TAX

COMPLIANCE

GUIDELINES

DE 83 Rev. 1 (4-18)

(INTERNET)

CU

DE 83 Rev. 1 (4-18) Page i of iv

(INTERNET)

TABLE OF CONTENTS

CHAPTER

PAGE

NUMBER

1.

INTRODUCTION

Introduction

1

Collection Program Functions

2

Central Operations Functions

3

Field Operations Functions

3

Promote Voluntary Compliance

4

Authority to Enforce Collection

5

Collection Policies

6

Prohibited Collection Activities

7

2.

REPORT DELINQUENCIES

Report Delinquencies

1

Report Delinquencies - Historical

2

Payroll Tax Deposits

3

Quarterly Contribution Return and Report of Wages

Continuation (DE 9C) 3

Quarterly Contribution Return and Report of Wages (DE 9)

5

Quarterly Wage and Withholding Report (DE 6)

6

Annual Reconciliation Statement (DE 7)

7

Quarterly Contribution Return (DE 3)

8

3.

COLLECTION MANAGEMENT

Collection Management

1

Time Frames

2

Reimbursable Accounts

2

4.

CONTACT EMPLOYER

Contact Employer

1

Entity Verification

2

Other Entity Types

6

First Personal Contact

8

Identify the Taxpayer

9

Payment History

9

Phone Contacts

9

Office Meeting

10

Preparation for the Field Call

11

Returning to the Office

11

Collection Letters

12

5. ESCROWS

Escrow

1

Responsibility for Demand and Clearance

3

Sale of a Business

4

Excess Funds

8

Home Equity Loans

8

Surplus Funds

8

Liquor License

9

Mortgage Refinance

9

Personal Property

10

Real Property

11

6. INVOLUNTARY COLLECTION DETERMINATION

Involuntary Collection Determination

1

Type of Involuntary Action

2

7. STATE TAX LIEN/NOTICE OF STATE TAX LIEN

State Tax Lien/Notice of State Tax Lien

1

Employer Notification

2

Required Information

3

Lien Priority

3

Purpose of a State Tax Lien

4

County Lien Fees

4

Secretary of State Filing Fees

4

Lien Extensions

5

Notice of State Tax Lien Identification

5

Lien Releases

6

Erroneous Liens

6

Liens That Are Not Erroneous

7

8. CONTRACTORS STATE LICENSE BOARD

Licensing

1

License Requirements

1

Issued to Correct Entity

1

Valid Time Period

2

Requesting a CSLB Hold 2

Sample of Demand Letter to Contractor

3

9. FARM LABOR CONTRACTORS

Farm Labor Contractors’ Licenses

1

Expiration Dates

1

License Demand Notification

1

Sample of Demand Letter to FLC 2

Sample of Stop Order

3

Page ii of iv DE 83 Rev. 1 (4-18)

(INTERNET)

TABLE OF CONTENTS

CHAPTER

PAGE

NUMBER

DE 83 Rev. 1 (4-18) Page iii of iv

(INTERNET)

TABLE OF CONTENTS

CHAPTER

PAGE

NUMBER

10. INTERAGENCY OFFSETS

Interagency Offsets

1

State Offsets

1

FTB Interagency Intercept Collection Program 2

Multiple PIT Offset Priorities 3

Other State Agencies’ Offsets

3

Security Deposits

4

Federal Levy

4

Federal Offsets

4

Bureau of Fiscal Service Offset Process

5

Priorities for Federal Offset

5

11. INTERIM REPORTING

Interim Reporting

1

Requirements for Interim Reporting

1

Termination of Requirement

2

12. LIQUOR LICENSE HOLD

Liquor License Holds

1

Type of License

1

Liquor License Demands

2

Establish Liability for Liquor License Demand

3

Insufficient Funds in Escrow Pro Rata

4

Disbursement of Money in Escrow

4

Payment Received

4

13. NOTICE OF LEVY

Notice of Levy

1

Issuance

2

Method of Service

2

Results

2

Process Payments

3

14. OFFERS IN COMPROMISE

Offers in Compromise

1

Conditions Required for Consideration

2

Forgiving Amounts of $10,000 or More

3

Case Assignments

3

Approved Applications

3

Denied Applications

4

Rescission

4

Processing a Rescission

4

TABLE OF CONTENTS

CHAPTER

PAGE

NUMBER

15. INSTALLMENT AGREEMENTS

Installment Agreements

1

Types of Agreements

1

Required Documentation and Approval

4

Acceptance

7

Denial

7

Monitoring

7

Default

8

16. ASSIGNMENT FOR BENEFIT OF CREDITORS, RECEIVERSHIP

Assignment for Benefit of Creditors

1

Receivership

1

Notification

2

Duties and Responsibilities

2

EDD Claims for Assignments and Receiverships 3

17. PROBATE

Probate

1

Types of Estate

2

Authority of Personal Representative

2

Responsibilities of Administrator or Executor

2

Sources of Information

3

When to File the Claim

3

Collection Staff Processing

4

18. DISCHARGE FROM ACCOUNTABILITY

Discharge From Accountability

1

Application for Discharge From Accountability

1

Authorization to Forego Collection of State Debt

2

Page iv of iv DE 83 Rev. 1 (4-18)

(INTERNET)

(INTERNET)

CHAPTER 1 INTRODUCTION

INTRODUCTION The Employment Development Department (EDD) administers

the Unemployment Insurance (UI) and Disability Insurance (DI)

programs for the S tate of California. The E DD Tax Branch

collects contributions for UI, DI, and the Employment Training

Tax (ETT). The contributions are used to fund the UI, DI, and

employment training programs. These programs provide

financial assistance to individuals who:

• Become unemployed through no fault of their own.

