This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 1 of 6 plazahomemortgage.com

FHA Fixed and ARM Program Guidelines

Correspondent

Revised 8/2/2024 rev. 136

Summary

FHA conforming and high balance Fixed Rate and 5/1 ARM. All loans must be eligible for FHA

Insurance Endorsement.

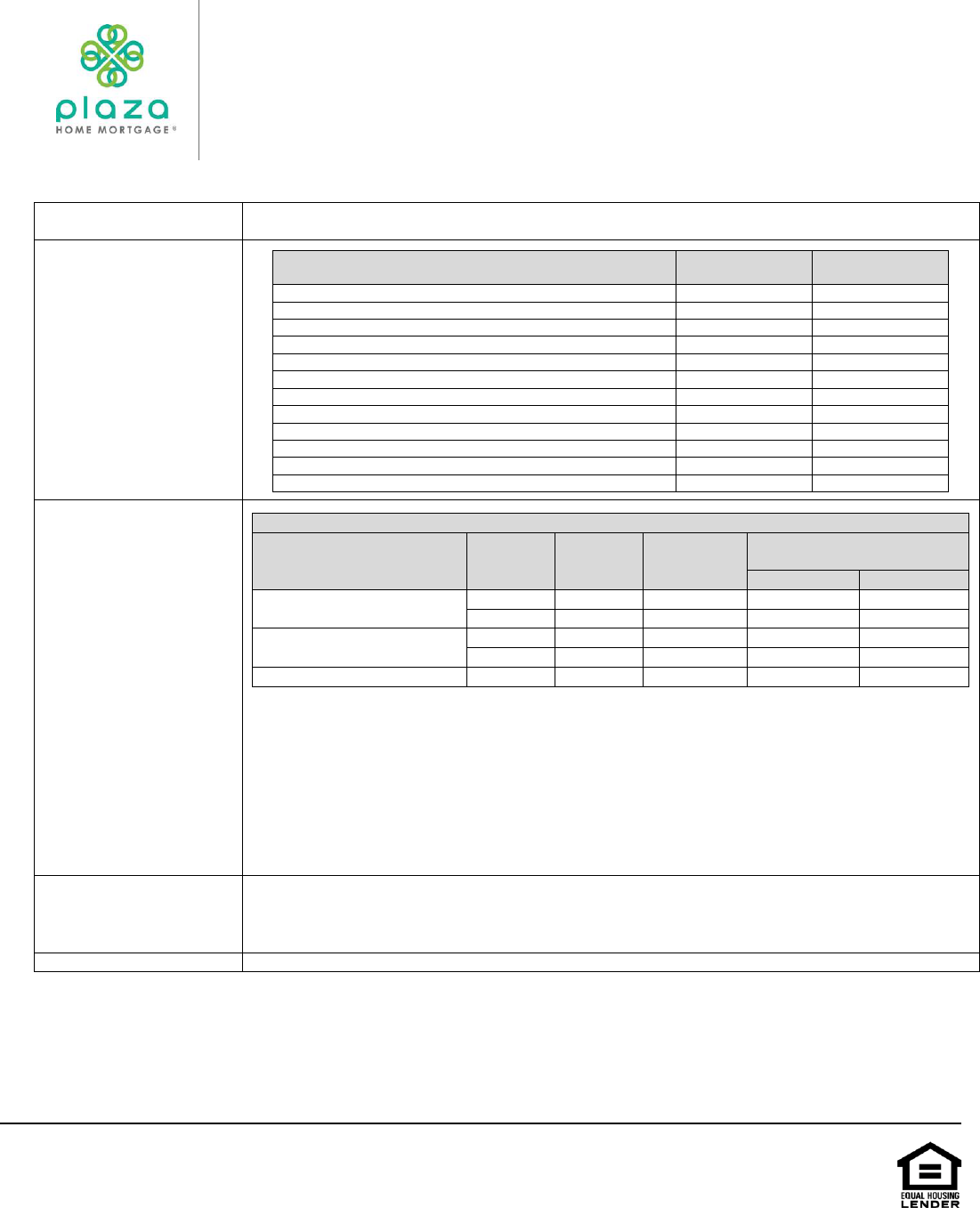

Products

Product Name

Product Code

Available Term

In Months

FHA 15 Year Fixed

FHA150

180

FHA 30 Year Fixed

FHA300

181-360

FHA 5/1 ARM

FHA51T

360

FHA 15 Year Fixed High Balance

FHA150HB

180

FHA 30 Year Fixed High Balance

FHA300HB

360

FHA 5/1 ARM High Balance

FHA51THB

360

FHA 30 Year Fixed w/3-2-1 Buydown

FHA30BD321

360

FHA 30 Year Fixed w/2-1 Buydown

FHA300BD21

360

FHA 30 Year Fixed w/1-0 Buydown

FHA300BD10

360

FHA 30 Year Fixed High Balance w/3-2-1 Buydown

FHA300HBD321

360

FHA 30 Year Fixed High Balance w/2-1 Buydown

FHA300HBD21

360

FHA 30 Year Fixed High Balance w/1-0 Buydown

FHA300HBD10

360

Eligibility Matrix

Conforming and High Balance

3

– Primary Residence

Purpose

LTV

CLTV

Min Credit

Score

Max DTI

Underwriting Method

AUS

Manual

Purchase

96.5%

96.5%

1

580

Per AUS

Per 4000.1

90%

90%

1

550

Per AUS

31/43%

Rate/Term Refinance or

Simple Refinance

97.75%

2

97.75%

2

580

Per AUS

Per 4000.1

90%

90%

1

550

Per AUS

31/43%

Cash-out Refinance

4

80%

80%

550

Per AUS

Per 4000.1

5

1.

On conforming balance purchase transactions there is no maximum CLTV for secondary financing provided

by Governmental Entities, HOPE grantees, or by HUD-approved Nonprofits. In addition, second liens held

by a family member are eligible up to a maximum 100% CLTV. Refer to 4000.1.II.A.4-Secondary

Financing (TOTAL) for eligible secondary financing, CLTV limits, and Borrower Minimum Investment (MRI)

requirements.

2.

Maximum LTV is 85% if the borrower has not owned and occupied the property for the last 12 months. If the

property has been owned less than 12 months and has been owner occupied since acquisition then the

