote smart cities that provide core

infrastructure, give a decent quality of life to its citizens, offer clean and sustainable environment and

apply Smart’ Solutions. One of the basic requirements of a smart city to sustain itself is housing without

which sustenance and further growth of a smart city will be limited. Unlike metros, these smart cities will

require good amount of affordable housing to cater to the large middle and lower-income population.

In September 2019, the government announced Rs100bn special window to provide last-mile funding

for the completion of ongoing housing projects that are not NPAs or facing bankruptcy proceedings

under NCLT.

Through budget 2020, the government increased the tax deduction limit on the home loan interest

component to Rs350,000 from Rs200,000 for housing units worth up to Rs4.5mn, which would boost

consumption.

These measures would provide boost to demand and supply of housing, in turn aiding growth of

concrete and paintable houses in India. In the next 4-5 years, these houses will enter the re-painting

cycle.

Exhibit 30: Progress of Pradhan Mantri Awaas Yojana as on CY19

Source: MOHUA, Nirmal Bang Institutional Equities Research

VI. Availability initiatives by company

All the eminent players in the decorative paint segment have been consciously and aggressively trying to

increase their distribution network in order to penetrate deeper into markets across India. Along with the

increase in urbanization and growing number of smaller towns and villages, the dealer universe, which

currently stands at an estimated 120,000-150,000 outlets, is expected to increase by ~10% every year. With

this growing number, companies have been proactively expanding their dealer base in newer geographies,

especially in tier II/II/IV cities and rural areas, to ensure adequate presence across the length and breadth of

the country.

Further, these companies have been moulding their product offerings as per evolving needs of the market

and consumers across various price points. Most players in the organized segment have been focusing on

growing the bottom of the pyramid space, which is far broader in terms of volume than the top-end and mid

segments, through continuous new offerings and focused advertising & marketing.

