1

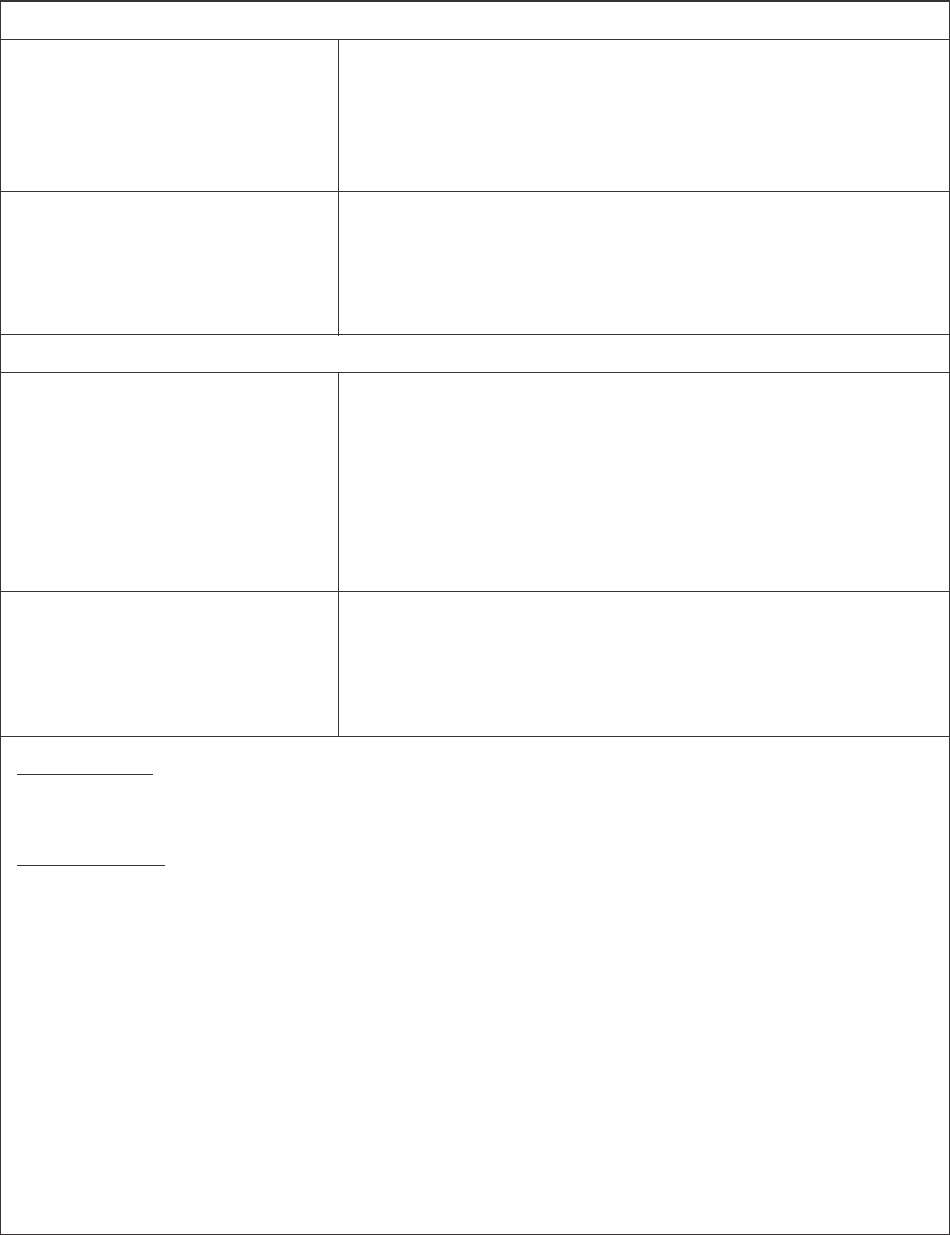

Self Employed Professionals) Application whichever is higher+ applicable taxes /

statutory levies.

Employed Non-Professionals) Application whichever is higher + applicable taxes /

statutory levies.

