AUDIT

ANALYTICS

aicpa.org | cpa.com

AICPA Assurance Services Executive Committee

The mission of the AICPA Assurance Services Executive Committee (ASEC)

is to assure the quality, relevance, and usefulness of information or its

context for decision-makers and other users by (1) identifying and prioritizing

emerging trends and market needs for assurance, and (2) developing related

assurance methodology guidance and tools as needed. ASEC achieves its

mission by:

providing guidance and leadership in identifying and prioritizing

signicant emerging assurance trends and market needs while engaging

users, preparers, and inuencers toward action;

developing assurance guidance by creating suitable criteria when

necessary, and/or performance guidance, as appropriate;

communicating new assurance methodologies, guidance, and

opportunities to our members and the profession on a global basis; and

creating alliances with industry, government, or other specialized groups

to improve CPA access to new assurance opportunities.

For additional information on the AICPA’s Assurance Services Executive

Committee please visit aicpa.org/ASEC.

AICPA Business Reporting, Assurance and Advisory Services Team

The overarching role of the AICPA’s Business Reporting and Assurance &

Advisory Services Team is to provide leadership oversight, direction and

visioning for emerging business reporting and assurance issues and initiatives

that are identied and addressed through input from AICPA members,

committees and staff.

For more information on the Business Reporting, Assurance and Advisory

Services Team initiatives, please visit aicpa.org/AAServices.

CONTINUOUS

AUDIT

AUDIT

ANALYTICS

AUDIT ANALYTICS and CONTINUOUS AUDIT

and

AUDIT

ANALYTICS

AUDIT

CONTIN UOUS

Looking Toward

the Future

17970-344_Audit Analytics_final.indd All Pages 7/9/15 10:14 AM

17970-344

AUDIT

ANALYTICS

CONTINUOUS

AUDIT

and

Looking Toward

the Future

17970-344_Audit Analytics_TitlePage.indd 1 7/9/15 10:16 AM

Notice to Readers

Audit Analytics and Continuous Audit: Looking Toward the Future does not

represent an ofcial position of the American Institute of Certied Public

Accountants, and it is distributed with the understanding that the author

and publisher are not rendering legal, accounting, or other professional

services in the publication. This book is intended to be an overview of the

topics discussed within, and the author has made every attempt to verify

the completeness and accuracy of the information herein. However,

neither the author nor publisher can guarantee the applicability of the

information found herein. If legal advice or other expert assistance is

required, the services of a competent professional should be sought.

Copyright © 2015 by

American Institute of Certied Public Accountants, Inc.

New York, NY 10036-8775

All rights reserved. For information about the procedure for requesting

permission to make copies of any part of this work, please email

written and mailed to the Permissions Department, AICPA, 220 Leigh

Farm Road, Durham, NC 27707-8110.

1234567890SP198765

ISBN: 978-1-94354-608-4

NOTICE TO READERS

This publication has not been approved, disapproved, or otherwise acted

upon by any senior technical committees of, and does not represent an

ofcial position of, the American Institute of Certied Public

Accountants. It is distributed with the understanding that the

contributing authors and editors, and the publisher, are not rendering

legal, accounting, or other professional services in this publication. If

legal advice or other expert assistance is required, the services of a

competent professional should be sought.

