Thomson Reuters Institute

Suspicious Activity

Reports Surge: 2023

Filings Expected to Set

Another Record

A deeper dive into the data

Contents

Introduction 3

Background: SARs and FinCEN 6

High-Level Findings and Trends 8

Seasonality 14

2023 SAR Prediction 16

Human Exploitation 17

Online Child Exploitation 21

Fraud 22

Supporting Criminal Data 27

Elder Financial Exploitation 29

Pandemic-related Fraud and

Suspicious Receipt of Government Payments. 32

Selected Industries and Terror Financing 33

International Comparisons 39

Takeaways and Closing Thoughts 40

© Thomson Reuters 2023

Suspicious Activity Reports 2023 3

Introduction

Financial institutions in the United States have reported soaring volumes of suspicious

nancial activity to U.S. anti-money laundering (AML) authorities over the past

three years.

Disruptions from the global pandemic created unique opportunities for nancial crime,

particularly fraud schemes involving checks, government benet payments, and investment

accounts. Vulnerable populations have grown in both size and susceptibility, especially

among migrants and the elderly, forming a target-rich environment for

threat actors.

In 2022, Financial institutions submitted more than 3.6 million Suspicious Activity Reports

(SARs) to the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN). SAR lings in

March 2023 set a monthly record, with more than 351,000 reports.

Based on data from the rst quarter of 2023, this year is likely to set additional records.

Since suspicious activity reporting became fully electronic in 2012, total SAR volumes had

increased modestly but steadily until approximately 2019, before spiking dramatically in

2020, 2021, and 2022.

Potential non-criminal drivers

Accelerated SAR lings may not necessarily correlate to symmetrical increases in actual illicit

activity. Rather, as the name implies, suspicious activity reports indicate that a nancial rm

detected and alerted authorities to customer activities known to suggest links to crime. A

rapid SAR-ling tempo may be driven by a variety of potential factors.

Several causes likely explain the surge in SAR lings, including heightened regulatory

pressure, enhanced threat awareness or detections by rms, and pandemic-related changes

such as proliferation of government programs and the rapid, widespread adoption of

mobile banking.

‘Defensive’ SAR ling

Additionally, the spike in reporting could be attributed to defensive ling, a widely recognized

practice in which rms apply overly broad detection criteria to minimize their own risk. While

© Thomson Reuters 2023

Suspicious Activity Reports 2023 4

aiming to preempt regulatory scrutiny, however, defensive ling produces a higher proportion

of SAR lings that unhelpfully point to legitimate activity.

Firms see a clear cost-benet equation here: Submitting a thinly substantiated SAR carries

no regulatory risk – whereas failing to report suspicious activity can attract signicant

enforcement action and painful penalties.

Key trends

While the sharp rise in SAR lings spanned virtually all categories of illegal activity, this

special report highlights key trends, which are supported with additional data.

Growth in suspected fraud linked to government programs likely stemmed from the

extensive, documented abuse of pandemic relief programs. Increases in suspected human

exploitation appear to reect heightened awareness by nancial institutions, owing to

recent alerts from the U.S. Treasury Department and outreach from non-governmental

organizations. Additionally, elder nancial abuse gured prominently in SARs data, also likely

reecting pandemic-era societal shifts that exposed seniors to new threats.

Correlation to crime

Considerable evidence, backed by expert consensus, indicates that elevated suspicious

activity reporting does reect a genuine increase in certain types of criminal activity.

Technological developments and documented increases in certain crime categories, including

identity theft and online fraud, are also likely contributors.

SARs related to check fraud have soared over the past three years, FinCEN data shows.

Contemporaneous statistics from the Federal Bureau of Investigation (FBI) demonstrate a

similar increase in reported fraud cases, particularly in the online domain, which suggests

that fraud is rising at an alarming rate.

The following report provides a user-friendly analysis of SAR-ling trends in critically

important areas, such as check fraud, human exploitation, and elder abuse. Data is presented

showing important annual and monthly trends.

SAR program background

Between 2000 and 2013, FinCEN published semi-annual SARs activity reviews, each

containing a detailed analysis of suspicious activity patterns and other nancial intelligence

insights, including from investigations by federal, state, and local law enforcement agencies.

Those reviews ended in 2013. Since 2017, FinCEN has maintained a comprehensive SAR

database on its public website

1

, which is updated monthly and includes tools for

data interrogation.

1

FinCEN’s SARs Database is available at https://www.ncen.gov/reports/sar-stats.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 5

SAR ling requirements became even more granular when Congress passed the Anti-Money

Laundering Act of 2020, requiring rms to report emergent threat typologies, such as money

laundering and terrorism nancing patterns and trends.

In January 2021, FinCEN began publishing Semi-Annual Trend Analyses, ve of which have

been issued to date

2

. Each analysis covers a single issue in detail, unlike the 2000-2013 SAR

Activity Reviews, which covered multiple issues in less detail. The new trend reports examine

unique threats such as ransomware, wildlife trafcking, Russian oligarchs, and business

e-mail compromise.

Methodology

This report relies on data from January 2014 through March 2023, obtained from FinCEN’s

online SAR stats database. All suspicious activity categories were included in our analysis,

as were all products, relationships, and specic regulators. To assess the broadest possible

dataset, no categories were omitted.

Monthly and annual SAR data was ltered by industry, suspicious activity designation, and

ling volume for specic periods.

To simplify data presentation and enhance relevancy, this report aggregates depository

institutions, money service businesses, and loan/nance companies into a single “nancial

institutions” group. Firms in the securities and futures sector, however, were segregated into

a separate group, because their regulatory regimes are sufciently unique to justify their

own category.

Additionally, all four gambling-related categories were combined into a generic “casino

industry” group. SARs originating from FinCEN’s “other” industry category were included in

the aggregate data but were not subject to additional analysis.

With regards to the total number of SARs led, it should be noted that an individual SAR

may describe multiple, separate suspicious activities. This report examines those underlying

designations to maximize granularity and context.Additionally, this document includes

information on threat indicators (or “red ags”) derived from ofcial alerts and warnings. Red

ags help rms better identify and report suspicious transactions.

The data and ndings presented throughout this report can be used for budgeting and

planning purposes. For example, monthly data reveals seasonal ling trends. Such

information is a valuable resource for corporate compliance, risk, and legal departments.

It may also be useful for AML, sanctions, and nancial crime units within nancial rms,

particularly for comparison purposes and presentations to senior management or boards

of directors.

2

FinCEN’s Financial Trend Analysis is available at https://www.ncen.gov/resources/nancial-trend-analyses.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 6

Background: SARs and FinCEN

SARs led with FinCEN are important tools to help monitor nancial activity that is unusual,

may reect a precursor or derivative of illegal activity, or might threaten public safety.

FinCEN collects and analyzes information about nancial transactions to combat domestic

and international money laundering, terrorism nancing, and other nancial crimes. It is

the single ling point for SARs and is responsible for distributing that information within

the government. FinCEN is also responsible for analyzing this information and producing

intelligence products useful to investigators, regulators, and the banking industry.

The suspicious activity reporting system was established to help authorities and nancial

institutions ght nancial crime by producing a continuous ow of data about potentially

serious activity between depository institutions and federal nancial supervisory agencies,

such as the Federal Reserve Board, Ofce of the Comptroller of the Currency, Federal Deposit

Insurance Corporation, National Credit Union Administration, FinCEN, and law enforcement

agencies throughout the United States.

Financial institutions are obligated to le a SAR when they detect a suspicious transaction

or activity by an identiable, individual involving at least $5,000, and lacking an apparent

lawful purpose, or when there is reason to suspect the funds were derived from

illegal activities.

SARs are a tool provided under the Bank Secrecy Act (BSA) of 1970. Originally called a

“criminal referral form,” SARs became the standard vehicle for reporting suspicious activity

in 1996. The USA PATRIOT Act of 2001 expanded SAR-ling requirements to help combat

domestic and global terrorism.

Failure to detect and report suspicious nancial activity can result in signicant enforcement

action and penalties.

The ow of such information can have life-and-death implications. SARs enable law

enforcement agencies to uncover and prosecute signicant money laundering, fraud,

terrorism, and other illegal operations.

When are SARs required?

Most commonly, FinCEN requires rms to le a SAR within 30 days of detecting customer

transactions featuring details that indicate potential money laundering, terrorism nancing,

Failure to detect and report suspicious nancial activity can result in signicant

enforcement action and penalties

© Thomson Reuters 2023

Suspicious Activity Reports 2023 7

or violations of the BSA. If more evidence is needed – such as the identities of transacting

parties – an extension not exceeding 60 days is available. Firms must retain SARs for ve

years after the date of ling.

What institutions must le SARs?

