Global Credit Outlook 2024

New Risks, New Playbook

Dec. 4, 2023

This report does not constitute a rating action.

Foreword

Dear reader,

Looking ahead at 2024 and after, it’s clear that the events since the COVID-19 pandemic have

brought on a profound transformation for the global economy and financial markets. While some

of the same challenges remain, other risks have emerged—all of which require a new playbook

for issuers and investors in the debt markets.

We are back to an environment of higher real interest rates, concluding an era of cheap money

that started in the wake of the Great Financial Crisis. With a durably higher cost of debt, a ramp-

up in maturities, and slowing economic activity in the cards for 2024, the focus comes back to

credit fundamentals and liquidity analysis. While still-robust employment levels and supportive

fiscal conditions should continue to underpin the resilience of stronger credits, we expect 2024

to come with additional credit deterioration and defaults for more vulnerable corporate and

government issuers.

Geopolitical risks have returned to center stage, with the war between Israel and Hamas, the

prolonged Russia-Ukraine conflict, and the ongoing U.S.-China tensions. This increased

geopolitical fragmentation affects corporates and governments in their strategies for supply

chain and energy security, with potential broader implications on food prices, global trade, and

inflation—while increasing the potential for event risk. New challenges are also emerging from

the necessity to accelerate the world’s transition to a low-carbon economy to limit the potential

dramatic consequences of climate change. At the same time, generative artificial intelligence (AI)

and an accelerating technological transformation, along with heightened risks from cyber

attacks, are forcing corporate and government entities to adapt their playbooks.

Against this backdrop, S&P Global Ratings’ Global Credit Outlook 2024 presents our credit and

macroeconomic outlooks for the year ahead, including our base-case forecasts, assumptions,

and key risks for what promises to be yet another challenging period for the global economy and

markets. Aligned with these risks, we address the questions that will shape 2024—about credit

headwinds; capital flows; geopolitical uncertainty; energy and climate resilience; and crypto,

cyber, and tech disruption—collected through our interactions with market participants.

This report harnesses the power of our regional and global Credit Conditions Committees (CCC),

which meet quarterly to review conditions in Asia-Pacific, Emerging Markets, Europe, and North

America, cascading into our global coverage. At the CCCs, we evaluate the trends affecting

economies, industries, and credit markets—to identify the base case and downside scenarios

and rank the exogenous risks that underpin our credit ratings and inform potential rating

changes across various asset classes. This publication also highlights the depth and breadth of

S&P Global Ratings’ analysts and the Credit Research & Insights team’s expertise on credit

markets.

Alexandra Dimitrijevic

Global Head of

Research

and Development

Co

-Chair, Global CCC

London

Gregg Lemos-Stein

Chief Analytical Officer,

Corporate Ratings

Co

-Chair, Global CCC

New York

gregg.lemos

Acknowledgements

We would like to thank the many

colleagues who have contributed

to this report to provide you with

S&P Global Ratings' essential

insights.

Special thanks to Ruth Yang, Molly

Mintz, Joe Maguire, Fatima Tomas,

Tom Lowenstein, Hilary Castle,

and

Nick Kraemer

.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 2

Contents

Global Credit Outlook 2024: New Risks, New

Playbook

4

Top Global Risks

14

Global Economic Outlook

16

Questions That Matter

21

Credit Headwinds

Corporates | Could interest rate and recession risks derail corporate credit?

22

Real Estate | Is the worst over for the global office sector and China’s residential market?

24

Capital Flows

Private Markets | How long can the golden age of private credit last?

27

Market Dynamics | How will the path of interest rates in 2024 affect corporate borrowing

strategies?

30

Geopolitical Uncertainty

Sovereigns | What are the credit implications of intensifying conflicts and political

disruption?

33

Emerging Markets | Which EMs are better positioned to outperform in 2024?

36

Energy and Climate Resilience

Physical Climate Risk | How will challenging credit conditions affect resiliency and

adaptation to more costly climate hazards in 2024?

39

Energy Transition | Can the shift to net-zero accelerate amid growing headwinds?

43

Cyber, Crypto, And Tech Disruption

Artificial Intelligence | What are the key credit risks and opportunities of AI?

46

Digital Assets | Will technological and regulatory developments unleash institutional

blockchain adoption?

49

Regional Credit Conditions

52

North America

53

Europe

55

Asia-Pacific

57

Emerging Markets

59

Contacts

61

Disclaimer

62

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 3

Contacts

Alexandra Dimitrijevic

London

alexandra.dimitrijevic

@spglobal.com

Gregg Lemos

-Stein

New York

gregg.lemos

-stein

@spglobal.com

Ni

ck Kraemer

New York

nick.kraemer

@spglobal.com

Cont

ributors

Joe Maguire

New York

joe.maguire

@spglobal.com

Molly Mintz

New York

molly.mintz

@spglobal.com

Global Credit Outlook 2024

New Risks, New Playbook

This report does not constitute a rating action.

An environment of increasingly rapid change, which began with the onset of the global COVID-19

pandemic, requires financial market participants to adapt their playbooks. Conditions that

borrowers and investors could safely take for granted for a decade or more have been pushed

aside. Most importantly, perhaps, is that markets can no longer expect ultra-accommodative

monetary policy and low inflation will be the norm.

S&P Global Economics expects real interest rates to remain elevated through 2024, with the

Federal Reserve unlikely to begin a cycle of policy-rate cuts before June, assuming core

inflation approaches the central bank's target. We expect a series of four quarter-point cuts,

which would bring the federal funds target rate to around 4.6% by the end of the year and 2.9%

by end of 2025.

Similarly, eurozone key rates may have peaked, but could take a long time to come down. We

forecast the European Central Bank will gradually lower its policy rate starting in June—with

three quarter-point moves in the year before easing further toward neutral levels in 2025.

The Fed will influence the magnitude of easing by emerging market (EM) central banks.

Disinflation will likely continue across most EMs in the coming quarters, which we expect will

encourage central banks to start lowering interest rates or continue doing so for those that have

already started. However, swings in the Fed's policy expectations will matter. If the Fed's policy is

more hawkish than what is implied by the market, EM interest rate curves are likely to adjust

Key Takeaways

• Borrowers across all asset classes will need to adjust to tighter financing conditions and

softer economic growth. While long-term yields will likely peak around midyear, financing

conditions will likely stay tight in real terms in 2024. Borrowers have reduced near-term

maturities, but the share of speculative-grade debt coming due rises significantly in 2025,

making 2024 a pivotal year. Defaults will likely rise further, to 5% in the U.S. and 3.75% in

Europe, above their long-term historical trends.

• We expect additional credit deterioration in 2024, largely at the lower end of the ratings

scale, where close to 40% of credits are at risk of downgrades. Sectors exposed to a

decline in consumer spending are most vulnerable. Meanwhile, investment-grade credits

should generally continue to show resilience despite some margin compression—with the

exception of the real estate sector.

• The main risks that could derail our baseline expectations, leading to further credit

deterioration, include persistent tight financing conditions amid entrenched inflation; a

sharper-than-expected slowdown in global growth; elevated input-cost inflation and high

energy prices that squeeze corporate profits and pressure governments’ fiscal balances;

vulnerable commercial real estate; and amplifying geopolitical tensions.

• Looking ahead, heightened geopolitical risks, the need to accelerate the decarbonization

of the economy to address the rise in climate-related risks, and the technology revolution

will increasingly shape the future of credit.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 4

upward, and central banks will likely proceed more cautiously with easing to prevent disorderly

capital outflows.

Global GDP growth is likely to slow significantly in 2024, to 2.8%, after a surprising resilience in

2023 fueled by strong employment, healthy consumer spending, and post-COVID tailwinds. As

the lagging effects of tighter monetary policy and diminished consumer purchasing power work

through major economies, we expect the U.S. to slip into a period of below-trend growth, with

Europe bordering on recession, and pain in China's property sector (along with high leverage on

corporate and local government balance sheets) dragging on economic activity. Given the

resultant hit to business and household confidence, we now expect China real GDP growth next

year of just 4.6%, and we think that could fall below 3% if the property crisis further deteriorates.

Overall, our base case is for a soft landing, but the risk of recession remains elevated (30%-35%

in the U.S.).

