MONETARY POLICY

IMPLEMENTATION

IN SRI LANKA

July 2023

Central Bank of Sri Lanka

MONETARY POLICY

IMPLEMENTATION

IN SRI LANKA

Central Bank of Sri Lanka

July 2023

ISBN-978-624-5917-13-6

First Edition: July 2023

Published by the Central Bank of Sri Lanka, No 30, Janadhipathi Mawatha, Colombo 1, Sri Lanka.

For inquiries, comments and feedback please contact:

Domestic Operations Department

Central Bank of Sri Lanka

Email: [email protected]

Telephone: 011 2477189

Monetary Policy Implementation in Sri Lanka

Table of Contents

List of Acronyms .................................................................................................................................. 3

Preamble ............................................................................................................................................. 4

Part I: Monetary Policy Formulation .............................................................................................. 7

Central Bank Objectives and Monetary Policy ................................................................. 7

Monetary Policy Framework in Sri Lanka ........................................................................... 8

Monetary Policy Decision Making Process ........................................................................ 9

Part II: Monetary Policy Implementation .........................................................................................11

Understanding Monetary Policy Implementation .............................................................11

Liquidity Management in Monetary Policy Implementation ............................................11

Central Bank Liquidity in Liquidity Management ..................................................12

Key Monetary Policy Instruments ........................................................................................16

Policy Interest Rates and Open Market Operations(OMOs)................................16

Standing Facility ......................................................................................................20

Statutory Reserve Requirement (SRR).....................................................................20

Other Policy Instruments ..................................................................................................... 21

Part III: Transmission Mechanism of Monetary Policy .................................................................... 23

List of Acronyms

AWCMR Average Weighted Call Money Rate

CCPI Colombo Consumer Price Index

DOD Domestic Operations Department

EPF Employees’ Provident Fund

FIT FlexibleInationTargeting

IOD International Operations Department

LCBs Licensed Commercial Banks

LOLR Lender of Last Resort

MLA Monetary Law Act, No. 58 of 1949

MOC Market Operations Committee

MPC Monetary Policy Committee

OMOs Open Market Operations

PIs Participating Institutions

SDF Standing Deposit Facility

SDFR Standing Deposit Facility Rate

SLF Standing Lending Facility

SLFR Standing Lending Facility Rate

SPDs Standalone Primary Dealers

SRC Standing Rate Corridor

SRR Statutory Reserve Requirement

3

Monetary Policy Implementation in Sri Lanka

4

Preamble

The Government and the monetary authority of a country play a vital role in enhancing

economic welfare and the living standards of the people. In doing so, both the Government

and the monetary authority rely on certain macroeconomic policies. The objectives of such

macroeconomic policies are to ensure that the economy achieves non-inationary, stable

and sustainable growth, thereby enhancing the welfare of the society. This is achieved by

implementing macroeconomic policies to minimise uctuations in the macroeconomic

variables, such as the Gross Domestic Product (output), employment, and the general price

levels. Policies employed to achieve these objectives are generally two-fold: scal policy

and monetary policy. Accordingly, both scal and monetary policy are instrumental in

macroeconomic management and in particular, achieving macroeconomic objectives for

thebenetofthecitizens.

Fiscal policy of the Government is mainly related to taxation and government spending and

theirinuenceoneconomicconditions.FiscalpolicyoftheGovernmentcanensuretheoverall

economic stabilisation and growth. However, in general, it takes time to legislate taxes and

spending changes. Moreover, economic agents may take time to respond and adjust their

behaviourtoscalpolicychanges.Hence,monetarypolicyisgenerallyconsideredthemore

quick and effective mean of stabilising the economy, especially price levels.

Monetary policy involves the actions taken by the central bank to inuence the cost and

availability of money in the economy. Monetary policy actions employed by the central bank

aimtoachievepricestability(lowandstableination)andreduce economic uctuations,

commonly known as minimising the intensity business cycles. The central bank uses instruments

inuencingthesupplyofmoneyandcreditandalteringinterestratesintheeconomy.Hence,

adjustment to interest rates and money supply play an important role in an economy as it

affects the behaviour of the borrowers and lenders. These actions affect the general price

levels as well as employment, output of the economy and ultimately the welfare of the people.

Such effects of monetary policy ensure low and stable price levels and thus low ination.

Propercoordinationbetweenscalandmonetarypoliciesisvitallyimportanttoensurebetter

outcomes for the macroeconomy.

Thecentralbank,whichistheapexnancialinstitutionofacountrycarriesoutkeymonetary

andnancialfunctions.Suchfunctionsincludeissuingcurrency,conductingmonetarypolicy,

providing and regulating payment systems, acting as a lender of last resort, and conducting

nancialsectorsupervision,amongothers.Generally,acentralbankofacountryisestablished

as an independent institution, which is responsible for administering various statutes on money,

banking,andthenancialsector.

In implementing monetary policy to achieve the objective of price stability, a central bank

uses a range of policy instruments. In the modern context, the most important monetary policy

instrument is the use of policy interest rates and the open market operations, among several

other instruments. Any changes made to policy interest rates and other policy instruments are

meant to affect interest rates of money and capital markets and, in turn, affect interest rates

that nancial institutions deal with their customers. Accordingly, through such retail interest

rates,monetarypolicydecisionsinuenceconsumerspendingandbusinessinvestmentsand

overall demand in the economy.

Monetary Policy Implementation in Sri Lanka

5

In Sri Lanka, the Central Bank of Sri Lanka (referred to as ‘the Central Bank’ hereafter) is

mandated to undertake a vital role as the nation’s monetary authority. Accordingly, the

Central Bank is responsible for formulating and implementing monetary policy in Sri Lanka,

thereby operationalising several monetary policy instruments. As a part of achieving price

stability objective of the economy and thereby implementing monetary policy, the Central

Bank attempts to continuously communicate with market participants and the general public

in order to enhance transparency of monetary policy actions of the Central Bank. Accordingly,

the Central Bank disseminates information on its current and future policy direction, economic

developments and the outlook, and the likely path for future monetary policy decisions. Such

information is crucial for conducting monetary policy effectively and managing expectations

of the general public.

This pamphlet aims at enhancing the awareness and understanding of the general public

about the role of the Central Bank in implementing monetary policy in Sri Lanka. Having a

clear understanding of the tools and policies used in monetary policy implementation would

helpthestakeholdersinthenancialsystemandthegeneralpublictobetteraligntheiractions

in line with the monetary policy decisions of the Central Bank and their intended outcomes.

This pamphlet consists of three parts. Part I provides a background discussion on monetary

policy, including monetary policy objectives, frameworks, and decision making processes. Part

II of the pamphlet discusses the implementation of monetary policy, including market liquidity

management and monetary policy instruments in the context of Sri Lanka. Part III discusses the

monetary transmission mechanism.

Monetary Policy Implementation in Sri Lanka

Figure 1: Central Bank Mandate and Monetary Policy Implementation

Mandate

Price Stability

Indicator

Low and Stable

Ination

Strategy

Monetary Policy

Actions

Implementation

of Actions to

inuenceCost

and Availabiltiy of

Money

The Central Bank conducts monetary policy to achieve the

objective of maintaining economic and price stability (low and

stableination).