In s titu tio n a l E q u itie s

Paints Sector

17

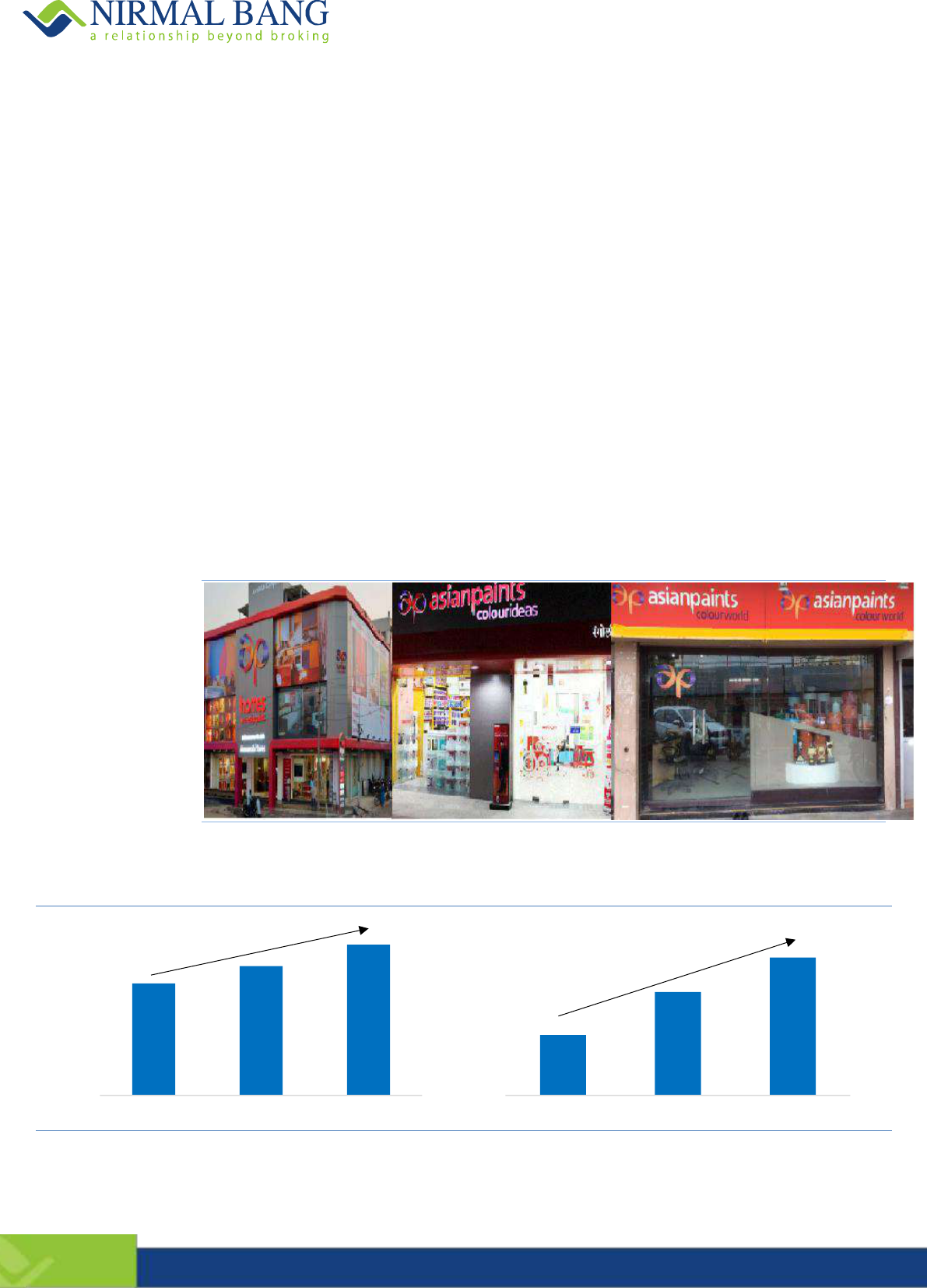

Exhibit 31: Number of dealers have grown along with…

Exhibit 32:…increase in number of depots for most companies

0

20,000

40,000

60,000

80,000

APNT BRGR KNPL

FY18 FY20

0

50

100

150

200

APNT BRGR KNPL

FY18 FY20

Source: Company, Industry, Nirmal Bang Institutional Equities Research

Source: Company, Nirmal Bang Institutional Equities Research; Note: For BRGR

FY19 no. of depots taken as annual report is not yet available for FY20

VII. Innovations, upgradation and growth in premium segment

While there is no linearity in upgradation of paints used by consumers, the industry has been witnessing

changes with regards to up-trading/premiumization over more than a decade including shift from-

Distemper to interior emulsion

Mid-segment to top-end segment

Low-end to top-end segment

Cement paint to exterior emulsions

Unorganized to organized in smaller towns, especially in tier III/IV cities and rural areas

Albeit metros and the tier I cities, even tier II cities to certain extent, have a relatively larger contribution to

the top-end product offering, smaller towns have been showing increasing interest for premium products as

well. This has come into play as consumers are now more aesthetically aware and also have the means to

opt for better value products, even at higher prices. Another factor that influences consumers to opt for

premium variants is cost of labour, which is largely inflexible at all levels and contributes significantly (~60-

70%), thereby making the choice of the paint variant relatively indifferent.

Further, paint companies have been launching products offering health centric benefits, like APNT’s Royale

Health Shield (anti-bacterial) and Royale Atmos (anti-pollution, air-purifying), BRGR’s Silk Breathe Easy

(anti-bacterial, anti-pollution), KNPL’s Impressions Eco Clean (anti-bacterial, fungal resistant). Currently,

there are fewer options available in the value added sub category and mainly in the premium price range but

with the increasing demand for these products, companies are likely to launch more specialized products.

Exhibit 33: Premium-end offerings of APNT/BRGR/KNPL over the recent years

Source: Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

18

Key players in the decorative space

I. Top 4 players

Asian Paints Ltd. (APNT): APNT is India’s largest paint company commanding over 40% of the overall

domestic paint industry and ~55% in domestic decorative paint industry. The company is present in 15

countries and has 26 manufacturing facilities across the globe. During FY20, the company generated

Rs202bn in revenue with ~84% contribution coming from its domestic decorative business. APNT strives to

be a holistic home décor company, from a conventional paint company, through its foray into the home

improvement space.

Berger Paints India Ltd. (BRGR): BRGR is India’s second largest paint company commanding ~12%

market share of the overall paint industry and over 20% market share of the domestic decorative paints

segment. On a consolidated basis, decorative paint segment contributes a bit over ~80% to the company’s

revenue, and the balance 20% is contributed by industrial paints. The company has 14 manufacturing plants

in India (6 outside India) with total capacity of ~609,247 KL. The company also caters to overseas markets

such as Nepal, Poland and Russia through its subsidiaries.

