OFFICE OF

INSPECTOR GENERAL

DEPARTMENT OF THE TREASURY

WASHINGTON, D.C. 20220

August 24, 2012

OIG-CA-12-006

The Honorable Orrin G. Hatch

Ranking Member

Committee on Finance

United States Senate

SD-219 Dirksen Senate Office Building

Washington, DC 20510

Dear Senator Hatch:

This letter and its enclosures respond to your letters of October 18, 2011, and

January 18, 2012. In those inquiries, you asked the Council of Inspectors General

on Financial Oversight (CIGFO) to review the responses to inquiries that you made

to voting members of the Financial Stability Oversight Council (FSOC) in late July

and early August of 2011 regarding the debt limit.

Our response to your specific questions is provided as Enclosure 1. Your letters are

provided as Enclosure 2.

In preparing our response, we (1) obtained and reviewed relevant information and

documentation from the Department of the Treasury (Treasury) and (2) interviewed

Treasury officials including the Deputy Assistant Secretary for FSOC, the Deputy

General Counsel, senior counsel for the Treasury Office of Banking and Finance,

and the Director and Assistant Director of the Office of Fiscal Projections. This

work was performed by staff of the Treasury Office of Inspector General under my

direction. I shared a draft of this response with the members of CIGFO.

We are also sending a copy of this letter to the Honorable Max Baucus, Chairman,

Senate Committee on Finance. We would be pleased to brief you or members of

your staff on this response. If you have any questions, you may contact me at

Enclosure 1

Page 1

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

1. Determine whether Treasury was internally projecting, using its cash

projection models, that it would not have sufficient cash to meet all

projected incoming due obligations on July 28, 2011, or any day thereafter,

absent an increase to the debt limit.

We reviewed the Department of the Treasury’s (Treasury) daily cash balance

projections as of July 21, 2011, for the period July 28 through August 31,

2011. Absent an increase to the debt limit, our analysis of these projections

showed that a sufficient cash balance would not be available to meet all

incoming due obligations by August 11. Furthermore, we noted that the cash

deficit would grow with each day that the debt limit was not raised. The

projections assumed that investors would be willing to rollover existing debt

that came due during the period. As shown in the August 2, 2011, Daily

Treasury Statement, Treasury had an ending cash balance of approximately

$54 billion. According to Treasury officials, had investors not been willing to

roll-over debt securities, the cash balance could have been exhausted almost

immediately because a payment of $87 billion would have been needed to

pay maturing Treasury securities on August 4, 2011.

Treasury officials stated that prior to August 2, 2011, they were concerned

about how investors in Treasury securities might react if the debt limit was

not raised by that date. The specific concern was that if the government’s

borrowing authority were to expire on August 2, investors who ordinarily

would roll over maturing Treasury securities (that is, reinvest the proceeds of

maturing Treasury securities in new Treasury securities) might choose to

invest elsewhere.

Treasury’s daily cash balance projections are calculated by the Office of the

Fiscal Assistant Secretary (OFAS) and updated on a regular basis. These

estimates are based on (1) projected receipts, (2) projected cash outlays for

government operations, and (3) projected net cash flows from marketable

and non-marketable securities activity.

1

Treasury officials told us that daily

1

Marketable securities consist of Treasury bills, notes, bonds, and Treasury Inflation-Protected

Securities. After original issue by the Treasury, marketable securities can be bought and sold in the

Enclosure 1

Page 2

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

cash balance projections are inherently imprecise, as there are significant

variations in the amount of receipts and expenditures for any given day.

According to Treasury officials, the margin of error in these estimates at a

98 percent confidence level is plus or minus $18 billion for 1 week into the

future and plus or minus $30 billion for 2 weeks into the future.

2. Determine what Treasury’s daily cash balance projections and daily

projections of incoming due obligations were from July 28

th

through

August 30

th

, 2011.

We reviewed Treasury’s daily cash balance projections and daily projections

of incoming due obligations from July 28 through August 31, 2011, as of

July 21, 2011. Treasury makes these projections on a daily and monthly

basis. We were told that in the days leading up to the debt limit, OFAS ran

the daily projections multiple times per day as current information became

available. Furthermore, OFAS ran its daily projections under various policy

scenarios and finance assumptions. It should be noted that the monthly

projection we reviewed, which was run as of July 21, 2011, was predicated

on a resumption of borrowing on August 15. With that in mind, some

examples of daily cash balance point projections were as follows: $52.7

billion for July 28; $20.8 billion for August 4; -$0.8 billion for August 11;

and $56.5 billion for August 18. As discussed in our response item 1 above,

it should also be remembered that there are significant margins of error in

these point estimates.

financial marketplace, and ownership is transferable. Non-marketable securities, such as U.S.