The Central Bank follows a Flexible Ination Targeting (FIT)

framework to maintain headline ination (based on the

Colombo Consumer Price Index-CCPI) between 4-6 per cent

over the medium term.

Monetary policy actions of the Central Bank stimulate or

dampenaggregatedemandandhelptoreachtheination

target by adjusting short term interest rates. The Average

Weighted Call Money Rate (AWCMR) serves as the operating

target of the FIT framework.

The Central Bank reviews and takes decisions on the monetary

policy stance and communicates the monetary policy decisions

to the general public.

AWCMR inuences other short term and long term

interest rates in the economy, including the lending and deposit

ratesofnancialinstitutions,whichaffecteconomicdecisions

of the stakeholders.

A reduction in interest rates stimulates consumer spending

and business investment and supports economic growth.

An increase in interest rates dampens consumer spending

and business investment, thereby resulting in a slowdown in

economicgrowthanddecelerationinination.

6

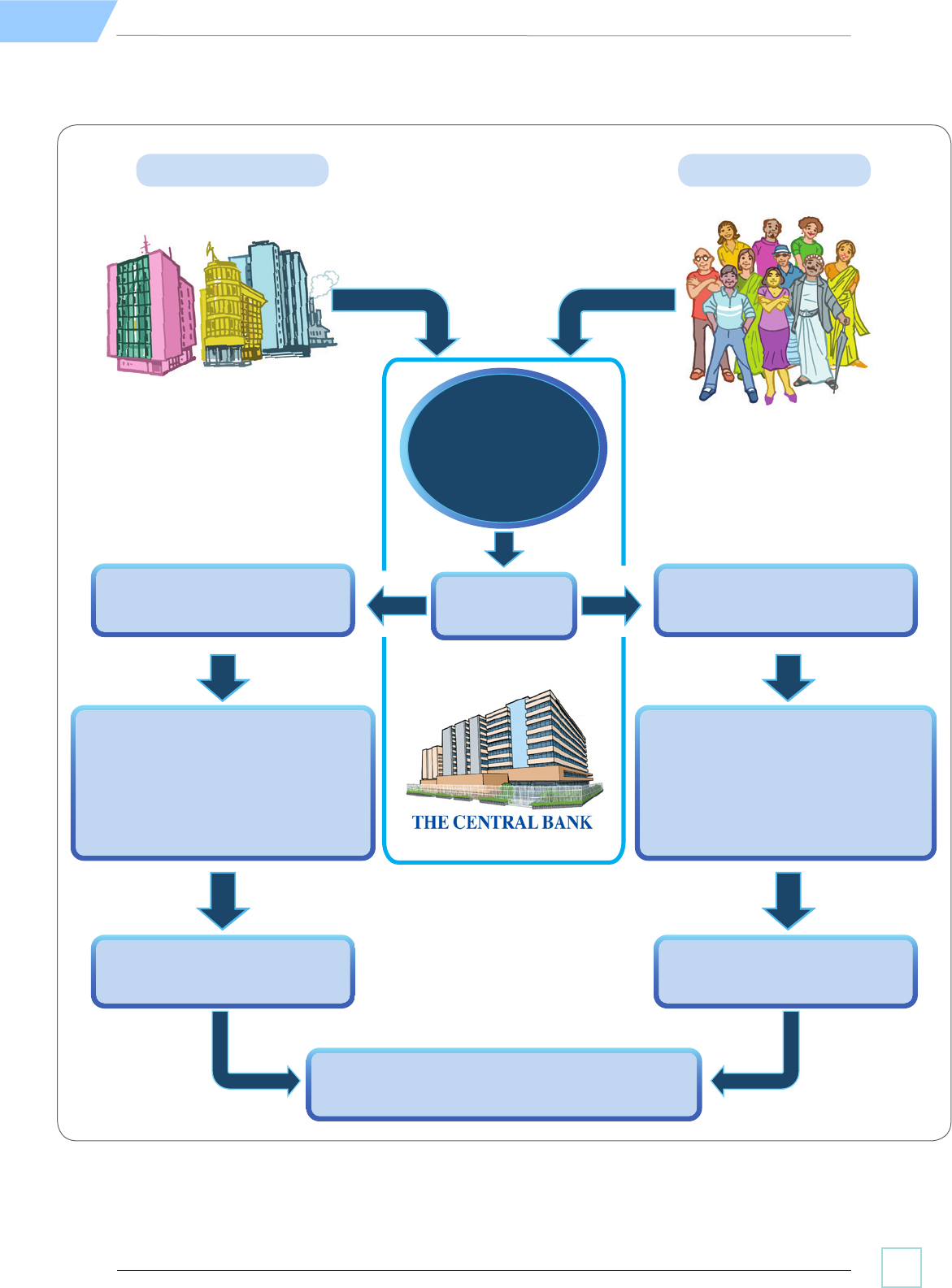

Figure 2: Monetary Policy Formulation and Implementation in Sri Lanka - A Snapshot

Monetary Policy Implementation in Sri Lanka

The Central Bank attempts to maintain AWCMR within SRC by

managing liquidity in the domestic money market using Open

Market Operations (OMOs).

The Central Bank deploys policy interest rates, namely the

Standing Deposit Facility Rate (SDFR) and the Standing

Lending Facility Rate (SLFR), that form the Standing Rate

Corridor (SRC) to signal the monetary policy stance along

with the other policy instruments.

Standing Deposit Facility Rate (SDFR)

Standing Lending Facility Rate (SLFR)

Standing Rate Corridor and AWCMR

SLF

SDF

Jun -12 Apr-13 Feb-14 Dec-14 Oct-15 Aug-16 Jun-17 Apr-18

CBSL POLICY RATES

Part I: Monetary Policy Formulation

The Central Bank attempts to achieve two core objectives, namely, maintaining economic and

pricestability,andmaintainingnancialsystemstability.Pricestabilityensuresthatthereareno

wideuctuationsinthegeneralpricelevelintheeconomyreectinglowandstableination,

whichpreservesthevalueofmoney.Whentherearenomaterialpriceuctuations,economic

agents can make rm decisions with certainty on their consumption and investment, thus

enablingefcientallocationoflimitedresources.ThismandateoftheCentralBankreectsthat

price stability is an essential condition

for creating a stable economic and

businessenvironment,whichisbenecial

to economic activity,employment, and

the welfare of the general public.

Financial system stability refers to

the ability of the nancial system

to withstand both internal and

external shocks such as economic

recessions and economic imbalances,

commodity and assets price bubbles,

etc. A stable nancial system supports

mobilising savings and allocating them

to productive investment, managing

risks, and facilitating payments and

settlements even under challenging

economic circumstances. Hence,

nancialsystemstabilityensuresaconduciveeconomicandnancialenvironmentformarket

participants, which facilitates investment, economic growth and welfare of the people. These

two objectives are interrelated as actions taken to ensure price stability are transmitted to the

economyviathenancialsystem.

The Central Bank conducts monetary policy to achieve price stability in the economy. Monetary

policyinvolvesactionstakenbyacentralbanktoinuencethecostandavailabilityofmoney/

credit in the economy to achieve price stability. By controlling the cost of money (interest rate)

and amount of money (currency and deposits), or the amount of credit (lent by banks and

othernancialinstitutions),acentralbankisabletoinuenceeconomicactivities.Bydoingso,

acentralbankcaninuenceconsumptionandinvestmentspendingintheeconomy,thereby

affectingeconomicgrowthandination.