• Are in need of occupational retraining to help them return to

the workforce.

• Are too ill or injured to work due to non-work related causes.

Tax Branch collects California Personal Income Tax (PIT) that

employers withhold from their employees' wages. When these

funds are remitted to the EDD, they are transferred to the

Franchise Tax Board (FTB). In addition, Tax Branch has

contracted with the Department of Industrial Relations (DIR) to

collect various fees and penalties.

Collection Division (CD), a division within Tax Branch, is

responsible for administering the employment tax and benefit

overpayment collection programs. The employment tax

programs are designed to encourage voluntary compliance by

employers, claimants, and their representatives. Involuntary

collection action may be necessary to reach the goal of full

compliance.

The principal mission of CD is to maximize accounts receivable

collections and promote voluntary compliance. CD has

programs that qualifying employers may use if the full liability

cannot be paid. Programs include offers in compromise and

installment programs. CD may use statutory involuntary

collection action to collect contributions from employers and

responsible persons. CD secures delinquent tax returns to

ensure timely and prompt resolution of claims for benefits and

collects liabilities that are owed to the EDD.

DE 83 Rev. 1 (4-18) Page 1 of 9

CHAPTER 1 INTRODUCTION

INTRODUCTION

(cont

’d.)

CD must responsibly serve the needs of the people of California

in an efficient and effective manner. CD strives to incorporate a

balanced approach by providing quality customer service while

posting unfiled tax returns to the system and collecting final

liabilities.

CD is comprised of three major operations:

• Central Operations (CO)

• Field Operations (FO)

• Administration Section

COLLECTION

PROGRAM

FUNCTIONS

CO and FO staff conducts tax collection activities on assigned

and unassigned delinquent accounts that include:

• Working with employers, internal customers, and other

governmental agencies to collect and, in some instances,

resolve tax liabilities and delinquencies.

• Ensure long-term compliance with the California

Unemployment Insurance Code (CUIC).

• These activities include:

• Initiating appropriate action for the timely and efficient

resolution of delinquent returns and taxes.

• Monitoring installment agreements.

Page 2 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 1 INTRODUCTION

CENTRAL

OPERATIONS

FUNCTIONS

CO provides the following essential advisory and/or support

services to:

• Provide customer service and account resolution to

employers and claimants who contact the EDD because

they received delinquency notification(s) and/or collection

activities were commenced against the employer and/or

responsible person.

• Process bankruptcy and probate claims.

• Process Notices of State Tax Lien, including subordination

and partial releases.

• Process liquor and contractor license holds.

• Assist with complex legal problems and refer complex

cases to the Office of the Attorney General for advice and in

some cases counsel.

• Administer the Offer in Compromise (OIC) program.

• Facilitate Interagency Intercepts.

• Collect UI and DI benefit overpayments.

• Collect various DIR fees and penalties.

• Attend tax hearings on behalf of the EDD.

FIELD

OPERATIONS

FUNCTIONS

FO conducts collection activities on the assigned delinquent

tax accounts that may require collection actions and contact

with employers, representatives, and responsible persons for

resolution.

A field investigation is often necessary in order to resolve a

delinquent account. Field staff are permitted to conduct

on-site meetings with employers at their places of business.

Field staff may also conduct inspections to evaluate business

activities and properties.

Page 3 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 1 INTRODUCTION

FIELD

OPERATIONS

FUNCTIONS

(cont’d.)

FO also provides the following functions:

• Attend tax hearings on behalf of the EDD.

• Initiate holds on liquor, farm labor, and contractor licenses.

• Initiate compliance complaints and citations.

• Initiate the issuance of warrants for the seizure and sale of

real and personal property.

• Meet with delinquent taxpayers to secure payment of

amounts due, review financial statements, and determine

ability to pay.

• Receive and

respond

to initial

contacts that

request

subordination of liens.

• Initiate collection actions.

PROMOTE

VOLUNTARY

COMPLIANCE

To improve service to employers, maintain good customer

service, and encourage voluntary compliance with the CUIC, Tax

Branch provides the following:

• California Employer Newsletter

• California Employer’s Guide (DE 44)

• Household Employer’s Guide (DE 8829)

• Internet access to the EDD at www.edd.ca.gov

• Outreach seminars

• Small Business Employer Advisory Committee

• e-Services for Business

• Facebook, Twitter, and YouTube

Page 4 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

(INTERNET)

CHAPTER 1 INTRODUCTION

AUTHORITY TO

ENFORCE

COLLECTION

The laws authorizing CD to enforce collection activities are

contained in the following:

• Business and Professions Code

• Civil Code

• Code of Civil Procedure

• Commercial Code

• Corporations Code

• Family Code

• Government Code

• Penal Code

• Probate Code

• Revenue and Taxation Code

• California Unemployment Insurance Code

• United States Bankruptcy Code

• United States Code

• California Code of Regulations

• Code of Federal Regulation

When voluntary compliance is not obtained, CD may take

involuntary collection actions. These actions may include:

• Citation hearing

• Compliance complaint

• Earnings Withholding Orders for Taxes (EWOT)

• Earnings Withholding Orders (EWO)

• Lien on cause

• Notice of Levy (NOL)

• Notice of State Tax Lien

• Intercept

• Personal responsibility assessment

• Successor liability assessment

• Warrant

• Summary Judgement

DE 83 Rev. 1 (4-18) Page 5 of 9

CHAPTER 1 INTRODUCTION

COLLECTION

POLICIES

The EDD follows the collection practices contained in the

Rosenthal Fair Debt Collection Practices Act (RFDCPA) cited in

Sections 1788 through 1788.33 of the Civil Code. The EDD

endorses the principles listed in the RFDCPA in an effort to

ensure that CD exercise fairness, honesty, and regard for the

rights of the taxpayer during collection activities.

