Defense Information Systems Agency

Annual Financial Report - GF

Fiscal Year 2018

Table of Contents

Management Discussion and Analysis ........................................................................................ 1

Principal Statements ................................................................................................................... 32

Notes to the Principal Statements .............................................................................................. 37

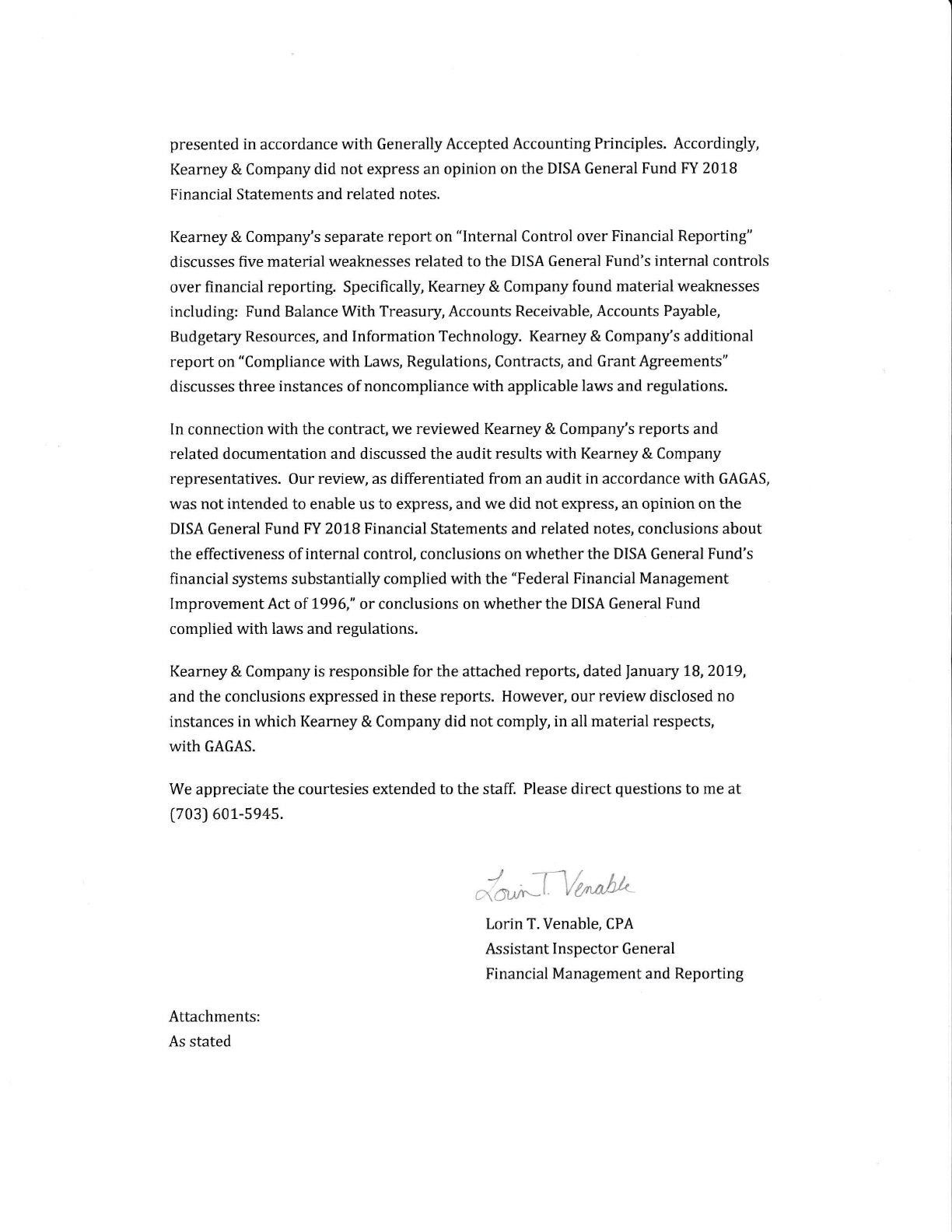

DoD OIG Transmittal Letter ..................................................................................................... 65

Independent Auditors’ Report ................................................................................................... 67

Attachment 1 DISA Management’s Comments on the Auditor’s Report ............................. 89

i

Fiscal Year 2016 Defense Information Systems Agency General Fund Agency Financial Report

Management’s Discussion and Analysis (v4)

The Defense Information Systems Agency (DISA) is pleased to present a Management

Discussion and Analysis (MD&A) to accompany the financial statements and footnotes for its

fiscal year (FY) 2018 Consolidated Financial Statements. The key sections within this MD&A

include the following:

1. Mission and Organizational Structure

2. Performance Goals, Objectives & Results

3. Analysis of Entity’s Financial Statements

4. Management Systems, Controls & Compliance with Laws and Regulations

5. Limitations of the Financial Statements

1. Mission and Organizational Structure

History & Enabling Legislation: DISA is an operationally focused Department of Defense

(DoD) combat support agency that delivers information technology to enhance the capabilities of

the nation's warfighters and all who support them in defense of the nation. DISA’s roots go back

to 1959 when the Joint Chiefs of Staff (JCS) requested the Secretary of Defense (SECDEF)

approve a concept for a joint military communications network to be formed by consolidation of

the communications facilities of the Military Departments. This would ultimately lead to the

formation of the Defense Communications Agency (DCA), established on 12 May 1960, with

the primary mission of operational control and management of the Defense Communications

System (DCS). On 25 June 1991, DCA underwent a major reorganization and was renamed the

Defense Information Systems Agency to reflect its expanded role in implementing the DoD's

Corporate Information Management (CIM) initiative, and to clearly identify DISA as a combat

support agency. DISA established the Center for Information Management to provide technical

and program execution assistance to the Assistant Secretary of Defense (C3I) and technical

products and services to DoD and military components. DISA's role in DoD information

management continued to expand with implementation, in September 1992, of several Defense

Management Report Decisions (DMRD), most notably DMRD 918. DMRD 918 created the

Defense Information Infrastructure (DII), and directed DISA to manage and consolidate the

Services' and DoD's information processing centers into 15 megacenters. In FY 2018, the

organization that came to be known as the Joint Service Provider (JSP) declared full operational

capability and moved into its new place in the Defense Department’s organizational chart as a

subcomponent of DISA. It marked a major expansion of mission and budget authority for DISA,

which now controls the funding and personnel that provide most IT services for the Pentagon

and other DoD headquarters functions in the National Capital Region. DISA continues to offer

DoD information systems support, taking data services to the forward deployed warfighter.

The DISA Vision: To be the trusted provider to connect and protect the warfighter in

cyberspace.

The DISA Mission: To conduct DODIN operations for the joint warfighter to enable lethality

across all warfighting domains in defense of our nation.

1

Organization: To fulfill its mission and meet strategic plan objectives, DISA operates under the

direction of the DoD Chief Information Officer (CIO) who reports directly to the Secretary of

Defense.

The Agency is budgeted to support the IT needs and requirements of the entire Defense

Department, including the offices of the Secretary of Defense and of the Chairman and Vice

Chairman of the Joint Chief of Staff, the Joint Staff, military services, combatant commands, and

Defense agencies. DISA also provides support to the White House and many federal agencies

through a number of capabilities and initiatives.

During FY 2015, DISA embarked on the most extensive reorganization in over ten years. The

reorganization presented many challenges Agency-wide. In FY 2018, the Agency further

enhanced the outcome of the initial reorganization, and as a result, optimized the organizational

structure in order to more effectively execute strategy, optimize force posture into an agile cyber

force, improve accountability, reduce duplication, and improve cost management.

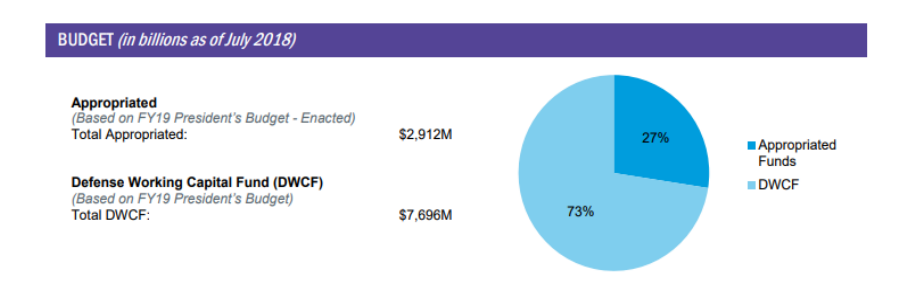

DISA's Appropriated Budget

Through its appropriated budget, DISA is funded by Congress through the National Defense

Authorization Act, the U.S. federal law specifying the budget and expenditures for DoD, and

defense appropriations bills authorizing DoD to spend money. This budget enables the Agency

to implement the White House's national security strategy, the secretary's planning and

programming guidance, and the initiatives of the DoD CIO.

DISA aligns its program resource structure across six mission areas, which reflect DoD's goals

and allows DISA to execute its core missions and functions:

1. "Transition to the Net-Centric Environment" funds capabilities and services that

transform the way that DoD shares information by making data continuously available in

a trusted environment. This mission area includes enterprise services, engineering

services, and technical strategies developed by DISA's chief technology officer (CTO).