Kansai Nerolac Paints Ltd. (KNPL): KNPL, a subsidiary of Kansai Paints Co. Ltd. Japan, and has

completed 100 years of presence in India. KNPL is the leader in industrial paints in India (~45% of topline)

within which it is the leader in automotive coatings, general industrial coatings and powder coatings. In

decorative paints, KNPL is the third largest player in India (~55% of revenue). The company has

manufacturing capacity of 518mn litres across 6 plants in India and has another unit coming up at

Visakhapatnam in Andhra Pradesh. The distribution network comprises 27,500+ dealers and 104 sales

depots. The company has also acquired Marpol Pvt. Ltd. (powder coating) and Perma Construction Aids Pvt

Ltd (construction chemicals) and has filed for the merger of these companies with itself.

Akzo Nobel India Ltd.: The fourth largest player in the industry is present in decorative segment (~60%

contribution) and industrial segment (~40% contribution), including marine coatings, protective coatings,

powder coatings, specialty coatings and vehicle refinishes. The company's portfolio includes brands such as

Dulux, Interpon, Trinar, Resicoat, Wanda, Sikkens etc. AKZO has five plants, which are located at

Telangana, Karnataka, Madhya Pradesh, Punjab and Maharashtra. Presently, the company has 52 sales

depots. In the recent years, Akzo Nobel has ventured into adjacent categories of waterproofing through

‘Dulux Acquatech’ and woodcare through ‘Sadolin’. AKZO’s focus will continue to remain on its premium

paints portfolio along with innovation and renovation of its brand.

Exhibit 34: Top 4 players command more than 95% share in the organized decorative market

Asian Paints

55%

Berger Paints

20%

Kansai Nerolac

15%

Akzo Nobel

7%

Others

3%

Source: Industry, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

19

II. Other players

Shalimar Paints: Shalimar Paint Colour & Varnish Company was established in 1902 in Howrah, West

Bengal by two Britishers - A N Turner and A N Wright. Shalimar Paints has a pan-India sales and distribution

network. With 30+ depots, the company services more than 5,000 dealers across the country. Manufacturing

facilities are located at Howrah, Nashik, Shikandrabad and a fourth one is coming up in Chennai.

Nippon Paint India: Nippon Paint India, the domestic arm of the Japan-based company has been

operational in India for more than 10 years and produces coats for automotive, industrial and decorative

segments. Within the decorative space, which contributes ~55% to its topline, the company offers a range of

interior, exterior emulsions and enamel and is also into construction chemicals. Kerala, Karnataka, Tamil

Nadu and Andhra Pradesh are some of the markets where the company is faring well in the decorative

segment,

Indigo Paints: Indigo Paints started operations in 2000 and it is present across segments, such as interior

and exterior emulsion, enamels, wood coating, putty, primer and ceiling and floor coat. The Sequoia Capital

backed company has 33 sales depots across India. In 2019, Indigo Paints had planned to increase its

capacity by investing Rs400-500mn every year for five years towards all its three plants. Largely focused on

India's small towns (tier II/III cities), the company has recently entered bigger markets like Mumbai and Delhi.

Kamdhenu Paints: Kamdhenu Paints, launched in 2008, is the paint vertical of business conglomerate

Kamdhenu Ltd. Offerings include decorative paint products like exterior and interior emulsions, cement

paints, water and solvent based primers, acrylic distempers, enamels, wood finishes, textured to designer

finishes. The company has 31 sales depots and a network of 4,000 dealers. The company’s manufacturing

unit is located at Bhiwadi, Rajasthan.

JSW Paints: JSW Paints Pvt. Ltd., part of the US$13bn JSW Group, started the paint division in April 2019.

The company set up its first largest and fully-automated industrial coil coatings facility with an annual

capacity of 25,000 KL in Mumbai and decorative paints unit with 100,000 KL annual capacity at Vijayanagar

in Karnataka. Currently, the company’s products are available in the southern and western states of the

country. The company plans to scale up availability to pan-India by the end of FY21. It’s the only company

offering all water based decorative paints portfolio in the country.

Other paint companies in India with smaller presence are Jenson & Nicholson Paints Pvt. Ltd. (JNPL), Snowcem

Paints, Jotun Paints, etc.

