CONSUMER FINANCIAL PROTECTION BUREAU | MARCH 2020

Market Snapshot:

First-time Homebuyers

Table of contents

Table of contents.........................................................................................................1

1. Introduction...........................................................................................................2

2. Data........................................................................................................................3

3. First-time homebuyer analysis............................................................................4

4. Conclusion ..........................................................................................................16

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 1

1. Introduction

1

Most American households desire to own a home.

2

However, for households attempting to

make the transition from renting to owning, shifts in the housing and mortgage markets can

play a large role in whether they can afford to buy a home. Unlike most repeat buyers, first-time

buyers do not have the benefit of accumulated home equity or an existing investment that

generally insulates homeowners from rising housing costs. As a result, rising home values can

disproportionately affect first-time buyers. Additionally, renters do not benefit from a credit

history that reflects monthly mortgage payments, and many times their rental history will not be

reflected in their credit history either.

In this Market Snapshot, we investigate the prevalence and ease of first-time homeownership

today by comparing current and historical market trends. Specifically, we look at the credit

characteristics and product usage of first-time buyers, the demographics of first-time buyers,

and where first-time buyers are able to buy.

1

Report prepared by Kristin Wong and Logan Herman.

2

https://www.nar.realtor/research-and-statistics/research-reports/aspiring-home-buyers-profile;

https://stories.wf.com/survey-many-americans-willing-takes-homeowners/

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 2

2. Data

Our analysis primarily relies on the National Mortgage Database (NMDB), a nationally

representative, 5 percent sample of all outstanding, closed-end, first-lien, 1–4 family residential

mortgages.

3

We look at consumers purchasing their first home between 2002 and 2018, a

timeframe that covers a wide range of market conditions. We solely analyze home purchasers

buying a primary residence. For loans with more than one borrower, our analysis uses the

borrower with the longest payment record.

4

In the NMDB, first-time homebuyers are defined as borrowers who appear to have no previous

mortgage in the preceding seven years. Other analyses define first-time buyers more broadly, a

common definition of a first-time buyer is any borrower who did not appear to have a mortgage

for the preceding three years. Our analysis also differs from those that analyze cash-sales along

with financed purchases, such as the Home Buyers and Sellers Report from the National

Association of Realtors (NAR).

5

Among first-time buyers the number of cash-sales appears to be

small. The 2017 NAR Report found that 96 percent of first-time buyers financed their purchase

with a mortgage.

6

3

https://www.fhfa.gov/PolicyProgramsResearch/Programs/Pages/National-Mortgage-Database.aspx

4

Some loans have a mix of first-time and repeat borrowers. By analyzing only one borrower, the estimated number of

first-time buyers in this snapshot will be slightly higher than measures that require both borrowers to be first-time

buyers and slightly lower than measures that require only one borrower to be a first-time buyer.

5

https://www.nar.realtor/research-and-statistics/research-reports/highlights-from-the-profile-of-home-buyers-

and-sellers

6

https://libertystreeteconomics.newyorkfed.org/2019/04/a-better-measure-of-first-time-homebuyers.html

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 3

3. First-time homebuyer

analysis

Despite rising home prices, first-time buyers still account for

approximately half of the home purchase mortgage market.

At the end of 2018, the average home price in the US was 12% above its 2007 peak.

7

Combined

with historically low housing inventory, affordability has been a concern expressed by many in

the housing industry.

8

Despite these concerns, about half of all home purchase mortgages have gone to first-time

buyers each year since 2002. While 600,000 fewer mortgages went to first-time buyers in 2018

than in 2002, this is primarily a result of the overall decline in the purchase market during the

financial crisis of 2007 to 2009 and the steady recovery since 2011.

FIGURE 1: NUMBER OF HOME PURCHASE LOANS ORIGINATED FOR FIRST-TIME AND REPEAT BUYERS

The reason for this may be that while home prices have been increasing, household incomes also

have been increasing and interest rates have been low. Indeed, according to the National

7

Black Knight HPI data

8

Joint Center for Housing Studies of Harvard University, The State of the Nation’s Housing 2019

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 4

Association of Realtor’s Housing Affordability index, housing was more affordable in 2018 than

in 2000 based on the median family income.