Below are guidelines to be used when contacting taxpayers:

• When talking with the taxpayer:

o Be a good listener.

o Speak in a clear and precise manner.

• Be considerate of the diversified employer community.

• Be flexible in setting appointments.

• Keep the appearance and/or tone of your voice professional.

• Treat the taxpayer in a fair and equitable manner.

• Verify information supplied by the taxpayer.

Page 6 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

Page 7 of 9

CHAPTER 1 INTRODUCTION

PROHIBITED

COLLECTION

ACTIVITIES

The following types of activities are prohibited under the

RFDCPA, and Tax Branch staff is not to use these collection

activities:

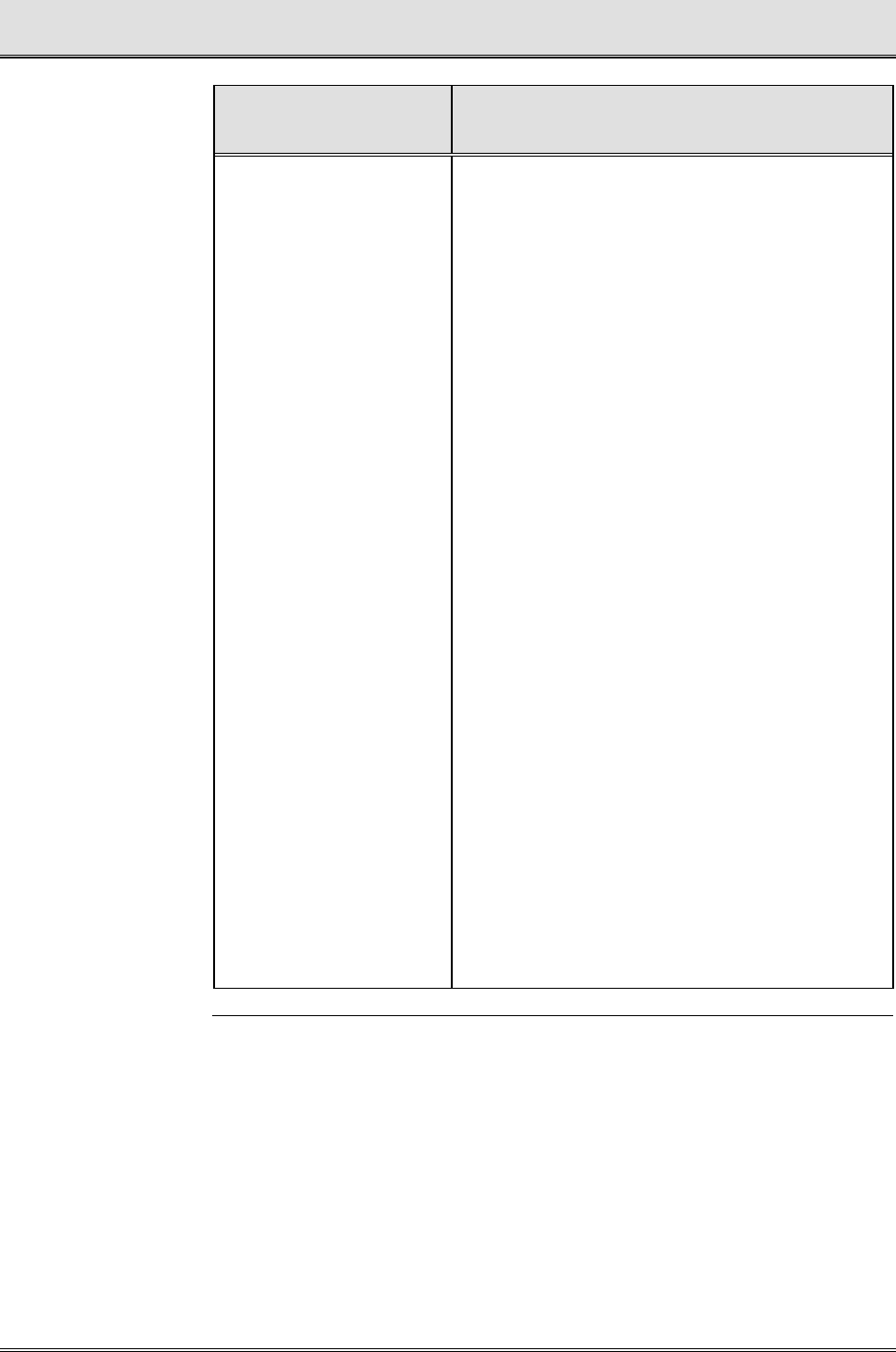

TYPE OF ACTIVITY EXAMPLES OF IMPROPER ACTIVITY

Harrassment

• Use obscene or profane language.

• Contact a taxpayer without identifying

oneself as a representative of the

EDD.

• Make a taxpayer accept a collect

phone call or pay for a telegram.