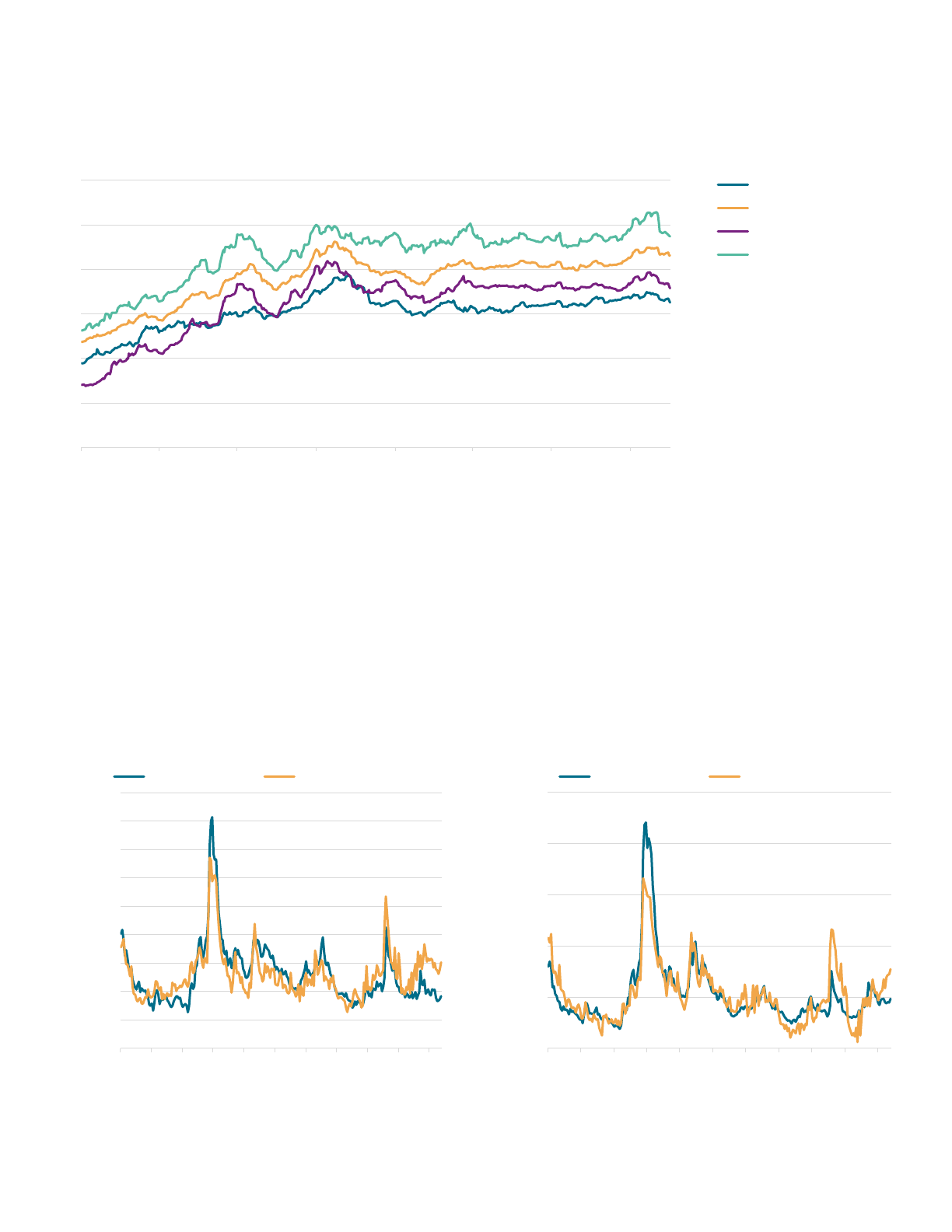

Chart 1

*Growth in debt due in 2025 as of Jul. 1, vs debt due in 2024 a year earlier. ECB--European Central Bank. IG--Investment

grade. ROW--Rest of world. SG--Speculative grade. Source: S&P Global Ratings.

On the back of a slowing economy and the high cost of debt, we expect further credit

deterioration in 2024, continuing the diverging trends of resilience at the investment-grade level

and downgrades largely at the lower end of the ratings scale. This is reflected in the 9.4% of

investment-grade credits with negative outlooks or on CreditWatch with negative implications

(below the historical average), and negative outlooks on speculative-grade (rated 'BB+' or lower)

and 'B-' and below credits, in particular, at 19.6% and 37.4%, respectively—indicating significant

downgrade risk ahead. For global nonfinancial corporate debt, the net outlook bias, which

indicates potential rating trends, is at negative 8.4%, back to pre-COVID levels (see chart 2).

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 5

Chart 2

Global financial and nonfinancial corporate net bias (%)

Net bias--The difference between ratings with a positive outlook or on CreditWatch with positive implications and those with

a negative outlook or on CreditWatch negative. Source: S&P Global Ratings.

Sectors most exposed to a decline in consumer spending face higher risk of downgrades. The

consumer products sector has the highest negative bias—with 22.3% of issuers having a negative

outlook or on CreditWatch with negative implications. Two sectors, health care, and

homebuilders and real estate, suffered the highest deterioration in terms of increased negative

bias in 2023 (see chart 3). On the other side, the oil and gas sector has the highest positive bias,

at 17.5%, as energy cash flows remain strong despite geopolitical challenges and weaker prices.

Chart 3

Global negative bias by sector (%)

Q4 data as of Nov. 15, 2023. Source: S&P Global Ratings.

Defaults are poised to rise. Defaults have already picked up to above historical averages in the

U.S. and Europe, and are poised to increase further in 2024 as debt maturities ramp up and

competition for funding intensifies. S&P Global Ratings now expects the trailing-12-month

speculative-grade default rates in the U.S. and Europe to reach 5% and 3.75%, respectively, by

September, under our base case for a soft landing. In the U.S., the proportion of ‘CCC/C’ ratings

among all corporate borrowers is historically large, at 7%, with many of these firms suffering

-40

-35

-30

-25

-20

-15

-10

-5

0

Jan. 2020 Jul. 2020 Jan. 2021 Jul. 2021 Jan. 2022 Jul. 2022 Jan. 2023 Jul. 2023

0

5

10

15

20

25

Aerospace and defense

Automotive

Capital goods

Chemicals, packaging and

environmental services

Consumer products

Diversified

Financials (excl.

insurance)

Forest products and

building materials

Health care

High technology

Homebuilders/real estate

Insurance

Media and entertainment

Metals, mining and steel

Oil and gas

Retail/restaurants

Telecommunications

Transportation

Utility

Q1 2023 Q2 2023 Q3 2023 Q4 2023

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 6

negative cash flows and large maturities due in 2024 and 2025. This signals a high level of

sensitivity to a drop in growth or a further rise in interest rates, which could push the default rate

to our pessimistic scenario of 7%. In Europe, too, debt coming due in 2024-2025 will force many

lower-rated borrowers to refinance at much higher rates than they enjoyed over the past five

years. This would further strain cash flows and could keep the default rate elevated into late-

2024 or beyond.

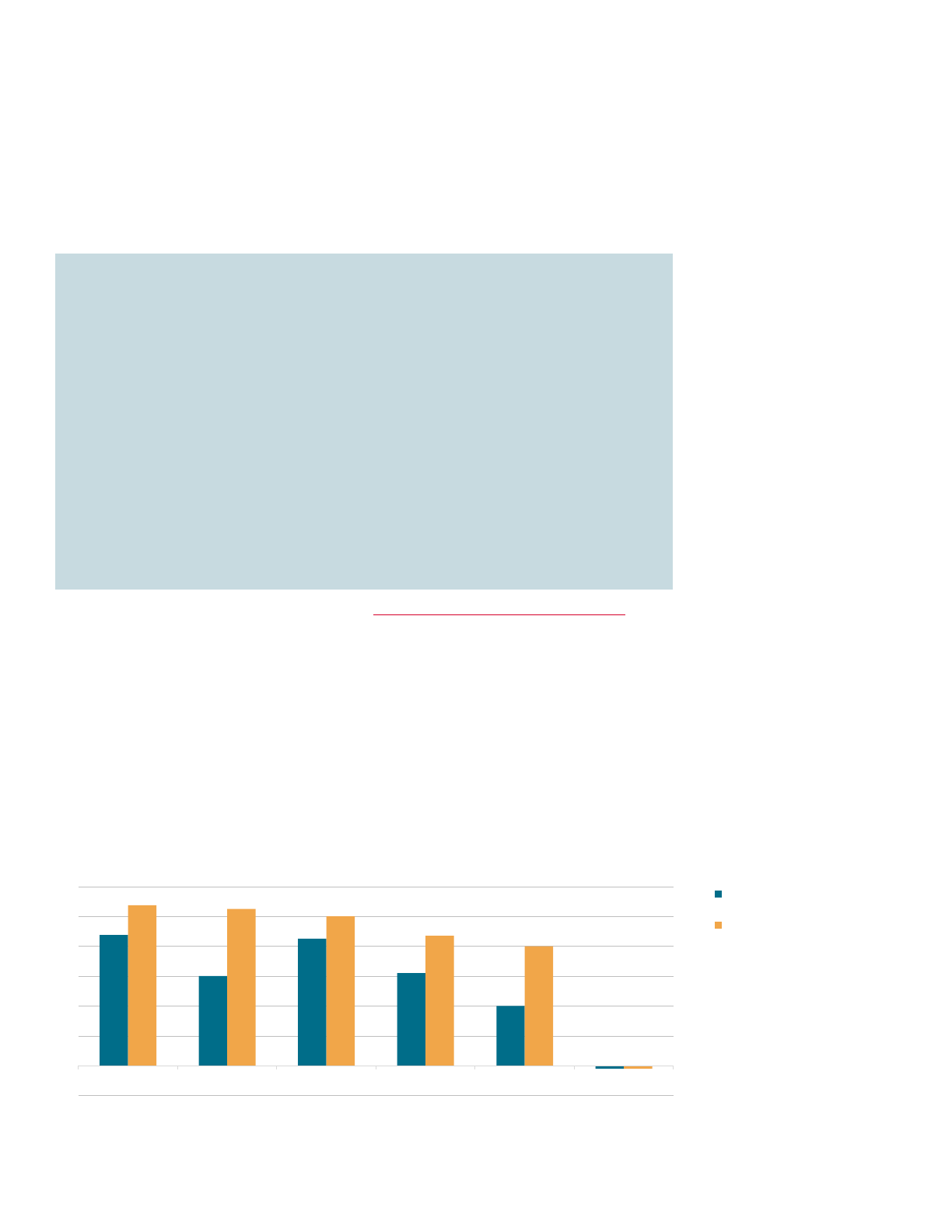

With no clear signs that long-term yields will fall materially any time soon, financing conditions

will likely continue to tighten in real terms in 2024, particularly given the steeper maturity wall

beginning in 2025. While borrowers globally have reduced near-term maturities—trimming

speculative-grade corporate debt due in 2024 by 34% in the past year—the share of speculative-

grade debt coming due rises in coming years, reaching a peak in 2028 (see chart 4). The U.S.

accounts for the bulk of upcoming debt maturities rated 'B-' and below (see chart 5).