Savings Bonds, are non-transferable securities issued by the government and registered to the

owner. They cannot be sold in the financial market, but they can be redeemed, subject to

restrictions. Other types of non-marketable securities include Domestic Series securities, Foreign

Series securities, Rural Electrification Authority securities, State and Local Government Securities,

and Government Account Series debt.

Enclosure 1

Page 3

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

3. On August 1

st

, was Treasury projecting (point estimate) that its operating

cash balance for August 2

nd

, 2011, would be below its projection of due

obligations in the absence of an increase in the statutory debt limit?

Based on our review of Treasury’s daily cash balance projections as of

July 21, 2011, for the period July 28 to August 31, 2011, Treasury’s

operating cash balance for August 2 would not be below its projection of

due obligations in the absence of an increase to the statutory debt limit. In

fact, based on the document we reviewed, Treasury’s estimated daily cash

balance was $69 billion and $65.6 billion on August 1 and August 2,

respectively. Furthermore, a Treasury official told us that Treasury’s daily

projection produced on August 1 showed that due obligations would not

exceed its operating cash balance for August 2. Another Treasury official

emphasized to us that Treasury had not stated that the government would

be out of cash on August 2, 2011. According to the official, Treasury stated

that the government would be out of borrowing authority on that date

absent an increase to the statutory debt limit. In this regard, Treasury

released statements on June 1 and July 1, 2011, where it announced, and

reiterated, that borrowing authority would be exhausted on August 2, 2011.

We also noted that Secretary Geithner had publicly emphasized this point as

well.

4. Determine whether there were contingency plans developed by FSOC voting

member agencies for disruptions that could have occurred if the debt limit

had not been raised and the federal government defaulted or if there was a

credit rating downgrade on the U.S.

According to the Treasury’s Deputy Assistant Secretary for FSOC, individual

FSOC members recognized the fiscal policy challenge, but there was no

collective initiative by FSOC to create an FSOC-directed/coordinated set of

contingency plans had the debt limit not been raised. He further stated that

although FSOC had conversations regarding the debt limit, creating such

contingency plans would be outside of FSOC’s authority. FSOC does not

interpret its statutory mandate to recommend fiscal policy. According to the

Deputy Assistant Secretary for FSOC, FSOC is charged with identifying risks

Enclosure 1

Page 4

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

and responding to emerging threats to financial stability. In this regard, FSOC

did identify and report the threat to financial stability if the debt ceiling was

not raised. The Deputy Assistant Secretary for FSOC further stated that it is

FSOC’s view that Congressional action was the clear response to the debt

limit.

Treasury, acting outside of its capacity as a FSOC member, considered a

range of options with respect to how Treasury would operate if the U.S. had

exhausted its borrowing authority. Treasury considered asset sales; imposing

across-the-board payment reductions; various ways of attempting to

prioritize payments; and various ways of delaying payments. We were told

that similar options had been evaluated by previous administrations during

debt limit impasses. That said, Treasury reached the same conclusion that

other administrations had reached about these options—none of them could

reasonably protect the full faith and credit of the U.S., the American

economy, or individual citizens from very serious harm. However, Treasury

officials told us that organizationally they viewed the option of delaying

payments as the least harmful among the options under review. Ultimately,

the decision of how Treasury would have operated if the U.S. had exhausted

its borrowing authority would have been made by the President in

consultation with the Secretary of the Treasury.

The following describes the various options that were under consideration.

Asset Sales

Treasury officials rejected the option of selling the Nation’s gold to meet

payment obligations because selling gold would undercut confidence in the

U.S. both here and abroad, and would be destabilizing to the world financial

system. With respect to the portfolio of mortgage-backed securities owned

by Treasury, Treasury officials concluded that a “fire sale” of these assets

would be adverse to the interest of taxpayers and could jeopardize the still

Enclosure 1

Page 5

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

fragile housing market.