• Communicate by phone or in person

with the taxpayer with such frequency

as to be unreasonable and thus cause

harassment.

• Cause a phone to ring repeatedly or

continuously to annoy the taxpayer.

• Use involuntary collection actions (i.e.,

liens, warrants, offsets) while the

employer is bankrupt.

Make threats against

the taxpayer

• Use, or threaten to use, violence or to

inflict physical harm to the person,

reputation, or the property of any

person.

• Tell a taxpayer they have committed a

crime.

• Disclose information about the

taxpayer to a third party that would

defame the taxpayer.

• Tell a taxpayer they will be arrested or

imprisoned.

• Threaten to take property (i.e., by lien,

warrant, offset, etc.) unless such

action is contemplated and permitted

by law.

DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 1 INTRODUCTION

PROHIBITED

COLLECTION

ACTIVITIES

(cont’d.)

TYPE OF ACTIVITY EXAMPLES OF IMPROPER ACTIVITY

Providing false

information to a

taxpayer or about a

taxpayer

• Use of false names in the performance

of their duties.

• Falsely state or imply:

o That you are an attorney.

o That legal papers being sent to the

taxpayer have been written by an

attorney.

o That the collector works for a

consumer reporting agency or that

the taxpayer will be reported to

one.

• Misinform the taxpayer regarding the

purpose of the collection action.

• Misinform the taxpayer concerning

their legal rights in the collection of the

debt.

Page 8 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 1 INTRODUCTION

PROHIBITED

COLLECTION

ACTIVITIES

(cont’d.)

TYPE OF ACTIVITY EXAMPLES OF IMPROPER ACTIVITY

Unfair collection

activity/practices

• Communicate with a taxpayer's

employer unless necessary to collect

the debt.

• Communicate with a taxpayer's family

except to locate the taxpayer and/or

assets.

• Refer the taxpayer's name to a list

commonly called "Deadbeat List."

• Print anything on an envelope other

than the name, address, and phone

number of the tax collector or

taxpayer.

•

Initiate judicial proceedings in a county

other than the county in which the

taxpayer incurred the debt or in the

county where the taxpayer resides.

• Initiate judicial proceedings against a

taxpayer when there is no legal right to

do so.

• Communicate with the taxpayer, other

than with statements of amounts due,

when the taxpayer has requested their

attorney represent them (unless the

attorney fails to communicate with the

collector).

• Collect amounts greater than the debt

due.

Page 9 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

REPORT

DELINQUENCIES

A tax report delinquency occurs when an employer fails to file the

required reports electronically or online through e-Services for

Business at www.edd.ca.gov/e-Services_for_Business, to

comply with the e-file and e-pay mandate, within the time limits

established by the California Unemployment Insurance Code

(CUIC).

Assembly Bill (AB) 124

5 requires all employers to file employment

tax returns and wage reports electronically and remit payroll tax

deposits by Electronic Funds Transfer (EFT) to the EDD. This

requirement will be referred to as the e-file and e-pay mandate.

January 1, 2017: Employers with 10 or more employees were

required to file electronically and pay by EFT.

January 1, 2018: All remaining employers are required to file

electronically and pay by EFT.

For more information on this mandate, visit

www.edd.ca.gov/EfileMandate.

Since January 18, 2011, the reports required of most employers

are:

FORM CUIC SECTION

Payroll Tax Deposit, DE 88ALL

1088(b)

Employer of Household Worker(s) Quarterly

Report of Wages and Withholdings, DE

3BHW

1088

Employer of Household Worker(s) Annual

Payroll Tax Return, DE 3HW

1088

Quarterly Contribution Return and Report of

Wages, DE 9

1088(a)

Quarterly Contribution Return and Report of

Wages (Continuation), DE 9C

1088(a)

Page 1 of 8 DE 83 Rev. 1 (4-18)

(INTERNET)

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

REPORT

DELINQUENCIES -

HISTORICAL

Between January 1, 1995, and December 31, 2010, the reports

required of most employers were:

FORM CUIC SECTION

Payroll Tax Deposit (DE 88)/Payroll Tax

Deposit Return Envelope (DE 88E),

DE 88/DE 88E

1088(b)

Quarterly Wage and Withholding Report,

DE 6

1088(a)

Annual Reconciliation Statement, DE 7

1088(e)

Quarterly Contribution Return (Voluntary

Plan), DE 3D

1088(c)

Employer of Household Worker(s) Quarterly

Report of Wages and Withholdings, DE 3BHW

1088

Employer of Household Worker(s) Annual

Payroll Tax Return, DE 3HW

1088

DE 83 Rev. 1 (4-18) Page 2 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

REPORT TYPES

PAYROLL TAX

DEPOSITS

Section 1088 of the CUIC requires that a subject employer file

Payroll Tax Deposits (DE 88) electronically or online through

e-Services for Business at

www.edd.ca.gov/e-Services_for_Business to comply with

the e-file and e-pay mandate to:

Pay employer taxes of Unemployment Insurance (UI) and

Employer Training Tax (ETT).

Submit deposits of Disability Insurance (DI) and Personal

Income Tax (PIT) withheld as required by law.

Deposits of UI and ETT are due quarterly, while withholdings of

DI and PIT are generally due at the same time as federal due

dates. Penalty and interest are charged on late deposits.

For payroll tax deposit payments that are not made electronically,

there is a 15 percent penalty on the amount due.