The Central Bank is responsible for conducting national monetary policy in Sri Lanka as per the

powers vested under governing laws relating to establishment and enforcement of Central

Bank’s operations. Accordingly, the Central Bank adopts monetary policy decisions with the view

of achieving economic and price stability. With the aim of achieving this objective, the Central

Bankattemptstomaintaininationasmeasuredbytheyear-on-year(Y-o-Y)changeintheCCPI

within the range of 4-6 per cent over the medium term. Although there could be deviations from

the target temporarily due to various shocks, the Central Bank aims at maintaining price stability

over the medium term through appropriate monetary policy actions.

7

What is the

role of

a central bank?

To maintain

stability in the general

price level and the overall

economy, including the

stability of the

nancial system

Central Bank Objectives and Monetary Policy

Monetary Policy Implementation in Sri Lanka

Monetary Policy Framework in Sri Lanka

The monetary policy framework of Sri Lanka has evolved signicantly over time. Since the

establishment of the Central Bank in 1950 and until the introduction of economic liberalisation

policies in 1977, Sri Lanka’s monetary policy framework was primarily based on exchange rate

considerationstoxthevalueoftheSriLankarupeetoaninternationalcurrency.Underthis

xedexchangerateregime,theimplementationofdomesticmonetarypolicywasconstrained

anddomesticinationwasaffectedbyforeignination.

After implementing open economy policies from 1977, the Central Bank gradually adopted

anominalanchortocontrolinationandmovedawayfromdirectcontrols,whileadopting

market based monetary policy tools. The introduction of market based monetary policy tools

also aimed at strengthening savings mobilisation and improving the efciency of resource

allocation, which had been suppressed by direct interest rates, exchange rates or credit

controls. A nominal anchor for monetary policy refers to a variable that the central bank uses

to manage actions and pin down expectations of economic agents about the nominal price

level and its path or about what the monetary authority would do with respect to achieving

that desired path. Generally, two types of nominal anchors, namely, quantity based nominal

anchors and price based nominal anchors are used by the Central Bank. The quantity based

nominal anchor targets money, while the price based nominal anchor targets interest rates or

exchange rates.

During the early 1980s, the Central Bank adopted Monetary Targeting (MT) as its monetary

policy framework and under MT, monetary aggregates were used as the key nominal anchor

in the conduct of monetary policy in Sri Lanka. In particular, reserve money (comprised of

currency in circulation bank deposits with the Central Bank) was used as the operational

target, which is under direct control of the Central Bank, and broad money was used as an

intermediatetargettoachieveinationoutcomes.

8

1980-

2014

Prior to

1980

2015-

2019

2020

onwards

Exchange

Rate

Considerations:

• Maintaining

axed

exchange

rate regime

• No explicit

operating

target

Monetary

Targeting (MT)

Framework:

• Relying

on monetary

aggregates

• Operating

Target-

Reserve

Money

Enhanced

Monetary

Policy

Framework:

• Gradually

declining

importance

of monetary

aggregates

• Operating

Target-

AWCMR

Flexible

Ination

Targeting (FIT)

Framework:

• Increased

importance

on price and

real output

stability

• Operating

Target-

AWCMR

Figure 3: Evolution of the Monetary Policy Framework in Sri Lanka

Monetary Policy Implementation in Sri Lanka

9

Monetary Policy Decision Making Process

At present, the responsibility of decision making on monetary policy is vested with the Monetary

Board of the Central Bank. The Monetary Board usually reviews the monetary policy stance

eight times a year. The dates of these eight meetings are published at the beginning of the

year. At each meeting of the Monetary Board, the Monetary Policy Committee (MPC) of the

Central Bank, chaired by the Governor, provides a comprehensive analysis on the outlook

of the economy, along with developments in the domestic and global macroeconomy and

nancialmarkets.Further,theMPCsubmitsrecommendationsonthemonetarypolicystance

to the Monetary Board based on its technical analyses and the forecasts.

The Monetary Board adopts appropriate monetary policy decisions that best suit the current

and expected economic conditions. For instance, if medium term projections suggest that

the economy is overheating due to fast increasing aggregate demand, the Monetary Board

may increase the policy interest rates and adopt a contractionary monetary policy stance

(monetary tightening) in order to stem aggregate demand pressures and minimise risks

associated with high ination. Generally, the Central Bank adopts a tight monetary policy

stanceduringtimesofhighinationorhighexpectedination,bysettingpolicyrateshigher,

absorbing liquidity through sales of government securities under OMOs and/or increasing

the Statutory Reserve Requirement (SRR). On the other hand, when medium term projections

suggestsloweconomicgrowthandlowinationpressuresoreconomicdownturnorrecession,

the Monetary Board would follow an expansionary monetary policy (monetary easing) to

stimulate the economy. An expansionary policy is intended to boost consumer spending and

promote investment by lowering policy interest rates and injecting liquidity into the economy

through purchases of government securities under OMOs, and/or lowering the SRR. Such

monetary policy decisions are then communicated to the general public by the Central Bank.

Underthisframework,any changes in moneysupplywerethekey factors inuencingprice

stability. Hence, monetary operations were broadly aligned to control the money supply of

the country. However, due to high volatility and the weakening relationship between money

supplyandination,theroleofmonetarytargetsasanominalanchorbecameuncertainand

complicated the Central Bank’s communication strategy, compelling the Bank to upgrade its

monetary policy framework.

Accordingly,sincetheearly2000s,theCentralBankkeptintroducingseveralmodicationsto

the monetary policy framework. Since 2015, the Central Bank has conducted monetary policy

withinanenhancedmonetarypolicyframeworkwithfeaturesofbothMTandFlexibleInation

Targeting(FIT),mainlyduetotheweakenedrelationshipbetweenmoneysupplyandination.

The FIT framework has been instrumental in further improving expectation management,

transparency, and credibility of monetary policy. In the FIT framework, the Central Bank adjusts

monetarypolicytoolstoachieveaninationtargetof4-6percentoverthemediumterm,

measuredintermsofCCPIbasedheadlineination,whilesupportingtoachievesustainable

economic growth.

The operating target is a variable that a central bank can effectively control in support of the

achievement of monetary policy objectives. Accordingly, at present, AWCMR, which is the

prime indicator of interbank call money market, is used by the Central Bank as its operating

target.

Monetary Policy Implementation in Sri Lanka

10

Economic Research

Department and Other

Relevant

Departments

Provide

comprehensive

analyses on current

economic status

and outlook

Domestic Operations

Department: Conducts

Domestic Money Market

Operations

Managing liquidity in

the domestic money

market to steer short

term interest rates

Market

Operations

Committee (MOC)

Decides the

actions on

domestic money

market and

domestic foreign

exchange market

operations on a

daily basis

International Operations

Department: Conducts

Foreign Exchange

Market Operations

Managing liquidity

in the domestic

foreign exchange

market to avoid large

uctuations in the

exchange rate, while

maintaining foreign

exchange

reserves at an

adequate level

* Under the proposed Central Bank Act, monetary policy decision making power is vested with the Monetary Policy Board.