Along with rising incomes, looser CLTV and DTI standards

have also helped first-time buyers afford pricier homes.

Conventional wisdom is that consumers should have a 20 percent down payment when

purchasing a home.

9

For first-time buyers, however, this task can be difficult and unnecessary.

Since 2002, the median combined loan-to-value ratio (CLTV)

10

for first-time buyers has been

greater than 80 percent. During the run up to the financial crisis, the median increased by five

percentage points, and it has since remained at this higher level. In the same time period, the

median CLTV for repeat borrowers also increased and now also remains at over 80 percent.

FIGURE 2: MEDIAN CLTV OF FIRST-TIME BUYERS

Homebuyer debt loads have increased as well. The median debt-to-income ratio (DTI) of repeat

and first-time buyers peaked at 41% and 40% in 2007, respectively, and then began to decline.

More recently, DTI ratios have been rising for both groups. At the end of 2018, the median DTI

of first-time buyers was one percentage point higher than of repeat buyers.

11

9

https://www.fanniemae.com/resources/file/research/housingsurvey/pdf/consumer_understanding_research.pdf

10

The CLTV is the ratio of all secured loans on a property to the value of a property.

11

The pre-crisis DTI medians are likely underestimated. During the housing boom, some DTIs may have been based

upon incomes that were overstated as a result of stated income lending. Post-crisis, lenders are now required to

verify a borrower’s income.

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 5

FIGURE 3: MEDIAN DTI OF FIRST-TIME BUYERS

However, looser CLTV and DTI standards have mainly helped

first-time borrowers with higher credit scores.

In the years prior to the financial crisis, the median credit score for both first-time buyers and

repeat buyers trended downward. Since 2007, however, that trend has been reversed as lenders

tightened their underwriting requirements. (In more recent years, an improving economy also

likely contributed to improved financial outcomes and overall higher scores.) In 2018, the

median credit score of first-time buyers was 32 points higher than in 2002. The spread between

the median credit score of first-time buyers and repeat buyers in 2018 was 45 points, slightly

higher than the spread in 2002.

FIGURE 4: MEDIAN VANTAGE SCORE OF FIRST-TIME BUYERS

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 6

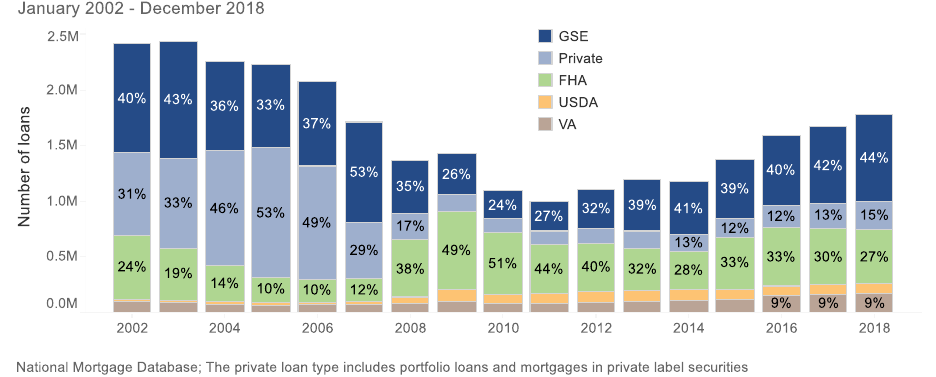

First-time buyers have migrated away from the private market and

are now most likely to turn to the GSEs.

Directly after the financial crisis, the private market shrank, and first-time buyers initially

migrated towards loans insured by the Federal Housing Administration (FHA loans). As the

market recovered, the FHA market share retreated and loans guaranteed by Fannie Mae or

Freddie Mac (Government Sponsored Enterprise loans or GSE loans) became the most common

choice for first-time buyers. Additionally, the GSEs introduced low down payment programs in

2014, which rendered the GSEs more competitive for borrowers with higher credit scores. This

trend is also seen among repeat borrowers. Even with these trends, among first-time

homebuyers the shares of both FHA loans and other government insured or guaranteed loans

are higher than they were in 2002, while the share of loans held by creditors on their own

balance sheets (“portfolio loans”) is half of what it was in 2002.