Effective January 1, 2017, credit cards will be accepted as an

electronic payment that satisfies both the AB 1245 e-file and

e-pay mandate Sections 1088(h)(1) (2) and 13021(d)(1) of the

CUIC. As a result, employers using credit cards to remit DE 88

payments beginning January 1, 2017, will not incur a 15 percent

non-compliance penalty.

QUARTERLY

CONTRIBUTION

RETURN AND

REPORT OF

WAGES

(CONTINUATION)

(DE 9C)

Employers are required to file a DE 9C electronically or online

through e-Services for Business at

www.edd.ca.gov/e-Services_for_Business each quarter

with the following information:

• The name and Social Security number of each employee.

• Total subject wages for each employee.

• The PIT wages for each employee.

• Amount of PIT withheld for each employee.

• Grand total of subject wages, PIT wages, and PIT withheld for

the quarter.

DE 83 Rev. 1 (4-18) Page 3 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

QUARTERLY

CONTRIBUTION

RETURN AND

REPORT OF

WAGES

(CONTINUATION)

(DE 9C)

(

cont’d.)

The DE 9C is due January 1, April 1, July 1, and October 1 each

year. If the filing due date falls on a Saturday, Sunday, or legal

holiday, then the filing date is the next business day. The DE 9C

is delinquent if not received electronically within 30 days after the

due date.

The information from the DE 9C is used to:

• Post wage information.

• Calculate UI and DI benefits.

• Update the Franchise Tax Board (FTB) PIT Table, which

provides PIT withholding figures.

Even if an employer has no employees for a particular quarter,

but anticipates employees in future quarters, a DE 9C must be

filed quarterly, either electronically or online through e-Services

for Business. An automated search identifies missing returns and

issues a demand for the missing DE 9C.

After the demand is issued and the employer does not file a

DE 9C, a Section 1114 of the CUIC penalty will be added. The

Section 1114 penalty is $20 ($10 for periods prior to the 3rd

quarter 2014) for every item listed on the DE 9C.

Penalties for non-compliance with the e-file and e-pay mandate

are $20 per wage item.

If a reporting error has been made on a previous DE 9C, a

Quarterly Contribution and Wage Adjustment Form (DE 9ADJ)

should be used to file the corrected information.

DE 83 Rev. 1 (4-18) Page 4 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

QUARTERLY

CONTRIBUTION

RETURN AND

REPORT OF

WAGES

(DE 9)

Employers are required to

file a DE 9 quarterly to reconcile payroll

tax deposit payments submitted during the quarter for

withholdings of DI and PIT, employer payments of UI and ETT,

and to reconcile the total subject wages reported on the DE 9C.

The DE 9 is due January 1, April 1, July 1, and October 1 each

year. If the filing due date falls on a Saturday, Sunday, or legal

holiday, then the filing date is the next business day. The DE 9 is

delinquent if not received electronically within 30 days after the

due date.

A final DE 9 must be filed within 10 working days after an

employing entity closes a business.

A DE 9 must be filed each quarter even if there is no payroll

during the quarter. If the employer fails to file a completed DE 9

within 60 days of the due date, an estimated assessment is

issued for that quarter. In addition, a Section 1112.5 of the CUIC

penalty of 15 percent (10 percent for periods prior to the 3rd

quarter 2014) of the estimated contributions and PIT withheld will

be charged. Penalties for non-compliance with the e-file and

e-pay mandate are $50 per return.

If a reporting error has been made on a previous DE 9, a

DE 9ADJ should be used to file the corrected information.

DE 83 Rev. 1 (4-18) Page 5 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

QUARTERLY

WAGE AND

WITHHOLDING

REPORT

(DE 6)

Between January 1, 1995, and December 31, 2010, employers

were required to file a Quarterly Wage and Withholding Report

(DE 6) each quarter with the following information:

• The name and Social Security number of each employee.

• Total subject wages for each employee.

• The PIT wages for each employee.

• Amount of PIT withheld for each employee.

• Grand total of subject wages, PIT wages, and PIT withheld

for the quarter.

The information from the DE 6 was used to:

• Post wage information.

• Calculate UI and DI benefits.

• Update the Franchise Tax Board (FTB) PIT Table, which

provides PIT withholding figures.

Even if an employer has no employees for a particular quarter,

a DE 6 must be filed quarterly if it is anticipated that there will

be employees in future quarters.

After the demand was issued and the employer did not file a

DE 6, a Section 1114 of the CUIC penalty was added. The

Section 1114 penalty is $10 for every item listed on the DE 6.

If a reporting error was made on a previous DE 6, a Tax and

Wage Adjustment Form (DE 678) was used to file the corrected

information.

DE 83 Rev. 1 (4-18) Page 6 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

ANNUAL

RECONCILIATION

STATEMENT

(DE 7)

Between January 1, 1995, and December 31, 2010, employers

were required to file an Annual Reconciliation Statement (DE 7)

annually to reconcile tax deposit payments submitted during the

year for withholdings of DI and PIT, employer payments of UI

and ETT, and to reconcile the total subject wages reported

during the year on the DE 6. The DE 7 was due on the first

business day of the subsequent year and was delinquent if not

postmarked on or before January 31 of that year. If January 31

fell on a Saturday or Sunday, the employer had until the next

business day to file the DE 7 timely.

A final DE 7 was required to be filed within 10 working days

after an employing entity closes a business.