Decision on

Monetary Policy

Stance

Monetary Policy

Committee (MPC)

Reviews and evaluates

factors on monetary

and macro-economic

developments to make

recommendations to

the Monetary Board

Technical

Inputs

(Data,

Information

and

Analyse)

Implementation

Communication

Monetary Policy

Decision

Monetary Policy

Communication

• Press releases and press

conferences

• Seminars and webinars

• Interviews and

discussions

• Social media publicity

Recommendations

Figure 4 : Monetary Policy Decision Making Process

(Stakeholders and Functions)

Monetary Policy Implementation in Sri Lanka

Monetary Board*

Deliberates on

the appropriate

monetary policy

stance

11

Understanding Monetary Policy Implementation

Monetary policy Implementation is the use of various monetary policy tools to operationalise

the monetary policy decisions taken by the Central Bank. The monetary policy decision is

operationalised by adjusting the quantity (money supply, i.e., the total volume of money

comprisedofcurrencyheldbythepublicanddepositsheldatnancialinstitutions)andprice

of money (interest rate) through monetary policy instruments, particularly, relevant to the

domestic money market. The Central Bank’s operations in the domestic foreign exchange

market also affect domestic money market conditions.

In the context of Sri Lanka, monetary policy implementation is carried out by respective

departments of the Central Bank in line with the decisions of the Monetary Board. Accordingly,

the Domestic Operations Department (DOD) carries out monetary operations in the domestic

money market, while the domestic foreign exchange market related transactions are carried

out by the International Operations Department (IOD).

The Central Bank uses an array of monetary policy instruments to make an impact on the

domestic market conditions. The policy interest rates, OMOs, and the SRR on deposit liabilities

of the Licensed Commercial Banks (LCBs) remain the key monetary policy instruments used in

monetary policy implementation in Sri Lanka. The objective of monetary policy implementation

using these instruments is to maintain the short term interest rates at a level in line with the

monetary policy stance of the Central Bank so as to achieve the objective of price stability.

The implementation of monetary policy is facilitated by the Participating Institutions (PIs) of the

domestic money market. Participation of such PIs helps to transmit the impact of monetary

policy actions to the money market and then to the overall interest rate structure of the

economy.

Part II: Monetary Policy Implementation

Liquidity Management in Monetary Policy Implementation

Liquidity management remains the central element of monetary policy implementation by

acentralbank.Itisdenedastheframework,setofinstrumentsandespeciallytherulesand

procedures that the central bank follows in managing the amount of bank reserves (liquidity)

in order to control their price, i.e., short term interest rates consistent with its ultimate goal

of price stability. Hence, liquidity remains an important variable in facilitating the process of

monetary policy implementation, as market interest rates and credit creation are closely

related to liquidity.

Accordingly, the framework for estimating and forecasting liquidity by a central bank invariably

forms the initial step of monetary policy implementation. It determines the type of monetary

operations that needs to be conducted by the central bank with the market participants on

a daily basis. Proper understanding and close surveillance of liquidity are critically important

as the selection of the tools and strategies of monetary implementation depends largely on

liquidity conditions. In fact, an accurate estimation of liquidity helps effective implementation

of monetary policy decisions taken by the Central Bank, in terms of steering the AWCMR, at a

desirable level and in the desired direction as per the monetary policy stance of the Central

Bank.

Monetary Policy Implementation in Sri Lanka

In general, banks hold cash in a

central bank account to meet their

day today settlement obligations. In

addition, the central bank requires

all banks requiring them to keep a

certain portion of banks’ deposit

liability with the central bank account

to prevent banks from lending all

deposits to their customers, which

is generally known as the reserve

requirement. Banks keep this reserve

in the same account which is used

to make their daily payments. In

Sri Lanka, all LCBs maintain reserve

balances with the Central Bank

to full the SRR and to meet their

day-to-day settlement obligations

(clearing purposes) as a key

depository institution for money

creation. The reserve balances

maintained by banks at the central bank to full the reserve requirement, remain the key

component of central bank liquidity management.

The concept of ‘central bank liquidity’ is different from the concept of market liquidity, which

is generally seen as a measure of the ability of market participants to undertake securities

transactions without triggering large changes in their prices. In addition, the term ‘liquidity’ is used

with several meanings and connotations, depending on the context within which it is being used.

Thesumofthereservebalances,i.e.,reservedepositsofnancialinstitutions(alsoknownasthe

balances in the current account, settlement account or clearing balances) held with the central

bank on a particular day is considered the liquidity with the central bank for monetary policy

implementation.

Accordingly,centralbankliquiditydependsontheseactualbalancesheldbynancialinstitutions

in their reserve accounts with the central bank. For instance, if all LCBs in Sri Lanka hold Rs. 150

billion in aggregate in their respective reserve accounts at the Central Bank on a given day

for the purpose of covering their SRR obligation and to meet their clearing requirements, the

overnight liquidity position of that particular day amounts to Rs. 150 billion.

Individual LCBs (Participating Institutions) can borrow and lend these funds in the interbank market.

However, for the system as a whole, the only source of these funds is the central bank itself.

Accordingly, the liquidity position can only be changed due to the transactions of the central

bankwithitscounterpartiesasreectedbythechangesinitsbalancesheet.Inthiscontext,the

factors that determine central bank liquidity are broadly categorised into two main subgroups,

i.e., autonomous factors and monetary operations related factors.

Autonomousfactorsaffectingliquiditycanbedenedastheitemsinthecentralbankbalance

sheet,excludingthereserveaccountsofnancialinstitutions,whosechangeisindependentof

the direct control of the central bank. The most important autonomous factors are the net foreign

12

Monetary Policy Implementation in Sri Lanka

Central Bank Liquidity in Liquidity Management

Why managing

liquidity is

important for the

Central Bank?

Managing

liquidity helps to

steer short term

interest rates

in line with the monetary

policy stance

13

Monetary Policy Implementation in Sri Lanka

Liquidity Reducing Factors

Liquidity Enhancing Factors

Figure 5: Factors Contributing to Changes in Central Bank Liquidity

• Sale of foreign exchange in the

domestic market by the central

bank

• Sale of foreign exchange by the

central bank to the Government

for repayment of foreign currency

denominated loans of the

Government

• Currency withdrawals by banks

from the central bank

• Maturing/retiring of government

securities held by the central

bank

• Repayment loans and advances

obtained by PIs from the central

bank

• Sale of government securities

to the secondary market by the

central bank (repo auctions)

• Sale of government securities

held by the central bank on an

outright basis

• Issue own securities by the

central bank

• Provide standing deposit facility

to PIs by the central bank

• Purchase of foreign exchange

from the domestic foreign

exchange market by the

central bank

• Purchase of foreign currency

denominated loan receipts of

the Government by the central

bank

• Deposit of currency at the

central bank by banks

• Purchase of government

securities by the central bank

from the primary market

• Release of central bank prots

to the Government

• Grant advances to the

Government by the central

bank

• Provision of loans and

advances to PIs by the central

bank

• Purchase of government

securities from the secondary

market by the central bank

(reverse repo auctions)

• Purchase of government

securities by the central bank

on an outright basis

• Retire of own securities issued

by the central bank

• Provide standing lending

facility

to PIs

by the central

bank

Autonomous Factors

Monetary Operations

14

Monetary Policy Implementation in Sri Lanka

assets of the central bank, currency in circulation, and the balances of government current

accounts with the central bank. The change in these items provides or withdraws (increases or

reduces)liquidityandthusdirectlyandindependentlyaffectsthereserveaccountsofnancial

institutions held with the central bank. For example, foreign currency transactions such as

purchases of foreign currency in the market by the central bank and foreign currency loan

receipts of the Government sold to the central bank lead to changes in net foreign assets of

the central bank and increase the reserve balances of nancial institutions, and increase in

liquidity. Further in the context of Sri Lanka, the provisional advances to the Government by the

Central Bank cause increase in net credit to the Government by way of depositing money to the

reserve account of a LCB maintained at the Central Bank on behalf of the Government, thereby

causing an increase in liquidity. Thus, any transaction that changes the balance sheet of the

centralbankbycreditingordebitinganyreserveaccountmaintainedbyanancialinstitution

would cause changes to the central bank liquidity position.