2. "Eliminate Bandwidth Constraints" focuses on capabilities and services that build and

sustain the Global Information Grid (GIG) transport infrastructure, while eliminating

bandwidth constraints and rapidly surging to meet demands. Capabilities funded in this

category include the Pathways Program, DoD Teleport Program, Defense Spectrum

Organization (DSO) activities, and Defense Information System Network (DISN)

enterprise activities, such as non-recurring costs for commercial circuits, commercial

satellites, and special communications requirements.

3. "GIG Network Operations and Defense" funds the operation, protection, defense, and

sustainment of the enterprise infrastructure and information-sharing services, as well as

enabling command and control. This mission area includes funding for network

operations (NetOps); the information assurance/public key infrastructure (IA/PKI)

program; cybersecurity initiatives; and budgets for DISA's field offices, which support

2

the combatant commands, and for the Joint Staff Support Center (JSSC), which supports

the Chairman, Vice Chairman, and Joint Chiefs of Staff in the Pentagon.

4. "Exploit the GIG for Improved Decision Making" focuses on transitioning to DoD

enterprise-wide capabilities for communities of interest, such as command and control,

and combat support that exploit the GIG for improved decision-making. This mission

area funds the Global Command and Control System – Joint (GCCS-J) program, Global

Combat Support System – Joint (GCSS-J) program, and senior leader and coalition

information-sharing activities.

5. "Deliver Capabilities Effectively/Efficiently" finances the means by which the Agency

effectively, efficiently, and economically delivers capabilities based on established

requirements. This area funds the command staff and the personnel costs for DISA's

shared service units.

6. "Special Mission Areas" enables the Agency to execute special missions to provide the

communications support required by the president as Commander-in-Chief, including

day-to-day management, fielding, operation, and maintenance of communications and

information technology. The White House Communications Agency (WHCA) and the

Communications Management Control Activity (CMCA) in the Network Services

Directorate are budgeted out of this mission area.

DISA's Defense Working Capital Fund (DWCF)

DISA also operates a DWCF budget. Unlike the appropriated budget, which is provided through

direct congressional appropriations, the working capital fund relies on revenue earned from

providing IT and telecommunications services and capabilities to finance specific operations.

Mission partners order capabilities or services from DISA and make payment to the working

capital fund when the capabilities or services are received.

A DWCF business unit is not profit-oriented and, therefore, only tries to break even, charging

prices set using the full-cost-recovery principle, which accounts for all costs — both direct and

indirect (or "overhead") costs. It is intended to generate adequate revenue to cover the full cost

of its operations and to finance the fund's continuing operations without fiscal year limitation.

DISA operates the information services activity within the DWCF. This activity consists of two

main components. The first component includes two lines of service, telecommunications

services and enterprise acquisition services. The second component includes computing

services. The major element of the telecommunication services component is the DISN, which

provides interoperable telecommunications connectivity and accompanying services that allow

the Department to plan and operate both day-to-day business and operational missions through

the dynamic routing of voice, data, text, still and full-motion imagery, and bandwidth services.

Some DISN services are provided to mission partners in predefined packages and sold on a

subscription basis via the DISN subscription service, while others are made available on a cost-

reimbursable basis.

3

The line of service for enterprise acquisition services enables the Department to procure best

value, commercially competitive IT services and capabilities through DISA's Defense IT

Contracting Organization (DITCO). DITCO provides complete contracting support and services.

The computing services component of DISA's DWCF activities comprises Computing

Ecosystem, which provide mainframe and server-processing operations, data storage, production

support, technical services, and end-user assistance for command and control, combat support,

and enterprise applications across DoD. These facilities and functions provide a robust

enterprise computing environment to more than four million users through 30 mainframes, more

than 7,000 servers, 8,000 terabytes of data, and approximately 450,000 square feet of raised

floor.

The organizational structure for DISA as of 30 September 2018 is depicted below with a detailed

description of major offices outlined following the chart:

Defense Information Systems Agency

Figure 1 – Snapshot of DISA organization chart to include organizations directly or indirectly supporting DWCF missions

4

Command Staff – The DISA Director, with the assistance of a Vice Director, an

Executive Deputy Director, their support staff, Fifth Estate Center (Special Missions),

Special Advisors, a Resource Management Center, a Development and Business Center,

and a Center for Operations that directly support DISA’s critical mission, and several

other direct reports, leads a global organization of military and civilian personnel.

Fifth Estate Center – Comprised of Special Program Offices, Special Mission

Organizations, Units and Offices that support a wide range of objectives within

Department of Defense including Information Assurance, IT acquisition management,

White House Communication Support, Joint Information Environment (JIE) Support, and

other critical services for the Department. These programs and offices are primarily

funded through Congressional appropriations at this time.

Special Advisors - These advisors ensure that DISA’s decision makers have accurate,

timely, reliable, and useful information needed to make sound decisions, serve as the

principle advisor to the DISA Director for their areas of expertise, and represents and

defends the Agency’s position on all matters within their areas of expertise.

Development and Business Center – The Development and Business Center (DBC)

provides the engineering and solution analysis, infrastructure development, testing and

evaluation, assured communications of optimized cyber solutions for the rapid design,

development, integration and transition of Business, Enterprise, and Command and

Control systems, services and capabilities for our Agency, the DoD, other U.S.

Government agencies, and our allies across the full spectrum of military operations.

Center for Operations – The Center for Operations (OC) coordinates and synchronizes

DISA’s Operate and Assure Line of Operation in support of the full spectrum of military

requirements and operations, and supports United States Cyber Command in its mission

to provide secure, interoperable and reliable operation of the DoD net-centric Enterprise

Infrastructure. The Center for Operations also provides available, reliable, and secure

capabilities in support of the DoDIN such as enterprise services (voice, video, and

collaboration), migration to cloud based services, application migration to core data

centers, cyber services, and virtualization, standardization, and automations services in

support of the DoDIN.

Resource Management Center/Comptroller – The Resource Management Center

(RMC) serves as the principal financial advisor to the Agency’s Director; develops

financial strategies; develops and controls the formulating budget submissions process;

ensures financial controls; and conducts program and organizational assessments. It also

represents and defends the Agency’s position on all financial matters and provides

financial management guidance and oversight for the efficient and effective use of

resources. The RMC establishes financial management policies for DISA including its

component parts and ensures that decision makers have accurate, timely, reliable, and

useful financial information needed to make sound decisions.

5

Resources: DISA is a combat support agency of the DoD with a 10.6 billion-dollar annual

budget.

DISA is a global organization of approximately 6,000 civilian employees; approximately 1,300

active duty military personnel from the Army, Air Force, Navy, and Marine Corps, and

approximately 10,000 defense contractors. With a presence in 22 states (and the District of

Columbia) and seven countries and Guam (US territory), the Agency’s mission is to conduct

Department of Defense Information Network (DODIN) operations for the joint warfighter to

enable lethality across all warfighting domains in defense of our Nation.

Global Presence: DISA’s headquarters is at Fort Meade, MD with 55% of its people based at

Fort Meade and the national capital region (NCR), and 45% based in field locations. In addition,

the following organizations are a part of DISA: White House Communications Agency, White

House Situation Support Staff, Joint Information Environment (JIE) Technical Synchronization

Office, Defense Spectrum Organization, Defense Information Technology Contracting

Organization, Joint Interoperability Test Command, and the Joint Force Headquarters DoDIN.

DISA provides a core enterprise infrastructure of networks, Computing Ecosystem centers, and

enterprise services (internet-like information services) that connect 4,300 locations reaching 90

nations supporting DoD and national interests. The following map portrays the global presence

of DISA operations.

6

2. Performance Goals, Objectives & Results

DISA is charged with the responsibility for planning, engineering, acquiring, testing, fielding,

and supporting global net-centric information and communications solutions to serve the needs

of the President, the Vice President, the Secretary of Defense, and the DoD components under all

conditions of peace and war. The challenges faced by the Department impact DISA directly in

achieving success with respect to these responsibilities. DISA provides, operates, and assures

command and control, information-sharing capabilities, and a globally accessible enterprise

information infrastructure in direct support to joint warfighters, national-level leaders, and other

mission and coalition partners across the full spectrum of operations. DISA’s number one

priority is enabling information superiority for the warfighter and those who support them.

Warfighters on all fronts require DISA's continued support because immediate connection,

sharing, and assured access to information capabilities are essential to our mission partners'

operational success.

The JIE is designed to create an enterprise information environment that optimizes use of the

DoD IT assets, converging communications, computing, and enterprise services into a single

joint platform that can be leveraged for all Department missions. These efforts improve mission

effectiveness, reduce total cost of ownership, reduce the attack surface of our networks, and

enable DISA’s mission partners to more efficiently access the information resources of the

enterprise to perform their missions from any authorized IT device anywhere in the world. DISA

continues its efforts towards realization of an integrated Department-wide implementation of the

JIE through development, integration, and synchronization of JIE technical plans, programs, and

capabilities.