LTV is not restricted to 85%. Seasoning is based on case number assignment date.

3.

Manufactured Housing not eligible for High Balance loan amounts.

4.

Manufactured Housing Cash-out: Multi-wide only. Single-wide not eligible for cash-out.

5.

Manually underwritten loans with Credit Scores below 580 may not exceed 31/43% ratios.

4506-C / Tax Transcripts

• A signed 4506-C for all years in which income was used in the underwriting decision are

required

• Refer to Plaza’s Delegated Correspondent Credit Overlay Matrix for tax transcript

requirements

Appraisal

Refer to 4000.1.II.B.1-Appraiser and Property Requirements

This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 2 of 6 plazahomemortgage.com

ARM Adjustments

Characteristic

ARM

Amortization Term

30 years

Index

Treasury, weekly average of U.S, Treasury securities adjusted to a constant

maturity of one year.

Margin

2.000%

Life Floor

5% below the start rate, but never lower than the margin.

Interest Rate Caps

Product

First

Adjustment

Subsequent

Adjustments

Lifetime

5/1

1%

1%

5%

Interest Rate

Adjustment Date

5/1

The first adjustment is 60-66 months after the first payment

date. Refer to Plaza’s Correspondent Seller Guide for

ARM interest rate change dates.

After the initial fixed period, the interest rate may adjust annually.

Payment

Adjustment Date

The payment adjustment date is the first of the month following the interest

rate adjustment and every 12 months thereafter.

Conversion Option

Not allowed.

Temporary

Buydowns

Not allowed.

Borrower Eligibility

Ineligible Borrowers:

• Partnerships

• Corporations

• Guardianships

• Life Estates

• LLCs

• Non-Revocable Inter Vivos Trusts

• Foreign nationals

• Borrowers with diplomatic immunity

• Charitable organizations

• Non-profit agencies

• State or local government agencies

Note: Deferred Action for Childhood Arrivals (DACA) program recipients are eligible for FHA

programs.