A central bank decides the volume and nature of monetary operations required to be

conducted in line with the prevailing monetary policy stance and based on the daily liquidity

forecast prepared on account of the changes in autonomous factors. Accordingly, the second

subgroup of the factors that determines the reserve levels (central bank liquidity) comprises of

the monetary operations, mainly the OMOs of a central bank.

The impact on liquidity due to the conduct of OMOs can be explained using the following

example. Assume that the Central Bank purchases government securities in the secondary

market from LCBs operating in Sri Lanka. Then, the Central Bank needs to pay them by crediting

their reserve accounts at the Central Bank, in effect, causing a rise in the balances of the

respective reserve accounts of LCBs, thereby increasing liquidity level. In the same way, when

the Central Bank sells securities to LCBs, the resultant impact on reserve accounts and liquidity

would be the opposite. Accordingly, a host of factors in combination provides an estimate of

the overall reserve balance of LCBs held with the Central Bank (see Figure 5).

The balance in the reserve account of LCBs can be, on a daily basis, lower or higher than the

reserve requirements imposed by the Central Bank although they need to cover the reserve

position on an average basis over a specied period. For example, assume that LCBs on

aggregate basis should maintain a balance of Rs. 150 billion based on the current level of SRR.

Onaparticularday,ifsuchreservebalancefallstoRs.135billion,LCBsshouldfulltherequired

level of reserves on average over a 15 day period, which is termed as the reserve maintenance

period. Accordingly, at the end of the reserve maintenance period, LCBs have to full their

reserve requirements for the reserve period, which is determined based on the deposit level of

individual LCB. This means that the average of the current account balances of the LCB over a

maintenance period must be at least equal to the minimum reserve requirement.

However, in reality, LCBs normally hold some excess reserves as the intraday transactions of banks

are uncertain or there could be some shortage of reserves due to unforeseen or unplanned

transactions. Accordingly, decit or excess liquidity is dened as the difference between the

balance in the reserve accounts held by LCBs and the level of their required reserves on a given

day. The banking system is considered in excess (excess liquidity) on a given day if the deposit

balances of LCBs with the Central Bank are higher than the balance that they would need

to maintain in their reserve account under the SRR requirement. For example, if the required

reserve level on a given day is Rs. 150 billion and the actual balance in the LCBs’ account with

the Central Bank is Rs.165 billion, then the amount over the required liquidity of Rs.15 billion is

consideredexcessliquidity.Incontrast,thebankingsystemisconsideredshort(decitliquidity)

on a given day, if the deposit balances of LCBs with the Central Bank are lower than the balance

15

Monetary Policy Implementation in Sri Lanka

that they would need to maintain on account of the SRR requirment.

LCBs individually manage their excess liquidity/reserves by either lending in the interbank

money market or parking the excess at the Central Bank for different tenures under OMO

auctions or on overnight basis under the Standing Deposit Facility (SDF) as the excess reserves

are unremunerated if it was held idle in the SRR account. On the other hand, when a bank is

in a short position, such short is generally funded through interbank borrowings. Accordingly,

whenfulllingtheliquidityrequirements,LCBsmayusetheinterbankcallmoneymarket,which

is an overnight or short term market for LCBs to meet their overnight liquidity requirements

by allowing them to borrow and lend money among each other without collateral. These

transactionsareveryshortterminnatureandreectthedemandforandsupplyofliquidity

in the market. However, if any bank could not fully cover its liquidity requirement through the

interbank bank, they will have to borrow from the Central Bank under OMO auctions or through

the overnight Standing Lending Facility (SLF).

Inmanagingexcessordecitliquiditybyacentralbank,itisparamounttohaveaneffective

framework for monetary operations. This is due to the impact of liquidity movements on the

interest rates of the markets and the economy. For example, when there is excess liquidity with

LCBs, there could be a tendency to induce a downward bias on AWCMR below the desired

level. Hence, in the event of excess liquidity, the Central Bank would conduct monetary

operations to absorb the excess to prevent an undue decline in the short term interest rates.

Similarly, when there is a liquidity shortage, there is a tendency to push AWCMR above the

desiredlevel.Hence,intheeventofaliquiditydecit,theCentralBankmaysupplyliquidity

through its monetary operations to meet market requirements, thereby minimising any undue

pressure on interest rates. Hence, absorptions or injections of liquidity are instrumental for the

Central Bank to steer the interest rates, in particular AWCMR which is the operating target

of monetary policy, in the context of Sri Lanka, thereby affecting the cost and availability of

money and credit in the broader economy.

Liquidity provision is linked with the core tasks within the central bank mandate. It constitutes

an essential pillar for the smooth functioning of the payments system and hence, safeguarding

nancial stability and for transmission of monetary policy. Adequate liquidity supports the

smoothfunctioningofthepaymentsystemintheeconomy,ensuringsufcientfundstohonour

paymentobligations.Althoughbankscanfullliquidityneedsofoneorafewinstitutions,they

cannot cover the entire needs of the system. However, the central bank can provide liquidity

to cater to the needs of the entire system and play an important role in regulating liquidity

inthenancialsystembylendingto,orborrowingfrom,nancialinstitutions.Inthatrespect,

proper management of liquidity through close monitoring and timely actions by the central

bank will ensure healthy levels of liquidity in the market, which is vital in stabilising interest rates

and ensuring the smooth functioning of the payment and settlements systems. Therefore,

liquidity management plays an important role in attaining stability in the interest rates, the

moneymarketandtheoverallnancialsysteminaneconomy.

16

Monetary Policy Implementation in Sri Lanka

Key Monetary Policy Instruments

Figure 6: Policy Instruments of the Central Bank

Policy Interest Rates and Open Market Operations (OMOs)

At present, the Central Bank predominantly implements country’s monetary policy under a

market based system of active OMOs. The primary objective of OMOs is to manage liquidity

levelsinthebankingsystemandtoinuencethemoneysupply(reservesinthebankingsystem)

and short term interest rates, which ultimately affect other longer term interest rates and assets

prices. The resultant impact on other interest rates, such as the deposit and lending rates, will

in turn inuence saving and spending decisions of the households and businesses, and

ultimately economic activity and the general price level in the economy.