In s titu tio n a l E q u itie s

Paints Sector

20

Foraying into adjacencies

I. Waterproofing and construction chemicals

Many paint companies have been entering into the waterproofing and construction chemicals space in the

past few years. Although there has been a significant shift in the last 10 years in terms of seriousness

towards waterproofing, which was otherwise looked upon as an added cost, the Indian waterproofing market,

valued at US$0.7bn-US$0.8bn is fairly underutilized compared to China’s US$22bn market. Thus, there is a

lot of headroom to grow in this segment in the next 15-20 years. So far, paint companies have been able to

cross-sell their waterproofing products through their existing dealer network. Going ahead, other channels

like hardware shops, cement dealers can be exploited.

Exhibit 35: Most companies have ventured into waterproofing and construction chemicals

Source: Company, Nirmal Bang Institutional Equities Research

II. Painting services

To reduce the hassle of the painting process faced by the end consumer, paint companies have taken steps

to make the process more organized by providing painting services. While APNT has been offering painting

services for many years, BRGR pioneered the concept of Express Painting. Following the Covid-19

outbreak, paint companies have taken appropriate measures and safety protocols for addressing the

paranoia felt by the consumer towards allowing outsiders (painters) into their premises.

Exhibit 36: APNT and BRGR have modified their painting services to ensure implementation of

adequate safety measures in response to COVID

Source: Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

21

III. Adhesives

The India adhesives and sealants market, valued at ~Rs90bn, is consolidated, with the top four players –

including Pidilite Industries, Henkel AG & Co, Sika, Bostik India, and H.B. Fuller - with an approximate

market share of 85%. During the past few years, along with construction chemicals, paint companies have

also entered into adhesives market, which would enable them to tap into the vast B2B and B2C channels

and also leverage their existing distribution network. Some paint manufacturers, though marginal players till

now, plan to expand their market share in adhesives and sealants market which may intensify competition in

the years to come.

Exhibit 37: Many companies have ventured into adhesives and sealants category

Source: Company, Nirmal Bang Institutional Equities Research

IV. Sanitizers and disinfectants

In the wake of the Covid-19 outbreak, many paint companies, including the leaders, have come up with a

range of sanitizers and disinfectants.

Exhibit 38: Sanitizers and disinfectants APNT/BRGR/KNPL

Source: Company, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

22

Raw material centricity

The industry uses over 300 raw materials in its manufacturing process. Major components involved in the

manufacture of paints include:

Resins (aka polymers/binders) that form the coating layer and hold the pigment in place

Pigments that impart colour and opacity

Solvents (aka thinner/vehicle) that dissolve or disperse different components used in the paint

formulation, making paint the desired consistency for application. Once paint is applied, the solvent

evaporates, allowing resin and pigment to produce a film of paint and dry rapidly.

Additives that are used to modify the properties of the liquid paint or dry film.

Exhibit 39: Crude oil and its derivatives form over 50% of the industry’s raw materials

Source: PPG investor presentation, Nirmal Bang Institutional Equities Research

Importance of crude prices

Over 50% of raw materials like phthalic anhydride, pentaerythritol, methyl methacrylate, aromatics, etc,

which act as resins, solvents and additives, are derivatives of crude oil, thereby making crude oil prices an

important indicator to track input costs. Further, since crude oil is a heavily imported commodity, fluctuation

in foreign exchange becomes another parameter to track.

Another way to look at the impact of volatility in crude prices on the profitability of a paint company is that it

acts as a natural hedge during economic downturn. This is on account of conjunction of global demand and

crude prices. We have seen that with outbreak of the Covid-19 pandemic, oil prices plummeted 50% due to a

drastic fall in demand across the globe. Thus, when demand is impacted, lower crude oil prices aid in

expanding gross margins.

Since mid-2000s, the Indian market, much like global markets, has been moving towards environmentally

compliant water-based paints from the solvent-based ones. In general, gross margins are better in water-

based paints compared to solvent-based paints as they are relatively less sensitive (water-based paints use

certain crude derived products in the manufacturing process) to movement in crude oil prices. In line with the

global trend, even consumers have been increasingly preferring water-based coatings on account of their

superior aesthetics, durability and washability. Although demand for oil/solvent-based paints is here to stay,

exposure to price fluctuations in crude oil can be reduced to a certain extent given that usage of water-based

coatings is increasing.

In s titu tio n a l E q u itie s

Paints Sector

23

Importance of titanium dioxide (TiO2).