iii

TABLE OF CONTENTS

Page

Preface xi

Acknowledgements xiii

Author Biographies xv

Part I Essays

1 Continuous Auditing—A New View 3

Nancy Bumgarner, Miklos A. Vasarhelyi

1. Introduction—Continuous Assurance the Theory 3

1.1 Continuous Process Auditing 4

1.2 Conceptualizing Various Elements of CA 6

1.3 Guidance on Continuous Auditing 13

2. The Elements of Continuous Assurance Revisited 13

2.1 Continuous Auditing Versus Continuous

Monitoring 13

2.2 The Elements of Continuous Audit 17

3. Information Technology and the Auditor 19

3.1 Evolving Database Audit Conceptualization 22

3.2 Incremental Technological Change 23

3.3 The Audit Data Standard 24

4. The New Continuous Audit 26

4.1 Assurance Level 28

4.2 Time Focus 29

4.3 Time Interval 30

4.4 Data Source 31

4.5 Chosen Procedure 32

4.6 Choice of Assertion 33

4.7 Analytic Method 33

4.8 Assurance Entity 35

5. Questions Regarding Some Auditing Concepts

in the Modern Environment 35

5.1 Stochastic Opinion Rendering in a World

of Statistics 36

5.2 New Audit Products 37

5.3 Management, Control, Assurance, and

Other Meta-Processes Confusion of Concepts 38

5.4 Independence 39

v

CONTENTS

Page

1 Continuous Auditing—A New View—continued

5.5 Migration of Functions to Automation 39

5.6 The Audit Ecosystem 42

6. Conclusions 46

6.1 The New CA 47

References 49

2 The Current State of Continuous Auditing and

Continuous Monitoring 53

Paul Eric Byrnes, Brad Ames, Miklos Vasarhelyi

Introduction 53

Current Environment 54

Products and Services 55

Promotion Efforts 56

Skills Required 57

Supplemental Findings 58

Conclusions 59

References 60

Appendix—Continuous Auditing and

Continuous Monitoring in Action 60

Introduction 60

SAP Key Performance Indicator 61

DSAS/Audit Command Language 61

DSAS Database 61

Dashboard Feature 63

3 Evolution of Auditing: From the Traditional Approach

to the Future Audit 71

Paul Eric Byrnes, Abdullah Al-Awadhi, Benita Gullvist, Helen

Brown-Liburd, Ryan Teeter, J. Donald Warren, Miklos Vasarhelyi

Introduction 71

A Brief History of Auditing in the United States 72

The Traditional Audit 76

Automating the Audit 77

The Future Audit 78

Embedded Audit Modules 79

Monitoring and Control Layer 80

Audit Data Warehouse 81

Audit Applications Approach 81

vi

CONTENTS

Page

3 Evolution of Auditing: From the Traditional Approach

to the Future Audit—continued

Other Future Audit Considerations 82

Conclusion 83

References 84

4 Reimagining Auditing in a Wired World 87

Paul Eric Byrnes, Tom Criste, Trevor Stewart, Miklos Vasarhelyi

Overview 87

Introduction: Blue Sky Scenario 88

Using Technology to Transform Auditing 91

Technology Enablers 91

Audit Opportunities 92

More Effective Audit Data Analytics 92

More Assurance 95

Auditing With Big Data 96

Continuous Auditing, Continuous Assurance 97

More Effective Fraud Detection 98

Reducing False Positives 98

Audit Process Re-Engineering: An Example 99

Making It Happen 100

Encouraging Audit Research and Development 100

Providing Guidance and Updating Auditing

Standards 101

Encouraging and Recognizing New Resource Models 101

Blue Sky Scenario Revisited 102

References 102

5 Data Analytics for Financial Statement Audits 105

Trevor R. Stewart

Abstract 105

The Audit Context 105

DA and Generally Accepted Auditing Standards 106

Audit Applications of DA 108

Understanding the Entity, and Risk Assessment 108

Performing Substantive Analytical Procedures 109

Analyzing and Testing Populations of

Detailed Transactions and Balances 110

Considering and Testing for Fraud 111

vii

CONTENTS

Page

5 Data Analytics for Financial Statement Audits—continued

Testing the Operating Effectiveness of

Internal Control 112

Inquiry 112

A Look Ahead: Cognitive Computing in the Age

of Big Data 112

Utilizing Big Data 112

Cognitive Computing 113

Upping Our Game 114

Illustrative Examples 115

Example 1: Simple DA Visualization 115

Example 2: Financial Ratio Peer Analysis 120

Multivariate Ratio Analysis 125

References 128

6 Managing Risk and the Audit Process in a World of

Instantaneous Change 129

Paul Byrnes, Gerard Brennan, Miklos Vasarhelyi, Daehyun Moon,

Satyajeet Ghosh

Abstract 129

Introduction 130

CRMA Architecture—Overview 130

CRMA—General Process 132

CRMA—More Detailed Considerations 133

Risk Identication and Analysis 133

KRI Development and Implementation 134

Auditor Response to Changing Risk Levels 136

Management Response to Changing Risk Levels 137

Hypothetical Illustration of CRMA in Use 138

Systematic Implementation of Risk

Management and Assessment in a Process 139

Conclusion 142

References 142

Part II Case Studies

A Developing Continuous Assurance at Siemens 147

Ann F. Medinets, Jason A. Gross, Gerard (Rod) Brennan

Traditional Internal Audit 148

Continuous Controls Monitoring 148

viii

CONTENTS

Page

B Implementing Continuous Auditing and Continuous

Monitoring in Metcash—Change, Capabilities, and Culture 157

Glen Laslett, Catherine Hardy

Introduction 157

Value Proposition: Identifying the Need and

Addressing the Business Challenge 158

The Importance of Architecture 159

Denitions and Applications of CA/CM in Metcash 161

An Example Application: The Leave

Continuous Monitoring Routine (CMR) 162

Moving Forward—Key Risk Indicators 163

Challenges and Lessons Learned 164

Conclusion 166

References 166

C Increasing Audit Efciency Through Continuous

Branch KPI Monitoring 169

Carlos Elder de Aquino, Eduardo Miyaki, Nilton Sigolo, Miklos A.

Vasarhelyi, Paul E. Byrnes

Abstract 169

Introduction 170

The Process at SAB 170

Potential Enhancements 171

Conclusions 172

References 172

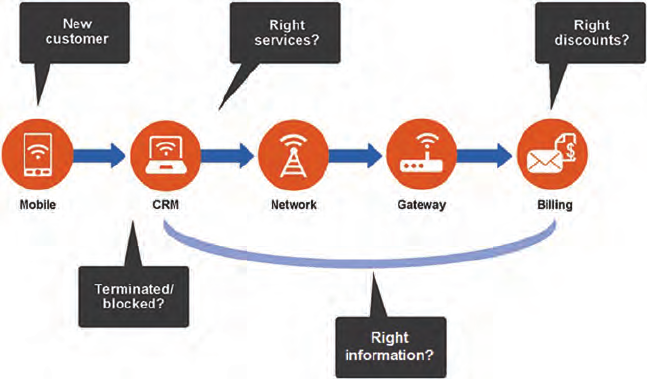

D Implementing Continuous Monitoring at Vodafone Iceland 175

Mar

´

ıa Arth

´

ursd

´

ottir, H

¨

orður M

´

ar J

´

onsson, Sindri Sigurj

´

onsson

Introduction 175

Continuous Monitoring in Vodafone Iceland 176

Revenue Leakage 177

Process of Monthly Financial Closing 178

The Billing Process 179

Fraud Monitoring 181

Customer Relationship Management 181

Culture Change and Enhanced Quality of

Work Flow 182

Challenges and Learning 183

The Future 183

Conclusion 184

ix

PREFACE

The world is evolving and so is the Accounting Profession (the

profession). Recent technological advances offer both challenges and

opportunities that will change the way CPAs operate into the foreseeable

future. In order to stay on top of these new and emerging trends, we need

to align the profession to continue to meet client needs and expectations.

As a step in this direction, the AICPA Assurance Services Executive

Committee (ASEC) Emerging Assurance Technologies Task Force

Continuous Assurance Working Group has developed this book, Audit

Analytics and Continuous Audit: Looking Toward the Future, which focuses

on continuous auditing, continuous control monitoring, and advanced

analytics.

In 1999, the Canadian Institute of Chartered Accountants (CICA) and the

AICPA developed a research report entitled Continuous Auditing.This

report discussed the viability of continuous audits, described a

conceptual framework for conducting them and identied signicant

issues that auditors would likely encounter when performing this type of

work. Audit Analytics and Continuous Audit: Looking Toward the Future,is

intended to be an update to the CICA and AICPA research report,

Continuous Auditing.

Audit Analytics and Continuous Audit: Looking Toward the Future is a

compendium of essays written by different subject matter experts that

expands upon the CICA and AICPA research report to discuss the

following:

r

The theory of modern continuous assurance

r

The current state of continuous auditing and continuous

monitoring

r

The evolution of auditing and what the future could look like

r

Audit analytics

r

Continuous risk monitoring techniques

The book also includes detailed examples and case studies of companies

today that have implemented elements of continuous auditing and

continuous control monitoring into their day-to-day operations.

xi

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Each author brings unique perspectives and insights to each of the essays

included within this book. The authors are made up of individuals in

public accounting, business and industry, as well as academia. Each

author shares a clear vision of the future, and is dedicated to the

advancement of the profession.

xii

ACKNOWLEDGEMENTS

AICPA Assurance Services Executive Committee

Robert Dohrer, Chair

Dorsey Baskin

Bradley Beasley

Greg Bedard

Nancy Bumgarner

Chris Halterman

Charles E. Harris

Don Kluthe

Chris Kradjan

Michael Ptasienski

Beth A. Schneider

Miklos Vasarhelyi

Deetra B. Watson

Don Pallais (Observer)

AICPA Staff

Amy Pawlicki

Director, Business Reporting, Assurance & Advisory Services

Dorothy McQuilken

Manager, Business Reporting, Assurance & Advisory Services

Rachelle Drummond, CPA

Technical Manager, AICPA Peer Review Program

Tanya Hale, CPA

Technical Manager, Business Reporting, Assurance & Advisory Services

xiii

AUTHOR BIOGRAPHIES

Abdullah Alawadhi, PhD

Assistant Professor, Kuwait University

Abdullah Alawadhi is an assistant professor in the College of Business

Administration (CBA) at Kuwait University. He received his PhD from

Rutgers University in 2015. His research interests include data

visualization, audit analytics and big data. For four years he worked at

the Continuous Auditing and Reporting Laboratory (CAR Lab) at

Rutgers University, conducting many research oriented projects.

Abdullah obtained his bachelor degree, majoring in Accounting, from

Kuwait University in 2008. In 2011, he graduated from the University of

Pittsburgh, Katz Business School, and obtained his Master of Science

degree in Accounting. Abdullah presented in several conferences,

including the 28th World Continuous Auditing and Reporting

Symposium (28WCARS) and the American Accounting Association

(AAA) 2014 Mid-Atlantic Region Meeting. In addition, he has several

working papers on the area of audit analytics and data visualization.

Brad Ames, CPA, CISA, CRMA

Director, Internal Audit, Hewlett-Packard

Company

Brad Ames’s role involves close collaboration with Hewlett-Packard’s

governance groups, compliance functions, customers and external

auditors in order to gain an ongoing view of emerging risk

enterprise-wide. His team is responsible for innovating and deploying

continuous auditing solutions for measuring risk to the business and

shortening the time to management action.

Brad is an active CPA, certied information systems auditor (CISA), and

holds a Certication in Risk Management Assurance

®

(CRMA

®

). He has

a bachelor of science from LeTourneau University and is a member of

the AICPA and Institute of Internal Auditor’s Professional Issues

Committee.

xv

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Carlos Elder Maciel de Aquino

Statutory Director, Diagnotics of America S/A

Carlos Elder Maciel de Aquino is currently statutory director at

Diagnostics of America S/A and is currently responsible for the areas of

accounting, receivables, accounts payable and corporate registration. He

was a partner at KPMG and previously worked at institutions such as

Ita

´

u Unibanco and Unibanco, where he held positions such as director of

internal auditing, executive director of leasing and managing director of

complementary social securitie. He was also the sector director of

Febraban’s internal auditing department, was a member of Redecard’s,

Tecban’s and Interbanco’s (Paraguay) auditing committees. He earned a

degree in accounting from UFPE, a graduate degree in Financial

Administration from FESP-PE and in Economic Engineering from

Universidade Cat

´

olica de Pernanbuco (UNICAP-PE). He has an

Executive MBA in Financing from Instituto Brasileiro de Mercado de

Capitais (IBMEC) and a Controller MBA from Universidade de S

˜

ao Paulo

(USP) and is an auditing course professor for the MBA in Internal

Auditing at Fundac¸

˜

ao Instituto de Pesquisas Cont

´

abeis, Atuariais e

Financeiras (FIPECAFI).