DISA is uniquely positioned to provide the kind of streamlined, rationalized enterprise solutions

the Department is looking for to effect IT transformation. The DISA owns/operates enterprise

and cloud-capable DISA Data Centers, the world-wide Defense Information Systems Network

7

(DISN), and the Defense IT Contracting Organization (DITCO). DISA Data Centers routinely

see workload increases – this trend will increase as major new initiatives begin to fully impact

the Department. As part of the Department’s transition to the Joint Information Environment

(JIE), DISA Data Centers have been identified as Continental United States (CONUS) Core Data

Centers (CDCs), and Defense Enterprise Email (DEE) has been identified as a DoD Enterprise

Service.

DISA also anticipates continuation of partnerships with other federal agencies. The

DoD/VA Integrated Electronic Health Record (iEHR) agreement to host all medical records in

the DISA Data Centers and the requirement for DoD to provide Public Key Infrastructure (PKI)

services to other federal agencies on a reimbursable basis are examples. We continue to move

forward on several new initiatives, including: accelerated implementation of multiprotocol label

switching (MPLS) technology; deploying and sustaining Joint Regional Security Stacks (JRSS)

to fundamentally change the way the DoD secures and protects its information networks;

operating a Joint Enterprise License Agreement (JELA) line of business with a low fee of 0.25

percent, and a new management concept in Computing Services that aligns like-functions across

a single computing enterprise to prioritize excellence in service delivery, process efficiency, and

standardization.

DISA Strategic Goals as outlined in the 2015-2020 Strategic Plan include:

Provide Global Infrastructure – DISA will develop, test, deploy, sustain, and maintain

a global elastic infrastructure, spectrum, computing, and storage capabilities that will

support full spectrum collaboration. The foundational elements of those services will be

comprised of reusable components. All elements will be normalized, converged, and

available at reduced cost, increased usability, and maximize portability to mobile

platforms. DISA will expand delivery of enterprise services to the Services, agencies,

and DoD and national-level leadership.

Provide Mission Partner and Leadership Support – DISA will design, develop,

implement, and maintain optimized, cost-efficient, interoperable decision support

systems to be used by mission partners at all levels of senior leadership. DISA will

ensure senior leadership has a modernized, reliable suite of services and capabilities that

enhance the execution of crisis management, coalition, and deliberate planning activities.

Provide Command and Control (C2) and Enable Cyberspace Sovereignty – DISA

will execute synchronized DoD Information Network (DODIN) command, operations,

and cyber defense missions to ensure freedom of maneuver for the warfighter and

mission partners. DISA will establish, train, and implement cyber workforce elements,

shape readiness through continuity programs, and execute synchronized operations that

will offer more visibility and response to cyber threats.

Program Performance

DISA’s information services play a key role in supporting the DoD’s operating forces. As a

result, DISA is held to high performance standards. In many cases, performance measures are

8

detailed in Service Level Agreements (SLAs) with individual customers that exceed the general

performance measures discussed in the following paragraphs.

Computing Services Performance Measures

The Computing Service business area tracks its performance and results through the Agency

Director’s Quarterly Performance Reviews. There are two key operational metrics which are

presented to the DISA Director in conjunction with regular, recurring Quarterly Program

Reviews. These two metrics depicted in the table below, reflect the availability of critical

applications in the Computing Centers. The first metric, “Core Data Center Availability,”

expressed as a percentage of availability, represents application availability from the end user’s

perspective and includes all outages or downtime regardless of root cause or problem ownership.

Tier II requires achieving 99.75% availability, which results in about 1,361 minutes of downtime

per year. Tier III, the standard for all DoD-designated Core Data Centers, requires achieving

99.98% availability, which results in about 95 minutes of downtime per year. A continuing

series of electrical and mechanical investments in the DISA Computing Ecosystem facilities

since 2008 have resulted in a steady decline in facility downtime. The second metric, “Capacity

Service Contract Equipment Availability” represents DISA’s equipment availability by

technology, i.e., how well DISA is executing its responsibilities exclusive of factors outside the

Agency's control such as last mile communications issues, base power outages or the like. The

Threshold refers to system uptime and capacity availability for intended use; this is the level

required by contract. The Objective is the value agreed on by the vendor and the government to

be an ideal target, and Actual is reported by the vendor monthly.

Core Data Center Availability

9

Capacity Service Contract Equipment Availability

Threshold Objective Actual

IBM System z Mainframe

99.95%

99.99%

100%

Unisys Mainframe

99.95%

99.99%

99.999%

P Series Server

99.95%

99.99%

100%

SPARC Server

99.95%

99.99%

100%

X86 Server

99.95%

99.99%

99.999%

Itanium

99.95%

>99.95%

99.994%

Storage

99.95%

>99.95%

99.999%

Communications Devices

99.95%

>99.95%

99.98%

Telecommunications Services Performance Measures

The DISN has operating metrics tied to the Department’s strategic goals of information

dominance. These operational metrics include the cycle time for delivery of data and satellite

services as well as service performance objectives such as availability, quality of service, and

security measures. Additionally, the Information Technology Enterprise Services Roadmap sets

a DISN performance target of 99.997% operational availability at all Joint Staff-validated

locations. DISA is working to meet the intent of this guidance through the evolving JIE

architecture and by building out the network as necessary to provide a growing number of

enterprise services. These categories of metrics have guided the development of the

Telecommunication Services budget submission. Shown below are major performance and

performance improvement measures:

Enterprise Acquisition Services Performance Measures

Enterprise Acquisition Services provides contracting services for information technology and

telecommunications acquisitions from the commercial sector and provides contracting support to

the DISN programs, as well as to other DISA, DoD, and authorized non-Defense customers.

These contracting services are provided through the DISA’s DITCO and include acquisition

planning, procurement, tariff surveillance, cost and price analyses, and contract administration.

10

These services provide end-to-end support for the mission partner. The following performance

measures apply for Enterprise Acquisition Services (EAS):

In addition to the program performance measures outlined above, DISA has increased

accountability of its assets by linking performance standards to internal control standards. Each

Senior Executive Service member at DISA has included in their performance appraisal a

standard to achieve accountability of property. This standard has filtered down to many of the

managers across the Agency. This increased focus on accountability has had a significant impact

on the focus these leaders have in the critical area of safeguarding assets.

3. Analysis of Entity’s Financial Statements

Background

DISA prepares annual financial statements in conformity with accounting principles generally

accepted in the United States. The accompanying financial statements and footnotes are

prepared in accordance with OMB Circular A-136, Financial Reporting Requirements. DISA

records accounting transactions on both an accrual and budgetary basis of accounting. Under the

accrual method, revenue is recognized when earned and costs/expenses are recognized when

incurred, without regard to receipt or payment of cash. Budgetary accounting facilitates

compliance with legal constraints and controls over the use of federal funds.

Since FY 2005, DISA has had an established Audit Committee to oversee progress towards

financial management reform and audit readiness. DISA leadership participates in Audit

Committee meetings to fully support the audit and in order to maintain senior leader tone-at-the-

top. The DISA Audit Committee is comprised of three members not part of DISA. The current

mission of the DISA Audit Committee is to serve in an advisory role to the DISA senior

managers. The committee is tasked with developing, raising, and resolving matters of financial

compliance and internal controls with the purpose of ensuring DISA’s consistent demonstration

of accurate and supportable financial reports. The committee develops and enforces guidance

established for this purpose. Amounts reflected as FY 2017 are unaudited.

11

DWCF Financial Highlights

The following section provides an executive summary and a brief description of the nature of

each financial statement, significant fluctuations, and significant balances to help clarify their

link to DISA operations.

Executive Summary – The DISA WCF reflects the results of budget execution that saw the

fund decrease $146.9 million (13%) for a total of $979.2 million on its unobligated balance

available, as compared to 4

th

Quarter, FY 2017. The Consolidated Statement of Net Cost reflect

a loss, through 4

th

Quarter, FY 2018 of $61.3 million and includes the non-recoverable

depreciation expense for network equipment transferred into TSEAS (PE55).

Obligations incurred increased by $536.3 million (8%), in comparison to the 4

th

Quarter

of last year partially driven by DISN IS Cybersecurity programs, and a $50 million

obligation for contracted support of the National Leadership Command Capabilities

(NLCC) Center.

The Consolidated Statement of Net Cost reflect a loss, through 4

th

Quarter, FY 2018 of

$61.3 million and includes the non-recoverable depreciation expense for network

equipment transferred into TSEAS (PE55).

Cash levels remained positive through the 4

th

Quarter, FY 2018 at 21.2 days of operating

cash.

All general ledger subsidiary detail has been reconciled to the field level accounting system trial

balances, and all journal vouchers posted to DDRS-B and DDRS-AFS have been reviewed,

reconciled and approved by DISA RM333 to ensure that the DDRS-AFS trial balance is 100%

supported by transaction detail.

Consolidated Balance Sheet

The balance sheet presents amounts available for use by DISA (assets) against amounts owed

(liabilities) and amounts that comprise the difference (net position).

Assets

Total assets of $1.9 billion are comprised primarily of Fund Balance with Treasury

($538.9 million), intragovernmental accounts receivable ($603.3 million), and Property,

Plant & Equipment (PP&E) ($756.6 million).