Titanium dioxide pigment, derived from ilmenite, comprises ~20-25% of the total content of paint and is

commercially available in two forms – Anatase and Rutile. Rutile TiO2 is considered to be more durable and

stable and also more efficient in scattering light. Anatase pigments are used mostly in cheap dispersion

paints, self-cleaning paints and in road marking paints. Application of rutile pigments is much broader and in

practice covers all paint types. Around 70% of India’s domestic demand for TiO2 is met through import

deliveries and China is the leading exporter of TiO2 to India. Imports from China for APNT and BRGR vary

between 8% and 10% of total raw material cost. Companies have been finding alternative sources to reduce

exposure and volatility.

Exhibit 40: Paint companies to benefit from low crude prices

Exhibit 41: TiO2 prices have stayed stable in the recent months

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Aug-13

Feb-14

Aug-14

Feb-15

Aug-15

Feb-16

Aug-16

Feb-17

Aug-17

Feb-18

Aug-18

Feb-19

Aug-19

Feb-20

Aug-20

EUCRBRDT Index

($/bbl)

150

190

230

270

310

Aug-13

Feb-14

Aug-14

Feb-15

Aug-15

Feb-16

Aug-16

Feb-17

Aug-17

Feb-18

Aug-18

Feb-19

Aug-19

Feb-20

Aug-20

TiO2 (Rs/kg)

(Rs)

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 42: USD/INR volatility impacts input costs

Exhibit 43: India WPI Phthalic anhydride

50.0

55.0

60.0

65.0

70.0

75.0

80.0

Aug-13

Feb-14

Aug-14

Feb-15

Aug-15

Feb-16

Aug-16

Feb-17

Aug-17

Feb-18

Aug-18

Feb-19

Aug-19

Feb-20

Aug-20

USD/INR

0

20

40

60

80

100

120

140

160

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

India WPI Phthalic anhydride

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 44: Raw material as a % of sales change consequent to change in crude prices

57.9

60.2

59.0

58.3

56.9

56.4

55.3

57.6

58.5

56.3

62.7

63.6

61.5

60.6

58.6

58.5

56.9

58.3

61.0

58.5

67.4

68.6

69.6

69.1

68.0

62.9

58.5

60.4

63.8

61.7

86.7

114.4

110.5

107.6

85.7

47.5

49.0

57.6

70.2

60.9

-

20.0

40.0

60.0

80.0

100.0

120.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

APNT BRGR KNPL Brent Crude (Yearly avg.)

(%)

($/bbl)

Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

In s titu tio n a l E q u itie s

Paints Sector

24

Capacity expansion during the recent years

Asian Paints Ltd. (APNT): APNT, the leader in the decorative paints segment, has been continuously

investing in expanding its manufacturing footprint to serve customer demand. During FY16, the company had

expanded the installed capacity of its plant at Rohtak, Haryana from 200,000 KL to 4,00,000 KL. During

FY19, the company commissioned two large paint manufacturing units with an installed capacity of

300,000KL each, at Mysuru, Karnataka in September 2018 and Visakhapatnam, Andhra Pradesh in January

2019. The plant at Mysuru, Karnataka (scalable upto 600,000 KL) has been built with estimated investment

of Rs23.0bn and the plant at Visakhapatnam, Andhra Pradesh (scalable upto 500,000 KL) has been built

with an estimated investment of Rs17.9bn. With these two capacity additions, the company’s overall installed

capacity stands at 1.73mn KL per annum.

Berger Paints India Ltd. (BRGR): BRGR has been significantly ramping up its capacities in the last few

years to cater to the increasing demand. The company had commercialized its paint and putty plants at

Naltali, Assam in FY17, which has an annual capacity of 48,000 KL/MT of water-based paints, 24,000 KL of

solvent based paints, 14,000 MT of resin and 24,000 MT of wall putty. During the same year, the British

Paints division of the company had commenced commercial production of its distemper and putty

manufacturing facility in Nalbari, Assam with a capacity of 6,600 KL/MT and 7,200 MT per annum,

respectively. During FY19, the effective capacity of the Hindupur water-based plant was increased to

109,200KL and the first phase of emulsion plant with final capacity 44,160MT in Rishra was completed.

Installation of BRGR’s holistic coatings facility at Sandila Industrial Area, Uttar Pradesh at an estimated

investment of Rs2.5bn is on track for completion in 2021.