50% of applicable fees or Rs. 4500/-

5 Fees for Top-Up Loan & HDFC Now (Self Processing Fees At Once Upto1.50%of the Loan amount or Rs. 4500/-

Renovation/ Refinance/ Plot Loans for Self Application whichever is higher+ applicable taxes /

Employed Non-Professionals. statutory levies.

Minimum Retention Amount:

+applicable taxes/statutory levies

whichever is higher

Minimum Retention Amount: 50% of

applicable fees or Rs. 3000/-+applicable

taxes/statutory levies whichever is higher

1 Fees for Resident Housing Loan/ Extension/ Processing Fees At Once Upto 0.50% of the loan amount or Rs. 3000/-

House Renovation Loan/ Refinance of Application whichever is higher + applicable

Housing Loan/ Plot Loans for Housing taxes / statutory levies.

(Salaried, Self Employed Professionals) Minimum Retention Amount: 50% of

applicable fees or Rs. 3000/- +applicable

taxes/statutory levies whichever is higher

3 Fees for Resident Housing/ Extension/ Processing Fees At Once Upto 1.50 % of the Loan amount or Rs. 4500/-

4 Fees for Top-Up Loan & HDFC Now (Salaried, Processing Fees At Once Upto 0.50 % of the Loan amount or Rs. 3000/-

+applicable taxes/statutory levies

whichever is higher

2 Fees for Resident Non-Housing Loan/ Processing Fees At Once Upto 0.50% of the loan amount or Rs. 4500/-

Extension/ Non-Housing Renovation Loan/ Application whichever is higher + applicable

Refinance of Non-Housing Loan/ Plot Loans taxes / statutory levies.

for Non-Housing (Salaried, Self Employed Minimum Retention Amount:

Professionals) 50% of applicable fees or Rs. 4500/-

+ applicable taxes/statutory levies

whichever is higher

Minimum Retention Amount:

50% of applicable fees or Rs. 4500/-

MOST IMPORTANT TERMS AND CONDITIONS (MITC)

For product features, checklists, calculators, new home loan inquires, existing Customer portal and other notifications visit our

website www.hdfc.com or download HDFC Home Loans App from Playstore/ AppStore. For loan specific details pertaining to the

loan amount, interest rates and repayment details, refer to the schedule of the Loan Agreement and/or the Offer Letter.

The nature and/or quantum of the fees/charges/levies mentioned herein may undergo review/modification at the time of actual

application, as per the then prevailing policies of HDFC in compliance with regulatory guidelines, as may be updated by HDFC in

its MITC from time to time. The Borrower shall be required to keep himself/herself updated of such changes through our website

www.hdfc.com

The Most Important Terms and Conditions (“MITC”) of the loan between the Borrower/s and Housing Development Finance

Corporation Ltd., a Company incorporated under the Companies Act, 1956 and having its registered office at Ramon House,

H T Parekh Marg, 169, Backbay Reclamation, Churchgate, Mumbai - 400 020 (herein after referred to as “HDFC”) are mentioned

below and are to be read in conjunction with the terms contained in the Offer Letter and the Loan Agreement and any other

document(s) (hereinafter collectively referred to as the “Transaction Documents”) which you have executed (jointly and severally

as may be applicable) with HDFC. The MITC mentioned herein is indicative and not exhaustive.

A. Various fees and other charges - as applicable on application/ during the term of loan/ conversion charges for switching from

floating to fixed interest and vice-versa and penalty for delayed payments, are as under:

1. Fees and Other Charges

Sr. Name of the Product/Service Name of Fee/ When Payable Frequency Amount in Rupees

No Charge levied

2

taxes/statutory levies whichever is higher

statutory levies.

whichever is higher

50% of applicable fees or Rs. 4500/-

taxes / statutory levies and charges.