Fund Balance with Treasury - Fiscal year-to-date (FYTD) net cash flow from current

year operations (collections less disbursements) reported to Treasury for FY 2018, along

with the impact of the current year transfers in and out and the inception-to-date (ITD)

balances are presented below:

12

During FY 2017, $96.9 million of prior year cash transferred from back to CS

from TSEAS (zero impact at consolidated level).

The $538.9 million cash balance at 30 September 2018 is comprised of a

$633.9 million current year beginning balance and a FYTD $95 million decrease

from current year operations (includes capital outlays).

All DISA WCF cash balances are reconciled monthly to Treasury via the Cash

Management Report (CMR).

General Property, Plant and Equipment, Net – General Property, PP&E consists

primarily of equipment used by DISA organizations to deliver computing services to

customers in the DISA Computing Ecosystem and telecommunication services over the

DISN. PP&E includes capital assets funded by DISA WCF operations to include one

facility, capital assets supporting the infrastructure of the services offered by the WCF

that are transferred in from the DISA GF, and capital assets associated with JRSS

transferred in from the Army. The depreciation expense associated with the capital assets

transferred into the DISA WCF is non-recoverable.

Liabilities

As of 30 September 2018, DISA reported liabilities of $743.4 million. Liabilities are

probable and measurable future outflows of resources arising from past transactions or

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

CS Beg 194,236$ 85,124$ 109,112$ 128%

CS YTD 68,776$ 12,212$ 56,564$ -463%

Transfers -$ 96,900$ (96,900)$ -100%

CS Total 263,013$ 97,336$ 56,564$ -100%

TS Beg 439,660$ 341,754$ 97,905$ 29%

TS YTD (163,742)$ 194,805$ (358,547)$ -184%

Transfers -$ (96,900)$ -$ 0%

TS Total 275,918$ 536,559$ (260,642)$ -49%

Consolidated Beg. Balance 633,896$ 426,878$ 207,018$ 48%

Total From Operations - FYTD (94,966)$ 207,018$ (301,983)$ -146%

CY Transfers -$ -$ -$ 0%

Consolidated ITD Balance 538,930$ 633,459$ (94,966)$ -56%

($ Thousands)

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

CS 162,592$ 146,425$ 16,167$ 11%

TSEAS 593,982$ 539,362$ 54,620$ 10%

Consolidated 756,574$ 685,787$ 70,788$ 10%

($ Thousands)

13

events. The largest component of liabilities as of 30 September 2018 was $659 million in

accounts payable due to the public.

Accounts Payable - The table below compares current year to prior year

intragovernmental and public accounts payable balances.

Accounts Payable decreased 23% from prior year:

The largest portion of the Accounts Payable balance is comprised of TSEAS

(PE56) public contract payables.

From a customer funding perspective, the DISA General Fund and Army continue

to provide the most customer funded contract requirements associated with the

Public Accounts Payable balance.

The decrease in Non-Federal Payables (to the Public) is primarily attributed to a

drop in PE56 Other Reimbursable Orders from the DISA GF, Army, and Air

Force customers.

Consolidated Statement of Net Cost

The Statement of Net Cost presents the cost of operating DISA programs. The goal of the

revolving fund is to break even over the long term, thus driving toward an objective where the

Statement of Net Cost does not produce a profit or loss over the long term, but rather nets zero.

Net Cost of Operations decreased 47% between fiscal years.

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

CS

Intragov. 119,037$ 97,760$ 21,277$ 22%

Public 3,350$ 721$ 2,629$ 364%

TSEAS

Intragov. 17,463$ 35,958$ (18,495)$ -51%

Public 659,973$ 858,191$ (198,218)$ -23%

Component

Intragov. (100,870)$ (89,563)$ (11,307)$ 13%

Public (4,372)$ 309$ (4,681)$ -1517%

Consolidated

Intragov. 35,630$ 44,155$ (8,525)$ -19%

Public 658,951$ 859,221$ (200,269)$ -23%

Total Cons. 694,581$ 903,376$ (208,795)$ -23%

($ Thousands)

14

WCF Net Cost of Operations includes non-recoverable costs such as depreciation expense, future

funded FECA and imputed costs totaling 145.5 million. The Recoverable Net Operating Results

is $206.8 million for FY 2018.

Gross Cost - Gross Cost for the DISA WCF increased 7% from the prior year. In accordance

with regulations and guidance, this reflects the full cost of the DISA WCF to include recoverable

and non-recoverable cost.

The primary drivers contributing to the increase in gross costs are PE56 Information

Technology Contracts and PE55 DISN Cyber Security Infrastructure Services and DISN

Reimbursable Satellite Services.

PE54 Computing Services had increases for Reimbursable Converged Solutions and

Pass-Through Other Reimbursable Services.

Earned Revenue - Earned Revenue increased 8% from FY 2017.

PE56 Information Technology Contract for Other Reimbursable Requirements had a

significant increase of $338 million.

The Army and Air Force continue to be DISA WCF’s biggest customers.

The bar chart below reflects earned revenue per customer for FY 2017 and FY 2018.

($ Thousands)

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

CS (33,471)$ 1,762$ (35,233)$ -2000%

TSEAS 94,807$ 113,423$ (18,616)$ -16%

Consolidated 61,336$ 115,185$ (53,848)$ -47%

($ Thousands)

15

Consolidated Statement of Changes in Net Position

The Consolidated Statement of Changes in Net Position (SCNP) presents the change in net

position during the reporting period. The DISA WCF net position is affected by changes to its

two components, Other Financing Sources (transfers in/out without reimbursement and imputed

financing from costs absorbed by others), and Net Cost of Operations (Cumulative Results of

Operations). The SCNP format displays both components of net position separately to enable

the user to better understand the nature of changes to net position as a whole.

Transfers in/out without reimbursement increased $47.3 million primarily due to an

increase in capital assets transferred into the DISA WCF.

Imputed financing costs absorbed by others increased $7 million primarily due to an

increase in imputed cost related to employee benefits.

Net Cost of Operations decreased $53.8 million from FY 2017.

Statement of Budgetary Resources

The Statement of Budgetary Resources provides information on the budgetary resources

available to DISA as of 30 September 2018, and 30 September 2017, and the status of those

budgetary resources. The results and variances of key amounts reported in the Statement of

Budgetary Resources not described elsewhere are outlined below.

Obligations Incurred:

The major drivers for Obligations Incurred for the DISA WCF are as follows:

16

30 September 2018 balances include a $234.9 million downward adjustment for (PE56) and

$77.3 million for (PE55). This adjustment was done after a review of Undelivered Orders

(UDOs) without activity was performed. It was determined that aged UDOs that are dormant (no

activity within 12 months) should be considered to be invalid and adjusted for financial

statement purposes; regardless of whether a contract closeout action has been processed and a

source document is available to support the adjustment. The adjustment represents ledger detail

at the project level that has not had activity within the last 12 months.

PE56 30 September 2018 balance includes a $50 million obligation for contracted

support of the NLCC Center.

Largest increases for TSEAS (PE55) were in the DISN Infrastructure Services business

line programs to include Cybersecurity and CSS MIPR Process, offset by a decrease in

Information Assurance Net Operations.

Largest increases for CS (PE54) were in Reimbursable Pass through Server Converged

Solutions, Reimbursable Pass through Other Reimbursable Services, HW/SW

Application Support, and Customer Management. Also contributing to the increase is

Rate Based Services for IBM Mainframe Processing, GIG Content Deliver Services and

milCloud 2.0.

9/30/2018 9/30/2017 Inc./(Dec.)

Total Obligations Incurred 7,611,279$ 7,074,976$ 536,303$

Less: PE56 Obligations Incurred 4,691,864$ 4,418,993$ 272,871$

Total DISA WCF Funded Obligations 2,919,416$ 2,655,983$ 263,433$

TSEAS (PE55)

CSS-MIPR Process 565,446$ 422,956$ 142,490$

CYBERSECURITY-Perimeter Defense-Other 65,913$ -$ 65,913$

CYBERSECURITY-Public Key Infras-Other 45,077$ -$ 45,077$

Info Assurance Net Ops Other 12,819$ 149,382$ (136,563)$

CS (PE54)

Reimbursable Pass Through Server Converged Solutions 59,938$ 40,052$ 19,886$

Rate Based IBM Mainframe Processing 42,814$ 31,363$ 11,451$

Reimbursable Pass-Through Other Reimbursable Services 15,978$ 5,829$ 10,150$

Reimbursable Pass Through Server HW/SW Application Support 15,766$ 9,797$ 5,968$

Reimbursable Pass Through Customer Management 18,575$ 14,205$ 4,370$

Reimbursable Server Implementation 15,369$ 11,097$ 4,272$

Rate Based GIG Content Delivery Service 32,864$ 29,217$ 3,647$

Rate Based MilCloud 2 3,580$ -$ 3,580$

Reimbursable Pass Through Server Reimbursable (w/o Comm) 20,537$ 17,080$ 3,457$

All Other Programs Balances 2,004,742$ 1,925,006$ 79,736$

($ Thousands)

17

GF Financial Highlights

The DISA General Fund Financial Statements for the year ended 30 September 2018 reflect a

fund that had a significant increase in overall appropriations in FY 2018 compared to FY 2017.