Mar

´

ıa Arth

´

ursd

´

ottir

Head of Financial Planning and Analysis,

Vodafone Iceland

Mar

´

ıa Arth

´

ursd

´

ottir is currently a part-time student at Reykjavik

University in Management Accounting and Business Intelligence (MABI).

She graduated from University of Iceland in Finance, Cand.Oecon, 1996.

Mar

´

ıa has been employed at Vodafone Iceland since 2006 and has

extensive experience in management accounting, business intelligence,

revenue assurance, continuous monitoring, planning and analysis. She

recently introduced and implemented rolling forecasting and Beyond

Budgeting in Vodafone Iceland.

Gerard (Rod) Brennan, CFE, PhD

NA Risk & Internal Control Ofcer, Siemens Corp.

Rod Brennan is a practitioner, frequent speaker, and published researcher

on the topic of continuous auditing and monitoring. He is currently NA

risk & internal control ofcer for Siemens and an adjunct professor in the

Rutgers University MBA program teaching Advanced Auditing and Info

Technology.

xvi

AUTHOR BIOGRAPHIES

He is a passionate advocate of using technology to audit and monitor and

is working with researchers from around the world to develop a

continuous auditing and monitoring culture and technology for Siemens.

Rod successfully defended his PhD thesis The Use of Intelligent Software to

Enable Continuous Auditing. The research work included the design and

development of a proof of concept ERP continuous auditing software

model (using SAP) incorporating some of the latest continuous auditing

research concepts. The model was co-developed with Rutgers

University’s Continuous Auditing Research Laboratory (CAR Lab)—a

leading continuous auditing research group.

Rod has been actively involved in the design and implementation of

automated auditing and monitoring solutions using a variety of software

applications and worked on a centralized risk and internal control

solution for Siemens. Siemens operates in diverse business sectors

throughout the world in more than 175 countries.

Helen L. Brown-Liburd, PhD, CPA

Assistant Professor, Rutgers University

Helen L. Brown-Liburd received her PhD from the University of

Wisconsin-Madison and a bachelor of business administration in

accounting from Baruch College. Her research focuses on issues and

factors that inuence auditors’ judgment and decision making related to

nancial reporting. She has published in Auditing: A Journal of Practice and

Theory, Accounting Horizons, Journal of Business Ethics,andIssues in

Accounting Education. Her teaching experience includes auditing, AIS,

and nancial accounting.

Helen has more than 16 years of experience in such diverse areas as

auditing, nancial and operating reporting, and analysis and project

management. She has worked for Bristol-Myers Squibb (BMS) as a

manager on several company-wide teams established to evaluate and

redesign major company-wide processes and she also served as an

internal audit manager responsible for supervising and monitoring

worldwide audits. She also worked for Pepsi Cola Company as manager

of special projects where she researched, developed, and implemented

accounting policies and procedures and performed nancial reporting for

acquisitions. She began her career in public accounting as a staff auditor

for Main Hurdman (now KPMG) and later moved to Arthur Young (now

EY) where she was promoted to audit manager.

Nancy Bumgarner, CPA

Partner, KPMG

Nancy Bumgarner is an audit partner with KPMG and has served in a

number of national, international, and global roles over her career. She is

xvii

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

currently in KPMG’s Department of Professional Practice in the audit

technical group and has worked in the Houston, Sydney, Tulsa, and

Oklahoma City ofces and completed a rotation to KPMG’s Global

Services Centre where she developed new and innovative technologies

and audit methodology that facilitate effective and efcient audits in

KPMG member rms around the world. While in the global role, Nancy

created a new electronic audit tool that harnessed data and analytics with

advanced modeling and algorithms that rene risk assessment and audit

approaches.

While in Australia, Nancy took a leading role assisting international

teams and clients with IFRS and U.S. GAAP differences, U.S. auditing

standards, nancial reporting, and SEC matters. Nancy is a frequent

speaker and panelist at various technical, diversity, and rm-sponsored

meetings. Nancy is a member of KPMG’s Women’s Advisory Board and

KPMG’s Partner Insight Committee on People.

Nancy is a member of the AICPA Assurance Services Executive

Committee and serves on its Continuous Assurance Working Group.

Paul Byrnes, CMA

PhD Student, Rutgers University

Paul Byrnes has an advanced degree in accounting and four-year degrees

in accounting, management, and psychology. In addition, he is a

Certied Management Accountant with about 15 years of relevant work

experience in both the accounting and management elds.

Thomas R. Criste, CPA

Retired Partner, Deloitte & Touche LLP

Tom Criste recently retired as a partner with Deloitte & Touche LLP, with

more than 30 years of experience in nancial and IT audit, risk

management, and internal controls. He served many of the rm’s largest

multinational clients in a number of industries, including automotive,

aerospace, consumer goods, and technology. He also served as the rst

chief learning ofcer for Deloitte & Touche LLP, the audit and assurance

rm of Deloitte, where he led a successful effort to establish Deloitte

University, one of the largest privately-owned learning centers in North

America.

Tom is currently a member of the accounting faculty at the Ross School of

Business of the University of Michigan in Ann Arbor, MI, with a focus on

accounting information systems and auditing. He is also on the Advisory

Board of Rutgers’ Continuous Auditing and Reporting Laboratory (CAR

Lab). He currently serves on an audit data analytics task force of the

xviii

AUTHOR BIOGRAPHIES

AICPA Assurance Services Executive Committee (ASEC) as well as the

continuous assurance working group.

Satyajeet Ghosh, MS, MSE, MBA, CIA, CISA, CFE

SVP, General Auditor and Risk Management, CA

Technologies, NY

Satyajeet (Saty) Ghosh joined CA Technologies in January of 2011 as the

general auditor responsible for assurance, process simplication,

Sarbanes-Oxley (SOX) compliance, and enterprise risk management.

Prior to joining CA, Satyajeet held numerous management and executive

roles in risk management, software development, technology capital

management, business transformation, and mergers and acquisitions in

various industry verticals. He has worked at AT&T Bell Labs, Dun &

Bradstreet, IDT Corporation, Telcordia, Fortent and United Engineers. He

is currently on the Advisory Board of CAR Lab and Senior Fellow at

Rutgers Graduate School of Business, and was a lecturer at numerous

universities. His current interests include predictive analytics, controls

monitoring, and risk maturity models.

Satyajeet holds an MBA from Columbia Business School and graduate

degrees in computer science and engineering from Drexel University and

the University of Pennsylvania, respectively, and an under-graduate

degree in engineering from the Indian Institute of Technology, Kanpur

(India). He is also a current and past member of various professional

organizations that include IIA, ISACA, ACFE, and IEEE.

Jason A. Gross, CPA, CIA, CFE, CISA, ACDA

Vice President, Controls Management, Siemens

Financial Services, Inc.

Jason A. Gross is responsible for ensuring an effective and efcient

internal control framework, leveraging his seven years of experience as

Siemens’ vice president, internal audit. In this capacity, Jason and his

department focus on the design, implementation, and monitoring of

controls via the continuous controls monitoring (CCM) program as well

as the management and oversight of various control programs, including

the SOX program. Prior to joining Siemens Financial Services, Inc. in

2002, Jason had ve years of internal audit experience with AT&T

managing internal audit activity of various business units and four years

of public accounting experience at the CPA rm of Weiser LLP.