Minimum Retention Amount: 50% of

8 Fees for Value Plus Loans Processing Fees At Once Upto 1.50% of the Loan amount or Rs. 4500/-

Application whichever is higher + applicable taxes /

Minimum Retention Amount: 50% of

applicable fees or Rs. 4500/-+applicable

and HDFC Maxvantage Loans Application whichever is higher + applicable taxes /

6 Fees for Equity/ Non-Residential Premises Processing Fees At Once Upto1.50% of the Loan amount or Rs. 4500/-

Minimum Retention Amount:

+applicable taxes/statutory levies

7 Fees for NRI Loans Processing Fees At Once Upto 1.25% of the Loan amount or Rs. 3000/-

Application whichever is higher + applicable

applicable fees or Rs. 3000/-+applicable

taxes/statutory levies whichever is higher

statutory levies and charges.

applicable fees or Rs. 3000/-+applicable

10 Delayed Payment Charges Additional Interest On Accrual Monthly A maximum of 24% P. A. on the delayed sum.

11 Expenses to cover costs Incidental Charges On incurring Incidental charges and expenses are levied

12A Statutory Charges Stamp Duty/ MOD/ On Fixing of As may be As applicable in the respective States.

Application applicable taxes / statutory levies.

taxes/statutory levies whichever is higher

other monies as per actuals applicable to a

addition of

security

12B Fees/Charges levied by Regulatory bodies Fees/Charges On Disbursement / As may be As per actual charges/ fee levied by

levied by entities Change or addition applicable Regulatory bodies + applicable taxes/

MOE/ Registration Disbursement/ applicable

such as CERSAI or deletion of statutory levies

security

whose services have been availed levied by such third applicable third party(ies) + applicable taxes/

parties such as statutory levies

Minimum Retention Amount: 50% of

mortgage

9 Fees for Loans under HDFC Reach Scheme Processing Fees At Once Up to 2.00% of the loan amount+

expenses to cover the cost, charges, expense and

guarantee company

Change or

case.

13 Switch to Lower Rate in Variable rate Conversion Fees On Conversion On every Upto 0.50% of the Principal Outstanding

12C Fees / charges payable to any third party(ies) Fees/Charges On Disbursement As may be As per actual fee/ charges levied by any

+ applicable taxes / statutory levies

whichever is lower.

Loans (Housing/ Extension/ Renovation) Spread and undisbursed amount (if any)at the time

Renovation) Conversion or a cap of Rs.50000/-

ever is lower.

Fixed Rate Loan (Housing/Extension/ undisbursed amount (if any) at the time of

+applicable taxes/ statutory Levies which

14 Switching to Variable Rate Loan from Conversion Fees On Conversion Once Upto 0.50% of the Principal Outstanding and

Change of Conversion or a cap of Rs.50000/-

Sr. Name of the Product/Service Name of Fee/ When Payable Frequency Amount in Rupees

No Charge levied

15 A Switch to a RPLR-NH Benchmark Rate Conversion Fees On conversion On change NIL

(Non–Housing Loans) and corresponding where the resultant of bench-

spread rate of interest mark rate

change of

15 B Switch to a RPLR-NH Benchmark Rate Conversion Fees On conversion On change Half of the spread difference on the principal

spread rate of interest benchmark plus taxes, with a minimum fee of 0.5% and

is lowered rate and/ Max. 1.50%

(Non–Housing Loans) and corresponding where the resultant of outstanding and undisbursed amount (if any)

or change

of Spread

remains the same and/or

Spread

16 Switch from Combination Rate home loan Conversion Fees On Conversion Once 1.75% of the Principal Outstanding and

fixed rate to Variable rate Undisbursed amount (if any)+ applicable

taxes / statutory levies at the time of

Conversion.

change taxes/statutory levies at the time of conversion.

22 Fees on account of External Opinion – Miscellaneous On incurring On every As per actuals.

27 A Switch to HDFC Maxvantage Scheme Processing Fee At the time of Once 0.25% of the outstanding loan amount +

Variable Rates Spread outstanding and undisbursed amount (if any)

Receipts SI Dishonour on no. of

Receipts request statutory levies.

Dishonour

post disbursement Receipts occurrence statutory levies.

change taxes/statutory levies at the time of Conversion.