See table below for comparative data for appropriations received between these two fiscal years.

Consolidated Balance Sheet

The balance sheet presents amounts available for use by DISA (assets) against amounts owed

(liabilities) and amounts that comprise the difference (net position).

Assets

Total assets of $3.5 billion are comprised primarily of Fund Balance with Treasury

($3 billion) and PP&E ($500.4 million).

Fund Balance with Treasury - Amounts recorded in the general ledger for Fund Balance

with Treasury (FBwT) have been 100% reconciled to amounts reported in the CMR,

representing DISA General Fund’s portion of the TI97 appropriated account balances

reported by Department of Treasury. All reconciling differences (i.e., undistributed) have

been identified at the voucher level.

General PP&E Net – (PP&E) consists primarily of equipment used by DISA

organizations achieve the Agency’s missions. The table below reflects the net book value

of PP&E recorded as of 30 September 2018 and 30 September 2017.

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

O&M (0100) 2,059,810$ 1,498,556$ 561,254$ 37%

PROC (0300) 719,245$ 988,419$ (269,174)$ -27%

RDT&E (0400) 270,820$ 250,275$ 20,545$ 8%

MILCON (0500) 1,175$ 5,218$ (4,043)$ -77%

Consolidated 3,051,050$ 2,742,468$ 308,582$ 11%

(in thousands)

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

O&M (0100) 951,680$ 743,155$ 208,525$ 28%

PROC (0300) 1,725,382$ 1,635,560$ 89,822$ 5%

RDT&E (0400) 269,622$ 247,990$ 21,632$ 9%

MILCON (0500) 37,852$ 37,149$ 702$ 2%

Consolidated 2,984,536$ 2,663,854$ 320,681$ 12%

(in thousands)

18

Liabilities

As of 30 September 2018, DISA reported liabilities of $263.8 million. Liabilities are

probable and measurable future outflows of resources arising from past transactions or

events. The largest component of Liabilities as of 30 September 2018 was $189.9 million

in federal accounts payable due to conducting business with intragovernmental trading

partners.

Accounts Payable - Balances reported as of 30 September 2018 and 30 September 2017

consist of the following:

Consolidated Statement of Net Cost

The Statement of Net Cost presents the cost of operating DISA programs. The GF consolidated

net cost for the Agency in FY 2018 totaled $2.5 billion and represented an overall increase of

$337 million from FY 2017.

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

O&M (0100) 378,715$ 386,524$ (7,809)$ -2%

PROC (0300) 108,657$ 73,696$ 34,961$ 47%

RDT&E (0400) 3,681$ 5,275$ (1,594)$ -30%

MILCON (0500) 9,382$ 9,857$ (475)$ -5%

Consolidated 500,436$ 475,352$ 25,083$ 5%

(in thousands)

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

O&M (0100)

Intragov. 118,602$ 137,457$ (18,855)$ -14%

Public (2,357)$ 15,802$ (18,158)$ -115%

PROC (0300)

Intragov. 38,293$ 11,748$ 26,545$ 226%

Public 3,648$ 23,508$ (19,860)$ -84%

RDT&E (0400)

Intragov. 32,966$ 22,134$ 10,832$ 49%

Public 8,870$ 8,686$ 184$ 2%

MILCON (0500)

Intragov. -$ 1$ (1)$ -100%

Public (4)$ 0$ (4)$ 0%

Intragov. 189,861$ 171,340$ 18,521$ 11%

Public 10,158$ 47,996$ (37,838)$ -79%

Total Cons. 200,019$ 219,336$ (19,318)$ -9%

(in thousands)

19

Consolidated Statement of Changes in Net Position

The Consolidated Statement of Changes in Net Position (SCNP) presents the change in net

position during the reporting period. The DISA GF net position is affected by changes to its two

components, Cumulative Results of Operations incorporating Net Cost of Operations to include

Other Financing Sources (transfers in/out without reimbursement and imputed financing from

costs absorbed by others) and Unexpended Appropriations consisting primarily of appropriations

received. The SCNP format displays both components of net position separately to enable the

user to better understand the nature of changes to net position as a whole.

Appropriations received increased $248.2 million primarily for O&M with an increase of

$553.3 million offset by a decrease of $303.8 million in Procurement funding for

FY 2018.

Other Financing Sources, Transfers in/out without reimbursement decreased by a net

$56.4 million from prior year driven by the transfers-out of assets to the DISA Working

Capital Fund.

Other Financing Sources, Imputed financing from costs absorbed by others decreased

$140.8 million due to the DoD early implementation of SFFAS 55 “Amending Inter-

Entity Cost Provisions” whereby the DISA GF was not required to record the imputed

cost of military labor for FY 2018 as was done for FY 2017.

Statement of Budgetary Resources

The Statement of Budgetary Resources provides information on the budgetary resources

available to DISA as of 30 September 2018, and 30 September 2017, and the status of those

budgetary resources. The results and variances of key amounts reported in the Statement of

Budgetary Resources not described elsewhere are outlined below.

20

4. Management Systems, Controls & Compliance with Laws and Regulations

Management Assurances

Our management structure, policies and procedures, and our Internal Control (IC) reviews of our

key mission processes contribute to the reasonable assurance that our internal controls are

operating as intended. Our Governance Board and Internal Control Structure along with the

Managers’ Internal Control Program (MICP) is managed through a three tiered approach, as

described in subsequent paragraphs. The first tier is supported by the DISA Senior Assessment

Team (SAT), which provides guidance and oversight to the MICP. The second tier is supported

by subject-matter expert team, the IC team, and the third tier is supported by the Assessable Unit

Managers (AUMs) who manage at the Program/Directorate level within the organization. The

SAT and IC teams maintain a charter that is available on the DISA webpage. Each document

outlines the mission, personnel, roles, and responsibilities of the team. AUMs are appointed in

writing each year, and the appointment letter delineates the role and responsibilities that AUMs

are charged with.

For FY 2018 reporting cycle, DISA identified 12 Assessable Units (AUs): RMC, Component

Acquisition Executive (CAE), Development and Business Center (DBC), Chief of Staff (DDC),

(in thousands)

9/30/2018 9/30/2017 Inc./(Dec.) % Chg.

(O&M 0100)

Obligations Incurred 2,231,058$ 1,618,184$ 612,874$ 38%

Unobligated Balances 83,331$ 82,159$ 1,172$ 1%

Undelivered Orders 844,888$ 586,927$ 257,961$ 419%

Unfilled Customer Orders 101,052$ 61,494$ 39,558$ 64%

(PROC 0300)

Obligations Incurred 934,353$ 1,008,161$ (73,808)$ -7%

Unobligated Balances 295,934$ 443,449$ (147,515)$ -33%

Undelivered Orders 1,400,555$ 1,166,400$ 234,155$ 20%

Unfilled Customer Orders 9,637$ 2,634$ 7,003$ 266%

(RDT&E 0400)

Obligations Incurred 335,765$ 318,795$ 16,970$ 5%

Unobligated Balances 68,471$ 63,270$ 5,201$ 8%

Undelivered Orders 208,332$ 211,823$ (3,491)$ -7%

Unfilled Customer Orders 51,805$ 50,631$ 1,174$ 2%

(MILCON 0500)

Obligations Incurred 1,062$ 2,470$ (1,408)$ -57%

Unobligated Balances 30,026$ 27,698$ 2,328$ 8%

Undelivered Orders 7,829$ 9,450$ (1,621)$ -17%

(Combined)

Obligations Incurred 3,502,238$ 2,947,610$ 554,628$ 19%

Unobligated Balances 477,762$ 616,576$ (138,814)$ -23%

Undelivered Orders 2,461,604$ 1,974,600$ 487,004$ 25%

Unfilled Customer Orders 162,494$ 114,759$ 47,735$ 42%

21

Defense Spectrum Organization (DSO), Inspector General (IG), Joint Force Headquarters-

DODIN (JFHQ-DODIN), JSP, Operations Center (OC), Procurement Services Directorate

(PSD), Risk Management Executive (RME), and White House Communications Agency

(WHCA). Each AU was led by at least one member of the Senior Executive Service (SES) or

military flag officer, or carries a distinct mission within DISA, which in turn causes the AU to

have unique operational risks that require evaluation. All organizations were also required to

identify the functions performed within their area (outside of the required testing areas of

Defense Travel System (DTS), Automated Time Attendance and Production System (ATAAPS),

Records Management, and Property, Plant and Equipment (PP&E)), identify the level of process

documentation available, and determine the associated risk of those functions. Additionally, the

AUM was responsible for identifying and documenting the key controls within their AU. RMC

documented processes and key controls for all ICOFR functions. Each AU documented its key

processes and risk on the Mission Processes Spreadsheet. The RMC MICP team advised the

AUMs to test, at a minimum, those key processes that were self-identified as high risk, as well as

Safety, Security (if applicable), and the required testing areas.