Jason is also an experienced speaker on SOX and internal controls and

has presented on several occasions for the Equipment Leasing and

Finance Association (ELFA), MIS Training Institute, the Bank

xix

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Administration Institute (BAI), and for the Institute of Internal Auditors

(IIA) at several IIA conferences. These IIA conferences included the

General Audit Management (GAM), Financial Services, the International

IIA conference, as well as the 2008 IIA webcast, Continuous Auditing: What

Works Best. Jason has received the distinction of being named to the list of

All-Star speakers for the IIA 2006 All Star Conference. In addition, he has

gained recognition in the industry as a subject matter expert on the topics

of utilization of audit tools including audit management systems, data

analytic tools and methodology, and continuous monitoring and

auditing. Jason was featured in the Best Practices of Highly Successful

Auditors by ACL and has been named to the 2009 100 Most Inuential

People in Finance of Treasury and Risk.

In addition to speaking on the topics of internal controls, SOX, and audit

tools, Jason has also authored articles in the Internal Auditor publication

of the IIA and in the ELT: The Magazine of Equipment Leasing & Finance

publication of the ELFA.

Benita Gullkvist, DSc

Associate Professor, Hanken School of

Economics, Finland

Benita Gullkvist received her DSc degree from Abo Akademi University

in 2005. Her research interests include behavioral, social, and

organizational issues related to accounting, especially within the eld of

accounting information systems. She has recently published in journals

such as European Accounting Review and Critical Perspectives on Accounting

among others. Funding from the Fulbright Center, Finland made it

possible to take part in auditing research at Rutgers Business School, USA

in 2011–2012.

Catherine Hardy, PhD

Senior Lecturer, University of Sydney

Catherine Hardy is a senior lecturer at the University of Sydney Business

School in the Business Information Systems Discipline. Her research

interests focus mainly on the complex and changing relationships

between technical innovation, organizational change and governance,

and accountability systems. Catherine’s current research project is a

case-based study on the adoption, implementation, and evaluation of

continuous auditing and continuous monitoring in Australian

organizations. She has extensive teaching, curriculum development, and

program management experience in a wide range of information systems

subject areas including information governance, information protection

and assurance, accounting information systems, and project

xx

AUTHOR BIOGRAPHIES

management. Prior to joining academia, Catherine was an accountant in

the nancial services industry.

H

¨

orður M

´

ar J

´

onsson

Partner, Expectus

H

¨

orður M

´

ar J

´

onsson is a management consultant at Expectus with more

than 15 years of experience in information technology focusing on

business intelligence, nancial planning, and continuous monitoring.

H

¨

orður’s unique background, combining IT and management

consulting, enabled him to develop a unique continuous monitoring

solution, exMon. H

¨

orður has a B.Sc. in computer science.

Glen Laslett, CA, CIA

Retired, Metcash Ltd.

Glen Laslett has recently retired as group business assurance manager at

Metcash Ltd.

Glen’s areas of business expertise include risk, internal audit, continuous

assurance, and process management. Glen has a particular interest in

continuous monitoring (CM) and, during his 14 years at Metcash,

developed an extensive CM framework that delivered substantial

benets to the business. The resulting CM framework comprises more

than 100 fully automated routines that deliver evidence of potential

control breakdowns and transactional anomalies to the business and

subsequently monitors their remediation. Prior to joining Metcash, Glen

worked in the nancial services and hospitality industries. Glen is a

chartered accountant and a certied internal auditor.

Ann Medinets, PhD

Professor, Rutgers University

Ann Medinets received her MBA and PhD from Rutgers University. She

teaches courses in managerial accounting, intermediate accounting, cost

accounting, and corporate governance at Rutgers. Her research interests

include resource allocation, management information systems, and

shareholder rights.

Daehyun Moon, CPA

PhD Student, Rutgers University

Daehyun Moon is currently a PhD student in accounting information

systems at Rutgers University and teaching accounting courses at

University of La Verne. He earned a bachelor’s degree in accounting from

xxi

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Indiana University Bloomington and an MBA in nance from Indiana

State University. He holds a CPA certicate in Illinois.

Eduardo Hiroyuki Miyaki, CIA, CCSA, CFSA

Managing Director of Internal Auditing, Ita

´

u

Unibanco Holding

Eduardo Hiroyuki Miyaki is currently the managing director of the

Internal Auditing function at Ita

´

u Unibanco Holding, responsible for

auditing investment banking, treasury, corporate, and small to midsized

enterprise operations and its international unities (retail and corporate).

He coordinates all continuous auditing initiatives at the bank. Prior to his

experience as internal auditor, he coordinated the implementation and

managed the Anti-Money Laundering Program at Banco Ita

´

uS.A.

He holds a degree in civil engineering; a specialization in nancial

management at Fundac¸

˜

ao Getulio Vargas; and an MBA in nance and

international business at New York University, Leonard Stern School of

Business, USA. He also holds CIA, CCSA, and CFSA certications.

Nilton Sigolo

Research Fellow, Rutgers Business School

Nilton Sigolo is a fellow at the Rutgers Business School’s CAR Lab and

worked for 35 years at the internal audit of Unibanco and Itau-Unibanco

in Brazil. During the last 13 years, he headed the continuous auditing

department. He participated in the Brazilian’s Bank Association

(FEBRABAN) New Bank Auditing Concepts task force and book in

collaboration with Deloitte. He has published in the Internal Auditor and

has performed recently a set of independent audits of different nature.

Sindri Sigurj

´

onsson

Partner, Expectus

Sindri Sigurj

´

onsson is a management consultant at Expectus. He has

worked with some of the largest companies in Iceland focusing on

strategy, performance management, nancial planning, business

intelligence, and business process re-engineering through the use of CM.

He has more than 15 years’ experience in assisting companies in

streamlining their processes and improving their performance.

Previously he was the director of business development at Shell Iceland,

where he implemented CM, and executive director of production

development at Actavis. Sindri has a M.Sc. in operational research and

B.Sc in industrial engineering.

xxii

AUTHOR BIOGRAPHIES

Trevor R. Stewart, CA, PhD

Retired partner, Deloitte & Touche LLP; Senior

Research Fellow, Rutgers Business School

Born and educated in South Africa, Trevor Stewart joined Deloitte in

Johannesburg, working there and in London before transferring to New

York in the early 1980s. In New York, he served in various national and

global roles until his retirement in 2009 after 38 years with the rm, 31 as

a partner. He is a chartered accountant (South Africa), has a bachelor of

science (honors) degree in mathematics from the University of Cape

Town and, post retirement, completed a PhD at VU University

Amsterdam with a thesis on audit assurance and component materiality

in group audits—work that was also published in The Accounting Review

in a paper with Professor William R. Kinney, Jr.

Trevor started Deloitte’s international audit technology research and

development center in Princeton, NJ, which he led for over a decade. He

developed, with Kenneth W. Stringer, a technique (STAR) that uses

multiple regression and other statistical methods for performing

analytical procedures, together with related software, and co-authored

Statistical Techniques for Analytical Review in Auditing (Wiley, 1996). He

served on the rm’s global audit technical policies and methodologies

committee until his retirement.

Trevor has served on several AICPA committees and task forces,

including the 2008 Audit Sampling Guide task force for which he wrote

the companion technical notes. He currently serves on an Audit Data

Analytics task force of the Assurance Services Executive Committee

(ASEC). He was vice-president, practice, of the Auditing Section of the

American Accounting Association, 2006–2008. He currently serves on the

advisory board of Rutgers’ CAR Lab.

Ryan Teeter, PhD

Professor, University of Pittsburgh

Ryan Teeter teaches accounting information systems at the University of

Pittsburgh. He received his PhD from Rutgers University in New Jersey

and has conducted audit research with Siemens and Procter & Gamble.

He specializes in remote auditing and audit automation.