Kansai Nerolac Ltd. (KNPL): From 4 facilities in FY15 to 6 facilities as on FY20, KNPL has been

aggressively augmenting its capacity over the past few years to match the demand of its expanding product

portfolio. In FY19, KNPL commercialized the plant at Sayakha, Gujarat, and in FY20 it commenced

production at its manufacturing facility at Goindwal-Sahib, Amritsar, Punjab. Both these facilities have a

cumulative capacity of 75,800KL and estimated capex of Rs5.7bn. Work is currently in progress to set up

another manufacturing unit at Visakhapatnam in Andhra Pradesh, which is has a planned capacity of

60,000KL and an estimated cost of Rs3.0bn. As on FY20, the company has a manufacturing capacity of

518mn litres.

Exhibit 45: Number of manufacturing plants of the top 3 players as on FY15 vs FY20

6 9 49 13 6

0

2

4

6

8

10

12

14

APNT BRGR KNPL

FY15 FY20

Source: Company, Nirmal Bang Institutional Equities Research

Further, smaller companies have also been on a capex investment mode:

Shalimar Paints ramped up its capacity by 70,000KL with Nashik plant getting commercialised in 2019.

The newest entrant, JSW Paints, plans to expand capacity with an investment of Rs750mn. Currently,

the company has two plants - Mumbai, Maharashtra (25,000KL) and Vijayanagar, Karnataka

(100,000KL).

Akzo Nobel India invested Rs650mn in its sixth facility in India located in Thane, Maharashtra.

In 2019, Indigo Paints had planned to increase its capacity by investing Rs400-500mn every year for

five years across all its three plants.

In s titu tio n a l E q u itie s

Paints Sector

25

Key risks to the sector

The evolving nature of the Covid-19 pandemic makes near term predictability a challenge.

Considering Covid-19 to be a near term risk to the industry, medium term/long term outlook

remains positive due to structural opportunities as mentioned above. Companies have been

initiating services revolving around safe painting and have received positive response from many

consumers. However, reaction of consumers to the pandemic getting prolonged and consequent

restrictions/lockdowns is yet to be gauged. Further, timing of the return of migrant workforce to

support demand-generating sectors such as real estate and infrastructure development is

dependent on the longevity of the pandemic.

Sensitivity to crude prices and USD/INR exchange rates will remain an inherent risk to the sector

since crude (and its derivatives) and TiO2 are major to raw materials used in paints and are largely

imported.

Paint consumption is positively co-related to GDP growth and therefore a slowdown in GDP would

affect the industry directly. Also, paint being a discretionary spend item, there is a likelihood of

customers putting their paint requirements on hold for some time, thereby impacting renovation

demand.

The vagaries of the monsoon - extended monsoon in some regions and deficit rainfall in others –

affect demand from the rural sector, as an extended monsoon can reduce the number of dry days

before the festive season and deficit rainfall affects income.

Slowdown in infrastructure and construction activities would affect overall demand for paint

companies. Delay in the revival of the auto industry would continue to pose a threat to the growth of

industrial paints demand.

In s titu tio n a l E q u itie s

Paints Sector

26

Key highlights from recent channel checks:

APNT - an undisputed leader: Most of the dealers we spoke to stated that demand for the products of

APNT is undoubtedly higher than the other players. There is outright demand for other companies’

products as well, but not as high as APNT’s. Sale of newer entrant’s or smaller player’s products

requires efforts from the dealer’s end, in terms of convincing the contractor/painter as to why the

product is suitable for their need, which at times they’re not willing to take.

Inventory days: For most dealers, average inventory days hover around 10-15 days – 5-6 days for

APNT and 15-18 days for other companies. Further, order placed with APNT is generally fulfilled within

4-6 hours while for other companies it takes between 12-24 hours.

Preference for returns over margins: While a dealer earns lower margins on products of the market

leader compared to the higher margins offered by other companies, the return generated on account of

higher number of rotations is far ahead of what can be earned from products of other companies. Thus,

it is the return that dealers primarily look at rather than margins.

Rise in consumer awareness: Many dealers mentioned that for the past few years, demand is purely

dependant on the customer’s preference compared to earlier times when the dealer could easily

influence consumer’s decision. Painters and contractors are much more aware of the product’s features

and applications. That is why it is difficult for dealers to push any specific company’s brand/product.