If an employer failed to file a completed DE 7, an estimated

assessment was issued for each active quarter on the

employer’s account. In addition, a Section 1117 of the CUIC

penalty was charged. The Section 1117 penalty is $1,000 or

five percent of contributions, whichever is less. This penalty is

after a demand had been sent and a DE 7 was not received

within 45 days. When a DE 7 was received after or an

assessment was issued, the penalty may have been reduced to

five percent of total contributions due.

If a reporting error was made on a previous DE 7, a DE 678

was used to file the corrected information.

DE 83 Rev. 1 (4-18) Page 7 of 8

(INTERNET)

CHAPTER 2 REPORT DELINQUENCIES

QUARTERLY

CONTRIBUTION

RETURN

(DE 3)

Prior to January 1, 1995, employers were required to file a

Quarterly Contribution Return (DE 3) (similar to a DE 9) and a

Report of Wages (DE 3B) (similar to a DE 9C). The DE 3 was

used by employers to report UI, ETT, and DI taxable wages

and the amount of PIT withheld. All amounts due were

submitted with the DE 3. The DE 3B was used to report each

employee’s name, Social Security number, and quarterly

wages.

The DE 3/DE 3B had the same due and delinquency dates as

the DE 9/DE 9C and the end of quarter DE 88 payment.

Payment must accompany the DE 3, including all funds that

were payable by the employer, as well as trust fund

withholdings.

DE 83 Rev. 1 (4-18) Page 8 of 8

(INTERNET)

CHAPTER 3 COLLECTION MANAGEMENT

COLLECTION

MANAGEMENT

Collection management is defined as a series of actions taken

to ensure that the interests of the people of California are fully

protected. Collection management incorporates the successful

integration of an automated collection system with individual

case assignment for intensive collection actions. To protect the

interest of the state, criteria have been established for how the

collection inventory and cases are to be worked in both the

automated centralized environment and for individual case

assignment.

Adjustments may be made to case inventories:

• To equalize workloads.

• To allow for improvements in customer service to

employers, taxpayers, claimants, other members of the

public, and business communities with whom we serve.

Collection management includes the following:

•

Applying a progressive system of collection actions and tools

with involuntary actions taken only when all other voluntary

actions are no longer effective.

•

Providing accurate information and support to our customers.

•

Evaluating and acting upon customer concerns or requests

in an objective, impartial, and timely manner.

•

Conducting Section 1735 of the California Unemployment

Insurance Code (CUIC) investigations while pursuing

collection of corporate liability.

•

Identifying aged accounts to be worked and resolved.

•

Utilizing staff and technological resources effectively.

•

Resolving all accounts in an expedient manner.

•

Transferring accounts when appropriate.

DE 83 Rev. 1 (4-18) Page 1 of 2

(INTERNET)

CHAPTER 3 COLLECTION MANAGEMENT

COLLECTION

MANAGEMENT

(cont’d.)

Questions concerning collection management should be

directed initially to a manager for a discussion of specific local

issues and how they impact the overall collection management

process. Program management team members are also

available to discuss collection management issues.

TIME FRAMES To ensure timely collection resolution, specific tasks have been

identified for effective collection management. In reviewing

assignments, staff and managers will discuss cases or workloads

that pose a particular challenge or offer a unique opportunity for

professional growth and added program knowledge. Assignments

that have not been worked within the time frames will be

identified. A partnership between staff and management will then

ensure that these assignments are fully worked in the most

efficient and effective manner possible.

REIMBURSABLE

ACCOUNTS

In lieu of the contributions required by employers, an entity, as

defined in Section 803(a) of the CUIC, may elect to reimburse

the Unemployment Insurance Fund the cost of benefits paid to

claimants. Reimbursable accounts generally are public entities

hospitals, religious, charitable, educational, and nonprofit

organizations. An application is required to be filed by the entity

and approved by the EDD. Section 803(h) of the CUIC

authorizes the EDD to terminate the election of any entity that is

delinquent in the payment of advances or reimbursements

required by the Director.

Notices of State Tax Lien (DE 2181) may not be filed on

governmental agencies. If an entity is delinquent, the entity may

be contacted. A meeting with the entity must be requested if

payment in full is not made. In addition, an investigation to

determine the responsible person for the entity should

commence. The area program manager must pre-approve ALL

compliance actions.

DE 83 Rev. 1 (4-18) Page 2 of 2

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

CONTACT

EMPLOYER

Professional conduct and demeanor are important when

communicating with customers. The first contact with an

employer gives them a lasting impression of the Employment

Development Department (EDD). Employers expect and deserve

quality customer service from every EDD employee. This

expectation is consistent with the EDD Vision Statement. The

first contact with an employer is an excellent opportunity to gain

the employer's attention, cooperation, and full compliance.

Understanding and learning how to motivate people are

important compliance enforcement tools. Developing these skills

requires an insight of the business methods and characteristics

of the individuals that make up the diversified employer

community. Generally, you will encounter four basic types of

employers:

•

Willing to pay/able to pay

•

Willing to pay/unable to pay

•

Unwilling to pay/able to pay

•

Unwilling to pay/unable to pay

Staff should develop, with training and experience, their own

technique for motivating an employer to pay voluntarily.

Experience leads to expertise.

Staff should also develop an approach to effectively deal with

each of the four types of employers that may be encountered in

collection activities. Knowing when and how to respond or initiate

necessary action is a prerequisite to becoming an effective

compliance person.

Contact with employers is made by letter, phone, office meeting,

or field calls to the employer's place of business. The degree of

urgency or type of collection assignment will determine the type

of contact to initiate first.