Miklos A. Vasarhelyi, PhD

Professor, Rutgers University

Miklos A. Vasarhelyi holds a PhD in MIS from UCLA, an MBA from MIT,

and a BS in economics and electrical engineering from the State

xxiii

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

University of Guanabara and Catholic University of Rio de Janeiro.

Professor Vasarhelyi is currently the KPMG Distinguished Professor of

Accounting Information Systems and director of the Rutgers Accounting

Research Center (RARC) CAR Lab. He has published more than 200

journal articles, 20 books, and directed over 30 PhD theses. He is the

editor of the Articial Intelligence in Accounting and Auditing series and the

Journal of Information Systems. Professor Vasarhelyi has taught executive

programs on electronic commerce to many large international

organizations including GE, J&J, Eli Lilly, Baxter, ADL, Volvo, Siemens,

Chase Bank, and AT&T. Professor Vasarhelyi is credited with the original

continuous audit application and as the leading researcher in this eld.

The CAR Lab’s projects include among others Siemens, KPMG, P&G,

AICPA, CA Technologies, and Itau-Unibanco. He was the co-recipient of

the AAA outstanding educator of 2013 and ISACA’s Wasserman award

of 2012.

J. Donald Warren, Jr., PhD

Assistant Professor, University of Hartford

J. Donald Warren, Jr., PhD, is an assistant professor in the Barney School

of Business at the University of Hartford. He previously taught in the

Rutgers Business School and served as the director of the Masters of

Accountancy in Financial Accounting. Professor Warren retired from

PricewaterhouseCoopers LLP after a career of 31 years. He served in

many capacities with PwC, including being responsible for the direction

of the IT audit practice and serving as a national consulting partner on

accounting and auditing matters and the rm’s liaison to the SEC.

Additionally, in that capacity, one of his responsibilities was to review

and interpret the AICPA Code of Professional Conduct which contains

the ethical standards for CPAs. He co-authored PwC’s SEC Manual and

the third edition of the Handbook of IT Auditing. His other work

experience includes the US General Accountability Ofce and FASB. His

research interests include continuous audit methodologies and processes

and their related technologies.

xxiv

PART I

Essays

1

ESSAY 1

Continuous

Auditing—A New

View

Nancy Bumgarner, CPA

Miklos A. Vasarhelyi, PhD

1

1. INTRODUCTION—CONTINUOUS

ASSURANCE THE THEORY

2

This volume is intended as an update on the report Continuous Audit

(also called Red Book) published by the CICA and AICPA in 1999. In that

volume, some basic principles and a vision were presented that served as

a basis for additional guidance work by the Institute of Internal Auditors

(IIA) in 2005 and the Information Systems Audit and Control Association

(ISACA) in 2010. Fifteen years after that 1999 report, this volume presents

a much different state-of-the-art, and this essay proposes an expanded set

of concepts largely adding to Vasarhelyi and Halper (1991) and joining it

with an increasing set of experiences and literature from practice and

academia. The evolution of IT, the emergence of big data, and the

increasing use of analytics have rapidly changed the landscape and

prole of continuous assurance and auditing.

3

Many of the current audit

1

The suggestions and contributions of professors Michael Alles and Mr. Shrikant Despante are

gratefully acknowledged. This essay also substantively beneted from the suggestions of Messrs.

Bob Dohrer, Chris Kradjan, Dorothy McQuilken, and Beth Schneider.

2

The authors are appreciative for advice and guidance from Professor Michael Alles, the com-

ments of Mr. Shrikant Deshpande, and the research assistance of Ms. Qiao Li.

3

In general the eld of assurance incorporates both the traditional audit as well other types of as-

surance such as SysTrust, WebTrust or assurance on cybersecurity. In this essay continuous assurance

is also taken as potentially a larger set of topics than providing traditional auditing services but on a

more frequent basis. On the other hand, the terms continuous audit and continuous auditing are used

interchangeably.

3

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

standards were initially instituted by legislation based on the Securities

Act of 1933 and the Securities Exchange Act of 1934 and progressively

developed into the current, ever-evolving set of generally accepted

auditing standards, or GAAS. This formalization of "generally accepted"

has had an enormous effect on business practices and consequently large

effects on the social ecosystem.

Within this context, in addition to the external verication of nancial

statements, many contexts in need of third-party verication have risen.

Consequently, organizations developed internal audit departments,

consulting rms introduced auditing services, and some of these needs

are being satised on an ad hoc basis mainly by external audit rms.

Vasarhelyi and Alles (2006), in a study for the AICPA’s Enhanced

Business Reporting (EBR) project, characterized the umbrella of

verication services as "assurance," under which falls a set of services

such as the "traditional (external) audit," internal audit, and much of

what we later in this paper call "audit-like services." Several data analytic

and monitoring functions of the expanded set of activities that we hereby

call continuous assurance have dual or multiple functions serving

assurance, management, and other parties. Guidance on materiality,

independence, and required procedures will eventually be needed to

adapt to the new tools as the environment evolves. This essay illustrates

some of these needs.

Groomer and Murthy (1989) and Vasarhelyi and Halper (1991) have

respectively argued for and demonstrated the desirability and possibility

of "closer to the event" assurance processes. This approach, reecting the

evolution of technology to online, real-time systems, has had slow but

progressive adoption both in practice (Vasarhelyi et al, 2012; ACL 2006;

PWC 2006)

4

and in professional guidance (CICA/AICPA, 1999; IIA, 2005;

ISACA, 2010).

1.1 Continuous Process Auditing

Motivating the need for continuous assurance, Vasarhelyi and Halper

(1991) state: "There are some key problems in auditing large database

systems that traditional auditing (level 1) cannot solve. For example,

given that traditional audits are performed only once a year, audit data

may be gathered long after economic events are recorded." To deal with

these problems, the AICPA/CICA’s Red Book (1999) introduced the

current denition of continuous auditing:

A continuous audit is a methodology that enables independent

auditors to provide written assurance on a subject matter, for

which an entity’s management is responsible, using a series of

4

PricewaterhouseCoopers, Internal Audit Survey; Continuous Audit Gains Momentum, 2006.

4

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

auditor’s reports issued virtually simultaneously with, or a short

period of time after, the occurrence of events underlying the

subject matter. (CICA/AICPA, 1999)

Research studies have provided a much broader perspective on how

technology is changing auditing. Alles, Kogan, and Vasarhelyi (2002)

questioned whether there was an economic demand for continuously

provided assurance and suggested that the more likely outcome is audit

on demand. Alles, Brennan, Kogan, and Vasarhelyi (2006) expanded the

scope of the continuous audit by dividing it into continuous control

monitoring (CCM) and continuous data assurance (CDA). It has also

been shown that many internal audit procedures can be automated, thus

saving costs, allowing for more frequent audits and freeing up the audit

staff for tasks that require human judgment (Vasarhelyi, 1983, Vasarhelyi,

1985; Alles, Kogan, and Vasarhelyi, 2002).

In the last decade of the 20th century, many large companies, prompted

in part by the Y2K concern, replaced their legacy IT systems with new

enterprise resource planning (ERP) systems. These ERP systems are

controlled by extensive control settings while data is organized into

relational databases that are composed of complex, multi-dimensional

tables that are "related" to each other for the creation of reports by

common elds. Users, for highly justiable business reasons, are allowed

to override control settings. Consequently, new assurance needs have

emerged due to the ever increasing difculty of direct observation of

(1) control structures, (2) control compliance, and (3) data.

Control Structure

The ubiquitous usage of ERPs diminished concerns with the adequacy of

control structures as the systems are typically based on best of class

implementation and widely used even though each company will

determine how the ERP control structure will be adopted for

company-specic circumstances. Many questions remain, as the actual

control structure does not only involve the ERP systems but also the

entire manual and IT set of processes (that include many elements aside

from the ERP systems) and their integration. Controls can be overridden

or bypassed by the users, or may not exist at the upstream of the process,

and transactions will be received as legitimate.