2

Similarly, with respect to investments received in

connection with the Troubled Asset Relief Program, Treasury officials

determined that a “fire sale” of these investments would not maximize value

for the taxpayer and could be detrimental to the economy in general. For

both legal and practical reasons, Treasury officials determined that the sale

of the government’s portfolio of student loans was not feasible. Moreover,

even if Treasury had exercised these options, they would have bought very

limited time.

Across-the Board Payment Reductions

After reviewing various ideas for remaining within the debt limit by imposing

across-the-board payment reductions (such as cutting all payments by 40

percent or another amount necessary to remain within the debt limit),

Treasury officials concluded that such a payment regime would be difficult to

implement, as Treasury’s payment systems are not designed to make such

across-the-board cuts.

Prioritization of Payments

Treasury officials stated that Treasury also reviewed the idea of attempting

to prioritize the many payments made by the federal government each day.

Treasury noted that it makes more than 80 million payments per month, all

of which have been authorized and appropriated by Congress. According to a

2

The Housing and Economic Recovery Act of 2008 (HERA) authorized the Secretary of the Treasury

to purchase obligations and securities issued by the Federal National Mortgage Association (Fannie

Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Federal Home Loan

Banks. Treasury’s authority to make these purchases ended December 31, 2009. However,

Treasury was authorized to sell or otherwise exercise any rights received in connection with these

purchases, at any time. Under its HERA authorities, Treasury purchased and sold mortgage backed

securities guaranteed by Fannie Mae and Freddie Mac (these securities are referred to as “agency

MBS”). In total, before its purchase authority expired, Treasury acquired $225 billion of agency

MBS. Treasury started to sell its agency MBS in March 2011. As of July 2011, Treasury’s reported

its agency MBS portfolio holdings were $82.9 billion. On March 19, 2012, Treasury announced the

completion of its sale of remaining agency MBS and reported that overall, cash returns of

$250 billion were received from the agency MBS portfolio through sales, principal, and interest.

Enclosure 1

Page 6

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

Treasury official, the payments cover a broad spectrum of purposes deemed

important by Congress. While Congress enacted these expenditures, it did

not prioritize them, nor did it direct the President or the Treasury to pay

some expenses and not pay others. As a result, Treasury officials determined

that there is no fair or sensible way to pick and choose among the many bills

that come due every day. Furthermore, because Congress has never

provided guidance to the contrary, Treasury’s systems are designed to make

each payment in the order it comes due.

Delay of Payments

Treasury officials told us that it was the Department’s organizational view

that the least harmful option available to the country at the time, of these

very bad options, was to implement a delayed payment regime. In other

words, no payments would be made until they could all be made on a day-

by-day basis. Even under this option, Treasury officials acknowledged that,

because the U.S. operates at a deficit, payment delays under such a regime

would have quickly worsened each day the debt limit remained at its limit,

potentially causing great hardships to millions of Americans and harm to the

economy.

5. Provide any contingency plans identified in number 4 above.

As discussed in the response to number 4 above, there was no collective

initiative by FSOC to create contingency plans had the debt limit not been

raised. That said, Treasury officials did develop various options and

scenarios, and seemed to be settling in on a delayed payment regime.

However, we were told that there was never a final plan that was presented

to the President for approval. Accordingly, based on their description of

these documents, we considered them to be pre-decisional, working drafts

of options or scenarios, and therefore have no contingency plans to offer.

6. Determine whether the FSOC met its statutory mandate for collective

accountability for identifying risks and responding to emerging threats to

Enclosure 1

Page 7

Response by the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Request for Information Regarding the Debt Ceiling Issues of 2011

financial stability and whether the FSOC reported on systemic risks

surrounding the debt limit impasse.

Based on our review of the applicable sections of the Dodd-Frank Wall Street

Reform and Consumer Protection Act (Dodd-Frank Act) and other relevant

documentation, we concluded that FSOC met its statutory mandate for

identifying, responding, and reporting on emerging threats and systemic risks

to the U.S. with regard to the debt limit impasse.

As mandated by Section 112 of the Dodd-Frank Act, the purpose of FSOC is

“to identify risks that could arise from the material financial distress or

failure, or ongoing activities, of large, interconnected bank holding

companies or nonbank financial companies, or that could arise outside the

financial services marketplace… [and] to respond to emerging threats to the

stability of the United States financial system.” Section 112 also requires

FSOC to annually report and testify to Congress on, among other things,

“potential emerging threats to the financial stability of the United States.”