DE 83 Rev. 1 (4-18) Page 1 of 12

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

ENTITY

VERIFICATION

California recognizes many types of business entities. The

different entity types provide opportunities for people to raise

capital in different ways and to limit the degree of personal

liability. The six major forms of business entities are sole

proprietorship, general partnership, limited partnership, limited

liability partnership, limited liability company, and corporation.

Corporations are the most popular form of a business entity.

Entity types and their descriptions are outlined below:

Sole Proprietorship

A sole proprietorship is one individual who owns and operates

one or more businesses. The assets of the individual may be

used to satisfy the liability of the business.

General Proprietorship

Sections 16100 through 16962 of the California Corporations

Code (CCC) are known as the Uniform Partnership Act of 1994.

As provided in Section 16101(9) of the CCC, a partnership is an

association of two or more persons to carry on as co-owners of a

business for profit.

The partners jointly own the firm and share in its profits or losses.

Section 16306 of the CCC states that all partners are liable

jointly and severally for all obligations of the partnership. The

assets of the individual partners, as well as the partnership

assets, may be used to satisfy the liability.

A partnership agreement may be formal or informal, written or

oral. The intention to form a partnership may be determined from

the acts, conduct, and statements of the parties. General

partnerships originate in common law and do not require formal

authorization.

Statement of partnership papers are filed with the county clerk or

recorder’s office and are indexed by the name of the partnership.

All partners’ names and addresses are listed on the statements.

DE 83 Rev. 1 (4-18) Page 2 of 12

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

ENTITY

VERIFICATION

(cont’d.)

Dissolution of Partnership

Whenever a partnership is dissolved, a notice of the dissolution

shall be published at least once in a newspaper of general

circulation in the place where the business was operated. This

notice is filed with the county clerk within thirty days after the

publication.

Limited Partnership

Sections 15900 through 15912.07 of the CCC is known as the

Uniform Limited Partnership Act of 2008. A limited partnership is a

partnership formed by two or more persons, having members as

one or more general partners and one or more limited partners.

Limited partners are not liable for any obligation of a limited

partnership unless named as a general partner. The assets of the

limited partnership and all general partners are jointly and

severally liable for the full partnership debt.

The limited partnership is not dissolved if a limited partner

withdraws, dies, or is substituted.

The words “limited partnership” or “L.P.” must appear at the end of

the firm name. Limited partners’ names are not shown.

The Secretary of State (SOS) indexes certificates of limited

partnership by the name of the limited partnership. The certificates

will list the name and address of the general and limited partners,

as well as the agent for service of process.

Foreign Limited Partnership

A foreign limited partnership is a limited partnership formed under

the laws of any state other than this state or under the laws of a

foreign country. A certificate of registration should be on file with

the SOS. The same information as described above for a limited

partnership will be shown, as well as the location where the

partnership was formed.

Dissolution of Limited Partnership

A certificate of dissolution must be filed with the SOS. It will include

the name of the limited partnership, file number, and the date of

dissolution.

DE 83 Rev. 1 (4-18) Page 3 of 12

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

ENTITY

VERIFICATION

(cont’d.)

Limited Liability Company

Sections 17701.01 through 17701.17 of the CCC are known as the

California Revised Uniform Limited Liability Company Act. Limited

liability companies (LLC) are a cross between a limited partnership

and a corporation. The LLC s must have one or more m embers.

The owners are designated as members instead of shareholders

or partners.

In order to form an LLC, articles of organization must be filed with

the SOS and a SOS file number will be issued. The LLC Unit

within the SOS will provide copies of the documents and the date

of filing.

The LLCs are treated as corporations for collection purposes.

Members must be assessed under Section 1735 of the California

Unemployment Insurance Code (CUIC) when individual

responsibility is identified.

Limited Liability Partnership

Sections 16951 through 16962 of the CCC permit licensed

persons to render professional limited liability partnership services.

Limited liability partnerships (LLP) are limited in those businesses

dedicated to the practice of public accountancy, law, architecture,

engineering, or land surveying. The two types of LLPs are

Registered Limited Liability Partnerships (RLLP) and foreign LLPs.

The assets of the LLP and a partner assessed under a

Section 1735 of the CUIC assessed partner are responsible for the

liabilities.

A RLLP is formed when a partnership, other than a limited

partnership, files a registration with the SOS. It must be submitted

by one or more of the partners authorized to execute a registration.

A foreign LLP must be a registered LLP pursuant to an agreement

governed by the laws of the foreign jurisdiction and denominated

or registered as an LLP under the laws of that jurisdiction.

The name of the RLLP shall contain the words “Registered Limited

Liability Partnership” or “Limited Liability Partnership” or one of the

abbreviations “L.L.P.,” “LLP,” “R.L.L.P.,” or “RLLP.”

DE 83 Rev. 1 (4-18) Page 4 of 12

CHAPTER 4 CONTACT EMPLOYER

ENTITY

VERIFICATION

(cont’d.)

LLPs possess some qualities of a partnership as well as some

qualities of a corporation. The partners are required to be licensed

under the provisions of the Business and Professions Code to

practice law, professional accountancy, or architecture, or be

related to a RLLP to provide facilities to or services related or

complementary to the professional LLP.

Verification or copies of the registration documents for both entities

are located in the Limited Liability Unit at the SOS.

The LLP members must be assessed under Section 1735 of the

CUIC to be held individually responsible for LLP tax liabilities.