Deferred Action for Childhood Arrivals (DACA) program recipients:

• Must be borrower’s principal residence;

• Borrower must have a valid Social Security Number (SSN), except for those employed by the

World Bank, a foreign embassy, or equivalent employer identified by HUD;

• Borrower must be eligible to work in the U.S. as evidenced by the Employment Authorization

Document issued by USCIS, and

• The borrower satisfies the same requirements, terms and conditions as those for U.S. citizens.

The Employment Authorization Document is required to substantiate work status. If the Employment

Authorization Document will expire within one year and a prior history of residency status renewals

exists, the lender may assume that continuation will be granted. If there are no prior renewals, the

lender must determine the likelihood of renewal based on information from the USCIS.

A borrower residing in the U.S. by virtue of refugee or asylee status granted by the USCIS is

automatically eligible to work in this country. The Employment Authorization Document is not

required, but documentation substantiating the refugee or asylee status must be obtained.

Social Security Number:

• Each borrower on the loan transaction must have a valid Social Security number.

• ITIN (IRS Tax Identification Numbers) are not allowed.

This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 3 of 6 plazahomemortgage.com

Credit

Qualifying Credit Score:

• A tri-merge credit report is required on all loans

• Qualifying score:

o Where three scores are reported, the middle score is the qualifying score

o Where two scores are reported, the lowest score is the qualifying score

o Where only one score is reported, that score is the qualifying score

• Where the Mortgage involves multiple Borrowers, the lowest qualifying score of all borrowers is

used

• Where the Mortgage involves multiple Borrowers and one or more of the Borrowers do not have

a credit score (non-traditional or insufficient credit), the lowest qualifying score of the

Borrower(s) with credit score(s) is used

• At least one occupant borrower must have a credit score. Manual underwriting guidelines apply

for loans that receive a “Refer” recommendation where the co-borrower does not have a credit

score. Non-traditional credit must be established per FHA guideline requirements.

Housing Payment History:

• For purchases and refinances evaluated by an AUS, refer to 4000.1 II.A.4-Accept Risk

Classifications Requiring a Downgrade to Manual Underwriting for situations where the

loan must be manually downgraded.

o Refer to 4000.1.II.A.4 – Housing Obligations/Mortgage Payment History and 4000.1.II.A

Undisclosed Mortgage Debt for additional requirements.

• When the housing payment history is not evaluated by an AUS, or for Refer or Manually

Downgraded underwritten loans:

o There may be no history of any 30-day late mortgage or rental payments within the last 12

months.

o There may be no more than two 30-day late mortgage or rental payments in the previous 24

months.

o The housing payment history must be documented by:

▪ The credit report; or

▪ VOR received directly from the landlord (for landlords with no Identity of Interest with the

borrower); or

▪ VOM received directly from an institutional mortgage servicer; or

▪ Canceled checks that cover the most recent 12-month period.

• Borrowers who are living rent free are eligible provided the Mortgagee obtains verification

directly from the property owner that the borrower has been living rent-free and the amount of

time the borrower has been living rent free.

Revolving and Installment Accounts - Manually Underwritten Loans:

• Installment Accounts must have no more than 0 x 30 in the last 12 months and 2 x 30 in the last

24 months.

• Revolving Accounts must have no more than 2 x 60 or 0 x 90 in the last 12 months.

Down Payment / Gifts

Per FHA requirements.

Energy Efficient

Mortgages

Allowed per FHA Guidelines.

Escrow Accounts

An Escrow/impound account is required for property taxes and insurance on all FHA loans.

Geographic Restrictions

Hawaii:

• Properties in Lava Flow Zones 1 or 2 are not allowed.

• Manufactured housing not eligible.

Iowa: An attorney’s opinion of title is acceptable in lieu of a title policy, or a title policy may be

ordered through the Title Guaranty Division (TGD) of the Iowa Financial Authority.

Kansas: Properties located in the State of Kansas require the lender to obtain the market value.