According to Treasury’s Deputy Assistant Secretary for FSOC, FSOC met its

statutory responsibility in its 2011 Annual Report, where it highlighted the

clear need for the debt limit situation to be addressed. The official noted that

the risk to financial stability posed by a failure to raise the debt limit is

different than other risks to financial stability, as the ability to eliminate the

risk is entirely within the control of the U.S. government. If Congress had

not raised the debt limit, it was the view that this would have inflicted

significant harm on the U.S. and its citizens.

Enclosure 2

Page 1

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Contents

October 18, 2011, letter from the Honorable Orrin G. Hatch ............................ 2

to Inspector General Thorson

Attachment A: July 27, 2011, letter from the Honorable Orrin G. Hatch ................. 9

to members of the Financial Stability Oversight Council

Attachment B: July 29, 2011, letter from the Honorable Orrin G. Hatch ................. 12

to members of the Financial Stability Oversight Council

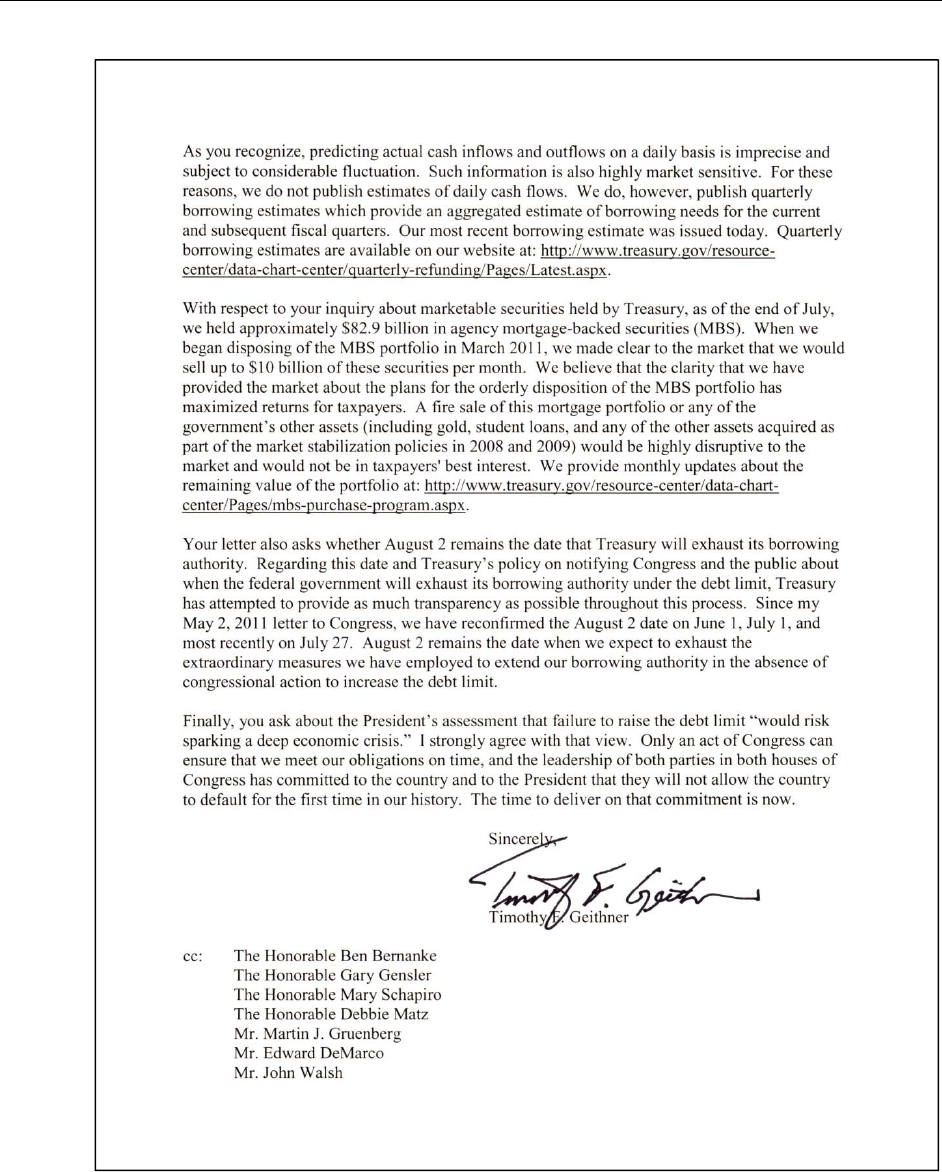

Attachment C: August 1, 2011, letter from Secretary of the Treasury Geithner ....... 13