Control Compliance

Control compliance, on the other hand, became a much larger problem as

established exible and widely applicable control structures often entail a

very large number of controls and for operational reasons these controls

may have to be temporarily re-parameterized. For example, a particular

checking account may be allowed to go over its credit limit for

5

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

operational reasons. The need to monitor and assure control settings and

the nature of overrides generated a new type of audit objective and

process.

Data

Data is in general stored in ERPs, in les for legacy systems, or in more

recent times in large repositories external to the organization that are

called big data (Vasarhelyi, Kogan, and Tuttle; 2015). The access to these

data for observation, monitoring, or mass retrieval requires the auditor’s

knowledge and extensive use of software tools. This access is not only

technically challenging but also organizationally difcult (Vasarhelyi,

Romero, Kuenkaikaew, and Littley; 2012).

1.2 Conceptualizing Various Elements of CA

Table 1-1 illustrates the uses, purposes, and approach of the expanded

model of continuous assurance differentiating between internal and

external usage and further differentiating between diagnostic, predictive,

and historic usage.

Table 1-1: Users, Purpose, and Approach of the Elements of Continuous

Assurance

Data

assurance

Controls Compliance

Risk

monitoring

and

assessment

Operations

(monitoring)

Who uses

•

Management

X X X X X

•

Audit (internal

or external)

X X X

•

Investors

X

•

Regulators

X X X

Purpose

•

Diagnostic

X X X X

•

Predictive

X X

•

Historic

X X X X X

Primarily performed by

•

Automation

X X X X X

•

Manual

X X X

Each of these elements is discussed in the following sections.

Continuous assurance (CA) has the potential to benet a wide variety of

users. Management will be interested in all aspects, from data assurance

6

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

to monitoring operations. Investors may primarily be interested in data

assurance though, depending on the industry, compliance and risk

monitoring may be equally as important.

CA is well suited for historic analyses, particularly given the speed with

which CA provides information on attributes such as accuracy. Auditors

that provide assurance on historic information will likely be primarily

interested in the ability of CA to be used for such purpose. Access to

sophisticated ERPs and complex data sets create an opportunity for CA

to be used for diagnostic purposes. Where an error or anomaly has been

identied, CA may perform a retrospective diagnostic of the

situation—providing insight and analyses to management.

Diagnostically, CA could also be tied to effectively assessing operational

and structural strengths and weaknesses of an organization—enabling

strategic decisions to be made in a timely manner and with sufcient

context.

Automation is an essential element to CA, though manual involvement

remains important particularly in situations where extensive judgment is

required and where anomalies, exceptions, and outliers are identied.

Continuous Data Audit CDA

Vasarhelyi and Halper called the process of monitoring and constantly

assuring AT&T’s RCAM system continuous audit. The architecture of the

system described in gure 1-1 shows data being (1) extracted from

pre-existing reports, (2) sent to the business units through the remote job

entry network, (3) transferred to an email system, and (4) extracted

through individual text mining programs. This technique, analogous to

what is called today "screen scrapping," was chosen to avoid interference

in the long and complex system process development protocol. All

information was collected from existing reports and placed in a relational

database. This database drove hypertext graphs that were given to

auditors to interact with the system. The several layers of the RCAM

system were represented as owcharts respecting the internal auditors’

documentation practices and experience in data analysis. Many of the

analytics impounded into the system were drawn from knowledge

engineering (Halper, Snively, and Vasarhelyi, 1989) internal auditors and

capturing the calculations they made with paper reports. The

formalization of these processes allowed for their repetition at repeated

frequency, and often reliance on these tests up to the moment that alerts

were generated. Although internal auditors started relying on these

exception reports, they also requested that the source reports be retained

mainly for their traditional audit reports.

7

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Figure 1-1: CPAS as Continuous Data Audit (from Vasarhelyi & Halper,

1991)

Although the idea of a continuous audit was conceptualized initially as a

data monitoring and exception system (Vasarhelyi, 1996), its concept was

expanded in an implementation at Siemens (Alles et al, 2006) as a

reaction to Sarbanes Oxley and the need to issue opinions on the

adequacy of internal controls. This expansion was entitled continuous

control monitoring (CCM).

Continuous Control Monitoring (CCM)

Siemens had over 150 instances of SAP that were reviewed by technical

experts using that narrow guidance of a standardized set of audit action

sheets. These were a formalization of the audit plan to review controls

and features of a particular SAP implementation and were adapted to

each audit instance. Alles et al. (2006) developed a proof of concept tool

where a baseline of control settings would be compared with the actual

congurable control setting every night and auditors would be alerted of

variations. Teeter (2014) extended the original work examining the

potential for automation of not only the deterministic settings of SAP but

a wider set of controls and parameters in the SAP system.

The...essay...investigates the implementation of a comprehensive

continuous controls monitoring (CCM) platform for evaluating

8

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

internal controls within a highly formalized and well-controlled

enterprise resource planning environment. Utilizing the IT audit

plan as a template, auditor expertise as a guide, and manual audit

output as a validation tool, this eld study examines the process of

audit formalization and implementation of CCM at a software

division of a large, multinational corporation. (Teeter, 2014)

The results of the applied effort

5

indicated that 62 percent of the controls

arguably could be formalized, creating the possibility of a control

certication or assurance layer on top of the SAP instance. Conceptually,

this layer could be a part of SAP or an add-on, could be generic in

conguration or tailored to the instance, and could be re-thought as a

way to increase audit coverage as the original audit plan was applied in

an 18- to 24-month cycle, and under this design this layer would be

executed every day. Furthermore, the audit plan contained many

qualitative questions such as "Is there documentation for XYZ system?"

Elder et al. (2013) narrate a continuous monitoring effort at a large South

American bank in which internal audit monitored 18 different key

performance indicators (KPIs) for over 1400 branches of a bank. Daily

extracts of variances were obtained and, on a selective basis, followed up

by emails to the regional managers for the branches. These KPIs looked

to control overrides such as credit above allowable level or reversal of

certain types of transactions.

These examples illustrate (1) situations where auditors were in positions

of control over operational controls, which could result in a conict to the

auditor’s objectivity or independence and (2) that technology has

changed the needs, capabilities, and roles of the assurance function. As

suggested earlier, a more exible set of conceptualizations must evolve,

concerning auditor independence in particular. These examples are

focused on internal auditors, but a similar monitoring role could be

developed for external auditors and an ongoing monitoring opinion

could potentially be issued as a new CPA product.

Figure 1-2 describes the vision developed for multi-instances of ERPs and

an analytic engine supporting a set of functions. This view, however,

could be immediately after the event based on the two experiences

described above and would be an ex-post-facto overnight process, which

we would describe as retroactive close to the event meta-control or

assurance process.

5

Private notes Teeter, R.A., Warren, J.D., Brennan, R., and Vasarhelyi, M.A. 2007.

9

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Figure 1-2: Pilot Continuous Monitoring of Business Processes at

Siemens, Rutgers CAR-Lab & Siemens Adding Intelligence (from

Alles et al, 2006)

Incorporating the concept of CCM into the original CA conceptualization

led to the renaming of the original CA to Continuous Data Audit (CDA)

where CA = CDA + CCM.

Continuous Risk Monitoring and Assessment (CRMA)

Vasarhelyi, Alles, and Williams (2010) suggested the addition of

Continuous Risk Monitoring and Assessment (CRMA) into the CA

schema where: CA = CDA + CCM + CRMA. CRMA is discussed in more

detail in essay 6, "Managing Risk and the Audit Process in a World of

Instantaneous Change" of this book. The essence of the CRMA concept is

displayed in gure 1-3 where risks are divided into three areas: (1)

operational, (2) environmental, and (3) black swans (Taleb, 2010). Black

swans are very remote risks with strong consequences that could arise, as

Taleb predicted the crisis of 2008. Risks are chosen judgmentally by the

audit team or management, and key risk indicators (KRIs) are associated

with the most important risks in each of the categories. The same basic

variance and acceptable variance model can be adapted to detecting

signicant changes of risk. The model can be parameterized at the initial

10

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

audit planning stage with heuristic or otherwise developed weights and

optimization procedures applied to determine an audit program. When

substantive changes in risk are perceived by the risk monitoring

procedures, the algorithm can be rerun, but management must also be

informed and joint action by assurance and management must follow.