DISA delegates authority only to the extent required to achieve objectives and management

evaluates the delegation for proper segregation of duties to prevent fraud, waste, and abuse. In

addition, DISA relies on external stakeholders, such as DFAS as our accounting data processor,

bill payer, and payroll processor to better achieve our mission as documented in a Service Level

Agreement (SLA).

The DISA IG maintains a hotline for the anonymous reporting of ethics and integrity issues that

is available to employees 24 hours a day, 7 days a week. Additionally, the DISA IG conducts

reviews and inspections to identify or prevent instances of fraud, waste, and abuse.

The RMC/Comptroller conducts the testing and reports on the overall Internal Controls Over

Financial Reporting (ICOFR) for the Agency. The DISA Chief Information Officer (CIO)

conducts the testing and reports results of the Internal Controls Over Financial Systems (ICOFS)

for the Agency. Agency AUMs perform testing and report results of the Internal Controls over

Non-Financial Operations (ICONO).

DISA’s senior management evaluated the system of internal control in effect during the fiscal

year as of the date of this memorandum, according to the guidance in OMB Circular No. A-123

and the Government Accountability Office (GAO) Green Book. Included is the Agency’s

evaluation of whether the system of internal controls for DISA is in compliance with standards

prescribed by the Comptroller General.

The objectives of the system of internal controls of DISA are to provide reasonable assurance of:

Effectiveness and efficiency of operations,

Reliability of financial reporting,

Compliance with applicable laws and regulations; and

Financial information systems are compliant with the FFMIA of 1996 (Public Law 104-

208).

22

The evaluation of internal controls extends to every responsibility and activity undertaken by

DISA and applies to program, administrative, and operational controls. Furthermore, the concept

of reasonable assurance recognizes that (1) the cost of internal controls should not exceed the

benefits expected to be derived, and (2) the benefits include reducing the risk associated with

failing to achieve the stated objectives. Moreover, errors or irregularities may occur and not be

detected because of inherent limitations in any system of internal controls, including those

limitations resulting from resource constraints, congressional restrictions, and other factors.

Finally, projection of any system evaluation to future periods is subject to the risk that

procedures may be inadequate because of changes in conditions, or that the degree of compliance

with procedures may deteriorate. Therefore, this statement of reasonable assurance is provided

within the limits of the preceding description.

DISA management evaluated the system of internal controls in accordance with the guidelines

identified above. The results indicate that the system of internal controls of DISA, in effect as of

the date of this MD&A, taken as a whole, complies with the requirement to provide reasonable

assurance that the above mentioned objectives were achieved. This position on reasonable

assurance is within the limits described in the preceding paragraph.

Using the following process, DISA evaluated its system of internal controls and maintains

sufficient documentation/audit trail to support its evaluation and level of assurance.

As previously discussed, DISA manages MICP through a three-tiered approach. The first tier is

supported by the DISA SAT, which provides guidance and oversight to the MICP. The SAT met

multiple times during this cycle; initially to discuss Enterprise Risk Management (ERM) and

finally to summarize results for the Agency Statement of Assurance (SOA). In FY 2018, the

DISA Director signed a “Tone-at-the-Top” memo that defines management’s leadership and

commitment towards an effective MICP: openness, honesty, integrity, and ethical behavior. The

memo directed the Agency to ensure a risk-based and results-oriented program in alignment with

the Government Accountability Office (GAO) Green Book and OMB A-123. The tone at the top

is set by all levels of management and has a trickle-down effect to all employees. The second

tier, supported by a subject matter expert (SME) team, coordinates requirements with OSD

Comptroller regarding the MICP, in addition to providing guidance, oversight, and validation in

accordance with OSD Directives to the AUMs. DISA provided internal control training for the

AUMs in January 2018 and conducted additional workshops in February 2018. The MICP team

compiles AU submissions for the Agency’s SOA, communicates OSD requirements to

leadership, facilitates information sharing between AUMs, and consolidates results.

Internal Controls over Financial Systems - DISA performed the FY 2018 review of the core

financial systems for the three financial reporting units: 1) Working Capital Fund (WCF),

Financial Accounting Management Information System (FAMIS), Telecommunications Services

and Enterprise Acquisition Services (TSEAS), 2) WCF FAMIS Computing Services (CS) Mod,

and 3) Washington Headquarters Services Allotment Accounting System (WAAS) for the

General Fund (GF). Using independent tests, OMB Circular A-123, Appendix D, and the

Implementation Guidance for FFMIA, the DISA CIO Director of OC, and the Director of RMC

jointly assessed DISA’s core financial systems. Two of the three core financial systems, FAMIS

TSEAS and WAAS, are legacy systems that have certain limitations. DISA relies on several

23

interfaces to the legacy financial systems to achieve certain requirements of FFMIA compliance.

The FY 2018 assessment considered the risks associated with relying on external systems for

core requirements and the necessity to implement manual control activities to mitigate the risk.

There were control deficiencies addressed in the FY 2016 Independent Public Accountant (IPA)

report. To the extent appropriate, the issues identified have been corrected. DISA’s core

financial management systems routinely provide reliable and timely information for managing

day-to-day operations, as well as providing information used to prepare financial statements and

maintain effective internal controls. All of these factors are key indicators of FFMIA

compliance. Additionally, DISA provides application hosting services for the Department’s

service providers (Defense Finance and Accounting Service; Defense Logistics Agency; Defense

Contract Management Agency; Defense Human Resource Activity (DHRA); Military Services,

and Other Defense Organizations). As a result, DISA is responsible for most of the IT general

controls over the computing environment in which many financial, personnel, and logistics

applications reside. In order for service providers and components to rely on automated controls

and documentation within these applications, controls must be appropriately and effectively

designed.

In FY 2018, DISA embarked on two Statement on Standards for Attestation Engagement (SSAE)

18 efforts and received unmodified opinions on both; application hosting services (sixth

consecutive year) and ATAAPS (second consecutive year). These unmodified opinions provide

DISA’s Mission Partners and their auditors the confidence that they can rely on for the

automated controls and documentation within these applications. DISA’s core financial

accounting systems are also covered in this attestation. The WAAS replacement by the Defense

Agencies Initiative (DAI) and FAMIS-TSEAS Enterprise Resource Planning (ERP) replacement

by FAMIS Enterprise Acquisition Services (EAS) Modernization were implemented in

October 2018. The implementation of these ERP approved systems will facilitate resolution of

compliance issues associated with the legacy systems. Finally, DISA considered the FFMIA

compliance Determination Framework to determine whether the Agency complies with the

Section 803(a) requirements of FFMIA. Some of these key indicators include the fact that DISA

consistently provides timely and reliable financial statements to OMB within 21 calendar days at

the end of the first through third quarters and unaudited financial statements to OMB, GAO, and

Congress by 15 November each year. DISA has not reported anti-deficiency violations in more

than a decade, and the Agency continues to demonstrate compliance with laws and regulations.

In addition, Information Assurance (IA) policies and procedures were converted from

Department of Defense Information Assurance Certification and Accreditation Process

(DIACAP) to the Risk Management Framework (RMF) as of March 2018.

Internal Controls over Financial Reporting - The RMC/Comptroller documented end-to-end

business processes and identified key internal control activities supporting key business

processes for ICOFR. DISA conducted an internal risk assessment that evaluated the results of

prior year audits, internal analysis of the results of financial operations, and known upcoming

business events. An internal control assessment was conducted within DISA for mission specific

key processes.

Based on the results of the internal risk analysis, internal testing was conducted to evaluate the

significance of potential deficiencies identified. Specific areas of testing included the following:

24

Year End Obligations (GF)

Revenue/Collections (GF and WCF)

Expense/Disbursements (GF and WCF)

Accounts Payable (WCF)

Accounts Receivable (WCF)

Integrated Defense Enterprise Acquisition System (IDEAS) Telecommunication

(TELCOM) initial contracting actions (WCF)

Undelivered Orders (UDOs) (GF)

Year-End Roll Forward (GF and WCF)

PP&E Disposals (GF)

PP&E Non-DISA Sites (GF)

Employee Debt Review (WCF)

Unfilled Customer Orders (UCOs) (WCF)

The details of these internal control reviews and the supporting documentation are kept on file

for reference. No material weaknesses were found.

DISA is currently undergoing an FY 2018 full financial statement audit for both the WCF and

GF. Because DISA’s FY 2016 audit was out-of-cycle and not completed until July 2017, a

decision was made to forego the audit of FY 2017 financial statements.

DISA is one of the few DoD agencies to navigate the rigors of a full financial statement audit.

This success is a culmination of the DISA efforts in support of the Department-wide initiatives to

achieve audit readiness. DISA is recognized for best practices for building a foundation through

compliant processes, establishing a seasoned audit support team, standardizing reconciliations

and analyses, building a staging library of key supporting documents, and establishing an overall

culture of readiness. DISA was able to successfully provide universe of transaction details,

monthly Fund Balance with Treasury (FBwT) reconciliations, capital property existence,

completeness and valuation requirements and support, aging schedules for accounts receivable

and accounts payable (AP), journal voucher coordination with the Defense Finance and

Accounting Service (DFAS), and elimination reconciliations with DISA’s trading partners.