Massachusetts: Septic system inspection required when a property is transferred to a different

owner (purchase money). All systems must be inspected within 2 years prior to the transfer of title to

the property served by the system. Inspections conducted up to 3 years before the purchase may be

eligible when accompanied by records demonstrating that the system was pumped at least once a

year during that time.

This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 4 of 6 plazahomemortgage.com

Montana: Lot size of the property may not exceed 40 acres.

Rhode Island: Manufactured housing not eligible.

West Virginia: Delegated deliveries only.

Good Neighbor Next

Door

Allowed per FHA Guidelines.

HUD REO

Allowed per FHA Guidelines.

Identity of Interest

The terms Identity of Interest and Non-Arm’s Length describe certain transactions between parties

with family or business relationships that may pose increased risk and warrant additional precautions

when evaluating that risk.

Conflicts of Interest:

Participants that have a direct impact on the mortgage approval decision are prohibited from having

multiple roles or sources of compensation, either directly or indirectly, from a single FHA-insured

transaction. These participants are:

• Underwriters

• Appraisers

• Inspectors

• Engineers

Indirect compensation includes any compensation resulting from the same FHA-insured transaction,

other than for services performed in a direct role. Examples include, but are not limited to:

• Compensation resulting from an ownership interest in any other business that is a party to the

same FHA-insured transaction; or

• Compensation earned by a spouse, domestic partner, or other Family Member that has a direct

role in the same FHA-insured transaction.

Participants that do not have a direct impact on the mortgage approval decision may have multiple

roles and/or sources of compensation for services actually performed and permitted by HUD,

provided that the FHA-insured transaction complies with all applicable federal, state, and local laws,

rules, and requirements.

Ineligible

• Temporary Buydowns for ARM transactions

• One-time close construction

• Borrower may not act as an interested party to a sales transaction for the subject if the builder

and/or property seller is a company owned by the borrower or where the borrower is a principal

agent, sales agent, loan originator, mortgage broker or partner for the builder or property seller.

• Realtor/loan broker acting as the listing agent as well as the mortgage originator/broker.

• Borrower is a principal of the title company and/or settlement agent for the subject transaction.

Loan Limits

For most single-family mortgage insurance programs, the maximum insurable amount is the lesser

of:

• The Nationwide Mortgage Limit for the area, usually a county or metropolitan statistical area

(MSA), or

• The applicable LTV limit, determined by a fixed percentage of the lesser of the sales price or the

appraised value.

• Manufactured Housing is not eligible for High Balance loan limits.

Maximum Base Loan Amount

Unit

Contiguous States

Hawaii

1

Standard

High Balance

Standard

High Balance

1

$766,550

$1,149,825

$1,149,825

N/A

2

$981,500

$1,472,250

$1,472,250

N/A

3

$1,186,350

$1,779,525

$1,779,525

N/A

4

$1,474,400

$2,211,600

$2,211,600

N/A

1.

There are no properties in Hawaii with loan limits higher than the applicable base conforming limits for 2024.

As a result, there are no High Balance limits specific for this state.

Maximum base loan amounts are county specific and may be lower in a particular county.

This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 5 of 6 plazahomemortgage.com

Manufactured Housing

• Must be classified as Real Property

• Single-wide and multi-wide allowed

• Single-wide manufactured homes are limited to purchase and rate/term refinance transactions

only

• Manufactured homes must have been built on or after June 15, 1976

• Manufactured homes must be at least 12 feet wide and have a minimum 400 square feet of

gross living area

• Leasehold properties are ineligible

• Condo projects, including site condos, comprised of manufactured homes are ineligible

• The manufactured home may not have been previously installed or occupied at another location

• All manufactured housing must meet FHA guidelines, restrictions in these Program Guidelines,

and Plaza’s Manufactured Housing Guidelines.

• Manufactured housing not eligible in states of Hawaii and Rhode Island.