For emerging markets, maturities start to ramp up in 2024 and increase further in 2026-2027. U.S.

dollar strength is compounding the pressures on many, given the $46 billion of rated dollar-

denominated debt coming due next year (excluding China).

Chart

4

Speculative

-

grade nonfinancial corporate maturities rise in

upcoming years

(bil. $)

Chart

5

U.S. accounts for most of the upcoming 'B

-' and lower

maturities

(bil. $)

Data as of Jul. 01,

2023. Includes nonfinancial corporate issuers' bonds, loans, and revolving credit facilities that are rated 'BB+' or lower by S&P Global Ratings.

Excludes debt instruments that do not have a global scale rating. Foreign currencies are converted to U.S. dol

lars at the exchange rate on Jul. 01, 2023. Source: S&P

Global Ratings Credit Research & Insights.

Borrowing Costs Are Likely To Remain Elevated Through 2024

Borrowers will need to adjust to tighter financing conditions (see chart 6). Long-term rates have

been elevated for most of the past 18 months, and even as central banks have paused rate hikes,

the bite of quantitative tightening has come alongside increased borrowing by the U.S. Treasury.

This has boosted Treasury yields, pulling most other governments’ benchmark rates up with

them. At the same time, corporate yields from the U.S. to Europe to Latin America have all risen

roughly 4% since the start of 2022.

0

100

200

300

400

500

600

700

800

900

1,000

2024 2025 2026 2027 2028

(Maturity year)

0

50

100

150

200

250

300

2024 2025 2026 2027 2028

(Maturity year)

US Europe Rest of world

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 7

Chart 6

Higher-for-longer: corporate yields elevated globally (%)

EM--Emerging market. HY--High yield. Sources: ICE Data Indices, LLC, ICE BofAML yield indices effective yields, retrieved

from FRED, Federal Reserve Bank of St. Louis, S&P Global Ratings Credit Research & Insights.

And while bond spreads haven't tightened considerably this year, we estimate that current

spreads may be well narrower than what is appropriate—as has been the case through most of

the post-pandemic period. The speculative-grade bond spread in the U.S. was at 367 basis points

(bps) at the end of October, compared to our estimate of 604 bps; the European equivalent

spread was at 483 bps, compared to our estimate of 771 bps (see charts 7 and 8). It is more likely

that any widening of spreads ahead will be the result of even higher corporate yields rather than

a major decline in risk-free rates. And if a recession were to occur, spread widening would likely

be particularly acute.

Chart

7

Actual versus estimated spreads, U.S.

bps

--Basis points. SG--Speculative grade. Source: S&P Global Ratings.

Chart

8

Actual v

ersus estimated spreads, Europe

HY

--High yield. Sources: ICE Data Indices, LLC, ICE BofAML yield indices

effective yields, retrieved from FRED, Federal Reserve Bank of

St. Louis, S&P

Global Ratings Credit Research & Insights.

0

2

4

6

8

10

12

Dec. 2021

Mar. 2022 Jun. 2022 Sep. 2022 Dec. 2022 Mar. 2023 Jun. 2023 Sep. 2023

Asia EM

Latin America EM

Europe HY

U.S. 'B'

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

(bps)

SG spread Estimated spread

0

5

10

15

20

25

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

(%)

HY spread Estimated spread

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 8

Corporate borrowers are already feeling the effects of elevated interest rates, and the erosion

of margins is also becoming evident, with almost two-thirds of industries globally seeing annual

margins decline in the third quarter, albeit from relatively high levels. Further margin erosion on

the back of weaker growth would likely have longer-term implications and feed into an increase in

unemployment.

At the same time, the resilience of consumers may not last much longer—particularly in the U.S.,

for those at the lower end of the income scale. Household savings, once fattened by COVID-

related stimulus, are shrinking, and consumers are becoming more wary of spending, especially

on discretionary goods. Spending on services is now back to its pre-pandemic trend, leaving little

pent-up demand. Moreover, real disposable income in the U.S. has declined four months in a row,

with the savings rate falling to a very low 3.4% in September.

By contrast, in Europe, notwithstanding higher mortgage costs in countries exposed to variable

rates, we anticipate the consumer will provide support to growth next year as real disposable

incomes rise on the back of relatively high wage growth and disinflation.

EM corporates will face increasing headwinds in 2024 as growth in major economies slows, cost

pressures linger, the effects of rapid monetary-policy tightening surface, and debt maturities pile

up. For many borrowers, this will mean falling revenues amid increasing financing costs as debt

comes due, resulting in weaker cash flows.

Nonfinancial corporates’ revenue growth has stalled, and EBITDA continues to decline. Third-

quarter results showed that, at an annual rate, global revenues were near-flat, rising just 0.3%

(and down 1.4% vs. the same quarter a year earlier), with EBITDA falling 4.4%. Moreover, the

pressure from surging cash interest payments is growing apace, up an aggregate 23% annually

overall and 27% for speculative-grade borrowers. Leverage is drifting higher, and interest-cover

continues to erode.

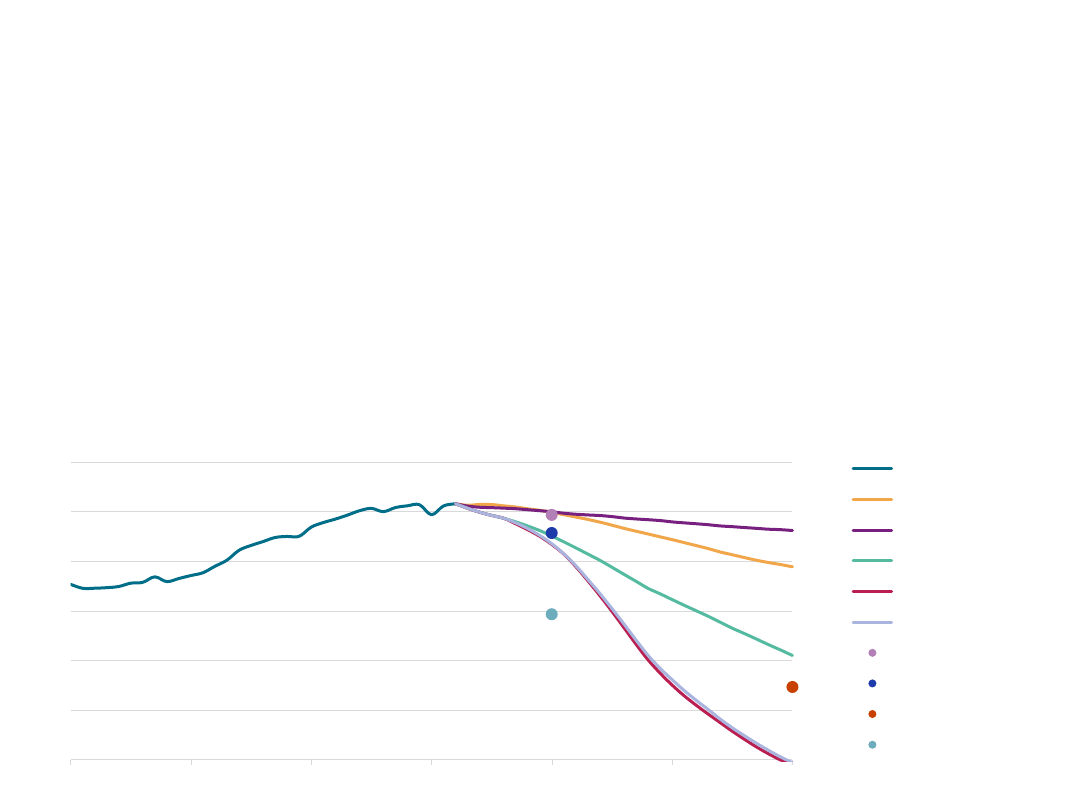

Our global and regional Credit Cycle Indicators (CCIs) suggest a credit correction will persist

through 2024. We believe the tailwinds from the post-pandemic recovery, stronger-than-

expected economic resilience in 2023, some degree of fiscal stimulus still in place, and pushed-

out debt maturities have delayed the peak in credit stress. While the CCIs show nascent signs of

a trough, a credit recovery looks unlikely to occur before 2025.

Chart 9

A credit upturn may not come until 2025

Global Credit Cycle Indicator (standard deviations)

Data as of Q1 2023. Note: Peaks in the CCI tend to lead credit stresses by six to 10 quarters. When the CCI’s upward trend is

prolonged or the CCI nears upper thresholds, the associated credit stress tends to be greater. Sovereign risk is not included

as a formal part of the CCI. Sources: Bank for International Settlements, Bloomberg, S&P Global Ratings.