Many types of nancial rms are subject to SAR-ling requirements, including banks and

credit unions, stock and mutual fund brokers, and various money service businesses, such as

check-cashing companies and money-order providers. However, casinos, dealers of precious

metals and gems, insurance companies, and mortgage businesses are also subject to the

BSA, and thus are required to le SARs.

Condentiality is key

The effectiveness of reporting suspicious activity relies in part on condentiality. At no time

may a person under investigation be notied about a SAR ling. Additionally, it is a federal

criminal offense to disclose SAR contents to outside parties, such as news organizations.

When a bank or nancial institution reports suspicious activity, they are required to ensure

the information provided is reviewed at multiple stages by internal investigators, company

management, and legal counsel before nalizing the SAR. Special privileges protect

those who submit SARs, whether on a company’s behalf or as a private individual. The

submitting party is not required to disclose their identity, and they are immune to legal

discovery processes.

All reporting entities receive immunity for statements made in the SAR.

How are SARs Filed?

SARs are submitted through FinCEN’s electronic ling portal. The digital system facilitates

data standardization and increased efciency which are critical in situations involving public

safety concerns.

Figure 1: SAR Filings Must include Five Sections of information:

•

I

dentifying information: Names, addresses, social security numbers, birth dates,

driver license or passport numbers, occupations, and phone numbers of all

parties involved.

•

I

ncident data: Dates and suspicious activity codes.

•

I

nstitution name: The rm where the suspicious activity occurred.

•

I

nstitution contact: Contact details for the reporting rm.

•

I

ncident narrative: A written description of the suspicious activity, providing a

narrative to the data.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 8

High-level Findings and Trends

FinCEN received reports from more than 260,000 registered nancial institutions and other

e-lers in 2022, according to its latest annual review

3

. The review provides valuable insight

into the data cited in this report, and it should be noted that apparent differences between

this report and FinCEN’s annual publication stem from our consolidation of ling entities by

industry, as well as our disaggregation of suspicious activity designations in SARs containing

multiple entries.

We have attempted to present the data in a reader-friendly manner. In most cases, the

infographics tell much of the story, but in some areas, we have included additional analysis

and context.

FinCEN’s Year in Review for 2022 revealed some astonishing statistics, which we have

highlighted below. Note that FinCEN’s statistics differ slightly from ours, due to FinCEN

operating on a governmental scal-year basis rather than our calendar-year methodology.

3

Financial Crimes Enforcement Network (FinCEN) Year in Review for FY 2022; April 2023. Available at https://www.ncen.gov/sites/default/les/shared/

FinCEN_Infographic_Public_2023_April_21_FINAL.pdf

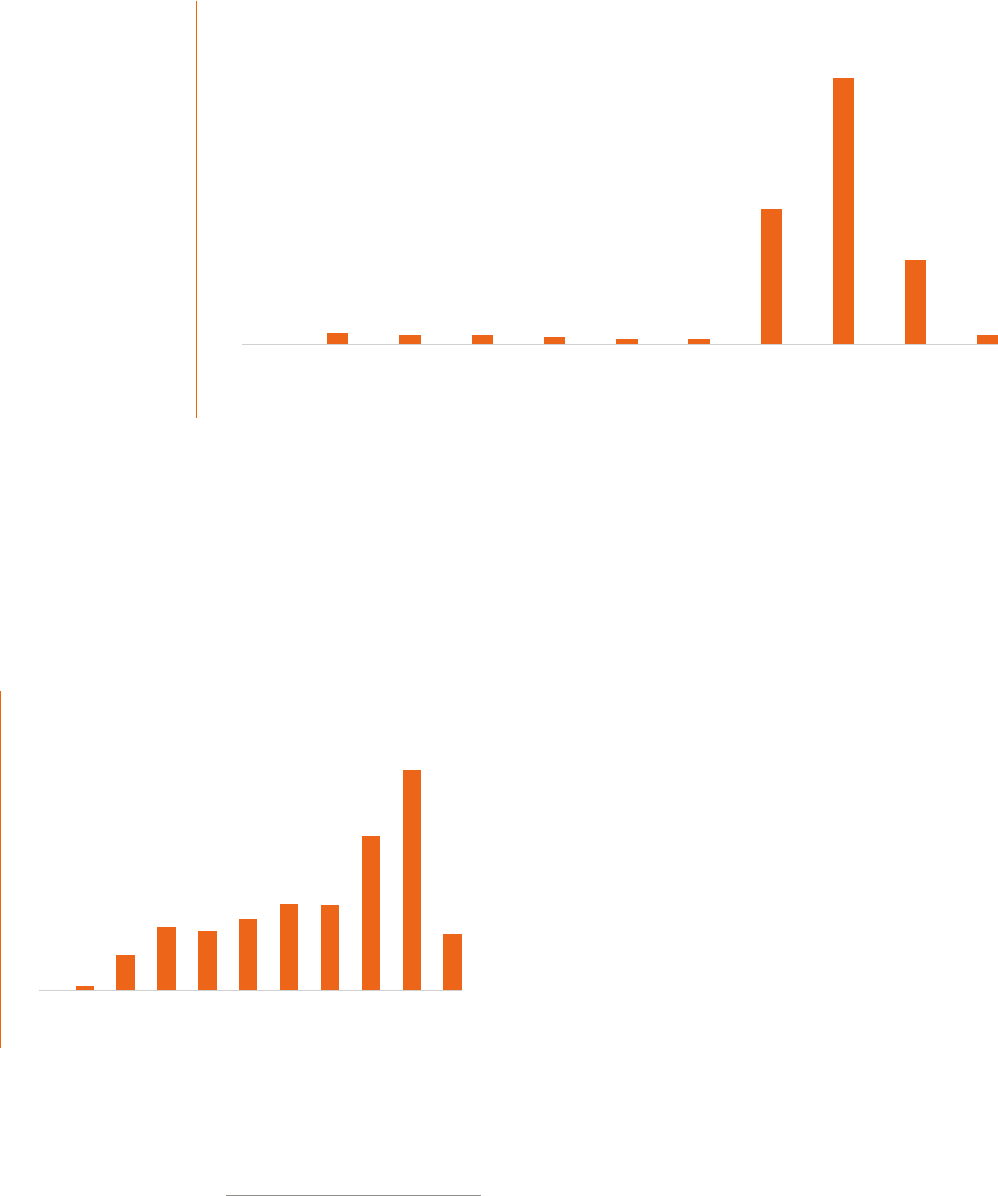

Figure

2: Total SARs Filed (all industries)

0

500,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1,659,123

1,812,665

1,975,638

2,034,406

2,171,173

2,301,163

2,504,509

3,069,450

3,616,450

938,444

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

0

* 2023 Stats include Jan-March filings

Figure 2: Total SARs Filed (all industries)

© Thomson Reuters 2023

Suspicious Activity Reports 2023 9

Figure 3: Notable SAR stats:

• Approximately 3.6 million SAR forms were submitted in 2022, or almost 10,000

reports per day

• The top-10 SAR lers submitted approximately 52% of all SARs in scal 2022

• Depository institutions and money services businesses (MSBs) led the vast

majority (85%) of all SARs

• Law Enforcement and other authorized users conducted more than 2.3 million

queries of FinCEN data in 2022

• More than 14,800 nancial institutions shared data with law enforcement agencies

• More than 7,600 nancial institutions participate in 314(b) information sharing

(bank to bank)

© Thomson Reuters 2023

Suspicious Activity Reports 2023 10

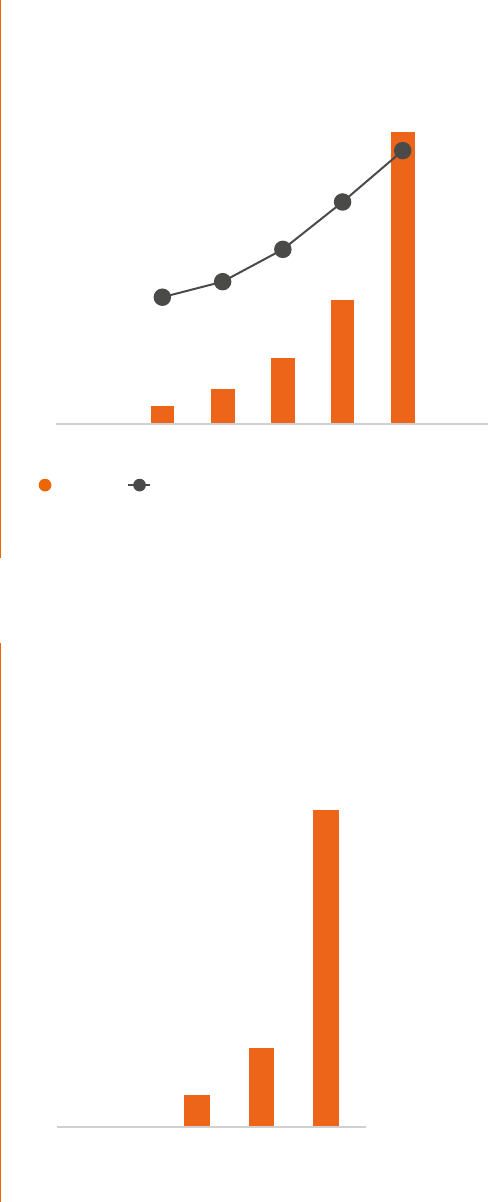

Growing volume of SARs

More than 3.6 million SARs were led in 2022, an 18% increase over 2021. The 3.1 million

SARs led in 2021 represented a 22.5% increase over 2020.