The key element of the OMO framework is the interest rate corridor formed by the policy

interest rates which is referred to as the Standing Rate Corridor (SRC). Policy interest rates are

the benchmark interest rates in the economy, on which all other interest rates are determined.

Banksandother nancialinstitutionsinthe economyarefree tosettheirown interestrates

for lending and deposits, based on guidance provided by the policy interest rates on the

level and the direction of interest rates. Accordingly, policy interest rates play a key role in

thenancial system,thebankingsystem,andtheoveralleconomy,and hence remain the

maininstrumenttoachievethetargetedinationpath.Policy interest rates are also used as a

mechanism to signal the monetary policy stance of the Central Bank and to ensure stability in

interest rates of the economy.

• Policy Interest Rates and Open

Market Operations

• Statutory Reserve Requirement

• Quantitative Restrictions on

Credit

• Ceiling on Interest Rates

• Effective Communication and

Forward Guidance

• Moral Suasion

Key Monetary Policy Instruments

Other Policy Instruments

• Macroprudential Measures

• Foreign Exchange Operations

• Renance Facilities

• Bank Rate

The Central Bank uses an array of monetary policy instruments to manage liquidity in order to

maintain short term interest rates at the desired level. To that effect, policy interest rates, OMOs

and SRR remain the key monetary policy instruments of the Central Bank.

Policy interest rates which form the SRC of the Central Bank, serve as the upper and lower

bounds for the overnight interest rates in the money market. The Standing Deposit Facility Rate

(SDFR), which is the lower bound of the corridor, and the Standing Lending Facility Rate (SLFR),

which is the upper bound of the corridor, are instrumental in stabilising short term interest rates

in the economy. It is of utmost importance that interest rates, in particular, short term interest

rates, which can be directly impacted by the Central Bank, remain stable to ensure overall

stability in interest rates. Once the Central Bank announces changes to the policy interest

rates, that will have an immediate effect on the interbank call money market. Changes in

interbank call money rate get transmitted to other short term money market rates (such as

Treasury bill rates) within a short period of time. Subsequently, such changes get transmitted to

all medium and long term interest rates in the economy including lending and deposit rates of

nancialinstitutions.TheCentralBankattemptstomaintaintheinterbankcallmoneyrate(i.e.,

AWCMR)withintheSRC,whichistherstloopoftheinterestratetransmissionandtoensureits

stability.

The Central Bank conducts OMOs for this

purpose. OMOs refer to buying and selling

of securities to inject or absorb liquidity in

the market by the Central Bank to maintain

AWCMR within the SRC. Hence, OMOs are

the main market based monetary policy

operations conducted by the Central Bank

by using government securities to manage

liquidity in the domestic money market to

inuenceshortterminterestrates,whichinturn

inuence longer term interest rates and the

overall economic activity.

The Central Bank conducts OMOs based on

the decisions of the Market Operations Committee

(MOC), which is responsible for translating

monetary policy decisions into daily monetary

operations. MOC decides on the operational

activities in line with the prevailing monetary

policy stance, by taking into consideration

various factors, such as the estimated liquidity

forecast, desired level of the operating target,

liquidity distribution amongst PIs, and the need

for devising appropriate market signals.

For example, if the Central Bank observes an

excess amount of money (liquidity surplus) in

the banking system, it would consider absorbing

such excess as it might lead to a downward

bias in interest rates. In such instances, the

Central Bank attempts to reduce surplus

liquidity by selling government securities under

repurchase agreements, usually called as

repo transactions, thereby absorbing liquidity.

When there is a liquidity shortage (liquidity

The

Central Bank

conducts Open Market

Operations to inuence

liquidity and maintain

short-term interest

rates at a level in line

with the monetary poli

-

cy stance

Why

the Central Bank

conducts Open

Market

Operations?

17

Monetary Policy Implementation in Sri Lanka

LKR

LKR

LKR

BANK

LKR

First Leg:

The Central Bank sells government securities and

PIs buy government securities under repo auctions for a

predetermined tenure (excess liquidity is absorbed by the

Central Bank)

Second Leg:

At the maturity of the agreement, PIs return

the

securities to the Central Bank and receive investment plus interest

Note: The process of a reverse repo transactions is as follows: First Leg – The Central Bank purchases government

securities from PIs for the agreed tenure (liquidity is injected by the Central Bank). Second

Leg – At the maturity, PIs return the borrowed funds with an interest to the Central Bank and receive their

securities back.