-3

-2

-1

0

1

2

3

4

1995 Q1 1998 Q1 2001 Q1 2004 Q1 2007 Q1 2010 Q1 2013 Q1 2016 Q1 2019 Q1 2022 Q1

CCI

Household sub-

indicator

Corporate sub-

indicator

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 9

Amid steeper funding costs and more-selective lending, risks of further increases in

nonperforming loans and defaults could shape credit conditions in 2024. For banks, this could

mean increased credit losses. But while most asset-quality measures have been worsening, it is

generally more a normalization toward historical averages in most cases. Although we expect

further weakening in 2024, we believe that owing to decent pre-provision earnings, banks are

generally well-positioned to absorb associated credit losses.

All told, our outlook for global banks remains steady. As of Oct. 31, 79% of bank ratings outlooks

were stable, with this resilience largely due to solid capitalization, improved profitability, and still-

sound asset quality. Still, higher-for-longer interest rates and continuing stress in the office

sector may mean elevated commercial real estate (CRE)-related loan losses for debtholders,

such as U.S. banks—with regional banks more exposed as a percentage of assets than their

larger competitors.

Recovery prospects for corporate debt remain under pressure. Even before macroeconomic

concerns about higher-for-longer interest rates and uncertain economic growth, there was an

expectation that bloated debt structures with high debt leverage and concentrations of first-lien

debt and covenant-lite structures might weigh on recovery rates given default.

In the U.S., our average expectation for future first-lien recoveries (using the rounded recovery

percentages that are part of our recovery ratings) is 64%—well below the long-term historical

average of 75%-80% (see chart 10). Average recovery expectations for first-lien debt of issuers

rated ‘B,’ ‘B-,’ and in the ‘CCC’ category are lower still, at 61%, 59%, and 58%, respectively.

Further, out-of-court restructurings will likely push many first-lien recoveries lower and increase

dispersion.

Chart 10

Expected recovery on newly issued North America first-lien debt (%)

Data through Sept. 30, 2023, based on the rounded point estimates included in our recovery ratings for rated nonfinancial

corporate entities in the U.S. and Canada. Source: S&P Global Ratings.

For Europe, our average expectation for future first-lien recoveries is 59%--compared to the

long-term historical average of 70%-75%. Average recovery expectations for European first-lien

debt of issuers rated ‘B,’ ‘B-,’ and in the ‘CCC’ category are 63%, 58%, and 51%, respectively. The

generally lower European recovery expectations reflect a heavier concentration of first-lien-only

debt structures.

60

62

64

66

68

70

72

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2017 2018 2019 2020 2021 2022 2023

New 1L debt, average

recovery estimate

Average outstanding

recovery

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 10

Will Sovereigns Unwind Their Fiscal Stimulus?

Much of the recent global economic resilience has been bolstered by governments' large,

expansionary fiscal stimulus. Given the associated increase in governments' debt leverage,

policymakers will eventually have to unwind at least some of this support—especially given the

cost of servicing debt in a higher-for-longer interest-rate environment.

The scaling back of stimulus will likely weigh on demand and dent economic activity, and is thus

complicated by upcoming national elections in more than 50 countries, both developed and

emerging.

Increased geopolitical strife threatens to disrupt the credit landscape. The escalating war

between Israel and Hamas adds another dimension to existing geopolitical tensions, already

intensified by the prolonged fighting between Russia and Ukraine. Any significant spread of the

fighting in the Middle East raises the potential for energy-supply shocks and the renewed

dislocation of supply chains that had more or less normalized once the worst of the pandemic

passed.

While we think there is a broad desire that the conflict remain contained and for other countries

in the region not to participate directly, the possible involvement of Hezbollah (a well-armed

Lebanese Islamist political and militant group with close ties to Iran) would risk drawing in Iran

and, conceivably, the U.S.

Against this backdrop, key potential channels of transmission to the rest of the world could

include: an energy-supply shock, as price pressures and volatility in the oil market would almost

certainly increase if the conflict escalated significantly; supply-chain disruptions, which could

underpin inflation at a time of increasing economic uncertainty; and a surge in social unrest, with

the possibility of protests or outbreaks of violence becoming politically destabilizing across the

Middle East and beyond.

From an energy-supply perspective, the Middle East conflict is especially concerning, given that

roughly one-third of the world's liquefied natural gas and almost one-quarter of its oil travels

through the 104-mile strait of Hormuz, which is the only shipping route from the Persian Gulf to

the open sea.

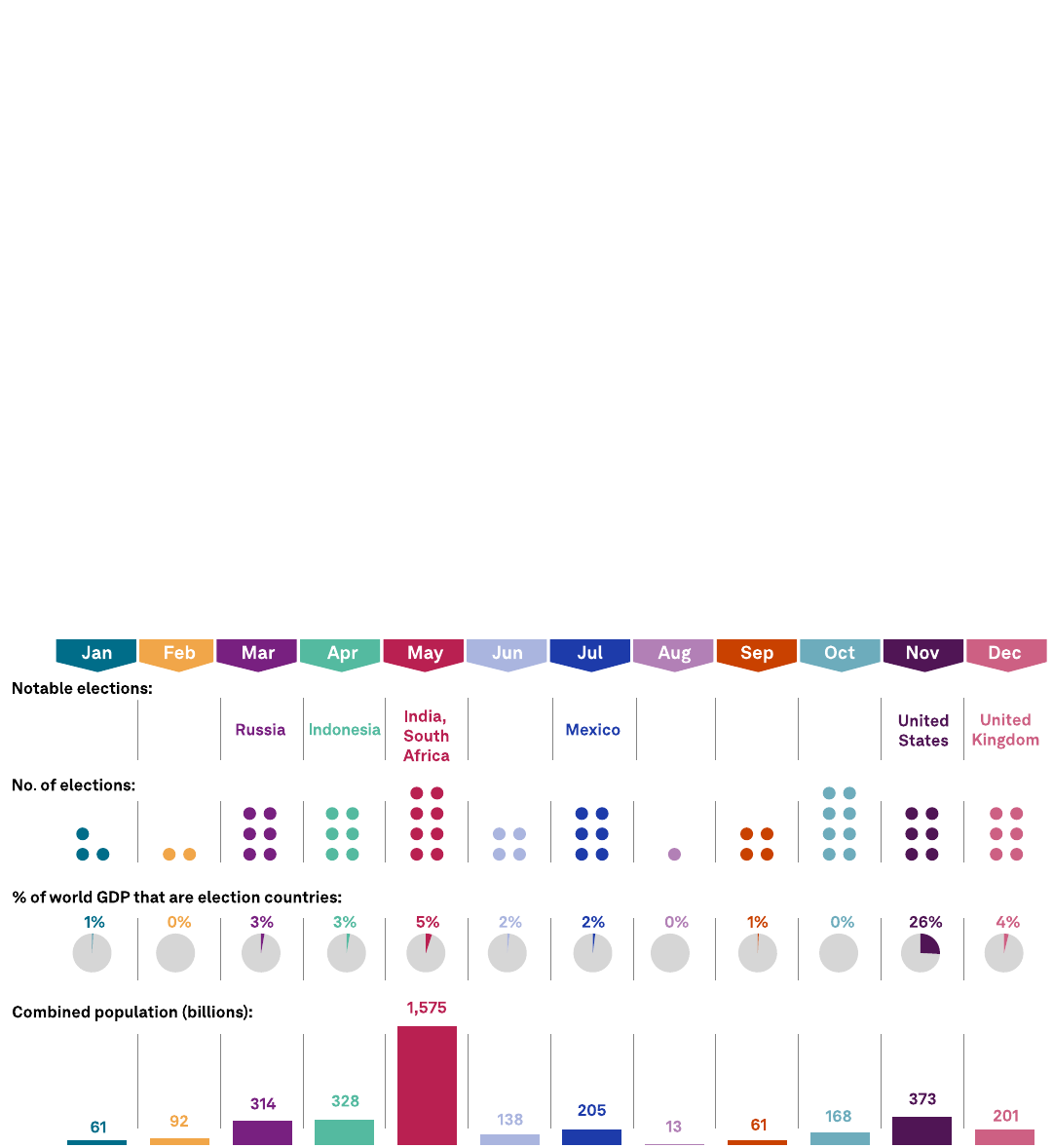

Meanwhile, there are elections (presidential and/or legislative) in more than 50 countries in

2024, many of which could have global ramifications (see chart 11).

Both Russia and Ukraine, mired in a war that will soon enter its third year, have presidential

elections in March.

Adding a layer of uncertainty to both the Middle East and Russia-Ukraine situations are the U.S.

presidential and legislative elections in November, given the different positions in Congress

regarding support for additional funding for Ukraine and Israel.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 11

Chart 11

Key elections in 2024

Source: S&P Global Ratings.

Real Estate Remains Under Pressure

Worries about real estate remain around the globe, albeit with varying dynamics. In the U.S. and

Europe, the focus has been on commercial real estate—in particular, the office space—while in

China, the ongoing downturn in residential real estate is dragging on the economy.

In the West, CRE concerns have shifted from how pandemic-prompted pressures hurt hotels and

retail properties to how hybrid and remote work patterns have depressed demand for office

space. Asset valuations have declined in many major cities across the U.S., U.K., and continental

Europe. The sharp rise in interest rates has weighed on borrowers’ interest coverage and raised

refinancing risk.