• Manufactured Homes located within a Special Flood Hazard Area are not eligible unless a

FEMA National Flood Insurance Program (NFIP) Elevation Certificate (FEMA Form 086-0-33)

prepared by a licensed engineer or surveyor stating that the finished grade beneath the

Manufactured Home is at or above the 100-year return frequency flood elevation is provided,

and flood insurance under the NFIP is obtained.

Maximum Loans

A maximum of four Plaza loans is permitted to one borrower.

Property Eligibility

Ineligible Properties:

• Commercial property

• Cooperatives

• Condotels

• Geothermal homes

• Geodesic Domes

• Mobile homes

• Non-warrantable condos

• Timeshares

• Working farms, ranches, orchards

• Properties with C6 quality rating

• Properties with C5 or C6 condition rating

• Properties secured with PACE obligations or PACE like assessments

New Construction – Refers to Proposed Construction, Properties Under Construction and

Properties Existing less than One Year:

FHA treats the sale of an occupied Property that has been completed less than 1 year from

the issuance of the Certificate of Occupancy or local authority equivalent as an “existing”

Property.

• New Construction must comply with the minimum documentation requirements per Sections

II.A.8.i.i.i-v of the 4000.1 Handbook.

• Refer to Plaza’s FHA New Construction Documentation Requirements document.

Repair Escrows

Per FHA guidelines.

Escrow holdbacks are not allowed on manufactured housing.

Seasoning

Cash-Out Refinances of Government Loans:

• The borrower must have made at least six consecutive monthly payments on the mortgage that

is being refinanced beginning with the payment made on the first payment due date.

• The first payment due date of the refinance loan must occur no earlier than 210 days after the

first payment due date of the existing loan.

This information is provided by Plaza Home Mortgage and intended for mortgage professionals only, as a courtesy to its clients and is meant for instructional

purposes only. It is not intended for public use or distribution. None of the information provided is intended to be legal advice in any context. Plaza does not

guarantee, warrant, ensure or promise that information provided is accurate. Terms and conditions of programs and guidelines are subject to change at any

time without notice. This is not a commitment to lend. Plaza Home Mortgage, Inc. is an Equal Housing Lender. © 2024 Plaza Home Mortgage, Inc. Plaza

Home Mortgage and the Plaza Home Mortgage logo are registered trademarks of Plaza Home Mortgage, Inc. All other trademarks are the property of their

respective owners. All rights reserved. Plaza NMLS 2113. P.N.FHA Fixed and ARM Program Guidelines.G.136.8.2.24

Page 6 of 6 plazahomemortgage.com

Single Unit Approved

(SUA) Condos

• TOTAL Scorecard Accept required for LTV > 90%

• HUD Form 9991 along with all documents required per the FHA Single-Unit Approval

Document Checklist (FM-530) must be sent to Project Standards department for approval

• General SUA requirements are listed below. Refer to Plaza’s Project Standards for full SUA

requirements.

o Must be an established project with 5+ units

o Project with manufactured homes are not eligible

o 50% or more owner occupancy required

o Single Entity Ownership maximum of 10% for projects with 20+ units and maximum 1 unit for

projects with fewer than 20 units

o FHA Concentration maximum of 10% for projects with 20+ units and maximum 2 units for

projects with fewer than 20 units

Subordinate Financing

New or existing subordinate financing is allowed per the LTV/CLTV limits.

Properties with Property Assessed Clean Energy (PACE) obligations are ineligible.

• Any PACE obligations or liens must be paid and satisfied at or prior to closing.

• PACE liens may not be subordinated.

Temporary Buydowns

Temporary Buydowns are eligible subject to the following:

• 3-2-1, 2-1 and 1-0

• Purchase transactions only

• Qualify at the note rate

• Funds may come from the lender, borrower, seller or other eligible interested party

• Interested Party Contribution (IPC) limits apply when the source of funds is a party to the

transaction

• Buydown Agreement must be included in the loan file

Texas Home Equity

Cash out is not allowed in Texas.

Transactions

• Purchase

• Rate/Term Refinance

• Simple Refinance

• Cash-Out Refinance

Underwriting Method

All loans must be decisioned through FHA TOTAL Scorecard as submitted to DU, LPA, or

LoanScoreCard.