Reach)- Variable Rate Spread undisbursed amount (if any) + applicable

Receipts request statutory levies

a minimum fee of 0.5% and Max 1.50%

21 Photo Copy of Documents Miscellaneous Event On every Upto Rs. 500/- + applicable taxes / .

change + applicable taxes / statutory levies with

25 Disbursement cheque cancellation charge Miscellaneous Event On every Upto Rs. 500/- + applicable taxes /

20 Cheque/ACH/SI Dishonour Charge Miscellaneous On Cheque/ACH/ Depends Rs. 300/- Per Dishonour.

such as legal/technical verifications. Receipts expenses occurrence

Receipts request statutory levies.

23 List of documents Miscellaneous Event On every Upto Rs. 500/- + applicable taxes /

date of sanction Re-Application statutory levies.

18 Switch to Lower Rate (Plot Loans)- Conversion Fees On Conversion On every 0.5% of principal outstanding and

Variable Rate Spread undisbursed amount (if any) + applicable

19 Switch to Lower Rate (Loans under HDFC Conversion Fees On Conversion On every Upto 1.50% of the principal outstanding and

17 Switch to Lower Rate (Non-Housing Loans)- Conversion Fees On Conversion On every Half of the spread difference on the principal

24 PDC swap Miscellaneous Event On every Upto Rs. 500/- + applicable taxes /

26 Re-appraisal of loan after 6months from Processing Fees At Once Rs. 2000/- + applicable taxes /

time of conversion

27 B Reversal of Provisional Prepayment under Processing Fee At the time of On every Rs. 250/- plus applicable taxes/statutory

HDFC Maxvantage Scheme Reversal reversal levies at the time of reversal

Conversion applicable taxes/statutory levies at the

Sr. Name of the Product/Service Name of Fee/ When Payable Frequency Amount in Rupees

No Charge levied

3

4

For any loan sanctioned to individual borrowers with or without co-obligants no

prepayment charges shall be payable on account of part or full prepayments

made through any sources, except when the loan is sanctioned for business

purpose**.

B. On Foreclosure/Prepayment Charges

A. Adjustable Rate Loans (ARHL)

and

Combination Rate Home Loan (“CRHL”)

during the period of applicability of the

Variable Rate of interest

B. Fixed Rate Loans (“FRHL”)

and

Combination Rate Home Loan (“CRHL”)

during the period of applicability of the

Fixed Rate of interest

Housing Loans

Non Housing Loans and loans classified as business loans**

For all loans sanctioned with or without co-obligants, the prepayment charge

shall be levied at the rate of 2%, plus applicable taxes/statutory levies of the

amounts being so prepaid on account of part or full prepayments except when

part or full prepayment is being made through own sources*.

No prepayment charges shall be payable on account of part or full prepayments

on Loans against Property / Home equity loans sanctioned to individuals for

other than business purposes**

For all loans sanctioned with or without co-obligants, the prepayment charge

shall be levied at a rate of 2% plus applicable taxes/statutory levies of the

amounts being so repaid on account of part or full prepayment.

A. Adjustable Rate Loans (ARHL)

and

Combination Rate Home Loan (“CRHL”)

during the period of applicability of the

Variable Rate of interest

B. Fixed Rate Loans (“FRHL”)

and

Combination Rate Home Loan (“CRHL”)

during the period of applicability of the

Fixed Rate of interest

For all loans sanctioned with or without co-obligants, the prepayment charge

shall be levied at a rate of 2% plus applicable taxes/statutory levies of the

amounts being so repaid on account of part or full prepayments.

5. Top up loans for Business Purpose i.e. Working Capital, Debt Consolidation, Repayment of Business Loan, Expansion of

business, Acquisition of Business asset or any similar end usage of funds.

2. Loans against property / Home Equity Loan for Business Purpose i.e. Working Capital, Debt Consolidation, Repayment of

Business Loan, Expansion of business, Acquisition of Business asset or any similar end usage of funds.

BUSINESS LOANS: **The following loans shall be classified as business loans:

1. LRD loans

3. Non Residential Properties

OWN SOURCES: *the expression "own sources" for this purpose means any source other than borrowing from a

Bank/HFC/NBFC or Financial Institution.