The graph below, Figure 4, below shows the total annual volume of suspicious activity

designations, or “ags,” reported across all lings. For those unfamiliar with the SAR form,

numerous check-box options are available when describing the suspicious activity being

reported. It is widespread practice to select multiple suspicion ags because some activities

straddle multiple categories.

Both datasets – i.e., total SARs and total suspicious activity designations – are important.

Aggregated annual ling data provides a broad, holistic view and is valuable for forecasting.

The designation-specic data provides granular visibility of specic threat vectors, such as

fraud or money laundering, targeted by illicit actors.

In general, since data became available in 2014, there has been steady growth in reported

suspicious activity. This is partly due to increasing sophistication in corporate anti-money

laundering and anti-fraud programs, as well as advances in detection technology, evolving

regulatory priorities, and enhanced scrutiny by enforcement bodies.

However, the notable surge in SAR volumes between 2020 and 2023, where the number of

suspicion designations grew from 6.3 million to 9.3 million, represents an increase of 46%.

Figure 4: Total Suspicious Activity Designations (all industries)

1,000,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

3,992,945

4,312,258

4,782,217

4,976,592

5,241,847

5,596,620

6,395,818

8,068,757

9,356,155

2,493,523

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

0

* 2023 Stats include Jan-March filings

© Thomson Reuters 2023

Suspicious Activity Reports 2023 11

Figure 5: Top 10 Suspicious Activity Flags (Overall)

Suspicious Activity 2019 2020 2021 2022 2023

Transaction with no apparent economic,

business, or lawful purpose

313,124 430,669 686,481 780,057 213,281

Check 285,716 284,888 350,372 683,541 185,584

Suspicion concerning the source of funds 391,650 445,874 594,713 608,043 173,618

Transaction(s) below currency

reporting threshold

306,324 426,664 552,640 573,057 139,429

Suspicious use of multiple transaction locations 401,922 429,501 480,224 521,028 141,559

Transaction(s) below BSA recordkeeping

threshold

479,496 494,076 564,264 493,287 119,608

Other suspicious activities 262,987 277,074 346,811 477,336 110,027

Two or more individuals working together 244,922 287,023 355,253 467,448 130,493

Suspicious electronic transfers 244,814 356,958 467,053 450,754 112,662

Transaction out of pattern for customer(s) 231,967 307,971 402,180 420,854 107,817

* 2023 Stats include Jan-March lings

Pandemic response-related fraud

Since 2020, all industries have seen signicant growth in fraud of all types, from simple check

fraud and scam activity to business email compromises and electronic intrusions resulting in

nancial losses. We investigate the pandemic’s role in fraud growth later in this report.

Digital-rst banking

With digital-rst banking, customer interactions occur primarily through digital channels,

such as websites and mobile device applications. Adopting this approach has been a priority

for national and regional banks for several years, as it allows them to reach more customers

outside traditional community branches by offering around-the-clock access to bank accounts

and services. That exibility became a crucial selling feature when pandemic mitigation

measures disrupted daily life in 2020.

Pivoting to the digital-rst paradigm required nancial rms to balance the competing

priorities of maximizing security while minimizing customer friction. Fraudsters took

advantage of the built-in incentives driving banks to streamline customer-facing processes,

and the result was fraud on a massive scale

© Thomson Reuters 2023

Suspicious Activity Reports 2023 12

4

FinCEN Alerts/Advisories/Notices/Bulletins/Fact Sheets, available at https://www.ncen.gov/resources/advisoriesbulletinsfact-sheets.

Regulatory pressure

FinCEN has issued dozens of advisories, alerts, and notices since July 2020

4

, highlighting its

focus on emergent AML concerns ranging from cryptocurrency abuse to human trafcking,

elder nancial exploitation, ransomware, sanctions evasions, mail-theft-related check fraud,

and illicit real estate activity.

Regulators have consistently reminded nancial institutions of their suspicious-activity

reporting obligations, while providing additional direction on how to make SARs more

informative and actionable for authorities. FinCEN also compiles and shares threat typologies

and red-ag indicators to help nancial institutions detect and report suspicious activity. We

have reiterated many of these red ags throughout the report.

Defensive lings

While most individual SAR lings never lead to criminal convictions, the cumulative ow of

data is of immense value to nancial intelligence and law enforcement agencies. Regulators

are therefore unlikely to ever discourage rms from reporting grey-area transactions that,

while appearing unusual, do not meet the technical criteria for raising suspicion.

Suspected money laundering and general suspicious activity account for most SARs lings,

followed closely by fraud. The data also shows many rms consider incomplete customer

information as sufcient grounds to report a money laundering concern.

Three of the 10 most reported suspicious activities relate to information gaps about a

customer or out-of-pattern transactions that raised red ags. Many SARs are led when

analysts and investigators cannot determine funding sources, cannot nd legitimate reasons

for unusually large deposits or withdrawals, or cannot identify relationships between parties

that could explain out-of-pattern activity.

Suspicious Activity 2019 2020 2021 2022 2023

Transaction with No Apparent Economic,

Business, or Lawful Purpose

313,124 430,669 686,481 780,057 213,281

Suspicion Concerning the Source of Funds 391,650 445,874 594,713 608,043 173,618

Transaction Out of Pattern for Customer(s) 231,967 307,97 1 402,180 420,854 107,817

Total: 936,741 1,184,514 1,683,374 1,808,954 301,675

* 2023 Stats include Jan-March lings

Figure 6: Designations Commonly Used in Defensive SAR Filings

© Thomson Reuters 2023

Suspicious Activity Reports 2023 13

If AML analysts and investigators as a group had sufcient time, resources, and data, they

likely could remediate or avoid a statistically signicant portion of the suspicious transactions

listed in the chart below. These grey-area reports account for approximately 20% of all

SAR lings.

Indeed, with the right combination of public records, transactional insights, and relevant

input from customers, nancial institutions can signicantly reduce the volume of extraneous

SAR lings.

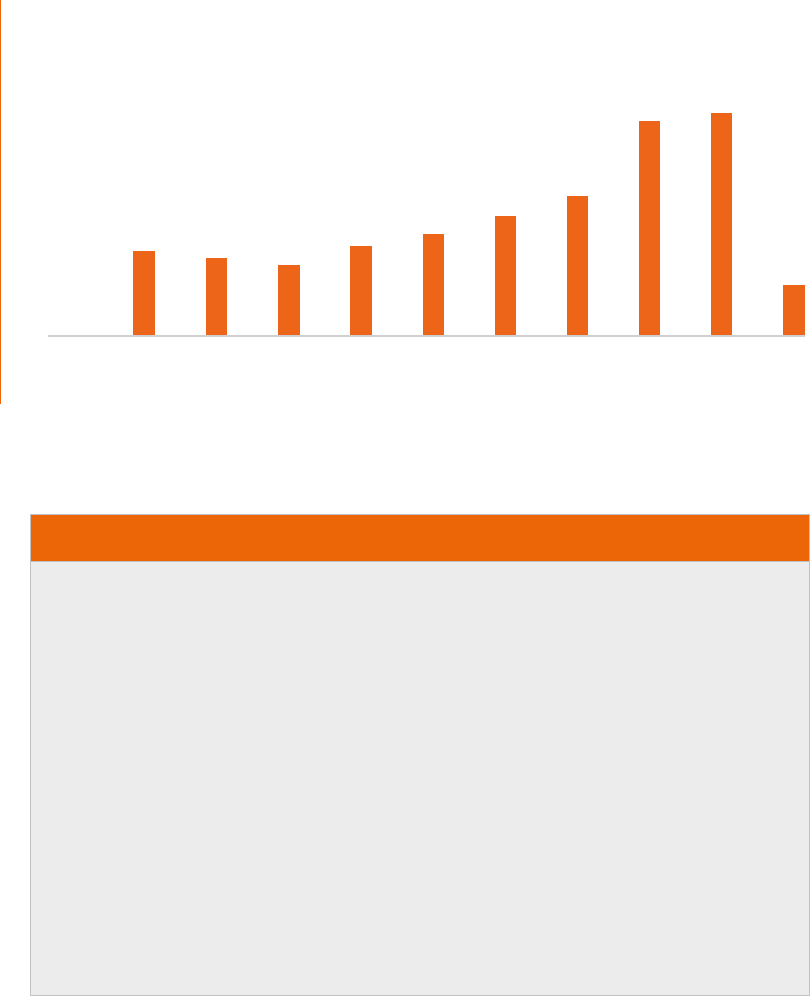

Figure 7: Year-Over-Year SAR Filings by Financial Institutions

0

500,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

1,545,879

1,680,784

1,832,080

1,794,625

1,872,323

1,995,250

2,154,397

2,605,935

3,080,947

812,395

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

0

* 2023 Stats include Jan-March filings

The financial institution group consists of depository institutions, money service businesses (MSBs), and

loan or finance companies. This industry category files more than 85% of all SARs. According to FinCEN,

the 10 most prolific SAR filers in fiscal 2022 produced 52% of all reports.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 14