to the Honorable Orrin G. Hatch

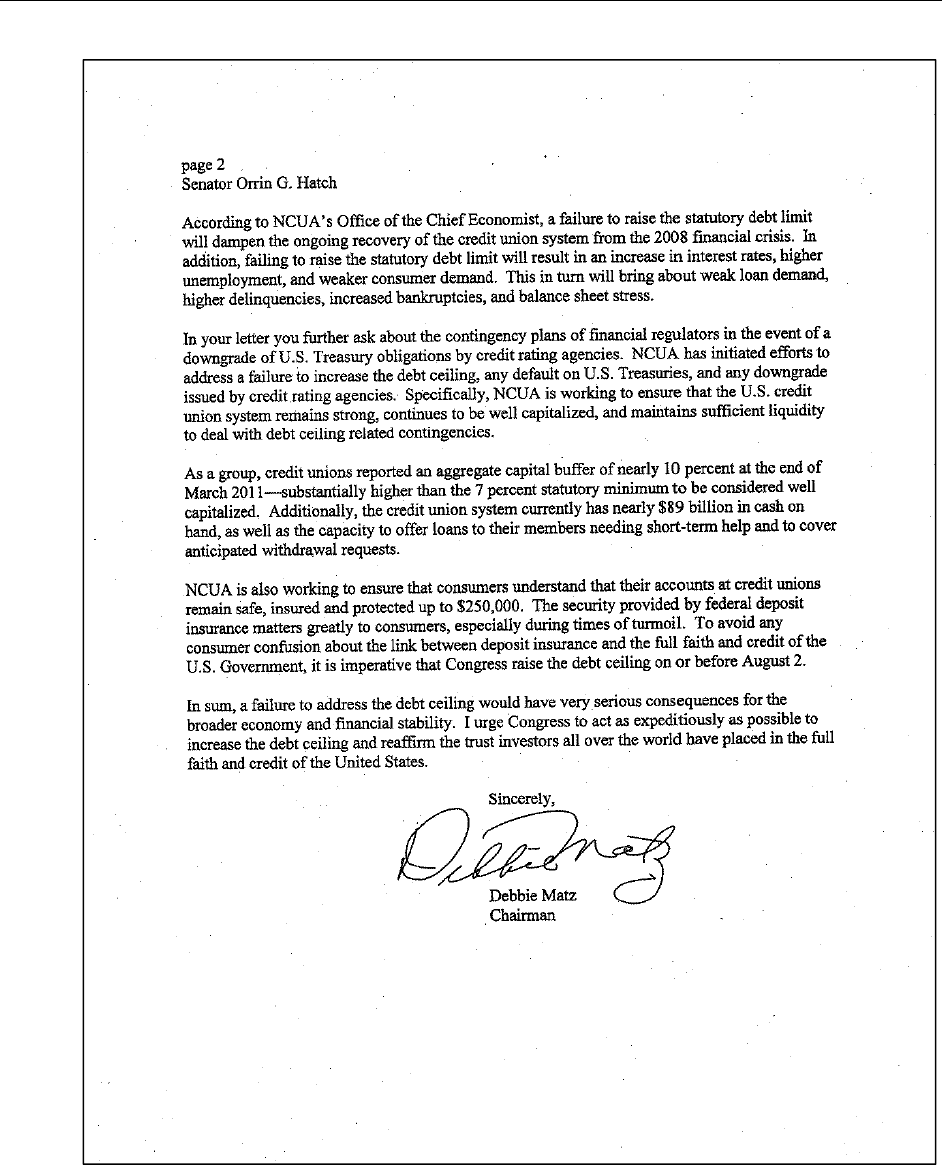

Attachment D: July 28, 2011, letter from Chairman Matz, National Credit Union ..... 15