4. Non Residential Equity Loan

The Borrower will be required to submit such documents that HDFC may deem fit & proper to ascertain the source of funds at the

time of prepayment of the loan.

The prepayment charges are subject to change as per prevailing policies of HDFC and accordingly may vary from time to time.

Borrowers are requested to refer to www.hdfc.com for the latest charges applicable on prepayments.

5

The Borrower shall:

(ii) Regularly provide HDFC information, including details regarding progress/delay in construction, any major damage

to the property, non-payment of taxes and statutory levies and charges, as may be applicable from time to time

pertaining to property, etc.

4. Brief Procedure to be followed for Recovery of overdue amounts:

Borrowers are explained the payment process of the loan in respect of, tenure, periodicity, amount and mode of repayment of

the loan. No notice, reminder or intimation shall be given to the Borrower regarding his/her obligation to pay the EMI or PEMI

regularly on due date.

The recovery process of enforcement of mortgage/ securities, including but not limited to, taking possession and sale of the

mortgaged property in accordance with the procedure prescribed under the Securitisation and Reconstruction of Financial

Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act) or under any other law, is followed as per the

directions laid down under the respective law. Intimation/ Reminders/ Notice(s) are given to Borrower prior to initiating steps

for recovery of overdues, under the Negotiable Instruments Act, Civil Suit as well as under the SARFAESI Act.

(iii) Ensure that construction being undertaken is as per the approved plan and has satisfied himself/herself that all

required approvals for the project have been obtained by the developer (by the seller incase of resale purchase of

property).

Not with standing what is stated herein, it shall be the liability of the Borrower to ensure that the Pre-EMI/ EMls are regularly

paid on the due dates.

(iv) Satisfy HDFC on the utilization of the proceeds of any prior disbursements of the loan amount and provided

adequate proof of the same.

g. Ensure that no event of default has happened in terms of the Loan Agreement executed/ to be executed by the borrower.

h. Ensure that there is no breach of the terms of the Offer Letter/Loan Agreement.

i. The following conditions shall be applicable for all loans.

(i) Pay the own contribution amount (total cost of unit less the loan amount), as specified in the Sanction Letter.

(v) Furnish End Use Certificate for Equity / Top-up Loans.

On non-payment of Pre-EMI/EMI by the due dates, HDFC shall remind the Borrowers by making telephone calls, sending

written intimations by post and electronic medium or by making personal visits by HDFC's authorized personnel at the

address/es provided by the Borrower. Costs of such calls/communication/visits shall be recovered from the Borrower.

Credit information relating to any Borrower's account is provided to the Credit Information Bureau (India) Limited (CIBIL) or

any other licensed bureau on a monthly basis. To avoid any adverse impact on the credit history with CIBIL, it is advised that

the Borrower should ensure timely payment of the amount due on the loan amount.

(c) Insurance of Borrower : The Borrower may avail health and /or life insurance cover for himself with HDFC as the sole

beneficiary under the policy/ policies.

e. Ensure that he has absolute, clear and marketable title to the property (security) and the said property is absolutely

unencumbered and free from any liability whatsoever.

f. Ensure that no extra-ordinary or other circumstances have occurred which shall make it improbable for the Borrower to

fulfill his obligations under the Loan Agreement for the present loan.

2. (a) Insurance of property

The Borrower shall ensure that the property is, during the pendency of the loan, always duly and properly insured against

all risks such as earthquake, fire, flood, explosion, storm, tempest, cyclone, civil commotion, etc. HDFC be made the sole

beneficiary under the policy/policies.

(b) In the event the Borrower fails to provide insurance for the property duly assigned in favor of HDFC, HDFC shall have t h e

option to procure insurance for the Property to preserve the property from destruction and recover the same from the

Borrower.