* 2023 Stats include Jan-March lings

Monthly SAR Filings - All Industries

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

January 130,342 167,693 151,620 166,854 177,537 182,655 189,304 207,953 293,320 295,760

February 122,452 130,716 145,716 144,296 160,132 176,363 190,438 211,130 271,374 291,595

March 126,754 150,211 163,943 186,042 192,786 196,876 199,904 246,411 325,378 351,089

April 145,226 152,984 163,668 156,667 179,171 183,080 202,120 256,745 292,621

May 140,813 141,306 157,010 177,677 188,204 209,066 166,229 258,017 286,702

June 143,585 152,593 191,516 17 7,625 181,926 184,782 183,527 277,334 309,408

July 142,908 155,932 164,103 157,952 174,018 196,480 223,788 263,780 291,870

August 134,718 140,574 171,970 187,391 209,468 198,579 220,348 264,122 330,581

September 144,651 157,882 177,329 175,763 167,193 187,609 238,884 268,224 312,379

October 150,304 147,031 153,958 168,882 186,616 210,507 225,608 268,224 286,721

November 138,539 157,894 164,246 168,116 182,276 190,188 223,849 267,052 310,487

December 138,831 157,849 170,559 167,141 171,846 184,978 240,510 280,458 305,609

Monthly

Average

138,260 151,055 164,637 169,534 180,931 191,764 208,709 255,788 301,371 312,815

Key: <Average >Average > 1 σ

Seasonality

Monthly SAR loads tend to vary year to year, as economic and societal factors likely play

a role in periods featuring high reporting volumes. Pre-pandemic, anti-fraud and AML

specialists typically observed a spike in lings during the spring and tax-return season, as

well as the end-of-summer and back-to-school period. The monthly SAR chart highlights

in red any month where SAR lings exceeded that year’s average by at least one standard

deviation. Orange highlights indicate ling volumes that were above the annual average but

still typically within range. White months had average or below-average volumes.

The monthly SARs chart conrms that for the last nine years, January and February typically

showed below-average SAR volumes, while late spring and late summer were often

particularly busy. These ndings align tightly with observations by AML experts.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 15

January and February typically showed below-average SAR

volumes, while late spring and late summer were often

particularly busy.

Figure 8: Takeaways from Monthly SAR Volumes Include:

• 2022 saw exceptionally high SAR volumes in March and August, with moderately

above-average levels in June, September, November and December

• Every month in 2022 showed more SAR-ling activity than corresponding months

in 2021

• 2020-2021 saw heightened caseloads during the back-to-school and winter-holiday

shopping seasons.

• 2017-2019 saw below-average caseloads between November and February.

• Consistently lower caseloads between January and April of each year.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 16

2023 SAR Prediction:

A Record Year in Volume

Based on monthly data, we can project that approximately 3.75 million SARs will be led

in 2023, representing another record year in volume. This projection also considers current

regulatory trends, which suggest that SAR-ling requirements will only increase in the

near- to medium-term. Additionally, data from the rst quarter of 2023 is consistent with the

overall growth trend in SARs lings.

Figure 9: 2023 End-Of-Year Projected SAR Filings

0

500,000

2019 2020 2021 2022 2023

1,000,000

SARs Filed

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

0

* 2023 Stats include Jan-March filings

** Projections subject to change based on overall market

Projection

Financial institutions led an average of 312,815 SARs per month in the rst quarter of 2023,

reecting a 4% increase from the previous year’s rst-quarter monthly average. That increase

was slightly less than in 2019. In 2018 and 2019, however, monthly average SAR growth in

the rst quarter roughly matched the average rate of increase for the entire year, so we have

chosen to incorporate that pattern into our projection for 2023.

Risk leaders should plan for a normal busy season at the beginning and end of summer.

It should be noted that annual SAR volumes are largely driven by a combination of factors,

including consumer spending velocity, regulatory guidance, and technological or

process innovations.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 17

Human Exploitation

FinCEN data showed a 373% increase in human smuggling related SAR lings from 2020 to

2021, followed by a subsequent 173% increase from 2021 to 2022. In the rst quarter of 2023,

FinCEN received 4,776 human-smuggling SARs, compared to 6,461 such reports for all

of 2021.

SARs related to human trafcking increased by 32% from 2020 to 2021, followed by a further

42% increase from 2021 to 2022. The rst quarter of 2023 saw 2,237 human-trafcking

SARs led.

FinCEN distinguishes between two types of human exploitation – smuggling and trafcking –

according to the following criteria:

• Human smuggling: Facilitation, transportation, or attempted transportation of persons

across national borders, in violation of immigration laws. Smuggling is typically conducted

for prot, with the individuals being smuggled often voluntarily paying smugglers to help

them enter another country illegally. Subjects of human smuggling can often become

victims of human trafcking.

• Human trafcking: Modern-day slavery, involving the use of force, fraud, or coercion

to exploit individuals for labor or commercial sex purposes. Trafcking in people often

involves physical violence, psychological manipulation, or debt bondage. Victims can

include men, women, and children. Victims can be trafcked across local, state, and

national borders.

Figure 10: Human Exploitation SAR Filings

0

2,000

2018 2019 2020 2021 2022 2023

4,000

Human Smugling

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0

* 2023 Stats include Jan-March filings

Human Trafficking

6,461

4,092

4,776

2,237

3,096

1,581

3,384

2,432

177

336

17,646

5,798

© Thomson Reuters 2023

Suspicious Activity Reports 2023 18

FinCEN issued an alert in January 2023

5

addressing human-trafcking trends, typologies,

and red ags to help nancial institutions better identify and report suspicious transactions

related to the multi-billion dollar criminal enterprise.

“Illicit actors, including transnational criminal organizations, engage in human smuggling

activity at the U.S. southwest border to reap illicit nancial gains, and they do so without

regard for the well-being or physical safety of those involved,” said FinCEN Acting Director

Himamauli Das. “Financial institutions need to know that their vigilance and prompt

Bank Secrecy Act reporting matters – it aids investigations tied to human smuggling and

transnational organized crime and can ultimately save lives.”

Human trafcking is one of FinCEN’s eight national priorities related to anti-money

laundering and countering the nancing of terrorism, as mandated by the Anti-Money

Laundering Act of 2020.

Human smugglers operating across the southwest border of the United States have exploited

a period of surging migration to generate an estimated $2 billion to $6 billion in yearly

organized crime revenue, according to the U.S. Department of Homeland Security. These

networks are often associated with transnational criminal organizations, including drug

cartels, which control the territories through which smuggling operations take place.

The increase in SAR lings has been largely driven by renewed FinCEN guidance on

identifying and reporting human trafcking activity in October 2020

6

. In response,

organisations started awareness and education efforts, as well as making more lings.

Government programs and organizations such as The Knoble

7

have also driven reporting and

law enforcement action.

5

FinCEN Alert on Human Smuggling along the Southwest Border of the United States; (FIN-2023-Alert001) January 13, 2023; available at

https://www.ncen.gov/sites/default/les/shared/FinCEN%20Alert%20Human%20Smuggling%20FINAL_508.pdf.

6

https://www.ncen.gov/sites/default/les/advisory/2020-10-15/Advisory%20Human%20Trafcking%20508%20FINAL_0.pdf

7

See The Knoble, at https://www.theknoble.com/.

“Recent events involving the death of migrants attempting to cross into the

United States illustrate the dangers associated with human smuggling and

how smuggling networks exploit human beings for prot,” FinCEN stated.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 19

Laundering the proceeds of human exploitation

Human smuggling is often tied to larger criminal groups whose money laundering methods

overlap signicantly with those of drug cartels and similar organizations.

Smuggling fees are often paid by migrants’ U.S.-based family members using transfers

disguised as common remittances. Funds are sent to “funnel accounts” at nancial

institutions with branches along both sides of the southwest border where they are

subsequently withdrawn as cash to pay smugglers. Migrants primarily pay smugglers in cash

which requires the criminals to move cash in bulk and use it to purchase high-value assets

such as real estate and businesses.

Human smugglers also use mobile payment applications and other peer-to-peer networks to

transfer funds, albeit less frequently.