FIGURE 5: NUMBER AND SHARE OF LOANS ORIGINATED FOR FIRST-TIME BUYERS BY LOAN TYPE

Although first-time buyers are now most likely to have GSE loans, government programs still

play an important role in getting first-time buyers into homes. Originations of loans insured or

guaranteed by the Department of Agriculture (USDA loans) and loans guaranteed by the

Department of Veterans Affairs (VA loans) increased immediately after the financial crisis and

their volume remains higher than before—USDA loans went from 1% of first-time buyer

originations to 5% from 2002 to 2018, and the VA market share increased from 4% to 9%.

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 7

Research from the CFPB found that the share of first-time homebuying servicemembers using

VA loans increased from 30% before 2007 to 78% in 2016.

12

The majority of loans originated under government programs still go to first-time buyers.

However, these programs have grown to attract more repeat buyers, particularly the VA

program. The VA program allows borrowers to purchase a home with no downpayment; as of

2019, nearly 90% of VA borrowers take advantage of this benefit.

13

FIGURE 6: PERCENT OF HOME PURCHASE ORIGINATIONS THAT WENT TO FIRST-TIME BUYERS BY

LOAN TYPE

Generally, first-time buyers obtain mortgages at the same

age they did before the financial crisis. Black borrowers

become first-time buyers noticeably later than before.

During the years prior to the financial crisis, the median age of first-time buyers decreased.

Over the past decade, the age of first-time home buyers when they buy their home has increased.

This has fueled concerns that younger buyers can no longer afford homeownership. However,

the ages of today’s first-time buyers are not so different than in the recent past. The median age

of first-time buyers in 2018 is the same as it was in 2002 and 2003, 32 years old.

12

https://files.consumerfinance.gov/f/documents/cfpb_consumer-credit-trends_first-time-homebuying-

servicemember-mortgages_022019.pdf

13

https://www.va.gov/housing-assistance/home-loans/

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 8

FIGURE 7: MEDIAN AGE OF FIRST-TIME BUYERS

When broken down by race and ethnicity, it becomes clear that some groups have had larger

changes in the age of first-time homeownership than others. In 2018, the median first-time black

borrower was six years older than the median non-Hispanic white borrower. That is a much larger

disparity than in 2002, when the age gap between black and white first-time borrowers was just

two years. Black borrowers were particularly hard hit during the financial crisis, and accordingly,

were more likely to go from owning to renting.

14

The resulting lost wealth and generational impact

likely contributed to the increasing age gap in first-time homeownership.

15

14

https://files.stlouisfed.org/files/htdocs/publications/review/2017-02-15/the-homeownership-experience-of-

minorities-during-the-great-recession.pdf

15

https://www.urban.org/urban-wire/what-explains-homeownership-gap-between-black-and-white-young-adults

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 9

FIGURE 8: MEDIAN AGE OF FIRST-TIME BUYERS BY RACE AND ETHNICITY

First-time buyers in expensive MSAs have generally been

older than in more affordable areas. Post-crisis, the age gap

is growing.

Affordability challenges also differ by geographical regions and characteristics. First-time

borrowers in more costly metropolitan statistical areas (MSAs) tend to be older than buyers in

more affordable MSAs. The median age of first-time buyers declined in most MSAs during the

housing boom prior to the financial crisis. Median age in higher-cost MSAs has since increased

to levels higher than in 2002, while in many lower-cost MSAs the median age has returned to

pre-housing boom levels.

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 10

FIGURE 9: MEDIAN AGE OF FIRST-TIME BUYERS BY MSA COST

Despite the accelerated aging of rural areas, rural first-time

buyers borrow at similar ages to their urban counterparts.