In both the U.S. and Europe, higher financing costs, falling asset values, and declining cash flows

mean that debtholders—including banks, insurers, and commercial mortgage-backed securities

(CMBS)—could suffer elevated loan losses. The need to upgrade properties to meet ever-

increasing energy-efficiency standards is putting additional pressures on landlords in many

European countries.

Pressures in the sector will likely be drawn out. Office leases can last 10 years or more and

lenders (of which the majority are banks) have been more willing to extend loan maturities in

anticipation of an eventual decline in interest rates. But almost four years past the onset of the

pandemic, it’s clear that the secular shifts mean the office sector may need years to recover

from the recent downturn.

In China, the focus instead is on residential real estate and property development, which has

been mired in a prolonged downturn since late 2021. Weak property sales, particularly in lower-

tier cities, are persisting despite stimulus measures from Beijing. Slowing residential sales, which

fell nearly 4% in January-October 2023 (compared to the same period in 2022), are hitting

property developers’ cash flows and land sales—which are a key source of revenue for local and

regional governments.

Egypt presidential Iran legislative Taiwan both Ukraine both

India legislative Mexico both U.K. legislative Venezuela presidential

Indonesia both Russia presidential U.S. both

Election types by location

50+

countries

70+

elections

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 12

China Faces Stresses At Home And Abroad

This pain in the property market is dragging on China's economic rebound and driving downside

risk. While the worst may be over for China’s property developers, S&P Global Ratings expects

property sales to stay depressed amid the low number of construction starts, an inventory

overhang in lower-tier cities, and ever-tightening escrow restrictions.

We think a worsening of the property crisis (which assumes a further 20%-25% decline in 2024

property sales from 2022) could push China’s economy—long the engine of global GDP growth—

below 3% in 2024, compared to our base case of 4.6%.

At the same time, the U.S.-China relationship remains strained. With the U.S. presidential

elections set for November, bilateral tensions could intensify amid U.S. domestic political

posturing. Concurrently, the U.S.’ ongoing export curbs of advanced chips to China and limits on

investment in China’s advanced-tech sector, could cause renewed supply bottlenecks and crimp

capital flows for both—and other—countries.

More broadly, a partial decoupling of China from the West would reshape supply chains, which

carries significant costs and operational challenges.

Top Risks

While credit ratings reflect our base-case scenario, our regional and global Credit Conditions

Committees monitor top risks that could derail our baseline expectations, leading to further

credit deterioration. For 2024, these include the risks that:

• Tight and volatile financing conditions persist amid entrenched inflation, increasingly

pressuring debt-service capacity of more vulnerable borrowers;

• A deeper and longer-than-expected recession in the largest economies further damps global

growth;

• Persistent input-cost inflation and high energy prices, combined with weakening demand,

squeeze corporate profits and pressure governments’ fiscal balances;

• Stresses in global real estate markets result in materially higher credit losses and spillovers to

broader economies and markets; and

• Amplifying geopolitical tensions roil markets and weigh on business conditions.

Looking ahead at the structural risks that will shape the future of credit, we see greater pressure

on credit from the physical and transition risks associated with climate change, along with rising

systemic risks from cyberattacks.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 13

Global Credit Outlook 2024

Top Global Risks

An extended period of high real-interest-rate levels further strains the weakest borrowers

Risk level

Risk

trend

A prolonged period of historically elevated real interest rates could become more challenging as debt maturities increase in 2025, either locking out

the weakest borrowers or with most issuers facing higher debt-service costs. This could be exacerbated as revenues slow, raising the real impact of

higher borrowing costs. When faced with slower GDP growth, lenders typically become more selective or demand greater compensation for

increased risk. This could contribute to default rates reaching our pessimistic cases of 7% in the U.S. and 5.5% in Europe.

An economic hard landing leads to greater credit stress

Risk level

Risk trend

Most countries have entered a slower growth period. The U.S. economy has proven resilient, but signs of strain among consumers are growing. Most

of core Europe is already experiencing anemic growth, and in our base case for 2024 we expect most countries to slow further, including below-

trend growth in most emerging markets. Downside risks to these already slower growth projections are largely linked to any weakness in labor

markets, which in many countries are already tight. Consumer delinquencies are starting to rise and built-up savings from pandemic supports have

been deteriorating quickly, which will challenge economic resilience ahead. We currently project the U.S. has a historically high 35% likelihood of a

recession in the next 12 months, indicating increased downside vulnerability for the world's largest economy, which would have spillover effects

globally.

Stresses in global real estate markets result in materially higher credit losses and spillovers to broader economies and markets

Risk level

Risk trend

A combination of secular and cyclical factors--high interest rates, falling valuations and cash flows, hybrid work trends, increasingly stringent

environmental standards for buildings, and high leverage--are challenging established business models for commercial and residential real estate.

Beyond our base case assumptions, spillovers from these vulnerabilities could reverberate more broadly, whether through material losses for more

exposed banking systems (such as the U.S. and China), other non-bank financial sectors with real estate exposures, or through negative effects on

investor and consumer sentiment more generally.

China’s economic growth challenges cause ripple effects globally

Risk level

Risk trend

China’s economy could weaken on multiple fronts at once, with persistent weakness in the real estate sector, tepid household and business

confidence, high debt, and subdued exports already weighing on the country's growth momentum. Contagion risks within China from weaker

confidence could spill over from real estate and related sectors (such as local government financing vehicles) -- exacerbating credit stress for

banks. Lenders could restrict new debt given the corporate sector's already high leverage. Given China’s large proportion of global trade, its slump

could spread to multiple regions.

Structural risks

Geopolitical tensions threaten market and business confidence, trade, and a renewal of inflation

Risk level

Risk trend

The post-COVID era marks the return to geopolitical risks. The Israel-Hamas war adds another dimension to increasing geopolitical strife. The

potential for the war to escalate—and to affect the rest of the world through energy supply shocks, supply disruption, and risks to social

cohesion—is a key concern. Other tensions such as persistent U.S.-China frictions, the Russia-Ukraine conflict, and domestic issues in certain

emerging markets could curb business activity, trade, supply chains, and investment flows--as well as increase financial market volatility. 2024 will

also feature more than 70 elections in 50-plus countries whose outcomes could add complexity to already strained international and domestic

dynamics for many countries.

Moderate Elevated

High Very high

Improving Unchanged Worsening

Moderate Elevated

High Very high

Improving Unchanged Worsening

Moderate Elevated

High Very high

Improving Unchanged Worsening

Moderate Elevated

High Very high

Improving Unchanged Worsening

Moderate Elevated

High Very high

Improving Unchanged Worsening

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 14

Increased financial, business, and human implications from climate physical and transition risks

Risk level

Risk trend

Larger and more frequent natural disasters increase the physical risks public and private entities face and threaten to disrupt supply chains, such

as for agriculture and food. This may quickly become a headline risk in the near term as the El Niño phenomenon is expected to disrupt agricultural

commodities this year, particularly in emerging markets. At the same time, the global drive toward a "net-zero" economy heightens transition risks

(such as policy, legal, technology, market, and reputation risks) across many sectors and will likely require significant investments. Concerns about

energy supply and security are adding uncertainty to this transition.

Cyberattacks and the potential for rapid technological change threaten global business and government infrastructure

Risk level

Risk trend

Amid increasing technological dependency and global interconnectedness, cyberattacks pose a potential systemic threat and significant single-

entity event risk. Criminal and state-sponsored cyberattacks are likely to increase, and with hackers becoming more sophisticated, new targets and

methods are emerging. A key to resilience is a robust cybersecurity system, from internal governance to IT software, all requiring additional costs.

Entities lacking well-tested playbooks (such as active detection and swift remediation) are the most vulnerable. Meanwhile, increased digitization

and the introduction of AI by public and private organizations will foster broader operational disruptions, and potentially increase market volatility

for short periods or even pose greater economic adjustments.

Source: S&P Global Ratings.

Risk levels may be classified as moderate, elevated, high, or very high. They are evaluated by considering both the likelihood and systemic impact of

such an event occurring over the next one to two years. Typically, these risks are not factored into our base case rating assumptions unless the risk

level is very high.

Risk trend reflects our current view about whether the risk level could increase or decrease over the next 12 months.

Moderate Elevated

High Very high

Improving Unchanged Worsening

Moderate Elevated

High Very high

Improving Unchanged Worsening

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 15

Contacts

Paul F Gruenwald

New York

+1

-212-437-1710

paul.gruenwald@spglobal.com

Global Economic Outlook 2024

2024 Is All About The Landing

E

ditor’s note: This is an abridged report. For the full version, see: "Global Macro Update: 2024 Is All About The Landing,"

published Nov. 29, 2023.

Rate Hikes Have Been Synchronized, Macro Outcomes Have Not

Major central banks (excluding Japan) have raised policy rates by about 400 to 500 basis points

(bps) since the first half of 2022 to slow inflation, which has surged to a four-decade high. The

effort to curb inflation appears to be succeeding, but macro performance has varied widely. This

reflects differing speeds of monetary transmission, differing fiscal impulses, and differing

external conditions and dependencies.

Chart 1

Major central bank policy rates

End period (%)

Sources: Central bank websites.