Growth in top-end products as well as low end products: Dealers have stated that there is healthy

growth in premium products, especially value-added products like APNT’s Royale Shield and BRGR’s

Easy Clean. Across regions, there is high grown in bottom of pyramid products like distemper and putty.

Sale of Birla and JK Cement’s putty is much ahead of any other paint companies.

Negligible sale of sanitizers for Paint companies as of now: Some paint companies have been

pushing their dealers to buy sanitizers but there is hardly any pick-up as no consumer would go to a

paint or a hardware shop to buy sanitizers. Few dealers believed that companies need to advertise for

their sanitizers on a local level rather than national level.

In s titu tio n a l E q u itie s

Paints Sector

27

Comparison of top 3 paint companies in decorative segment

Exhibit 46: APNT has done well across majority of the parameters over the years

Parameter (consolidated)

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Net sales growth (%)

APNT

15.6

24.3

13.3

15.7

11.3

1.9

5.5

11.7

14.4

5.0

BRGR

23.8

25.9

13.5

15.6

11.7

-2.3

7.8

13.5

17.3

5.0

KNPL

24.8

22.1

10.4

11.0

12.7

7.5

7.6

14.9

16.4

-2.7

Gross margin (%)

APNT

42.1

39.8

41.0

41.7

43.1

43.6

44.7

42.4

41.5

43.7

BRGR

37.3

36.4

38.5

39.4

41.4

41.5

43.1

41.7

39.0

41.5

KNPL

32.6

31.4

30.4

30.9

32.0

37.1

41.5

39.6

36.2

38.3

Employee cost (% of net sales)

APNT

5.9

5.5

5.7

6.0

6.5

6.9

6.9

6.6

6.4

6.8

BRGR

6.1

5.6

5.6

5.8

5.9

6.5

6.7

6.9

6.7

7.1

KNPL

4.4

4.2

4.3

4.4

4.2

4.6

5.0

5.0

5.2

5.9

Ad spends (% of net sales)

APNT

4.4

4.3

4.7

5.0

5.3

3.9

4.1

3.9

4.1

4.5

BRGR

4.8

5.1

5.5

5.6

6.6

4.9

5.3

4.8

3.3

NA*

KNPL

3.9

3.9

3.7

3.7

4.3

6.3

6.9

6.1

5.1

5.2

EBITDA margin (%)

APNT

17.2

15.4

15.3

14.8

14.7

19.4

19.8

19.0

19.6

20.6

BRGR

10.7

10.3

11.1

11.1

11.8

15.4

15.8

15.6

15.4

16.7

KNPL

13.3

13.3

12.1

11.8

12.9

15.5

18.2

17.0

13.9

15.2

Adj. PAT margin (%)

APNT

10.9

10.3

10.2

9.8

10.2

12.6

12.9

12.1

11.2

13.4

BRGR

6.4

6.1

6.5

6.4

6.1

8.7

9.4

8.9

8.2

10.3

KNPL

9.9

8.5

6.3

6.7

7.8

9.7

12.6

11.0

8.3

9.9

EPS (Rs)

APNT

8.8

10.3

11.6

12.8

14.8

18.7

20.2

21.3

22.5

28.2

BRGR

2.2

2.6

3.2

3.6

3.8

5.3

4.4

4.7

5.1

6.8

KNPL

3.8

4.0

3.3

3.9

5.1

6.8

9.4

9.5

8.4

9.7

ROE (%)

APNT

43.3

40.1

36.3

33.1

32.4

31.9

27.5

25.5

24.1

27.6

BRGR

23.3

24.3

25.0

24.1

22.2

26.1

24.8

22.5

21.3

25.8

KNPL

24.4

21.8

15.1

15.3

18.1

17.8

19.1

17.3

13.8

14.5

ROCE (%)

APNT

42.3

36.5

33.8

31.3

29.7

29.2

24.9

22.5

22.8

26.3

BRGR

17.7

18.2

18.1

17.4

16.5

20.4

20.8

19.3

18.9

22.8

KNPL

21.9

20.2

14.2

14.6

17.5

17.4

18.8

17.0

13.5

14.2

No. of employees (standalone)

APNT

4,937

4,937

5,236

5,555

5,897

6,067

6,156

6,238

6,456

6,750

BRGR

2,446

2,431

2,464

2,607

2,666

2,808

2,993

3,130

3,450

NA*

KNPL

2,220

2,336

2,456

2,298

2,388

2,566

2,697

2,861

2,997

2,992

Sales/employee (Rsmn)