3. Conditions for disbursement of the loan

The Borrower shall:

a. Submit all relevant documents as mentioned in the Sanction Letter/ Loan Agreement/ KYC Policy of HDFC.

b. Intimate HDFC of any change in his employment/ contact details/ other KYC related detaiIs.

c. Request for disbursement of the loan in writing (as per the manner prescribed by HDFC). Such request shall be deemed

to have been duly made when made by hand, mail or through website of HDFC (www.hdfc.com) or such other form/

manner as may be announced by HDFC from time to time.

d. Comply with all preconditions for disbursement of the loan as mentioned in the Sanction Letter.

6

5. Customer Services

HDFC Ltd, HDFC House, HT Parekh Marg, 165-166, Backbay Reclamation, Churchgate, Mumbai 400 020.

i) Customer Service Queries including requirement of documents can be addressed to HDFC through the following

channels: Write to us through our website: www.hdfc.com or notify us at:

iii) The Corporation shall endeavour to keep its customers informed of any change in interest rates / charges etc. through

letters or any other form of general or public announcement or displays, from time to time. In case such change is

disadvantageous to the customer he/ she may close his account within 60 days of the intimation of the change.

a. Photo Copies of documents, can be provided in 15 working days from date of placing request. Necessary

administrative fee shall be applicable.

c. Loan Account statement (time line): Within 7 working days of the receipt of request.

6. Grievance Redressal:

There can be instances where the Borrower is not satisfied with the services provided by HDFC in reference to the Loan

availed. To highlight such instances & register a grievance the Borrower may follow the following process:

a. The Borrower can post their grievance on our website www.hdfc.com or

The Chief Greivance Redressal Officer,

c. The Corporation shall endeavour to address/respond to all grievances within a time frame of six weeks of receipt of a

grievance and keep the borrowers informed about the status of their grievances.

ii) Visiting hours and the details of person to be contacted for Customer service with respect to all branches of HDFC are

available at www.hdfc.com.

b. Original documents will be returned within 21working days from the date of closure of loan. Necessary administrative

fee shall be applicable if the documents are collected beyond due date of release of documents.

d. In case the grievance remains unresolved beyond a period of 7 working days, the borrower may escalate the grievance to

the Chief Grievance Redressal Officer at:

iv) Contact HDFC Customer Service Officer at your nearest branch within the working hours as mentioned in the Loan

Application form for:

b. Borrower can meet or write to the Business Head for the respective dealing branch

Ramon House, H T Parekh Marg, 169, Backbay Reclamation, Churchgate, Mumbai 400020

(Signature or thumb impression of the Borrower/s)

f. The Borrower shall be entitled to raise any complaints regarding concerns with respect to the Loan and/or the services

being provided by HDFC. Any matter which is not related directly to the provision of such financial services by HDFC

(such as services/good/ provided by a third party and/or concerns related to the property and/ or project and/or insurance

products and/or any matter which is beyond the scope and purpose of the Loan Agreement and/or MITC) shall not qualify

as a valid Grievance and shall, therefore, not be addressed or responded to by HDFC.

e. In case the grievance remains unresolved beyond a period of 14 working days, the borrower may escalate the grievance

to the Managing Director at::

HDFC Ltd, HDFC House, HT Parekh Marg,165-166, Backbay Reclamation, Churchgate, Mumbai 400 020.

____________________________________________

(Signature of the authorized person of HDFC)

It is here by agreed that for detailed terms and conditions of the Loan, the parties here to shall refer to and rely upon the

loan and other security documents executed/to be executed by them. The above terms and conditions have been read by

the borrower/s / read over to the borrower by Shri/Smt. ____________________________________________________

_____________________________ of HDFC and have been understood by the borrower/s.

The Managing Director,

___________________________________________

g. In case of non redressal of grievance within 30 working days of registering the grievance the borrower may approach the

Complaint Redressal Cell of National Housing Bank by lodging its complaints in Online mode at the link

https://grids.nhbonline.org.in OR in offline mode by post, in prescribed format available at link

https://grids.nhbonline.org.in/(S(rvmej3wn0zroukvwus0aetc3))/Complainant/Default to Complaint Redressal Cell,

Department of Regulation & Supervision, National Housing Bank, 4th Floor, Core 5A, India Habitat Centre, Lodhi Road,

ND-110023.