Bank Secrecy Act obligations

FinCEN’s human exploitation alert advised rms that SARs related to human smuggling

should be included in the narrative the key term, “FIN-2023- HUMANSMUGGLING” in SAR

eld 2 (Filing Institution Note to FinCEN), as well as in the narrative, and be selecting SAR

eld 38(g) (human smuggling).

FinCEN noted that potential victims of human trafcking should not be reported as the

subject of a SAR. “Rather, all available information on the victim should be included in the

narrative portion of the SAR.” FinCEN further requests that nancial institutions reference

the advisory by including the key term: “HUMAN TRAFFICKING FIN-2020-A008” in SAR eld

2 (Filing Institution Note to FinCEN) to indicate a connection between the suspicious activity

being reported and the activities highlighted in the advisory. Additional information to report

includes behavioral indicators, email addresses, phone numbers, and IP addresses, when

possible, to aid law enforcement investigations.

Smuggling fees are often paid by migrants’ U.S.-based family

members using transfers disguised as common remittances.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 20

Indicators of human trafcking

• Customers frequently appear to move through, and

transact from, different geographic locations in the

United States. These transactions can be combined

with travel in foreign countries known to be signicant

conduits for

human trafcking.

• Transactions are inconsistent with a customer’s

expected activity or line of business and reect an

apparent effort to cover trafcking victims’ living costs

including housing, transportation, medical expenses,

pharmacies, clothing, grocery stores, and restaurants.

• Transactional activity that occurs largely outside of

normal business hours (e.g., a business that operates

during the

day but conducts many transactions at night), almost

always in cash, with deposits that are larger than

expected for

the business.

• An individual frequently purchases and uses prepaid

access cards.

• A customer’s account shares common identiers such

as a telephone number, email, social media handle,

or address associated with escort agencies and

commercial sex advertisements.

• Frequent transactions with online classied sites based

in foreign jurisdictions.

• A customer frequently sends or receives funds via

cryptocurrency to or from dark net markets or services

with known links to illicit activity. This may include

services that host advertising content for illicit services,

sell illicit content, or nancial institutions that allow

prepaid cards to pay for cryptocurrencies without

appropriate risk mitigation controls.

• Frequent transactions using third-party payment

processors that conceal transaction originators or

beneciaries.

• A customer avoids transactions that require

identication documents or that trigger reporting

requirements.

Indicators of human smuggling

• Transactions involving multiple wire transfers, cash

deposits, or peer-to-peer payments from multiple

originators in different locations either across the

United States, or Mexico and Central America, to one

beneciary located on or near the southwest border,

with no apparent business purpose.

• Deposits by multiple individuals from multiple locations

into a single account. The depositors are not afliated

with the account holder’s work or area of residence, and

the transfers lack an apparent economic purpose.

• Unexplained currency deposits into U.S. accounts,

followed by rapid wire transfers to countries with high

migrant ows, such as Mexico and Central America.

The transfers are inconsistent with expected customer

activity.

• Frequent conversion of small-denomination bills to

larger denominations by customers outside

cash-intensive industries.

• Multiple customers sending wire transfers to a single

beneciary, where the senders are not relatives but may

be located in the sender’s home country. The transfers

are inconsistent with the recipient customer’s usual

account activity and reported occupation.

• A customer depositing signicantly larger amounts

than expected of peers in similar professions or lines of

business.

• A customer making cash deposits that are inconsistent

with the customer’s line of business.

• Extensive use of cash to conduct transactions and

purchase assets such as real estate.

Source: www.ncen.gov/sites/default/les/advisory/2020-10-15/Advisory%20Human%20Trafcking%20508%20FINAL_0.pdf

Figure 11: Important FinCEN Trafcking and Smuggling Red Flags

© Thomson Reuters 2023

Suspicious Activity Reports 2023 21

Online Child Exploitation

FinCEN issued a notice in September 2021 alerting rms to increasing rates of online

child sexual exploitation

8

. It gave nancial institutions specic SAR-ling instructions

and highlighted related nancial trends. Unfortunately, the SARs data for children is not

separated into its own category.

The FinCEN alert provided direction for nancial institutions and their handling of online

child sexual exploitation (OCSE). The notice provided SAR ling instructions requesting that

nancial institutions reference the notice in SAR eld 2 (Filing Institution Note to FinCEN)

using the keyword “OCSE-FIN-2021-NTC3.” Financial institutions were also instructed to

select SAR Field 38(z) (Other) as the associated suspicious activity type. If human trafcking

or human smuggling are suspected in addition to OCSE activity, nancial institutions were

instructed to also select the respective categories.

International standard-setters have also launched initiatives targeting online child

exploitation. The United Nations partnered with the Association of Certied Anti-Money

Laundering Specialists (ACAMS) in March 2023 to create a no-cost certication program to

help AML professionals and law enforcement authorities better detect nancial transactions

linked to child sexual abuse. The move followed growing concern about the online sale of

visually recorded abuse material.

The ACAMS training program – Preventing Online Child Exploitation with Financial

Intelligence – teaches the use of cryptocurrency blockchain analytics and compliance data

to identify and track the billions of dollars in illicit proceeds generated by online child sexual

abuse materials (CSAM). It is supported by the Finance Against Slavery & Trafcking (FAST)

initiative from the U.N. University Centre for Policy Research.

‘The extent of organized, for-prot child abuse is only getting worse’, FAST Project Director

Daniel Thelesklaf said, echoing senior ofcials at ACAMS who designed the program.

Global events have exacerbated the threat. The COVID-19 pandemic forced at-risk children to

isolate at home with their abusers, and Russia’s February 2022 invasion of Ukraine displaced

millions of people, including thousands of Ukrainian children forcibly relocated to

Russian territory.

8

https://www.ncen.gov/sites/default/les/shared/FinCEN%20OCSE%20Notice%20508C.pdf.

Reports of suspected child exploitation rose 35% in 2021,

compared to the previous year, according to the National

Center for Missing and Exploited Children.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 22

Fraud

Fraud rates in general have exploded over recent years, targeting both public and private

sectors. As with other threats, the COVID-19 pandemic accelerated the proliferation of

fraudulent activity, as criminals leveraged lockdowns, technological shifts, and

demographic changes.

American consumers reported an

average of 2.6 million fraud cases

annually during the pandemic’s

three-year emergency phase

(2020-2022), according to Federal

Trade Commission data. While

fraud reporting volumes were

relatively stable during that period,

total reported annual fraud losses

increased dramatically.

Overall, nancial institutions

and other entities have reported

signicant year-over-year increases

across nine of the 10 most-

reported fraud categories.

Figure 12: FBI Internet Crime

Reporting by the Numbers

$10.3 Billion

Victim losses in 2022

2,175+

Average complaints recieved daily

651,800+

Average complaints recieved per year (last 5 years)

Over 7.3 Million

Complaints reported since inception

Figure 13: Top 10 Federal Trade Commission (FTC) Fraud Report Categories

Rank Category # of Reports % Reporting $ Loss Total $ Loss Median $ Loss

1 Imposter Scams 761,600 21% $2,731.5M $1,000

3 Online Shopping and Negative Reviews 359,706 43% $358.7M $179

3 Prizes, Sweepstakes and Lotteries 148,161 12% $308.6M $950

4 Internet Services 113,548 4% $28.5M $300

5 Investment Related 107,205 74% $3,907.6M $5,000

6 Business and Job Opportunities 94,129 32% $373.5M $2,000

7 Telephone and Mobile Services 91,220 9% $20.9M $200

8 Health Care 74,031 6% $16.7M $260

9 Travel, Vacations and Timeshare Plans 65,135 16% $105.1M $1,266

10 Foreign Money Offers and Fake Check Scams 41,159 32% $123.8M $2,000

Source: https://public.tableau.com/app/prole/federal.trade.commission/viz/FraudReports/FraudLosses

© Thomson Reuters 2023

Suspicious Activity Reports 2023 23

Source: FTC Public Data for 2022

Figue 14: Identity Theft Types

Figue 15: Top 10 SAR Fraud Flags

Rank Theft Type # of Reports

1 Credit Card Fraud 440,631

3 Other Identity Theft 326,468

3 Bank Fraud 156,116

4 Loan or Lease Fraud 153,569

5 Employment or Tax-Rlated Fraud 103,409

6 Phone or Utilities Fraud 77,308

7 Government Documents or Benets Fraud 57,898

Suspicious Activity 2019 2020 2021 2022 2023

Check 285,716 284,888 350,372 683,541 185,584

Other Fraud (Type) 201,222 262,530 382,037 390,238 110,702

Credit/Debit Card 214,682 189,470 220,586 349,439 100,369

Counterfeit Instrument 129,972 135,432 159,475 327,413 89,128

ACH 121,290 203,635 276,093 291,583 80,942

Wire 123,664 120,025 122,562 136,695 41,153

Consumer Loan (see instructions) 98,209 80,009 76,438 106,966 27,351

Mass-Marketing 13,462 20,996 22,229 33,225 12,707

Business Loan 3,440 16,386 49,008 29,417 9,899

Application Fraud 12,683 16,357 18,875 22,088 5,264

Source: https://public.tableau.com/app/prole/federal.trade.commission/viz/FraudReports/FraudLosses

Source: https://public.tableau.com/app/prole/federal.trade.commission/viz/FraudReports/FraudLosses

Filtering FinCEN’s suspicious activity data by fraud type (as coded in SAR forms) reveals

sharp increases in particular categories between 2019 and 2022, including a 140% increase

in reported check fraud, an 84% increase in credit/debit card fraud, and a 142% increase in

counterfeit currency.