These have all been identified as issues that, in the past, have prevented other DoD agencies

from achieving an audit opinion. To ensure quick responses to the auditors’ demands, RM3

prepositioned key artifacts in DISA's Financial Reporting library.

Internal Controls over Operations - During DoD IG Audit 2017-113, a potential material

weakness was identified with regard to payments made on 1,077 expired Communication

Services Authorizations (CSAs). DISA concurred with the DoD IG recommendation to

determine whether payments on expired CSAs were improper, in accordance with the Improper

Payments Elimination and Recovery Improvement Act (IPERIA). The research identified

approximately $205M in payments made on CSAs and related noncompliant contract actions.

The contract actions were noncompliant because DISA did not follow the Federal Acquisition

Regulations (FAR) when DISA continued a contractual relationship with a vendor without re-

competing the requirement or preparing a justification and approval.

25

While the payments for these noncompliant contract actions meet the definition of improper

payments under OMB A-123 guidance, the government cannot pursue recovery actions because

the government received value for the services rendered.

Accounting for Service Providers’ Internal Controls - DISA fully supports the Department's goal

to achieve auditable financial statements and as a service provider, demonstrates this

commitment through annual examinations by the IPA. For the seventh consecutive year, DISA

received an unmodified opinion on the hosting services platform Statement of Standard for

Attestation Engagements (SSAE) No. 18. The Agency continually works to improve processes,

enhance controls, and validate information. Additionally, DISA undertook an independent

application examination of the ATAAPS, for which the Agency received an unmodified opinion

for the second consecutive year. Even though DISA as a reporting agency has migrated to

Defense Agencies Initiative (DAI) Oracle Time and Labor module as of June 2018, the SSAE 18

process for ATAAPS will continue on behalf of DISA’s customers.

DISA hosts more than 100 financial systems throughout the DoD. DISA’s sustained clean

opinion on hosting services provides mission partners and their auditor the confidence that they

can rely on the automated controls and documentation within these applications.

In 2017, OSD Financial Improvement and Audit Readiness (FIAR) led Department-wide

discussions regarding SSAE 18s and the impact to component financial statements. DISA

participated in these discussions from both a service provider and reporting entity perspective.

As a result, 275 Complementary User Entity Controls (CUECs) were identified that had impact

to the financial statements. In addition to continued participation in multiple Service Provider

CUEC discussions in 2018, DISA has analyzed the 275 identified CUECs and determined the

Agency’s level of risk, and identified control descriptions and control attributes for each. For

those CUECs determined to be common across all the identified systems, testing was conducted

for areas of high risk.

26

Conclusion on Overall Assessment of Internal Control

27

28

29

In addition to FMFIA, DISA reports its compliance with the Federal Financial Management

Improvement Act (FFMIA). FFMIA requires an assessment of adherence to financial

management system requirements, accounting standards, and U.S. Standard General Ledger

transaction level reporting. For FY 2018, DISA is reporting overall substantial compliance. The

following is a comprehensive list of laws and regulations which were assessed for compliance by

the DISA WCF in context of the FY 2018 audit.

Acronym

Laws & Regulations

(Supplement Number)

ADA

Antideficiency Act, 31 U.S.C. 1341 and 1517, January 7, 2011 and OMB A-11,

Preparation, Submission and Execution of the Budget, July 2010.

FAM 803

DCIA

Provisions Governing Claims of the U.S. Government as provided primarily in 31

U.S.C. 3711-3720E (Including the Debt Collection Improvement Act of 1996) (DCIA).

FAM 809

PPA

Prompt Payment Act, 5 CFR 1315, September 29, 1999. FAM 810

CSRA

Civil Service Retirement Act

FAM 813

FEHB

Federal Employees Health Benefits Act

FAM 814

FECA

Federal Employees’ Compensation Act

FAM 816

FERS

Federal Employees’ Retirement System Act of 1986

FAM 817

PAS for

CEs

Pay and Allowance System for Civilian Employees as Provided Primarily in Chapters

51-59 of Title 5, U.S. Code

FAM 812

CFO Act,

A-123

Chief Financial Officers (CFO) Act of 1990 and OMB Circular A-136, Financial

Reporting Requirements, September 29, 2010.

FFMIA

Federal Financial Management Improvement Act (FFMIA) of 1996; OMB Circular A-

127, Financial Management Systems, January 9, 2009; OMB Circular A-130,

Transmittal Memorandum #4, Management of Federal Information Resources,

November 28, 2000.

FMFIA and

A-123

Federal Managers Financial Integrity Act (FMFIA) of 1982 and OMB Circular A-123,

Appendix A, August 1, 2005.

FISMA

Federal Information Security Management Act (FISMA) of 2002.

DoD FMR

Department of Defense (DoD), Financial Management Regulation 7000.14-R,

August 26, 2011.

IPERA

Improper Payments Elimination and Recovery Act of 2010 (IPERA) and OMB Circular

A-123, Appendix C, Parts I and II, April 14, 2011 and Part III, March 22, 2010.

30

Financial Management Systems Framework, Goals, and Strategies

DISA’s WCF financial related system implementations have been planned and designed within

the framework of the Business Enterprise Architecture (BEA) established within the Department

of Defense, which facilitates to the extent possible a more standardized framework for systems in

the Department. Financial system related initiatives target implementation of a standardized

financial information structure that will be compliant with FFMIA and BEA requirements, and

provide DISA with cost accounting data and timely accounting information that enables

enhanced decision-making.

The WAAS replacement by the Defense Agencies Initiative (DAI) and FAMIS-TSEAS

Enterprise Resource Planning (ERP) replacement by FAMIS Enterprise Acquisition Services

(EAS) Modernization were implemented in October 2018. The implementation of these ERP

approved systems will facilitate resolution of compliance issues associated with the legacy

systems. Finally, DISA considered the FFMIA compliance Determination Framework to

determine whether the Agency complies with the Section 803(a) requirements of FFMIA. Some

of these key indicators include the fact that DISA consistently provides timely and reliable

financial statements to OMB within 21 calendar days at the end of the first through third quarters

and unaudited financial statements to OMB, GAO, and Congress by 15 November each year.

DISA has not reported anti-deficiency violations in more than a decade, and the Agency

continues to demonstrate compliance with laws and regulations. In addition, Information

Assurance (IA) policies and procedures were converted from Department of Defense

Information Assurance Certification and Accreditation Process (DIACAP) to the Risk

Management Framework (RMF) as of March 2018.

DISA also conducted an internal review of the effectiveness of the internal controls over the

integrated financial management systems in accordance with Federal Financial Management

Improvement Act (FFMIA) of 1996 (Public Law I 04-208) and 0MB Circular No. A-123,

Appendix D. The "Internal Control Evaluation" section provides specific information on how

DISA conducted this assessment. Based on the results of this assessment, DISA can provide

reasonable assurance, except for the two non-conformances reported in the "Significant

Deficiencies/Material Weaknesses and Corrective Action Plans Template" that the internal

controls over the financial systems are in compliance with the FFMIA and 0MB Circular

No. A-l23, Appendix D, as of 30 September 2018.

5. Limitations of the Financial Statements

The principal financial statements have been prepared to report the financial position and results

of operations of the DISA WCF and GF, pursuant to the requirements of 31 U.S.C. 3515(b).

While the statements have been prepared from books and records of the DISA WCF and GF in

accordance with GAAP for Federal entities and the formats prescribed by OMB, the statements

are in addition to the financial reports used to monitor and control budgetary resources, which

are prepared from the same books and records.

The statements should be read with the realization that they are for a Defense Agency of the U.S.

Government, a sovereign entity.