This risk variance activation procedure also confounds the classical audit

theory, as many organizations have independent risk management areas

often broken down by type of risk or product. New conceptualization of

coordinated auditing or coordinated management, audit, and risk areas

must follow.

Figure 1-3: Structure for CRMA Effort

Continuous Compliance Monitoring

Very closely related to risk evaluation, and closely linked to the

increasingly regulated modern business world, is the area of compliance.

Although much of the traditional world of compliance is qualitative, it is

progressively being implemented by automated systems. Frequent

upgrades in ERPs, for example, at banks and insurance companies reect

the increased regulation, the need to reduce costs of compliance, and the

need to obey hundreds of regulations. In this essay, the development of a

compliance monitoring (COMO) approach to complement CA is

proposed.

11

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

The COMO approach would create comprehensive taxonomies of

compliance issues and progressive updates for regulatory changes

acknowledged by geography, area of activity, and the nature of

compliance rule (qualitative, quantitative, mixed, or other). It would

restate the CA equation to:

CA = CDA + CCM + CRMA + COMO

The integration of these views into a closer-to-the-event framework has

the advantage of improving assurance coordination, working towards

avoiding task repetition, and the potential usage of a conceptual and IT

platform. Table 1-2 illustrates one type of (quantitative) compliance

objective in relation to the topic of money laundering. As a caveat, if the

above functions are united into a joint conceptual view and one platform

implementation, the risks of their failure are much larger as a certain

degree of redundancy decreases risk but also increases costs.

Table 1-2: Example of Compliance Monitoring Table

Anti-money laundering

1. Compliance Topic: AML

2. Obligation or Compliance issue (for example, not to let over $10,000

through bank teller deposit without regulatory reporting)

3. Method of compliance: All transactions for a given deposit rule have

been captured and reported

4. Frequency capture daily, report quarterly

5. Importance: H M L HIGH

Compliance requirements can be largely qualitative, interpretive

especially of legal, regulatory requirements, but its fullment (for

example, fullment of the obligations) needs a degree of formalization in

measurement of supporting information, monitoring, and reporting.

Compliance fullment data is processed in the complex corporate legacy,

ERP, and other sources of big data where the company operates.

Traditional methods of extracting and evaluating an assertion of

fullment of compliance obligations to stakeholders and regulators are

anachronistic. Therefore the argument for continuous auditing applies to

compliance. Compliance management needs to be design-driven (for

example, formal structure for requirement denition, data capture, single

view of data bases, data visualization and interpretation from analytics

based representation). Continuous assurance and continuous compliance

assurance are complementary and can leverage many common design,

analytics, and technology components. Their integration is aimed to

12

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

alleviate the multiple problems generated by the proliferation of

audit-like organizations.

1.3 Guidance on Continuous Auditing

The rst guidance on continuous auditing was published jointly by the

CICA and AICPA (1999) and is often called the Red Book. This current

volume attempts to update the Red Book along several dimensions. Since

the publication of the Red Book, the Institute of Internal Auditors

published its GTAG 3 Continuous Auditing: Implications for Assurance,

Monitoring, and Risk Assessment (IIA, 2005) and ISACA its IT Audit and

Assurance Guidelines, G42, Continuous Assurance, (2010). In 2010, the

Australian Institute of Chartered Accountants also published its

Continuous Assurance for the Now Economy.

Leveraging this statutory work, continuous auditing literature reviews

(Brown et al, 2007; Chiu, Liu, & Vasarhelyi, 2014), and literature from

practice, this essay will summarize some basic theory postulates for

continuous assurance. Assurance, for purposes of this essay, is dened as

an umbrella of services that include the traditional audit and other services of a

similar or complementary nature that are emerging or being facilitated by new

technologies and business needs. (Vasarhelyi & Alles, 2006)

Considering the new assurance needs in control structure, control

compliance, data, and the existing guidance on continuous auditing, a

reconsideration and expansion of the elements in the concepts of

continuous assurance is needed.

2. THE ELEMENTS OF CONTINUOUS

ASSURANCE REVISITED

The advent of new information and analytic technologies has brought

about new products as well as new ways to perform business processes.

Since the early years of continuous auditing, business has substantially

evolved the continuous monitoring processes of production into many

other areas of activity including accounting and nance.

2.1 Continuous Auditing Versus Continuous

Monitoring

Considerable thought has been given to the problem of overlap between

management and assurance processes when they progress in the

automation route. KPMG (Littley and Costello, 2012) described it in

operational terms, as shown in table 1-3. Another approach would be to

13

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

consider some new type of conceptualization based on the new

economics of information, control, and risk.

Table 1-3: CA Versus CM

Continuous Auditing

Performed by Internal Audit

Continuous Monitoring

Responsibility of Management

•

Gain audit evidence more

effectively and efciently

•

Reactmoretimelytobusiness

risks

•

Leverage technology to perform

more efcient internal audits

•

Focus audits more specically

•

Help monitor compliance with

policies, procedures, and

regulations

•

Improve governance—aligning

business/compliance risk to

internal controls and remediation

•

Improve transparency and react

more timely to make better

day-to-day decisions

•

Strive to reduce cost of controls

and cost of testing/monitoring

•

Leverage technology to create

efciencies and opportunities for

performance improvements

Littley and Costello (2012), as shown in table 1-1 and the AT&T Bell

Laboratories development of Continuous Process Audit System (CPAS)

(Vasarhelyi & Halper, 1991) in parallel to management’s Prometheus

system (table 4) show a substantive overlap of management and

assurance analytics and the potential of the usage of similar systems to

support infrastructure. IBM’s

6

internal audit approach was to

commission three monitoring systems for auditees and progressively

obtain their agreement to use the system for monitoring by management.

Traditional audit thinking argues that if the auditor acts as a "monitorer,"

in one sense, he or she becomes part of the control system and loses

independence. On the other hand, the traditional audit can be viewed as

a form of tertiary control acting both as a deterrent as well as an

after-the-fact detective control. The progressively increasing set of layers

between the auditor and the data, as well as the massive nature of data

being used by large corporations, forces the existence of monitoring and

reporting layers, not to mention ERP software, web interfaces, legacy

systems, and outsourced processes.

Vasarhelyi & Halper (1991) initially developed the CPAS project aimed at

creating a meta-understanding of the system being audited and making

this system auditor-monitored. It became clear after a certain amount of

time that similar monitoring insight and analytics would be also of

interest to management and of benet in the utilization of the system

being monitored. Consequently AT&T developed the Prometheus system

(Vasarhelyi, Halper, & Esawa, 1995), which used the same technological

undercarriage of CPAS but with some unique analytics for both

6

As described in annual presentations at the World Continuous Auditing Symposium in Newark

(2011, 2012), that can be seen in http://raw.rutgers.edu/

14

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

management and auditing, as well as a larger common base of analytics

and monitoring controls.

Table 1-4 illustrates a series of reports, screens, and data monitoring

procedures based on AT&T’s RCAM system where there is examination

of data at multiple levels. While analytic 1 examines the overall

completion rate of the billing process, analytic 2 works at a much lower

and earlier level examining the data collected by the switches. Some

analytics are only provided to the audit functions, others are only of

interest to management monitoring, while others are to be supplied to

both. The CPAS conceptualization involved 4 major elements: (1) actuals,

(2) standards (models), (3) analytics and (4) alarms (alerts) in addition to

the method of measurement (direct data access or secondary capture).

Analytics in CPAS were provided in the form of formulae, rules, and, in

most of the instances, with graphic visualization.