-1

0

1

2

3

4

5

6

U.S. U.K. Canada Australia Eurozone Japan

Dec. 2022

Nov. 2023

Key Takeaways

• Following a synchronized rise in policy rates, growth is now unsynchronized across major

economies. The U.S. is outperforming whereas in Europe activity is flat. The common

macro thread comprises strong labor markets and spending on services, fiscal tailwinds,

and lingering core price pressures.

• Inflation has likely peaked as have policy rates, but central banks are on guard against

declaring victory too early. Our higher-for-longer view applies both to policy rates and

market interest rates, real and nominal. Caution among developed market central banks

is constraining potential rate cuts in emerging markets.

• We have moved our GDP growth forecasts marginally higher in some key emerging

markets but are broadly unchanged elsewhere. We have again pushed any necessary

slowdowns into the future.

• The next macro challenge is to "stick the landing." The risks to our soft-landing baseline

look balanced. Strong labor markets and fiscal tailwinds are driving the upside, whereas

uncertainties about the lagged transmission of cumulative rate hikes since early 2022 are

driving the downside.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 16

Our macro summary for the major regions and groups is as follows (details and links appear

below):

• The U.S. economy continues to outperform, posting nearly 5% annualized growth in the third

quarter, led by strong consumer spending and an inventory rebuild. Fourth quarter GDP is

tracking close to potential growth of 2%. (For further details, see "Economic Outlook U.S. Q1

2024: Cooling Off But Not Breaking," published on Nov. 27, 2023.)

• Activity in Europe has flatlined. Services-based economies (Spain) have done better than

manufacturing-based economies (Germany). Monetary transmission works faster than it does

in the U.S. (For further details, see "Economic Outlook Eurozone Q1 2024: Headed For A Soft

Landing," published on Nov. 27, 2023.)

• China’s growth has stabilized, reflecting targeted government stimulus. But household

confidence remains weak, and the property sector remains under stress. High inflation has not

been an issue. (For further details, see "Economic Outlook Asia-Pacific Q1 2024: Emerging

Markets Lead The Way," published Nov. 27, 2023.)

• Emerging markets have proven resilient overall, led by domestic-driven economies (India,

Indonesia), or those linked to the U.S. (Mexico). Policy rates cuts are in part currently

constrained by the U.S. Federal Reserve. (For further details, see "Economic Outlook Emerging

Markets Q1 2024: Challenging Global Conditions Will Constrain Growth," published Nov. 27,

2023.)

Strong labor markets are a bright spot almost everywhere, despite diverging growth outcomes.

Low unemployment rates stem from strong spending on services and labor hoarding. Higher

frequency indicators, including payroll additions, quits, and hours worked, do show signs of

slower labor demand. Ongoing robust fiscal spending helps in many economies as well.

Chart 2

Unemployment rates

July 1990 through present

Sources: FRED. S&P Global Ratings Economics.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 17

Both headline and core inflation continue to decline following their peaks of late 2022. Headline

inflation rose to higher rates than core and is now generally lower, reflecting the recent declines

in food and fuel prices. However, core inflation remains stubbornly high--near 5% in several major

advanced economies--and well above central bank targets, typically 2% over the medium term.

This stickiness reflects strong labor markets and spending on services and other non-tradable

goods. By extension, sticky inflation also implies that demand growth is too strong and that the

pace of activity needs to fall to bring inflation lower.

Chart 3

Inflation--selected economies

End of period (%)

PCE--Personal consumption expenditure. HICP--Harmonized index of consumer prices. Sources: Country websites.

Major central banks are signaling that they will need to keep rates near current levels for a

sufficiently long time, interpreted by markets as until the middle of 2024, because core inflation

remains high and sticky. This stems from strong labor markets, which are driving services

spending. Also, having been surprised by the jump in inflation in 2021 and responded too late,

central banks are wary of getting burned again and are therefore leaning higher. Markets have

bought the higher-for-longer view for the most part.

Latest Forecasts And Regional Narratives

Our updated GDP growth forecasts for the advanced economies are broadly unchanged for the

U.S. and eurozone as a whole (see chart 4). Our global growth forecast is 0.2% higher this year

and is unchanged over 2024-2026. The main revisions were in the big emerging markets: China

and India. We have nudged Spain, France, and the U.K. higher and Italy lower, with all of these

moves less than 30 bps, mainly due to carryovers from revisions to 2022 GDP. The emerging

markets had somewhat larger revisions for key countries.

0

1

2

3

4

5

6

U.S. PCE U.K. Canada Australia Eurozone HICP Japan

Headline

Core

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 18

Chart 4

GDP growth forecasts

Annual percentage change

World GDP is in purchasing power parity terms, based on sample of 33 countries we cover (excluding Russia).

*Fiscal year, beginning April 1 of the reference calendar year. Sources: S&P Global Market Intelligence. S&P Global Ratings.

Risks To Our Soft-Landing Baseline

We continue to see a material risk that macro developments will turn out better than

anticipated. Indeed, this has been the pattern for the past year, and many of the contributing

elements remain in place. Labor markets remain tight across a wide swathe of economies even

though headline growth numbers are diverging. The other factor is fiscal policy, which remains

expansionary for this part of the cycle. This is also occurring across a wide number of economies,

boosting output, labor demand, and wages more than would otherwise be the case.

An upside growth scenario also implies that interest rates will need to stay higher for longer.

This is relative to our already higher for longer baseline. Downside risks to our baseline scenario

relate mainly to uncertainties around the transmission of higher policy rates to financial

conditions and the real economy.

Given the steep increase in policy and market rates since early 2022, these resets will not be

small. To the extent that the reaction to higher rates is not linear, these large rate increases pose

greater downside risks. Not surprisingly, this downside is larger where the resets take longer and

the rate adjustment is higher.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 19

Non-macro risks are inherently more difficult to quantify but must be recognized. In particular,

geopolitical factors are at play. Spillovers of the ongoing conflicts between Russia and Ukraine

and Israel and Hamas have so far been lower than we expected. But we can't rule out escalations,

which could potentially move the macro needle. Tensions around the U.S.-China rivalry have

manifested so far in some modest realignment of trade and financial flows, but also remain

largely bounded.

Sticking The Landing

The macro focus has shifted from watching inflation to watching the landing. Since the

transmission of monetary policy works with a lag, the next few quarters will be critical in

determining whether we soft land or not. But what does this elusive soft landing look like?

Growth needs to slow below potential in order for excess demand pressures to ease and

inflation to fall back to target. In a soft-landing scenario the necessary adjustment takes place

gradually. Critically, there is little or no undershoot of the level of GDP nor the rate of inflation,

and no undershooting of policy rates. The glide path allows for a slower and more calibrated

adjustment.

The soft-landing story mostly hinges on the labor market. If workers keep their jobs, or expect

to keep their jobs, then spending is likely to be maintained. No paradox or thrift here, or a sharp

drop in spending.

Real rates remain positive throughout. This can be seen as the cyclical manifestation of higher

for longer. Policy rates will fall, but only after inflation is on a clear downward path. Real rates are

likely to remain elevated, and even rise in the coming quarters. When landing is achieved, inflation

will be at the target of 2% and the policy rate will exceed inflation by r*, the real rate of interest.

We think r* has risen globally and could be as high as 1%.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 20

Questions

That

Matter

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 21

Primary Credit Analysts

Gareth Williams

London

+44

-20-7176-7226

gareth.williams@spglobal.com

Gregg Lemos

-Stein

New York

+1

-212-438-1809

gregg.lemos

-stein@spglobal.com

Corporates | Could interest rate and recession risks

derail corporate credit?

How this will shape 2024

Weaker economic growth and a rising interest burden will test corporate issuers globally. The

corporate sector proved surprisingly resilient in 2023, with sustained consumer spending, notably

in the U.S., and supportive tailwinds from capital investment. Still, difficulties are apparent with

default rates edging higher, net downgrades, and contracting annual revenues and EBITDA. The

challenges will grow in 2024, as higher interest costs continue to filter through to effective

interest rates, refinancing pressures start to build, and the economic backdrop remains difficult.

Corporate decision-making will likely amplify broader economic trends. Continued resilience

and a gradual rebound in profits would likely contain credit pressures to the most vulnerable.

This could start to unlock cash balances for M&A and investment. However, if the global economy

weakens more than our forecasts assume, companies will likely act quickly to protect cash flows

through layoffs and investment cuts, traditional harbingers of recession.

Chart 1

The long decline in financing costs is likely over….

Cash interest paid/total debt and three

-month U.S.

interbank rates plus 350

basis points

Median,

LTM, rated U.S. nonfinancial corporates

Chart 2

…and interest cover risks are building for weaker credits

EBIT interest coverage

Median,

LTM, 'B' rated U.S. nonfinancial corporates

Source: S&P Global Market Intelligence Credit

Pro®, Compustat, S&P Capital IQ, NBER, S&P Global Ratings. Shows data for the contemporaneous rated universe

through time. Financial data from Compustat from 1982 to 1994, and S&P Capital IQ thereafter. LTM data to Q3 2023, with last

two markers indicating S&P Global

Ratings estimate for end

-2023 and end-2024.

3

4

5

6

7

8

9

10

11

12

13

86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

(%)

U.S. recession

BBB

BB

B

U.S. 3-month interbank rate plus 350 basis points

-1.0x

-0.5x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

84 88 92 96 00 04 08 12 16 20 24

U.S. recession

B+

B

B-

Interest cost pressures and a difficult economic backdrop mean credit pressures

will remain acute for weaker borrowers.