Administration to the Honorable Orrin G. Hatch

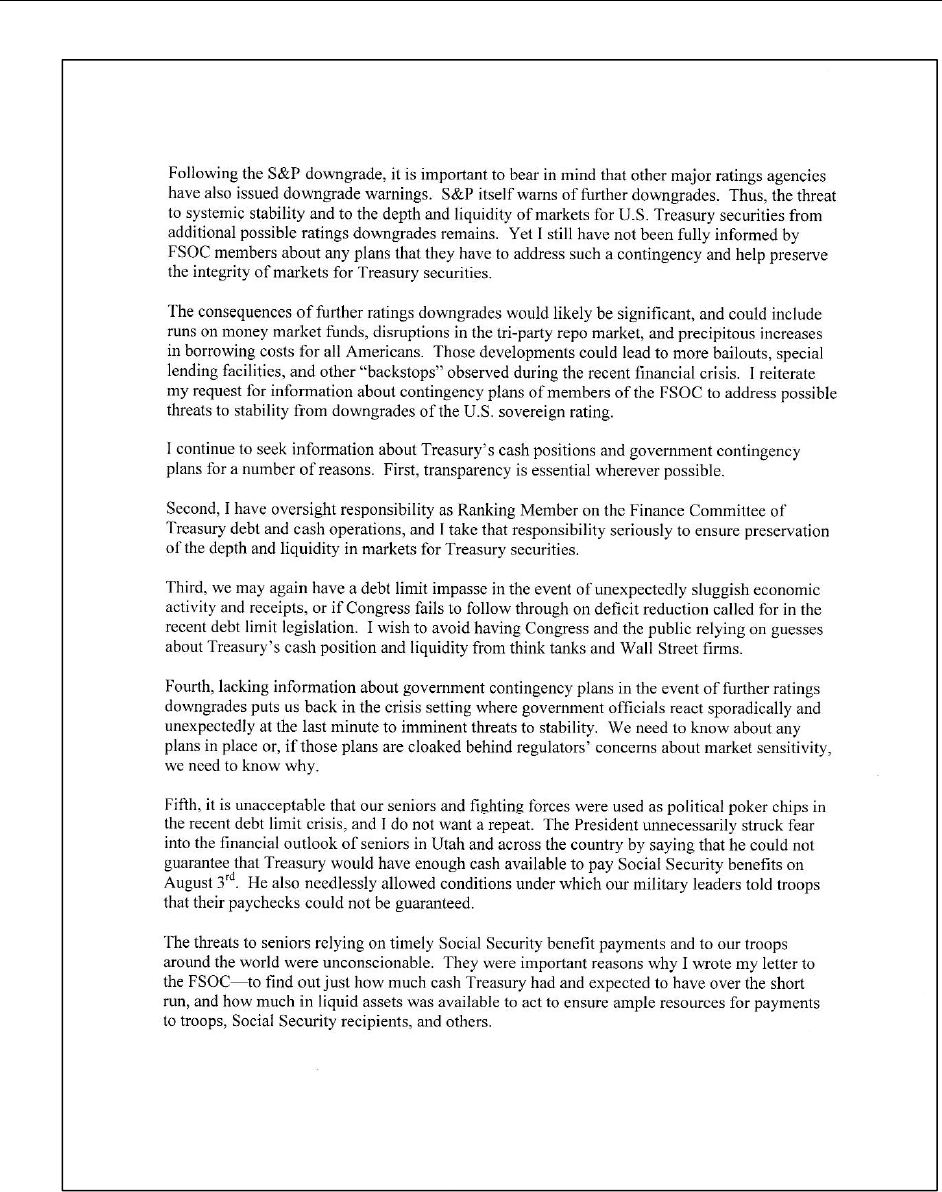

Attachment E: August 11, 2011, letter from the Honorable Orrin G. Hatch ............. 17

to Secretary Geithner

Attachment F: September 23, 2011, letter from Secretary Geithner ....................... 21

to the Honorable Orrin G. Hatch

January 18, 2012, letter from the Honorable Orrin G. Hatch ............................ 23

to Inspector General Thorson

Enclosure 2

Page 2

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 3

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 4

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 5

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 6

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 7

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 8

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 9

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 10

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 11

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 12

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 13

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 14

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 15

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 16

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 17

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 18

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 19

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 20

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 21

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 22

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 23

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury

Enclosure 2

Page 24

Letters to the Chair of the Council of Inspectors General on Financial Oversight

and Inspector General of the Department of the Treasury