Check fraud, analyzed in more detail below, was by far the most prevalent fraud type

reported in 2022, with over 680,000 SAR lings. It was the second largest of all SAR

categories that year. While rms have responded by reinforcing their anti-fraud organizations

overall, they have focused particular attention on check fraud. While rms have responded by

reinforcing their anti-fraud organizations overall, they have focused particular attention on

check fraud.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 24

Figure 16: Check Fraud (All Industry)

0

100,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

106,264

118,869

160,742

173,056

211,621

285,716

284,888

350,373

683,541

185,584

200,000

300,000

400,000

500,000

600,000

700,000

800,000

0

* 2023 Stats include Jan-March filings

Check Fraud

Suspicious activity reporting about check fraud nearly doubled in 2022. Financial institutions

led over 680,000 check fraud SARs last year, a 95% increase over the 350,000 led in 2021.

Figure 17: Fraud SAR Filing Trends

0 100,000 200,000 300,000 400,000

Other Fraud (Type)

Identity Theft

Credit/Debit Card

Counterfeit Instrument

ACH

* 2023 Stats include Jan-March filings

2019 2020 2021 2022 2023

A previous alert from 2021 warned rms that fraud, including check fraud, was “the largest

source of illicit proceeds in the United States” and was among the country’s top anti-money

laundering priorities.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 25

Figure18: Check Fraud Indicators Include:

• Uncharacteristically large withdrawals from a customer’s account via check to a

new payee.

• Customer complaints about checks stolen from the mail and deposited into

unknown accounts.

• Complaints about mailed checks never reaching intended recipients.

• Checks used to withdraw funds appear to be made of a noticeably different

paper stock than that used by the issuing bank or other stock used for known,

legitimate transactions.

• Existing customer with no history of check deposits has new, sudden check deposits

and withdrawals or transfers.

• Non-characteristic, sudden, abnormal deposit of checks, often electronically, followed

by rapid withdrawal or transfer.

• Examination of suspect checks reveals faded handwriting underneath darker

handwriting, suggesting that the original handwriting was overwritten.

• Suspect accounts may exhibit indicators of other suspicious activity, such as

pandemic-related fraud.

• New customer opens an account that is seemingly used only for the deposit of checks

followed by frequent withdrawals and transfers.

• A non-customer who attempts to cash a large check or multiple large checks in

person and, when questioned by the nancial institution, provides an explanation that

is suspicious or potentially indicative of money mule activity.

FinCEN warned nancial institutions in February 2023 of a nationwide surge in check fraud

schemes targeting the U.S. Postal Service

10

.

Criminals increasingly targeted U.S. mail carriers during the COVID-19 pandemic, regulators

said. This type of crime typically involves stealing personal checks, business checks, tax

refund checks, and checks related to government assistance such as Social Security and

unemployment benets.

10

https://www.ncen.gov/sites/default/les/shared/FinCEN%20Alert%20Mail%20Theft-Related%20Check%20Fraud%20FINAL%20508.pdf

Source: https://www.ncen.gov/sites/default/les/shared/FinCEN%20Alert%20Mail%20Theft-Related%20Check%20Fraud%20FINAL%20508.pdf

© Thomson Reuters 2023

Suspicious Activity Reports 2023 26

Fraudsters and organized criminal groups may alter or wash stolen checks, substituting

legitimate payee information with new personal or business accounts controlled by the

criminals, FinCEN said. In addition to check washers, the alert outlined the role of so-called

money mules, which it described as people who transfer or move illicit funds at the direction

of others.

FinCEN requested that nancial institutions indicate a connection between the suspicious

activity being reported and the activities highlighted in its alert by including the term “FIN-

2023-MAILTHEFT” in SAR eld 2, as well as in the narrative and by selecting SAR Field 34(d)

(check fraud).

Indicators of Check fraud

FinCEN advised nancial institutions to consider the surrounding facts and circumstances

before escalating suspicion, such as whether transactions are consistent with prevailing

business practices and whether a customer raises multiple red ags.

Financial institutions are obligated to le a SAR when they detect a suspicious

transaction or activity by a identiable, individual involving at least $5,000, and

lacking an apparent lawful purpose, or when there is reason to suspect the funds

were derived from illegal activities.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 27

Supporting Criminal Data

SAR and FBI Data Paint Bleak Picture

Data from the U.S. Federal Bureau of Investigations (FBI) validates the rising fraud trend

apparent in FinCEN’s SAR database.

FBI Internet Crime Complaint Center (IC3) data for 2022 showed:

• 127% increase in reported investment fraud, amounting to $3.3 billion in reported losses.

• Call center fraud affected more than 44,000 victims, accounting for over $1 billion

in losses.

• 2,385 complaints of ransomware targeting critical infrastructure, with reported losses

totaling over $34 million.

Figure 19: Complaints and Losses over the Last Five Years

3.26 Million Total Complaints

$27.6 Billion Total Losses

351,937

467,361

791,790

847,376

800,944

$3.5 Billion

$4.2 Billion

$6.9 Billion

$10.3 Billion

$2.7 Billion

202 2

2021

2020

2019

2018

Complaints Losses

Source: https://www.ic3.gov/Media/PDF/AnnualReport/2022_IC3Report.pdf (FBI’s IC3 Annual Report for 2022)

© Thomson Reuters 2023

Suspicious Activity Reports 2023 28

FBI Internet Crime Complaint Center (IC3)

Supporting Data

Takeaways:

• Exponential growth in victims and nancial losses.

• Exacerbated by the pandemic.

• Domestic and international organized crime as well as state-sponsored criminal

enterprises are all active in nancial crimes.

• Fraudulent events create devastating losses to victims.

• Major business opportunities for scam perpetrators.

• Signicant amounts of elder fraud go un-reported due to embarrassment, nancial

problems, and familial abuse.

Source: IC3 FBI’s IC3 Annual Report for 2022

Figure 20: FBI IC3's Top Five Internet Crime Types

2018 2019 2020 2021 2022

32,538

23,903

15,421

13,633

14,408

39,416

39,360

76,741

43,101

51,146

51,679

82,478

108,869

61 ,832

65,116

58,859

51,829

45,330

38,218

50,642

300,497

323,972

241,342

114,702

26,379

Tech support

Extortion

Non-Payment/

Non-Delivery

Personal

Data Breach

Phishing

number of reports to IC3

© Thomson Reuters 2023

Suspicious Activity Reports 2023 29

Elder Financial Exploitation

SAR data shows a dramatic increase in suspected elder nancial abuse. FinCEN recorded

nearly 107,000 SARs related to elder abuse in 2022. That gure’s correlation to incidents

of crime is supported by the FBI’s Internet Crime Complaint Center (IC3), which recorded

88,000 cases of online fraud targeting seniors. Losses by elder victims increased by 84% in

2022, FBI data showed.

Senior vulnerability to online fraud

was exacerbated by the COVID-19

pandemic which forced many

seniors to transition from in-branch

service to mobile banking. Instances

of phishing, identity theft, and other

cybercrime targeting the elderly

population became much

more prevalent.

Such scams are often perpetrated

through popular online services, such as the practice of “catshing,” in which fraudsters use

ctitious social-media proles to ensnare seniors in false romantic relationships resulting in

nancial abuse. Another tactic involves SMS-phishing – or smishing – whereby scammers

send text messages purporting to be from reputable companies in order to manipulate

targets into revealing personal information including passwords or credit card numbers.