Credit

headwinds

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 22

What we think and why

Interest rate and refinancing pressures will continue to bear down on corporates. Third-

quarter results to date show cash interest payments still surging, up 21% at an annual rate and

25% for speculative-grade entities overall. Refinancing conditions remain difficult, particularly for

weaker entities, with lending standards tightening and debt maturity pressures building next

year.

We think structural changes are at play that will put pressure on unsustainable capital

structures. The era of ever cheaper borrowing costs is over (see chart 1), as is the steady uptrend

in profitability wrought by globalization, muted labor cost inflation, and reduced energy intensity.

Trade and political tensions are unlikely to fade in the near term, although artificial intelligence

(AI) may be a productivity wildcard. Sustained higher financing costs will likely mean that credit

metrics such as interest cover, which had ceased to be of much relevance, will again be of value.

More broadly, the end of financial repression (defined as interest rates being held below the

inflation rate) may bring risks from unsustainable capital structures to a head.

Credit pressures are likely to be confined to the weakest credits. Despite these pressures, we

believe credit quality will remain robust in investment grade and the stronger parts of speculative

grade, absent a severe economic contraction, and allow a modest turnaround in the earnings

cycle (see chart 3). However, the weaker end of the credit spectrum is vulnerable. We estimate

median EBIT interest cover for U.S. 'B' rated nonfinancial corporates will drop below one by the

end of this year to 0.6x, its lowest level since Q3 2004, and remain below one in 2024 (see chart

2). Among U.S. 'B' category ratings, 11% have had EBIT interest coverage ratios of less than one

for three years or more (see chart 3), showing further evidence of fragility. For these reasons, we

expect default rates will continue to rise even if the broader story is one of recovery.

Chart 3

Avoiding rece

ssion should help global earnings rebound…

Data for global rated nonfinancial corporates.

Sources: S&P Capital IQ, S&P

Global Ratings.

Chart 4

…but weaker credits are struggling with interest costs

Source

s: S&P Global Market Intelligence CreditPro®, Compustat, S&P

Capital IQ, NBER, Refinitiv, S&P Global Ratings.

What could go wrong

Sustained inflationary pressures or a sharp economic contraction are the primary risks.

Prolonged or reignited inflation pressures would exacerbate the already significant impact of

higher interest rate costs, and likely be accompanied by intensified labor cost inflation and

margin pressure. A sharp economic contraction could entail a dangerous combination of falling

EBITDA and still elevated financing costs, with market volatility and higher risk premia likely to

overwhelm any benefit from the lower policy rates that would likely follow.

-15

-10

-5

+0

+5

+10

+15

+20

+25

+30

07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Sales growth (YOY%)

EBITDA growth (YOY%)

Estimate

0

5

10

15

20

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21 23

(%)

U.S. recession

Share Of 'B' Category Ratings With EBIT Interest Cover

<1 For >= 3 Years

Read more

Corporate Results Roundup Q3

2023: Deterioration continues and

revenues disappoint

, Nov. 16, 2023

Interest

-

cover risks are growing for

vulnerable corporate credit

, Oct.

26, 2023

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 23

Primary Credit Analysts

Ja

mes Manzi

Washington D.C.

+1

-202-383-2028

Ana Lai

New

York

+1

-212-438-6895

ana.lai@spglobal.com

Franck Delage

Paris

+33

-14-420-6778

fra

nck.delage@spglobal.com

Edward Chan

Hong Kong

+852

-2533-3539

Real Estate | Is the worst over for the global office

sector and China’s residential market?

How this will shape 2024

As the real estate sector confronts credit headwinds globally, persistent and prevailing risks

differ across type of real estate, region, country. This is true even for office buildings that are

right next to each other based on asset quality, occupancy, maturity profile, and more. And while

high interest rates remain the key risk for real estate assets globally, remote working is hurting

U.S. office landlords more than in Europe and China—as demonstrated by average vacancy rates

(see chart 1). Homebuilders are also facing diverging paths, largely based on geography; the U.S.

housing market remains resilient due to limited supply of existing housing while Chinese property

developers are facing a prolonged slump in demand. We expect real estate issuers to face a

challenging operating environment in 2024 given our expectations for interest rates to stay higher

for longer while revenue is pressured from weaker economic growth. We expect rates to stay

elevated in the next year, with gradual cuts beginning in the second half of 2024.

Chart 1

Global office vacancy snapshot (%)

Source

s: JLL, Property Council of Australia, Colliers International, Miki Shoji,

S&P Global

Ratings.

Chart 2

U. S.

and EMEA office CPPI, 2007-present (index)

Source

: Green Street.

Stress on the office segment remains high. Across commercial real estate, higher interest rates

have reduced debt-service coverage and raised refinancing risk. Declining demand for office

space—particularly in major cities across the U.S., U.K., continental Europe, and Australia—is

weighing on asset valuations (see chart 2). Demand increasingly concentrates on the most

centrally located and energy efficient assets. Offices in particular are also generating lower levels

of cash flow given increasing financing costs and credit headwinds. Rising operating expenses as

well as leasing incentives (e.g., rent concessions) have made it that much harder to meet interest

obligations, resulting in increased delinquency rates. Still, the picture is far less negative for cash

flows/revenues from hotels, industrial, and multifamily properties, which have held up well to

0

5

10

15

20

25

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Q2

2023

Europe U.S. Australia

Japan Hong Kong

0

20

40

60

80

100

120

140

160

Q1 2007

Q1 2008

Q1 2009

Q1 2010

Q1 2011

Q1 2012

Q1 2013

Q1 2014

Q1 2015

Q1 2016

Q1 2017

Q1 2018

Q1 2019

Q1 2020

Q1 2021

Q1 2022

Q1 2023

U. S. office EMEA office

Higher-for-longer interest rates remain the key risk for real estate assets globally.

The distress will likely be drawn out on the commercial side, and especially in the

U.S. where office vacancies are relatively higher. In China, as the property

downturn continues, we expect property sales will track an extended L-shaped

recovery in 2024.

Credit

headwinds

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 24

date. The stress in office will be drawn out for years, as office leases typically carry longer terms

– ten years or more.

Higher mortgage payments are hurting affordability. For residential real estate, the rapid rise of

mortgage rates is also dampening housing demand globally as buyers are adjusting to the highest

rates in almost two decades. We expect the U.S. and European housing markets to face pressure,

given worsening housing affordability. As steep increases in mortgage payments hurt home

purchasability, rental housing remains a cheaper option in many markets. We expect rental

housing demand in 2024 to remain healthy, albeit at slower pace. In Europe, residential rents will

remain supported by lagging indexation, falling supply, and higher demand from immigration.

Property sales in China will track an L-shaped recovery in 2024, after a decline of more than

one-third since the peak in 2021. As the property downturn enters into its third year, the

government’s continuous policy relaxations (including lowering mortgage rates) aimed at

stabilizing the sector will benefit the upper-tier markets, particularly the first-tier cities. Lower-

tier cities are contending with excess supply and depleted confidence. All developers will have to

manage slowing sales; in our view, their leverage will remain high for the next two years. In Hong

Kong, we expect residential property prices to fall in 2024, as leading developers will likely lower

prices to entice demand, as well as sacrifice margins to meet their contracted sales targets and

to gain market share.

What we think and why

Refinancing risk is growing. Higher-for-longer interest rates will continue to pressure asset

values and erode credit metrics in 2024, increasing refinancing risk across all property types.

Refinancing options remain more limited, given a pullback from bank lending while debt issuance

remain subdued due to steeper cost of borrowing. In the meantime, real estate transaction

volume remains low and will not likely recover until rates starts to decline (or at least stabilize),

perhaps toward the end of 2024.

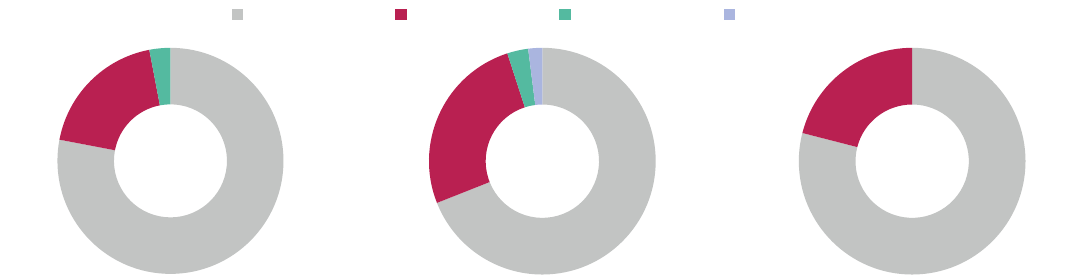

Amidst challenging financing conditions, we expect an increase in downgrades and many loans

to be restructured or default if maturities are unable to be extended. We maintain a negative

rating bias for the REIT sector globally—with about 20% of U.S. ratings on negative outlook,

compared to 26% in EMEA and Asia-Pacific’s 21% negative rating bias. In the U.S., the office

REITs space saw four fallen angels in 2023, and almost 40% of office REITs were speculative

grade as of November 2023. Growing refinancing risk has led to a growing number of 'CCC' ratings

in the U.S.

Chart 3

Global REITs rating outlook bias

Source: S&P Global Ratings.