Table 1-4: CA and CM at AT&T

7

Analytic

number

Process

CPAS (Continuous

Audit)

Prometheus

(Continuous

Monitoring)

1 Bill Completion

Monitoring

Percentage of bills

generated that were

completed

Percentage of bills

generated that

were completed

2 Calls recorded Long-term count of

calls adjusted for

cycle

Switch billing

integrity

comparisons

3 Bills missing Process integrity

reconciliation

Process integrity

reconciliation

4 Job sequencing in the

data center

Examination of

CA-7 and CA-11

reports

5 Discrimination of

reasons bills not printed

Staged counts

6 Specic Bill content

examination

Bill

images—content

extraction

summaries

For accuracy

verication

7 Bill sequencing controls For ctitious bill

detection

For production

monitoring

8 Continuity Equations For predictive

auditing (Kogan

et al, 2014;

Kuenkaikaew, 2013)

For error

detection and

process

monitoring

7

This table is illustrative in nature. It is loosely based on the actual experience of the monitoring

and assurance of the RCAM system in the 1986–1991 period.

15

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Kogan et al. (2014) applied the concept of continuity equations

expanding the original suggestion of Vasarhelyi and Halper (1991)

including the following:

r

Distinguishing exceptions from anomalies

r

Introducing time-lagged process measurements that reected

better the actual information ow in the system

r

Focusing on transaction-level monitoring with clarication of the

different levels of activities

r

Introducing the concept of automatic transaction correction into

the audit literature

Recent continuous auditing literature (Chiu, Liu, and Vasarhelyi, 2014)

has tried to improve the quality of the models that serve as the basic

elements of comparison for exception detection.

Table 1-5 compares and expands the original conceptualization of the

CPAS effort (Vasarhelyi & Halper, 1991; Halper, Snively, & Vasarhelyi

1988; Vasarhelyi, Halper & Esawa, 1995) with several research efforts

performed over the years.

Table 1-5: Expanding Conceptualization in CA/CM

8

Vasarhelyi & Halper

(1991),

Red Book (1999)

Expanded

Conceptualization

(1999–2014)

Notes

CPAS/Prometheus

effort

Several corporate

experimental

experiences

Work with P&G,

Siemens, Itau

Unibanco, and so

forth

Measuring Metrics Extractions from

many different

systems and

drawing from the

Big Data

environment

Great potential for

increased

validation of values

including database

to database

conrmations

Creating a

model

Standards Of comparison

Of variance

8

Highlighted items are expansions to the Vasarhelyi and Halper (1991) initial conceptualization.

16

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

Table 1-5: Expanding Conceptualization in CA/CM—continued

Vasarhelyi & Halper

(1991),

Red Book (1999)

Expanded

Conceptualization

(1999-2014)

Notes

Relating Analytics Representational

equations

Continuity

equations

Kogan et al., 2015

Visualization

Clustering and

transaction level

continuity

equations

For automatic fraud

detection and

transaction

correction

Alarms (4 levels)

Measurement Versus

Monitoring

Measurement

(indirect data

acquisition)

Direct data access

Introducing

external

comparative

benchmarks

Probabilistic data

relationships

Linking corporate

ERP data to big

data in the fringes

Dimension

Data Continuous data

auditing (CDA)

Vasarhelyi &

Halper 1991

Control Continuous Control

Monitoring (CCM)

Vasarhelyi, Halper

& Esawa, 1995;

Alles et al, 2006

Risk Risks (CRMA) Vasarhelyi, Alles, &

Williams, 2010;

Essay 6

Compliance Compliance (CM) Essay 1

2.2 The Elements of Continuous Audit

Vasarhelyi, Alles, and Williams (2010) have argued for the inclusion of

continuous risk monitoring and assessment (CRMA) in the CA schema:

"The audit planning process provides a template for how to make the

Continuous Assurance system dynamic: by formally incorporating into it

a risk assessment system that encompasses assessment of auditor

17

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

perceptions of risks and allocation of audit resources to risky areas of the

audit."

Vasarhelyi, et al. (2012) examined the continuous audit efforts of nine

large organizations. It was noteworthy that organizations had a series of

"audit-like" organizations (ALO) that competed for resources and

presented very different levels of technology use. In its principle 3.5, the

King report (Institute of Directors in Southern Africa, 1994, 2009) in

South Africa states that "The audit committee should ensure that a

combined assurance model is applied to provide a coordinated approach

to all assurance activities." A control and assurance automated

ecosystem can evolve the audit to create a more reliable and efcient

corporation.

All of the interviewed companies have a number of audit-like

organizations which perform assurance-like functions in different

areas. However, some of the audit areas overlap, and the results of

the review are not efciently shared among them as one manager

declared, "Let me start with my administrative boss. He is the director of

risk management for the organization. Underneath is internal audit.

Credit examination and our risk management/Sarbanes-Oxley...there is

another group that does testing that reports to Chief Legal Counsel.

Fraud is handled in our securities group, which is in our service

company. They perform investigations on internal and external

fraud...We do [received feedback], but not as much as we should."

One of the interviewed companies had up to seven ALOs, which resulted

in substantive differences in the quality of reviews, substantial

redundancy, lack of depth in the reviews, and what they called "audit

fatigue" where auditees would not cooperate due to the multiplicity of

assurance efforts. If the companies had continuous audit in stage 4, a full

continuous audit in stage 4, these problems could be eliminated as the

monitoring systems would be centralized and integrated. All ALOs could

share the systems and information, and their works would not overlap.

ALOs in this study included (1) internal audit, (2) compliance, (3) fraud,

(4) SOX, and (5) Basel, in most situations, although several other

nomenclatures and subdivisions existed. (Vasarhelyi et al, 2012).

18

ESSAY 1: CONTINUOUS AUDITING—A NEW VIEW

Figure 1-4: Expanded Scope of CA including Compliance Monitoring:

An evolving continuous auditing framework

The original framework of continuous assurance can be expanded into

four elements: data, control, risk, or compliance. Figure 1-4 expands

Vasarhelyi, Alles, and Williams (2010) components to add an element of

compliance monitoring, expanding the scope of the CA and CM effort.

The same considerations of opacity of the data processing environment

and the difculty of access to its information apply to all elements of the

auditing framework that evolved since the AT&T CPAS effort.

3. INFORMATION TECHNOLOGY AND THE

AUDITOR

Traditional auditing has changed considerably as a result of changes in

IT, including more advanced ERP systems, increasing the use of on-line

transactions with both customers and suppliers, use of the cloud, and the

rapid expansion of data available for use by management and auditors.

The continuously evolving IT landscape leads to a variety of audit

challenges that compound over time, as summarized in table 1-6

(Adapted from Vasarhelyi and Halper, 1991).

19

AUDIT ANALYTICS AND CONTINUOUS AUDIT:LOOKING TOWARD THE FUTURE

Table 1-6: The Evolution of IT and Associated Audit Challenges

(Adapted from Vasarhelyi & Halper, 1991)

9

Phase Period Evolution of IT Examples Audit Challenges

1 1945–1955 Input (I) Output

(O) Processing

(P)

Scientic and

military

applications

Data transcription

Repetitive

processing

2 1955–1965 I, O, P Storage (S) Magnetic tapes

Natural

applications

Data not visually

readable Data that

may be changed

without trace

3 1965–1975 I, O, P, S

Communication

(C )

Time-sharing

systems Disk

storage Expanded

operations support

Access to data

without physical

access

4 1975–1985 I, O, P, S, C

Databases (D)

Integrated

databases Decision

support systems

(decision aides)

Across-area

applications

Different physical

and logical data

layouts New

complexity layer

Decisions

impounded into

software

5 1986–1991 I, O, P, S, C, D

Workstations

(W)

Networks Decision

support systems

(non-expert) Mass

optical storage

Data distributed

among sites Large

quantities of data

Distributed

processing entities