Figure 20: Elder Financial Exploitation SAR Filings

0

20,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

21,656

25,566

52,633

62,807

53,924

62,298

62,014

72,173

106,754

36,911

40,000

60,000

80,000

100,000

120,000

0

* 2023 Stats include Jan-March filings

Figure 21: IC3 Victims Over 60 by the numbers

Sourced (FBI's IC3 Annual Report for 2022)

88,262

Total Victims Over 60

$3.1 Billion

Total Losses

84%

Increase in losses from 2021

$35,101

Average Losses Per Victim

5,465

Victims losing more then $100K

© Thomson Reuters 2023

Suspicious Activity Reports 2023 30

Source: FBI Elder Fraud Report 2022 (https://www.ic3.gov/Media/PDF/AnnualReport/2022_IC3ElderFraudReport.pdf)

Source: FBI Elder Fraud Report 2022 (https://www.ic3.gov/Media/PDF/AnnualReport/2022_IC3ElderFraudReport.pdf)

0

5,000

2018 2019 2020 2021 202 2

10,000

15,000

20,000

25,000

0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

$800,000,000

$0

Figure 22: Call Center Frauds - Victims Over 60

Losses Losses

0

$200,000,000

2020 2021 2022

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

0

Figure 23: Investment Scam

Losses by Victims Over 60

© Thomson Reuters 2023

Suspicious Activity Reports 2023 31

A 2022 FinCEN alert about elder abuse included both behavioral and nancial red ags

indicating suspicious activity

9

.

FinCEN requested that nancial institutions ling SARs on such activity mark the check box

for Elder Financial Exploitation and include the key term “EFE FIN-2022-A002” in SAR eld 2

and to ensure the narrative section describes a connection between the reported suspicious

activity and the specic indicators highlighted in the advisory.

9

https://www.ncen.gov/sites/default/les/advisory/2022-06-15/FinCEN%20Advisory%20Elder%20Financial%20Exploitation%20FINAL%20508.pdf.

Source: FBI Elder Fraud Report 2022 (https://www.ic3.gov/Media/PDF/AnnualReport/2022_IC3ElderFraudReport.pdf)

Figure 24: Confidence/Romance Scam Losses by Victims Over 60

2020

2021

202 2

0 $100,000,000 $200,000,000 $300,000,000 $400,000,000

© Thomson Reuters 2023

Suspicious Activity Reports 2023 32

Pandemic-related Fraud and Suspicious

Receipt of Government Payments

The chart above shows a dramatic spike in SAR lings related to public support programs

in 2020 and 2021, almost certainly driven by pandemic-related U.S. government spending

through the Paycheck Protection Program (PPP), Economic Injury Disaster Loans (EIDL), and

other state and federal unemployment benets.

Unemployment insurance fraud reached $60 billion

during the pandemic; the U.S. General Accounting

Ofce estimated in a February 2023 report

14

.

Investigations by the Department of Labor’s inspector

general, opened at a rate of 100 per week, resulted in

1,200 indictments or initial charges from April 2020

through January 2023.

Like other nancial institutions and government

agencies, federal housing programs have seen a surge

in SAR lings.

Government-sponsored enterprises (GSEs), which bring

capital to the housing market, include Fannie Mae,

Freddie Mac, and the Federal Home Loan Banks.

Figure 26:

Housing Government Sponsored Enterprises

0

1,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

160

1,267

2,285

2,127

2,553

3,106

3,054

5,476

7,877

2,146

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0

* 2023 Stats include Jan-March filings

Total SARs

Figure 25: Suspicious Receipt of Government Payments/Benefits

0

20,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

5,631

4,980

3,998

2,906

2,957

2,873

75,271

143,215

42,223

5,393

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0

* 2023 Stats include Jan-March filings

14

https://www.gao.gov/assets/gao-23-106586.pdf

© Thomson Reuters 2023

Suspicious Activity Reports 2023 33

Specic Industries and Terror Financing

Financial Institutions: Securities/Futures

Financial markets are also experiencing a sharp uptick in suspicious activity lings that

often overlap with other crime trends such as elder nancial exploitation. Although check,

credit card, and wire frauds occur at traditional nancial service rms such as banks, more

advanced frauds occur in the securities and futures markets.

Figure 27: Securities/Futures Industry SAR Filings - Steady Fraud Uptick

0 5,000 10,000 15,00 0 20,000 25,000 30,000

Credit/Debit Card

Identity Theft

Other Fraud (Type)

Suspicious EFT/

Wire Transfers

Wire

* 2023 Stats include Jan-March filings

Check

ACH

Account Takeover

2019 2020 2021 2022 2023

Sophisticated criminals have been raiding brokerage accounts by fraudulently transferring

assets through the Automated Customer Account Transfer Service (ACATS). ACATS frauds

could likely fall under several of the threat designations covered in this report.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 34

10

https://www.nra.org/rules-guidance/notices/23-06.

11

https://www.nra.org/rules-guidance/notices/22-21.

12

https://www.nra.org/rules-guidance/notices/21-18.

13

https://www.nra.org/rules-guidance/notices/20-13.

The Financial Industry Regulatory Authority (FINRA) issued Regulatory Notice 23-06

10

in

March 2023, highlighting effective practices for mitigating the risk of criminal actors abusing

ACATS. FINRA’s warning followed Regulatory Notice 22-21

11

, published in October 2022,

which highlighted a rising trend of fraud perpetrated through ACATS. It also outlined relevant

regulatory obligations and provided information for reporting fraud.

ACATS enables eligible participants to enter, review, and settle the transfer of customer

accounts. It facilitates the transfers of many different asset types, including equities,

corporate and municipal bonds, unit investment trusts, mutual funds, options, annuities,

and cash.

Criminal actors abuse the system by opening an online brokerage account using the stolen

personally identiable information of a legitimate client from another member rm.

“The bad actor may then engage receiving and/or carrying members to conduct a transfer

of the account of the legitimate customer at the carrying member into the new brokerage

account at the receiving member,” FINRA said.

“When that transfer is complete, the bad actor may then proceed with moving the ill-gotten

assets out of the newly established brokerage account to another external account or

nancial institution.”

Some of the safeguards rms employ resemble those for preventing identity theft and

phishing attacks. Firms should be on the lookout for grammatical and spelling errors, as well

as writing that changes in style from previous email communications. Additionally, some

of the practices are consistent with precautions outlined in Regulatory Notice 21-18

12

on

preventing online account takeovers and Regulatory Notice 20-13

13

, which warned rms about

fraud risk during the COVID-19 pandemic.

FINRA urged rms to evaluate their supervisory systems related to ACATS transfers and

fraud mitigation.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 35

Figure 29: Indicators of ACATS Fraud:

• Repeated transfer rejections due to incomplete or inaccurate information. Errors

might relate to account type or other basic information, including a carrying

member’s rejection of a receiving member’s account transfer request for the same

customer on multiple occasions.

• Rapid asset transfers following account creation. Soon after assets have been moved

into a new brokerage account, a bad actor sends instructions to quickly move those

assets to another external account or nancial institution.

• Changes in communication patterns. Customers who usually communicate by

telephone may suddenly prefer to communicating only by email, and when the

rm contacts the customer by usual means, the customer conrms that the email

communication did not come from the customer.

Source: https://www.ncen.gov/sites/default/les/advisory/2022-06-15/FinCEN%20

Advisory%20Elder%20Financial%20Exploitation%20FINAL%20508.pdf

Figure 28: Securities Industry SAR Filings

0

10,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

22,081

20,436

18,938

23,832

26,776

33,222

38,236

58,951

61,783

14,249

20,000

30,000

40,000

50,000

60,000

70,000

0

* 2023 Stats include Jan-March filings

© Thomson Reuters 2023

Suspicious Activity Reports 2023 36

Terror Financing

Suspicious transaction reporting related to terrorism nancing has declined in recent years,

a deviation from overall increases in other nancial crimes. The aggregate volume of

terrorism related SAR lings has, however, always been relatively low in absolute terms,

an ironic twist considering the landmark USA PATRIOT Act of 2001 created a host of new

AML/CFT obligations following the September 11 terrorist attacks in New York City and

Washington, D.C.

In addition to funding from wealthy sympathizers and rogue nations, terrorist organizations

rely on a variety of criminal activities to nance their operations, including fraud and drug

trafcking. As a result, nancial institutions may identify a suspicious transaction but lack

sufcient awareness to ascertain its indirect connection to terrorism, unless the named

originator or beneciary was ofcially sanctioned as a designated terrorist.

Firms may therefore le a fraud SAR, including the names of involved parties, and leave it to

law enforcement authorities with specialized intelligence to determine whether the activity is

linked to terrorism.

Furthermore, there has been some criticism of FinCEN over its apparent lack of focus on

alerts and advisories providing updated guidance and red ags with regards to terror nance.

Some experts believe a lack of recent, major terrorist attacks has allowed regulatory focus

to shift.

Figure 30: Terrorism Financing Related SARs

0

200

400

600

800

1000

1200

1400

1600

1800

0

* 2023 Stats include Jan-March filings

Known or Suspected Terrorist/Terrorist Organization Other Terrorist

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

© Thomson Reuters 2023

Suspicious Activity Reports 2023 37

Casino Industry

Casino-relate suspicious activity reporting saw a notable decline in 2020, due to pandemic

measures that closed many casinos, followed by a signicant drop in attendance after

gradual reopening.

The casino sector has, however, faced increasing regulatory pressure over

money-laundering concerns.