31

Principal Statements

32

7KHDFFRPSDQ\LQJQRWHVDUHDQLQWHJUDOSDUWRIWKHVHVWDWHPHQWV

LQ7KRXVDQGV

'HSDUWPHQWRI'HIHQVH

'HIHQVH,QIRUPDWLRQ6\VWHPV$JHQF\*HQHUDO)XQG

&2162/,'$7('%$/$1&(6+((7

$VRI6HSWHPEHUDQG

$66(761RWH

,QWUDJRYHUQPHQWDO

)XQG%DODQFHZLWK7UHDVXU\1RWH

$FFRXQWV5HFHLYDEOH1RWH

7RWDO,QWUDJRYHUQPHQWDO$VVHWV

$FFRXQWV5HFHLYDEOH1HW1RWH

*HQHUDO3URSHUW\3ODQWDQG(TXLSPHQW1HW1RWH

2WKHU$VVHWV1RWH

727$/$66(76

67(:$5'6+,33523(57<3/$17(48,30(171$

/,$%,/,7,(61RWH

,QWUDJRYHUQPHQWDO

$FFRXQWV3D\DEOH1RWH

2WKHU/LDELOLWLHV1RWH

7RWDO,QWUDJRYHUQPHQWDO/LDELOLWLHV

$FFRXQWV3D\DEOH1RWH

0LOLWDU\5HWLUHPHQWDQG2WKHU)HGHUDO

(PSOR\PHQW%HQHILWV1RWH

2WKHU/LDELOLWLHV1RWHDQG1RWH

727$//,$%,/,7,(6

&200,70(176$1'&217,1*(1&,(6127(

1(7326,7,21

8QH[SHQGHG$SSURSULDWLRQV2WKHU)XQGV

&XPXODWLYH5HVXOWVRI2SHUDWLRQV2WKHU)XQGV

727$/1(7326,7,21

727$//,$%,/,7,(6$1'1(7326,7,21

&RQVROLGDWHG

8QDXGLWHG

&RQVROLGDWHG

8QDXGLWHG

33

7KHDFFRPSDQ\LQJQRWHVDUHDQLQWHJUDOSDUWRIWKHVHVWDWHPHQWV

LQ7KRXVDQGV

'HSDUWPHQWRI'HIHQVH

'HIHQVH,QIRUPDWLRQ6\VWHPV$JHQF\*HQHUDO)XQG

&2162/,'$7('67$7(0(172)1(7&267

)RUWKHSHULRGVHQGHG6HSWHPEHUDQG

3URJUDP&RVWV

*URVV&RVWV

/HVV(DUQHG5HYHQXH

1HW&RVWEHIRUH/RVVHV*DLQVIURP$FWXDULDO$VVXPSWLRQ&KDQJHV

IRU0LOLWDU\5HWLUHPHQW%HQHILWV

1HW3URJUDP&RVWV,QFOXGLQJ$VVXPSWLRQ&KDQJHV

1HW&RVWRI2SHUDWLRQV

&RQVROLGDWHG

8QDXGLWHG

&RQVROLGDWHG

8QDXGLWHG

34

7KHDFFRPSDQ\LQJQRWHVDUHDQLQWHJUDOSDUWRIWKHVHVWDWHPHQWV

LQ7KRXVDQGV

'HSDUWPHQWRI'HIHQVH

'HIHQVH,QIRUPDWLRQ6\VWHPV$JHQF\*HQHUDO)XQG

&2162/,'$7('67$7(0(172)&+$1*(6,11(7326,7,21

)RUWKHSHULRGVHQGHG6HSWHPEHUDQG

81(;3(1'('$335235,$7,216

%HJLQQLQJ%DODQFHV,QFOXGHV)XQGVIURP'HGLFDWHG

&ROOHFWLRQV1$

%HJLQQLQJEDODQFHVDVDGMXVWHG

%XGJHWDU\)LQDQFLQJ6RXUFHV

$SSURSULDWLRQVUHFHLYHG

$SSURSULDWLRQVWUDQVIHUUHGLQRXW

2WKHUDGMXVWPHQWV

$SSURSULDWLRQVXVHG

7RWDO%XGJHWDU\)LQDQFLQJ6RXUFHV,QFOXGHV)XQGVIURP

'HGLFDWHG&ROOHFWLRQV1$

7RWDO8QH[SHQGHG$SSURSULDWLRQV,QFOXGHV)XQGVIURP

'HGLFDWHG&ROOHFWLRQV1$

&808/$7,9(5(68/762)23(5$7,216

%HJLQQLQJ%DODQFHV

%HJLQQLQJEDODQFHVDVDGMXVWHG,QFOXGHV)XQGVIURP

'HGLFDWHG&ROOHFWLRQV1$

2WKHUDGMXVWPHQWV

$SSURSULDWLRQVXVHG

2WKHUEXGJHWDU\ILQDQFLQJVRXUFHV

7UDQVIHUVLQRXWZLWKRXWUHLPEXUVHPHQW

,PSXWHGILQDQFLQJIURPFRVWVDEVRUEHGE\RWKHUV

2WKHU

7RWDO)LQDQFLQJ6RXUFHV,QFOXGHV)XQGVIURP'HGLFDWHG

&ROOHFWLRQV1$

1HW&RVWRI2SHUDWLRQV,QFOXGHV)XQGVIURP

'HGLFDWHG&ROOHFWLRQV1$

1HW&KDQJH

&XPXODWLYH5HVXOWVRI2SHUDWLRQV,QFOXGHV)XQGVIURP

'HGLFDWHG&ROOHFWLRQV1$

1HW3RVLWLRQ

&RQVROLGDWHG

8QDXGLWHG

&RQVROLGDWHG

8QDXGLWHG

35

7KHDFFRPSDQ\LQJQRWHVDUHDQLQWHJUDOSDUWRIWKHVHVWDWHPHQWV

LQ7KRXVDQGV

'HSDUWPHQWRI'HIHQVH'HIHQVH,QIRUPDWLRQ6\VWHPV$JHQF\*HQHUDO)XQG

&20%,1('67$7(0(172)%8'*(7$5<5(6285&(6

)RUWKHSHULRGVHQGHG6HSWHPEHUDQG

%XGJHWDU\5HVRXUFHV

8QREOLJDWHGEDODQFHIURPSULRU\HDUEXGJHWDXWKRULW\QHW

GLVFUHWLRQDU\DQGPDQGDWRU\

$SSURSULDWLRQVGLVFUHWLRQDU\DQGPDQGDWRU\

6SHQGLQJ$XWKRULW\IURPRIIVHWWLQJFROOHFWLRQV

GLVFUHWLRQDU\DQGPDQGDWRU\

7RWDO%XGJHWDU\5HVRXUFHV

1HWDGMXVWPHQWVWRXQREOLJDWHGEDODQFHEURXJKWIRUZDUG2FW

6WDWXVRI%XGJHWDU\5HVRXUFHV

1HZREOLJDWLRQVDQGXSZDUGDGMXVWPHQWVWRWDO

8QREOLJDWHGEDODQFHHQGRI\HDU

$SSRUWLRQHGXQH[SLUHGDFFRXQWV

8QDSSRUWLRQHGXQH[SLUHGDFFRXQWV

8QH[SLUHGXQREOLJDWHGEDODQFHHQGRI\HDU

([SLUHGXQREOLJDWHGEDODQFHHQGRI\HDU

8QREOLJDWHGEDODQFHHQGRI\HDUWRWDO

7RWDO%XGJHWDU\5HVRXUFHV

2XWOD\VQHW

2XWOD\VQHWWRWDOGLVFUHWLRQDU\DQGPDQGDWRU\

$JHQF\2XWOD\VQHWGLVFUHWLRQDU\DQGPDQGDWRU\

&RPELQHG

8QDXGLWHG

&RPELQHG

8QDXGLWHG

36

Defense Information Systems Agency

General Fund

Notes to the Principal Statements

4

th

Quarter Fiscal Year 2018, ending September 30, 2018

37

DISA General Fund

Note1.

Significant Accounting Policies

A. Reporting Entity

The Defense Information Systems Agency (DISA), a Combat Support Agency, provides,

operates, and assures command and control, information-sharing capabilities, and a globally

accessible enterprise information infrastructure in direct support of joint warfighters, national-level

leaders, and other mission and coalition partners across the full spectrum of operations.

The history of DISA is traceable to the Defense Reorganization Act of 1958, which authorized the

creation of a joint military communications network to be formed by consolidation of the

communications facilities of the Military Departments. This would ultimately lead to the formation

of the Defense Communications Agency (DCA). Over the next several years, DCA expanded its

mission and underwent a number of mergers with other agencies to enhance the interoperability

of command, control, and communications (C3). On June 25, 1991, DCA was renamed DISA to

reflect its expanded role in implementing the Department of Defense’s (DoD) information

initiatives, and to clearly identify DISA as a combat support agency. Currently, DISA is the

premier Information Technology Combat Support Agency that provides and assures command,

control, communications, computing, intelligence, surveillance, and reconnaissance (C4ISR) to

the warfighter, and delivers enterprise services and data at the user point of need. In addition,

with the standup of the new Joint Force Headquarters-DoD Information Network (JFHQ-DoDIN)

organization on January 15, 2015, DISA now serves as the joint operational arm of defense

cyberspace operations for the DoD. The JFHQ-DoDIN exercises command and control of DoDIN

operations and defensive cyber operations-internal defense measures globally in order to

synchronize the protection of DoD component capabilities and to enable power projection and

freedom of action across all warfighting domains. The DISA operates under the direction,

authority, and control of the DoD Chief Information Officer (CIO) who reports directly to the

Secretary of Defense.

The DISA operates using two funding sources: general fund (GF) appropriations and a working

capital fund (WCF). The DISA WCF is a separately reported fund and not included herein. The

DISA GF receives appropriations and funds through the established Office of Management and

Budget (OMB) and DoD fund distribution process. The DISA GF uses these appropriations and

funds to execute missions that are not funded by WCF, and it subsequently reports on resource

usage supported by financial transactions for civilian personnel, operation and maintenance,

research and development, procurement, and military construction.

The DISA GF is a party to allocation transfers with other federal agencies as a transferring parent

entity. An allocation transfer is an entity’s legal delegation of authority to obligate budget

authority and outlay funds on its behalf. Generally, all financial activity related to allocation

transfers (e.g., budget authority, obligations, and outlays) are reported in the financial statements

of the parent entity. As a parent, DISA GF allocates funds to U.S. Army Central.