APNT

15.6

19.4

20.8

22.6

23.7

23.5

24.5

27.0

29.8

29.9

BRGR

9.6

12.1

13.6

14.8

16.2

15.0

15.2

16.5

17.6

NA*

KNPL

9.4

10.9

11.4

13.5

14.7

14.7

15.0

16.3

18.1

17.6

Source: Company, Nirmal Bang Institutional Equities Research

*Note: FY20 annual report of BRGR is not out yet

In s titu tio n a l E q u itie s

Paints Sector

28

Sector View

In recent times, growth in India’s paint sector has been an outlier in the overall domestic consumer space.

The industry has been witnessing a gradual shift in terms of consumer preferences from the traditional

whitewash to better quality paints. Besides, it is also witnessing healthy competitive environment, where

players are applying different strategies to tap the growing demand in the market for a larger regional share.

Additionally, rise in disposable income of the average middle class, urbanization, growing rural market,

shortening of repainting cycle, upgradation, increase in sale of premium-end products and launch of many

innovative products (like eco-friendly, odour free and dust & water-resistant paints) are the major drivers that

are pushing the growth of the organized paint industry. Within the Indian decorative paint segment, Asian

Paints (APNT) and Berger Paints (BRGR) are the two largest players with more than 80% of their overall

revenues coming from the segment and within the industrial paints segment, Kansai Nerolac (KNPL) is the

leader (segment contributes ~45% to its revenue).

The overall current environment for discretionary products hinges on opening up of markets. The demand

conditions for the paint industry has improved progressively since May’20 driven by demand in upcountry

markets. Companies remain confident of the demand conditions with secondary sales improving month-on-

month. In terms of regions, Tier II/III/IV cities are expected to continue to do well and even Metros and Tier I

cities are expected to bounce back both for decorative paints and other segments as well. From cost point of

view, key raw material prices are benign, this along with cost rationalization measures will aid margin in the

near term. In the medium term, faster growth in the premium products, operating leverage led efficiencies

and savings in logistics costs (with additions of capacities) will add to operating margins.

Since in the current environment there is a preference for businesses that are relatively more resilient, sector

multiples at current levels in near term will look expensive. We initiate coverage on APNT (Accumulate

rating) and BRGR (Sell rating), as we believe that decorative paints, in Indian context, will continue to

witness maximum demand within this space, majorly led by steady shift from unbranded/unorganized to

organized players with bigger players gaining further share. We also think that these are fundamentally

strong businesses within the domestic decorative space.

Exhibit 47: Revenue of FMCG companies under our coverage universe and top 3 paint companies of India

Revenue (Rsbn)

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Hindustan Unilever

175

194

217

252

274

302

305

313

339

377

383

Gillette India

7

9

11

12

14

17

20

20

17

17

17

Colgate-Palmolive (India)

20

23

27

32

36

40

39

40

42

45

45

Dabur India

34

41

53

62

71

78

78

76

77

85

87

Emami

10

12

15

17

18

22

24

25

25

27

27

Britannia

38

46

55

62

69

79

84

91

99

111

116

Nestle India

51

63

75

83

91

99

82

91

100

113

124

ITC

182

212

248

296

329

361

362

396

403

444

451

Marico

27

31

40

46

47

57

60

59

63

73

73

Total FMCG revenue

544

631

740

862

949

1,054

1,053

1,111

1,166

1,291

1,323

APNT

67

77

96

109

126

140

143

151

168

192

202

BRGR

19

23

29

33

39

43

42

46

52

61

64

KNPL

17

21

25

28

31

35

38

41

47

54

53

Total Paint revenue

102

121

151

170

196

218

223

237

266

307

319

Source: Company, Nirmal Bang Institutional Equities Research

Note: Nestle year ending is December, Gillete year ending is June

In s titu tio n a l E q u itie s

Paints Sector

29

Exhibit 48: Paint companies have grown nine out of ten times ahead of coverage FMCG companies

during the last 10 years

16.0

17.4

16.4

10.1

11.0

-0.1

5.5

4.9

10.8

2.4

18.6

24.2

12.8

14.9

11.6

2.0

6.3

12.6

15.3

3.7

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FMCG companies Paint Companies

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 49: Valuation of Indian companies vis a vis global companies

Company

Country

MCap

($ bn)

P/E (x)

EV/

EBITDA (x)