* 2023 Stats include Q1 lings

**Casino Industry consists of: Casino/Card Club – Other, Casino/Card Club, Casino/Card Club - State Licensed

Casino and Casino/Card Club - Tribal Authorized Casino

Figure 31: Casino Industry SARs

0

10,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

45,013

49,559

57,120

59,098

53,591

51,275

39,480

54,937

62,003

16,068

20,000

30,000

40,000

50,000

60,000

70,000

0

Total SARs Filed

© Thomson Reuters 2023

Suspicious Activity Reports 2023 38

Figure 32: Insurance Industry SARs

0

500

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

2,738

2,307

2,389

2,687

2,523

2,697

2,556

2,597

2,654

698

1,000

1,500

2,000

2,500

3,000

0

Total SARs Filed

* 2023 Stats include Jan-March filings

Healthcare and Insurance Industry

The U.S. Department of Justice (DOJ) announced criminal charges in April 2023 against 18

defendants for their alleged role in healthcare fraud schemes that exploited the COVID-19

pandemic, resulting in over $490 million in false billings to federal programs and theft from

publicly funded pandemic programs.

Monitoring medical providers and other recipients of government health insurance payments

for fraudulent activity has always been difcult because it depends on an institution’s

ability to segment its clients. That challenge has escalated with the surge in COVID-related

programs such as the Health Resources and Services Administration’s program to help

the uninsured.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 39

International Comparisons

The quantity of SAR lings – called suspicious transaction reports internationally – varies

widely between countries, owing to differences in economic size and intensity. Their purpose,

however, remains the same: to detect and prevent illegal activity. These statistics reect

signicant annual growth in suspicious transaction lings internationally.

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

Fig 33: International SAR Filing Comparison

Country 2018 2019 2020 2021 2022

USA 2,171,173 2,301,163 2,504,509 3,069,450 3,616,450

United Kingdom 463,938 478,437 573,085 742,317 901,255

Canada 179,172 235,661 386,102 468,079 585,853

Source: United Kingdom Financial Intelligence Unit Annual Report:

https://nationalcrimeagency.gov.uk/who-we-are/publications/632-2022-sars-annual-report-1/le

Source: Canada Data: FINTRAC ANNUAL REPORT - https://ntrac-canafe.canada.ca/publications/ar/2022/1-eng

© Thomson Reuters 2023

Suspicious Activity Reports 2023 40

Closing Thoughts: Increasing Fraudulent

Activity, Increasing Surveillance Tools

The data presented in this report highlights signicant trends and changes in SAR lings.

Disruptions inherent to the COVID-19 pandemic created new opportunities for criminal

abuse, reected in broad reporting surges in nearly all types of nancial crime. Additionally,

increased regulatory pressure, warnings, and defensive ling practices have provided a

steady and growing momentum to ling volumes. Fraud has increased to unprecedented

levels as validated by data from the FBI and Federal Trade Commission.

Suspicious Activity Reports are an essential tool in law enforcement’s effort to ght crime.

They have also become a critical challenge for corporate compliance, anti-fraud, and risk

departments across virtually all nancial services rms.

Risk, BSA, compliance, and anti-fraud leaders should continuously monitor this data as it

provides insight into developments affecting industry peers.

Organizations should contrast the granular, publicly available data with their own internal

sources to benchmark themselves against the broader market. Bank leaders can use such

comparisons to identify strengths and weaknesses in their compliance programs and nd

potential blind-spots for illegal activity within their customer base. By taking the most recent

SAR statistics into account, nancial institutions and other businesses should reasonably be

able to identify the most prevalent fraud and money laundering threats.

Law enforcement agencies and professionals have repeatedly voiced concern over increases

in defensive lings, while urging rms to include more specic information in SAR lings.

Institutions should also be working to reduce unproductive alerts and working to leverage

technology to combat fraud proactively. Additionally, there is a growing need for qualied

subject-matter experts to examine trending fraud practices.

© Thomson Reuters 2023

Suspicious Activity Reports 2023 41

Thomson Reuters Institute

The Thomson Reuters Institute brings together people from across the legal, corporate, tax&

accounting and government communities to ignite conversation and debate, make sense

of the latest events and trends and provide essential guidance on the opportunities and

challenges facing their world today. As the dedicated thought leadership arm of Thomson

Reuters, our content spans blog commentaries, industry-leading data sets, informed

analyses, interviews with industry leaders, videos, podcasts and world-class events that

deliver keen insight into a dynamic business landscape.

Visit thomsonreuters.com/institute for more details.

About the authors

SUSANNAH HAMMOND

Susannah Hammond is Senior Regulatory Intelligence Expert for Thomson Reuters

Regulatory Intelligence with more than 25 years of wide-ranging compliance, regulatory and

risk experience in international and UK nancial services. She is co-author of “Conduct and

Accountability in Financial Services: A Practical Guide” published by Bloomsbury Professional.

TODD EHRET

Todd Ehret is a Senior Regulatory Intelligence Expert for Thomson Reuters Regulatory

Intelligence. He has more than 25 years’ experience in the nancial industry where he held key

positions in trading, operations, accounting, audit, and compliance for broker-dealers, asset

managers, private equity, and hedge funds. Before joining Thomson Reuters he served as a

Chief Compliance Ofcer and Chief Operating Ofcer at a Registered Investment Adviser/

Hedge Fund for nearly a decade.

Explore Regulatory Intelligence, the regulatory compliance solution from Thomson Reuters.

rs 2022

About the authors

JACOB DENMAN

With more than a decade of experience in nancial crime investigations, nancial crime

leadership roles, and law enforcement, Jacob has a wealth of knowledge and expertise in

risk, nancial crime, and fraud. As a Risk, Fraud & Compliance Manager at Thomson Reuters,

Jacob is responsible for developing and executing creative strategies to grow the risk and

fraud product lines by driving customer engagement and adoption of our products. He

collaborates closely with sales, product management, and other key business stakeholders to

ensure Thomson Reuters products are aligned with customer needs. Prior to joining Thomson

Reuters, Jacob was a lead investigator in nancial crimes at Wells Fargo, and TCF Bank. Jacob

also has more than seven years of experience in law enforcement.

BRETT WOLF

Brett Wolf is a Senior Anti-Money Laundering Correspondent for Thomson Reuters. For more

than two decades, Brett has been on the AML beat, producing daily regulatory intelligence

news and analysis to aid AML and sanctions compliance professionals. A proven investigative

journalist for Thomson Reuters, Brett also has experience reporting on Justice Department

efforts to combat money laundering, terrorist nancing, corruption, and offshore tax evasion

and non-compliance with the Bank Secrecy Act (BSA).

TODD EHRET

Todd Ehret is a Senior Regulatory Intelligence Expert for Thomson Reuters Regulatory

Intelligence. At Thomson Reuters he has authored numerous articles and white-papers, and

frequently presents at industry conferences, events, and seminars on a myriad of nancial

regulatory topics including ntech and crypto-assets. Todd has an enormous breadth of

experience gained from more than 25 years on Wall Street at nancial services rms dealing

with both institutional and retail clients. Before joining Thomson Reuters, he served as a

Chief Compliance Ofcer and Chief Operating Ofcer at a registered investment adviser/

hedge fund for nearly a decade.

Contributors

Rabihah Butler — Enterprise Content Manager – Thomson Reuters Institute

Alex Robson — Managing Editor - Thomson Reuters Regulatory Intelligence

Daniel Seleanu — Commissioning Editor - Thomson Reuters Regulatory Intelligence

Gregg Wirth — Content Manager - Thomson Reuters Institute

© Thomson Reuters 2023

Suspicious Activity Reports 2023 42

Thomson Reuters

Thomson Reuters is a leading provider of business information services. Our products

include highly specialized information-enabled software and tools for legal, tax, accounting

and compliance professionals combined with the world’s most global news service –

Reuters. For more information on Thomson Reuters, visit tr.com and for the latest world

news, reuters.com.

Thomson Reuters Regulatory Intelligence

Thomson Reuters® Regulatory Intelligence is a market leading solution that empowers you

to make well-informed decisions to condently manage regulatory risk, while providing the

tools to make proactive decisions and action change within your organization. It has been

developed with a full understanding of your compliance needs – locally and globally, today

and in the future.

Thomson Reuters Institute

The Thomson Reuters Institute brings together people from across the legal, corporate, tax

& accounting and government communities to ignite conversation and debate, make sense

of the latest events and trends and provide essential guidance on the opportunities and

challenges facing their world today. As the dedicated thought leadership arm of Thomson

Reuters, our content spans blog commentaries, industry-leading data sets, informed

analyses, interviews with industry leaders, videos, podcasts and world-class events that

deliver keen insight into a dynamic business landscape.

Visit thomsonreuters.com/institue for more details.

© Thomson Reuters 2023 TR3460290 / 5-2023