Figure 7: Repurchase (Repo) Transactions of the Central Bank

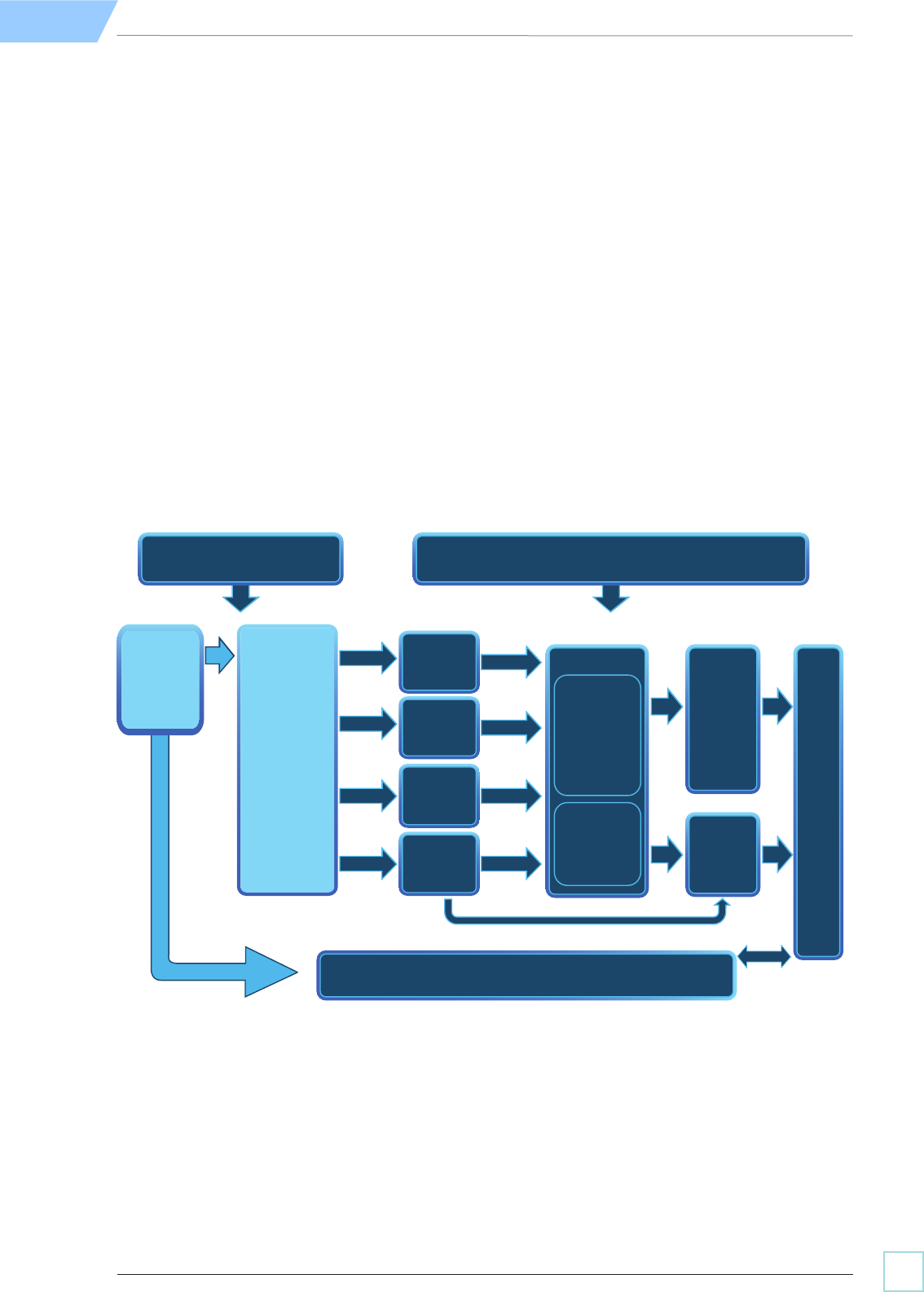

The Central Bank conducts different types of auctions under OMOs to change liquidity in the

domesticmoneymarketonatemporaryand/orpermanentbasis.Currently,allOMOtransactions

inSriLankaarecollateralisedbyTreasurybillsorTreasurybonds.Usually,repo/reverserepo

transactions are carried outtoadd/drainliquidityonatemporarybasisthroughovernight,short

term,andlongtermbases.However,whenthereisapersistentliquidityshortage/excess,the

CentralBankusesoutrightpurchases/salesofgovernmentsecuritiesinordertopermanently

affect market liquidity (see Figure 8).

18

Monetary Policy Implementation in Sri Lanka

decit),theCentralBankmaybuygovernmentsecuritiesandrelease money to LCBs using the

reverse repo transactions (liquidity injection). At the maturity of repo or reverse repo transactions,

thecashowsandthecollateralsarereversed(seeFigure7).

Figure 8: Synopsis of OMOs and Standing Facility

Liquidity Estimation of the Central Bank

Excess liquidity

Decision on monetary operations Decision on monetary operations

Auctions for liquidity injection

on temporary basis by the

Central Bank

- Overnight Reverse Repo

- Short Term Reverse Repo

- Long Term Reverse Repo

Auctions for liquidity absorption on

temporary basis by the

Central Bank

- Overnight Repo

- Short Term Repo

- Long Term Repo

SDF to deposit residual

excess funds at the Central

Bank at the end of the day

SLF to borrow residual funding

requirement from the Central

Bank at the end of the day

Funds Funds

Securities Securities

Decit liquidity

Auctions for liquidity absorption

on permanent basis by the

Central Bank

- Outright sales

of Treasury bills/ bonds

Auctions for liquidity injection

on permanent basis by the

Central Bank

- Outright purchases

of Treasury bills/ bonds

PIs

PIs

Steering the short term interest

rates (AWCMR)

19

Monetary Policy Implementation in Sri Lanka

Standing Facility

Standing facility is a window under OMOs that allows PIs to borrow funds overnight on collateralised basis

or deposit funds on an overnight basis without a collateral. Accordingly, these facilities help LCBs and other

eligiblePIstofulltheirday-to-dayresidualliquidityrequirements.TheCentralBankofferstwotypesofovernight

standing facilities on each business day: the Standing Lending Facility (SLF) and the Standing Deposit Facility

(SDF).

SLFallowsPIstocovershorttermanticipatedorunanticipatedliquidityrequirementsthatcannotbefullled

from the money market or from the auctions conducted by the Central Bank. SDF allows PIs to deposit excess

funds with the Central Bank on an overnight basis. The interest rate on SLF, i.e., SLFR and the interest rate on

SDF, i.e., SDFRprovideaceilingandaoor,respectively,fortheovernightinterestrateinthemoneymarket.

The main purpose of the standing facility is to minimise volatility of short term money market interest rates as

thisfacilitysupportsPIstofullresidualfundingneedsandremunerateidlefunds.Atpresent,inthecontextof

Sri Lanka, SDF remains uncollateralised (no securities are provided by the Central Bank on such deposits of

LCBs), while SLF is provided as a collateralised facility (LCBs pledge government securities when obtaining

funds).

Statutory Reserve Requirement (SRR)

SRR is a policy instrument used to inuence liquidity on a permanent basis and the level of money in the

economythroughthemoneymultiplier.InthecontextofSriLanka,SRRisdenedastheproportionofaverage

rupee deposit liabilities of LCBs, which is required to be maintained as reserves at the Central Bank as per the

MLA. At present, rupee deposit liabilities, including demand deposits, time and savings deposits and other

deposits of LCBs, are considered for the calculation of required reserves under SRR. The Central Bank relies on

SRRmainlytoaddresspersistentliquidityissuesinthemarket,whichinuencethemoneysupplyandinterest

ratesintheeconomy.BychangingSRR,theCentralBankcaninuencetheamountoffundsthatthebanks

can use to make loans to their customers.

In the process of maintaining SRR, LCBs are allowed to maintain a certain percentage in the form of currency

notes and coins as a part of their required reserves, which is known as the till cash concession. Such amount

is allowed to be deducted from SRR, as a concession, in deriving the amount of required reserves to be

maintained by LCBs.

For example, if the average total rupee deposit liabilities of LCBs is Rs. 8,000 billion,

SRR is 4%, and the till cash concession is 1% of rupee deposit liability (i.e., Rs. 80 billion), total reserves

required to be maintained by LCBs is Rs.240 billion during a particular reserve maintenance period (see

Table 1).

20

Table 1: Calculation of SRR

Component

Amount

(Rs. Bn.)

1. Average Total Deposit Liabilities (Rupee Deposits) 8,000

1.1 Demand Deposits

400

1.2 Time & Savings Deposits

7,500

1.3 Other Deposits

100

2. SRR (assuming the SRR as 4% of rupee

deposit liability)

320

3. Till Cash Concession (assuming 1% of rupee deposit liability)

80

4. Total Required Reserves for the Reserve Period (2-3) 240

Monetary Policy Implementation in Sri Lanka

Monetary Policy Implementation in Sri Lanka

21

ByincreasingSRR,theCentralBankcaninuencetheamountofmoneythatcanbeusedforlending

by LCBs by controlling the money creation ability of LCBs (contraction of the money supply), resulting

an increase in interest rates (cost of funds) in the economy. Conversely, by reducing SRR, the Central

Bank provides additional reserves to LCBs, allowing them to expand their credit (expansion of the money

supply), resulting in a reduction in interest rates. Further, SRR acts as a cushion for LCBs as it facilitates

any unexpected settlement of payment obligations that could occur during the day. Accordingly,

the balances under SRR are also referred to as settlement balances of the current account of LCBs

maintained at the Central Bank.

The impact of changes in SRR on the economy is depicted in Figure 9.

In addition, the Central Bank can use restrictions on credit granted to certain industries or sectors and

ceilings on interest rates that could be charged on lending or offered to customer deposits as a part of

monetary policy actions.