78%

19%

3%

North

America

69%

26%

3%

2%

EMEA

79%

21%

Asia-Pacific

Stable Negative Positive Watch Neg

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 25

“Higher-for-longer

interest rates

increase refinancing

risk across all

property types

.”

The effects on ratings are already evident in the U.S. CMBS market (with some 254 class ratings

lowered in the 12 months ended Oct. 31, 2023). Negative rating bias has also increased

significantly for rated REITs globally, and we have downgraded a growing number of issuers with

significant exposure to office assets. For banks, there have been increases in criticized

assets/loans (that is, showing a higher probability of default or deteriorating collateral values).

Across CRE loans and reserves, the impact seems muted for the larger entities that we rate. For

newer class-A offices with strong tenant rosters, or other types of CRE where the distress largely

stems from higher rates, lenders may extend loan maturities in the hopes that a decline in

interest rates and stabilization of property valuations will soon materialize. For example, we're

watching multifamily closely in the U.S. as some properties were underwritten at what might be

peak rents, thus having less margin for any corrections amid significantly higher rates.

Limited housing supply mitigates soft demand in housing. Despite sharp increases in home

mortgage payments, we expect demand for housing to remain resilient due to limited supply of

homes and relatively benign job markets in the U.S. U.S. homebuilders have gained share as

existing homeowners are reluctant to sell their homes at low mortgage rates, while European

homebuilders continue to face strong margin pressures due to significantly lower demand for

newly built residentials and elevated costs of constructions. Conditions for Chinese developers

remain challenging. We believe the spillover impact from China’s property market into other

property markets will likely be limited given the risks to Chinese banks are manageable. These

institutions have sufficient capital buffer to absorb the potential losses from property-sector

write-downs, while government policies are helping stabilize residential sales, particularly in

higher-tier markets.

What could go wrong

Higher for even longer could increase downside risk. The credit outlook for both global

commercial and residential real estate depends on the path of benchmark interest rates, likely

more so for commercial. While our macroeconomic base case does not call for a recession in

2024, weaker growth with higher unemployment and consumer spending could further pressure

real estate demand, particularly in a prolonged high-rate environment.

Loan distress could increase. Amid higher rates, declining asset values, and lower cash flows for

certain property types, elevated CRE-related loan losses may rise for debtholders including

banks, NBFIs, insurers, REITs, and CMBS. Reduced construction/new projects may also

contribute to slower macroeconomic growth, amid relatively lower demand for space.

A weaker macro landscape can slow demand further. If interest rates remain elevated for much

longer, residential investments could deteriorate significantly. If interest rates remain high or

move even higher, the already stressed market for refinancing would certainly worsen—and the

prospect of “higher-for-longer” loan rates could thwart any plans borrowers may have to simply

wait conditions out by extending their loans. While we expect benchmark rates to stay elevated in

the next year, our U.S. base case calls for gradual (policy) rate cuts beginning in the second half

of 2024, lowering mortgage rates from peak levels and supporting a recovery in housing demand

in 2024 and beyond. Persistently high mortgage rates could erode demand such that housing

could see more material pricing decline.

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 26

Primary Credit Analysts

David C. Tesher

New York

+1-212-438-2618

david.tesher@spglobal.com

Paul Watters, CFA

London

+44-20-7176-3542

Evan Gunter

Montgomery

+1-212-438-6412

Luca Rossi

Paris

+33-6-2518-9258

luca.rossi@spglobal.com

"Credit is credit, and

these borrowers face

the same

fundamental risks as

rated issuers."

Private Markets | How long can the golden age of

private credit last?

How this will shape 2024

We expect opportunities for private credit and funds to remain robust in 2024, after booming

in 2023. After years of strong fundraising, private credit funds have amassed more than $400

billion in dry powder globally (as of September), leaving them with cash to deploy. While limited

partners (LPs) appear to be responding to restrictive, higher-for-longer interest rates by slowing

contributions to alternative assets--especially private equity funds--private credit allocations

have held up better. Whether 2024 will be another golden year for private debt investors will

depend on their risk appetites and strategic focus, as well as the economic backdrop.

The pool of private credit continues to expand. In the U.S., private credit is growing its capacity

through nontraded business development companies, interval funds, and middle-market

collateralized loan obligations (CLOs). Direct lenders have tended to target traditional middle-

market borrowers with $25 million-$100 million (or equivalent in euros) of EBITDA, but the growing

trend for club deals has extended private credit’s reach to larger and more diverse borrowers.

Additionally, distressed and special situations funds--which represent as much as one-third of

available capital--are waiting in the wings for rescue financing opportunities.

Challenges for borrowers may be opportunities for lenders. Given challenging public markets,

borrowers are looking for other sources of funding to meet upcoming maturities. Broadly

syndicated loan (BSL) issuance in the U.S. and Europe is down nearly 30%, to its lowest level

since 2010 (at $318 billion). Meanwhile, ‘CCC’ bond issuance has fallen to its lowest level since

2008 (around $2 billion). Private credit is looking to take up some of the slack as upcoming

maturities of nonfinancial corporate debt rated ‘B-' and lower (in the U.S. and Europe) doubles to

$169 billion in 2025, from $83 billion in 2024.

What we think and why

Credit is credit, and these borrowers face the same fundamental risks as rated issuers.

Financial risks weigh more on the credit quality of borrowers with weak business risk profiles or

high leverage. In particular, companies issuing floating-rate debt, such as from private lenders,

will be vulnerable to the higher cost of funding amid higher-for-longer interest rates.

We see this in rising default rates. We expect the trailing-12-month speculative-grade corporate

default rate to reach 5% in the U.S. by September 2024 (up from 4.1% in September 2023) and

3.75% in Europe (up from 3.1%) as companies grapple with higher interest rates.

Cash flow metrics are regaining their importance as a key driver of credit quality, alongside

measures of leverage. We see many borrowers laser focused on maximizing cash flow through

various measures, including: cutting expenses, protecting margins, trimming inventories and

working capital, selling assets, reducing dividends and share buybacks, or raising equity. Cash-

constrained borrowers are also using payment-in-kind instruments on their balance sheets and

choosing to build cash buffers rather than repay debt.

Whether private or public, credit is credit. And with interest rates likely to remain

higher for longer, weaker borrowers and their lenders are paying far more attention

to cash flow metrics and borrowers' ability to service debt.

Read more

Testing Private Debt's Resilience

Through The Credit Estimate Lens

,

Nov. 2, 2023

Middle

-Market CLO And Private

Credit Quarterly: Strong CLO

Growth, But Weakening Underlying

Credit

, Oct. 20, 2023

Capital flows

Global Credit Outlook 2024: New Risks, New Playbook

spglobal.com/ratings/outlook2024

Dec. 4, 2023 27

“Even a moderate

stress could

diminish

the credit quality of

private credit

borrowers

.”

For businesses that require significant investment, the need to prioritize liquidity could come at

the expense of longer-term growth. In addition, some financial sponsors--facing the reality of

higher funding costs, lower valuations, longer hold times, and fewer exit routes for portfolio

companies--are resorting to new arrangements to raise debt, often hoping to bridge to a more

favorable business climate.

Tighter financing conditions will test financial vulnerabilities. In our base case, we expect

policy interest rates to only start easing in the second half of 2024, meaning financing conditions

will remain restrictive for a while. This is likely to pressure the credit quality of the more than

2,000 U.S. middle-market borrowers for which we have credit estimates. In the year to August

2023, a significant minority were already struggling to generate positive free operating cash flow

(FOCF), and 78% had a low 'b-' score, with 13% in the 'ccc' category. In comparison, about 30% of

global speculative-grade issuers are rated 'B-' or lower.

What could go wrong

Even a moderate stress could diminish the credit quality of private credit borrowers. Our

analysis highlights that many companies with 'b-' credit estimates could be at risk of a

downgrade from higher interest rates and lower earnings. We assume a moderate stress scenario

of SOFR rising 1 percentage point over our current base case of about 5%, together with a 20%

fall in EBITDA. In such a case, only about 35% of this set of middle-market borrowers would likely

generate positive FOCF, and about 28% of those with 'b-' credit estimate scores would be

vulnerable to a downgrade.

Interestingly, 55% of these credit estimates are for companies in the business and consumer

services, health care services, and technology software and services sectors. Technology

appears most vulnerable in our stress scenarios, with materially weaker interest coverage ratio

and covenant headroom.

Information asymmetry is more problematic for credit investors than equity providers.

Lenders are always more sensitive to downside risks than equity investors. One such risk is the

considerable information asymmetry in the private credit market, which is exacerbated by the

influx of less-sophisticated retail investors into the asset class.

While tighter documentation and close working relationships help to facilitate an open flow of

information between borrowers, lenders, and sponsors, LPs and institutional investors have a

more indirect flow of information. Disclosures about borrowers' operational and financial

performance, credit quality, and asset valuations may vary between funds and intermediaries.

Illiquidity could reveal contagion risk. Without a sizable secondary market, private credit assets

are largely illiquid buy-and-hold investments held in vehicles with capital that is typically locked

up for at least five years. We think the scale of private debt is unlikely on its own to threaten

financial stability in the U.S. or Europe, as it accounts for only about 4% and 1% of total

nonfinancial corporate debt in each region, respectively.

However, a material shock in this opaque, illiquid, and unregulated market could expose

vulnerabilities elsewhere in the financial system. For instance, there could be some contagion

risk to banks, insurance companies, and pension funds. Banks often provide private credit