Rural counties contain over 85 percent of “older age counties,”

16

many of which experience

persistent population loss of young adults.

17

However, rural areas remain a consistently strong

market for first-time homebuyers.

16

This analysis defines “rural” as non-metropolitan counties and “urban” as metropolitan counties according to the

USDA 2013 Rural-urban Continuum Codes. “Older age counties” are defined as counties with more than 20 percent

of their population age 65 or older.

17

https://www.usda.gov/media/blog/2018/12/20/rural-aging-occurs-different-places-very-different-reasons

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 11

FIGURE 10: NUMBER OF HOME PURCHASE LOANS ORIGINATED FOR FIRST-TIME BORROWERS BY

GEOGRAPHY

Since 2002, borrowers in rural areas have made up 11% to 13% of all first-time homebuyers. In

2018 the median age of a rural first-time borrower was two years younger than the median age

of an urban first-time borrower. That is a reversal of the situation in 2002 when the median age

of a rural first-time buyer was one year older than the median age of an urban first-time

borrower.

FIGURE 11: MEDIAN AGE OF FIRST-TIME BUYERS BY GEOGRAPHY

Rural borrowers benefit from a more affordable housing supply and USDA’s specialized loan

programs, which increase opportunities to purchase homes at a younger age. USDA loans have

become an increasingly important source of credit for rural first-time borrowers, increasing

from 4% of rural first-time buyer loans in 2002 to 17% in 2018.

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 12

FIGURE 12: NUMBER OF RURAL LOANS ORIGINATED FOR FIRST-TIME BUYERS BY LOAN TYPE

The median CLTV and DTI for rural first-time borrowers are

lower than for urban buyers although the gap has narrowed

since 2002.

Prior to the financial crisis, rural borrowers had lower CLTVs than urban borrowers. Since

2007, the CLTVs of first-time urban and rural borrowers have converged. This trend coincides

with a relative increase in rural USDA and FHA loans that tend to have higher CLTVs.

FIGURE 13: MEDIAN CLTV OF FIRST-TIME BUYERS BY GEOGRAPHY

Even though rural borrowers tend to have lower incomes in comparison to their urban

counterparts, the median rural borrower had lower DTIs over the past 15 years as rural

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 13

borrowers have greater access to relatively lower cost housing. In 2018, the median rural first-

time borrower had an income of $54,000, compared to $68,000 for urban borrowers.

18

FIGURE 14: MEDIAN DTI OF FIRST-TIME BUYERS BY GEOGRAPHY

The median credit score of first-time rural borrowers has

risen but remains below the median for urban buyers.

Prior to the start of the housing boom, the median credit score of first-time rural and urban

buyers was the same. In the early 2000s, median credit scores of rural and urban borrowers

diverged and have continued to grow apart. As of 2018, the median credit score of an urban

first-time homebuyer was 24 points higher than the median credit score of a rural first-time

homebuyer.

18

National Mortgage Database

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 14

FIGURE 15: MEDIAN VANTAGE SCORE OF FIRST-TIME BUYERS BY GEOGRAPHY

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 15

4. Conclusion

First-time buyers after the financial crisis face disparate sets of challenges on the road to

attaining homeownership. New buyers enter a market that is limited in inventory and has

shifted to borrowers with higher credit scores. While the overall median age of first-time buyers

has not significantly changed since the early 2000s, racial disparities continue to grow in the

market. The age gap between black and non-Hispanic white borrowers has tripled since 2002.

Home affordability also varies significantly by region and housing market. Rural borrowers

have lower DTIs and lower credit scores than their urban counterparts. Borrowers in some

affordable MSAs buy their first home around the same age as they did prior to the financial

crisis. Borrowers in expensive MSAs are typically older and their median age at the time of

purchase has continued to increase since the financial crisis. As home prices remain relatively

affordable for median-income households nationwide, credit scores, buyer demographics, and

location play key roles in determining when first-time buyers enter the housing market.

MARKET SNAPSHOT: FIRST-TIME HOMEBUYERS 16