Transparent and credible communication is also used by the Central Bank as another monetary policy

tool as the decisions of economic agents are often based on the expectations on future economic

developments as well. Effective communication and providing forward guidance to the market by the

Central Bank are vital, particularly during the times of high economic uncertainty.

The Central Bank uses moral suasion with a view to guiding PIs to align their activities to support the

attainment of the objectives of the Central Bank. Accordingly, the Central Bank directs PIs towards the

desired path whenever the market behaviour and expectations are misaligned with the intended policy

direction.

Other Policy Instruments

Depending on the need and circumstances in the economy, the Central Bank deploys other instruments

to complement monetary policy such as the macroprudential measures, foreign exchange transactions

renancefacilities,andtheBankRate.

The Central Bank uses macroprudential instruments, which are generally introduced to address the

systemic risk faced by the nancial system. For example, introducing margin requirements on imports

to curtail imports to minimise the pressure on the external sector and introducing measures such as

countercyclical capital buffers, capital conservation buffers, caps on leverage ratios, caps on debt

services-toincomeratioscanbeusedtoaddressunstableconditionsintheoverallnancialsystemand

economy.

The Central Bank also deploys foreign exchange operations in conducting monetary policy. For example,

theCentralBankmay enterintoforeignexchange swap transactionswhereitpurchases/sells foreign

currency with an undertaking of selling/buying back such foreign currency at a future date. These

operations affect money market liquidity.

Inaddition,tosupporttheeconomyandthenancialsysteminextraordinarycircumstances,theCentral

Bankcanproviderenancefacilitiestotheidentied sectors via nancial institutions or provide loan

facilitiestonancialinstitutions.

Banks can also receive funds from the Central Bank not only through monetary operations, but also

through liquidity assistance facility to address system wide liquidity stress as well as emergency liquidity

assistance in exceptional circumstances faced by a banking institution. The Bank Rate is the rate at

which the Central Bank provides liquidity assistance facility to banking institutions under the current legal

provisions. Usually, the Bank Rate is relatively a higher interest rate.

22

Monetary Policy Implementation in Sri Lanka

Deposits

Rs. 10 Bn

Deposits

Rs. 90 Bn

If the Central Bank reduces

SRR from 4% to 2%

Total Deposits

at ABC Bank

(Rs. 100 Bn)

If the Central Bank increases

SRR from 4% to 5%

SRR 4%

(Rs. 4 Bn)*

ABC Bank maintains Rs. 2 Bn in

the reserve account at the

Central Bank and uses Rs. 98 Bn

for lending to customers

(Permanent Liquidity Injection)

ABC Bank maintains Rs. 5 Bn in

the reserve account at the

Central Bank and uses Rs. 95 Bn

for lending to customers

(Permanent Liquidity Absorption)

• Interest rates decline

• Credit growth accelerates

• Interest rates increase

• Credit growth decelerates

Impact on economic activity and

the price level

Businesses Households

Figure 9: Monetary Policy Implementation under SRR

*Assumingthattillcashconcessioniszero

Part III:

Transmission Mechanism of Monetary Policy

The transmission mechanism of monetary policy describes how changes in monetary policy

actions of the central bank ow through to economic activity to achieve the objective of

price stability. This is generally a two stage process, involving a large degree of uncertainty in

thetimingandsizeoftheimpactontheeconomy,andhenceacomplexprocess.Theexact

relationship as well as timing of transmission is unclear, particularly for long term interest rates

and hence transmission is referred to as a black box in the monetary economics literature.

The rst stage of transmission explains how changes to policy interest rates inuence other

interest rates (both short term and long term interest rates), which is widely known as interest

rate pass-through. The second stage of transmission explains how the changes to interest rates

inuenceeconomicactivityandination.

Theinterbankcallmoneyrateistherstloopofinterestratepass-through,whichhasastrong

inuenceovertheotherinterestratesintheeconomy,generallyasdepictedbytheyieldcurve.

In general, policy rate changes cause a quick adjustment in the interbank call money rate.

Hence, once the central bank announces changes to the policy interest rates, such changes

have an immediate effect on the call money rate. Then such changes get transmitted to short

termandlongterminterestrates,includinglendinganddepositratesofnancialinstitutions.

However, other factors, such as the market competition as well as maturity and risk involved

inthedifferentmarketsandproducts,affectthetimingandsizeofshorttermandlongterm

interest rate adjustment.

In the second stage of transmission mechanism of monetary policy, the central bank decisions

affect the spending and investment decisions of economic agents, thereby affecting the

aggregatedemandconditionsandsubsequentlytheinationrateintheeconomy.However,

there is a time lag between the policy decisions and their effects on economic activity and

inationashouseholdsandrmswouldtaketimetoadjusttheirbehaviour.

Asimpliedstandard

version of the second stage of monetary transmission is illustrated in Figure 10.

Monetary Policy Implementation in Sri Lanka

23

Policy rates

increase

d!

My borrowing

cost has increased.

So I need to curtail

borrowings

Policy rates

increased!

It‛s a good

time to deposit

my money in a

fixed deposit

Central Bank

24

Monetary Policy Implementation in Sri Lanka

Accordingly, for example, when the central bank reduces policy interest rates (known as

monetary easing), individuals will increase consumption rather than savings due to low

interest rates in the banking system. Accordingly, lower interest rates increase overall demand

(aggregate demand) in the economy by stimulating spending. However, producers take

relatively more time to change the supply of goods as they need to hire more workers and

equipment to cater to the increased demand resulting in an excess demand, which creates

anupwardpressureonprices,leadingtohigherination.

On the other hand, when the central bank increases policy interest rates (known as monetary

tightening), borrowings become less attractive due to the high cost of borrowings. Accordingly,

higher interest rates tend to decrease the aggregate demand and lead to a slowdown in

economic activity, ultimately resulting in a deceleration in ination. However, this second

stage of monetary policy transmission is much more complicated than the rst stage. As

depicted in Figure 10, the changes in the policy interest rates and impact of monetary policy

instruments are usually transmitted to the broader economy via different, but interconnected

channels such as market interest rates, credit, asset prices, exchange rates, and expectations.

While the exchange rate channel affects net exports, other channels mainly affect the other

components of GDP, i.e., consumption and investment.

The transmission of monetary policy is also affected by ination expectations. Economic

agents’ expectations about future ination affect their current behaviour. For example, if

employees in the economy expect ination to rise, they may demand wage increases in

line with the expected changes in ination. Higher wage growth would then contribute to

higherprices.Byhavinganinationtargetandthrougheffectivecommunication,thecentral

bankattemptstoanchorinationexpectations.Thisenhancesthecondenceofhouseholds

and businesses in terms of making decisions about saving and investment due to reduced

uncertainty. The effectiveness and success of monetary policy are also dependent on the

credibilityandindependenceofthecentralbank■

Policy

Rates,OMOs

and Other

Instruments

Overnight

Interest Rate

(AWCMR)

Short term

Interest Rates

Long term

Interest Rates

(interest

rates for

households

and

businesses)

Ination

Stage 1:

Interest Rates

Stage 2:

Economic Activity and Ination

Market

Interest

Rates

Credit

Asset

Prices

Exchange

Rates

GDP

Consumption

and

Investment

Net

Exports

Domestic

Prices

Import

Prices

Ination Expectations

Figure 10: Transmission Mechanism of Monetary Policy