Corporations

Sections 100 through 2319 of the CCC are known as the General

Corporation Law. A corporation is an entity, separate and distinct

from its members. The entity holds title to the assets. A corporation

may be either domestic or foreign.

A domestic corporation operates and is incorporated in the state in

which it is chartered. Section 200 of the CCC provides that

applicants must file articles of incorporation with the SOS. A

corporate account number is issued by the SOS.

A foreign corporation operates in California and is incorporated in

another state. Section 2105 of the CCC sets forth the filing

requirements for foreign corporations. The SOS will issue a

certificate of qualification for a foreign corporation.

Private Corporation

The term “private corporation” refers to a corporation founded by

and composed of private individuals for private purposes.

Public Corporation

The term “public corporation” refers to a corporation created by the

State for political purposes and to act as an agency in the

administration of civil government.

Nonprofit Corporation

The term “nonprofit corporation” applies to any corporation formed

for other than profit reasons. A federal exemption under United

States (U.S.) Code, Title 26 (Internal Revenue Code),

Section 501(c)(3) must be obtained. Examples include religious,

charitable, and education institutions.

Page 5 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

ENTITY

VERIFICATION

(cont’d.)

De Jure and De Facto Corporations:

These issues arise only in the formation stage of the corporation.

A de jure corporation is one that is organized in full compliance

with all of the state requirements.

A de facto corporation operates as if it were a corporation although

it has not completed the legal steps to become incorporated (has

not filed its articles of incorporation, for example) or has been

dissolved or suspended but continues to function. The court

temporarily treats the corporation as if it were legal in order to avoid

unfairness to people who thought the corporation was legal.

Termination

The corporate existence may be terminated by:

• Voluntary dissolution

• Involuntary dissolution

• Proceeding by the state

Suspension

Suspension of a corporation for nonpayment of franchise taxes

under Section 23301 of the Revenue and Taxation Code does not

terminate the corporate existence. The corporate entity remains

the employing unit and legal entity that incurs liability under the

CUIC by reason of any employment of persons and payment of

wages during the suspension period.

OTHER ENTITY

TYPES

Association

Section 21300 of the CCC defines an association as including any

lodge, order, beneficial association, fraternal or beneficial society

or association, historical, military, or veterans organization, labor

union, foundation, or federation, or any other society organization,

or association, or degree, branch, subordinate lodge, or auxiliary

thereof. The association and a Section 1735 of the CUIC assessed

responsible person are responsible for the liabilities.

Page 6 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

OTHER ENTITY

TYPES

(cont’d.)

Estate

In case of death of a person, an executor of the estate may be

named in a will. If no executor is named, or if no will exists, courts

may appoint an administrator of the estate. Like trustees,

executors and administrators are not usually considered

employees of the estate, but perform services applicable under a

fiduciary capacity. A new EDD employer payroll tax account

number is not required unless employees are hired. The estate is

the employing unit and is responsible for the liabilities.

Joint Venture

A joint venture is the undertaking of two or more persons or

entities joined to carry out a single business transaction or

operation. Its existence depends on the intent of the parties. A joint

venture has neither a predecessor nor successor and the unity of

enterprise theory does not apply. The joint venture ceases when

the specific reason for its formation is complete. The joint venture

is the employing unit and is responsible for the liabilities.

Public Agency

A public agency includes every governmental subdivision, district,

public and quasi-public corporation, public agency and public

service corporation, town, city, county, city and county, municipal

corporation, whether incorporated or not. The public agency is

responsible for liabilities.

Trust

A trust is the designation of a third party (trustee) to manage

assets for the benefit of another party. A new employing unit is

created if employment services are performed for the trust. The

trust is the employing unit and is responsible for the liabilities.

Page 7 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

FIRST PERSONAL

CONTACT

The EDD’s policy is to make timely contact with the taxpayer

after case assignment. In general, 15 calendar days is

considered to be a timely initial contact but may be adjusted, not

to exceed 90 days, due to workload volume. Adjustment of

contact time frames requires management approval. A

representative’s primary goal is to make the first contact within

established time frames and to gain full compliance with an early

resolution. Use of the phone is generally the most cost-effective

way of speaking with the taxpayer.

Prior to contact:

•

Analyze the account and the liability.

•

Prepare to explain the liability.

•

Have questions ready to update missing account information.

•

Anticipate questions and have the answers.

•

Be familiar with:

o The EDD’s policy on the Rosenthal Fair Debt Collection

Practices Act, Sections 1788 through 1788.33 of the Civil

Code.

o Confidentiality policies.

o Employers’ Bill of Rights (DE 195).

o The CUIC and other California laws.

•

Know the laws related to payment agreements and collection

remedies.

•

Determine the owner or authorized person to be contacted.

Making contact:

•

Make sure you are speaking to the owner or authorized

person.

•

Explain the purpose of your call. Make a demand for

immediate payment in full of outstanding liabilities including

filing and payment of delinquent returns.

•

Communicate clearly and do not use acronyms.

•

Explain the advantages of full compliance if the taxpayer

cannot provide definite compliance dates.

Page 8 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

IDENTIFY THE

TAXPAYER

It is critical to speak to the person responsible for the payment of

the liability. Confirm that the person who is contacted is the owner,

partner, responsible person, or authorized agent. This may include

someone having a power of attorney. An individual responsible for

payment may not include the person who prepared the tax return,

unless that tax preparer also has check writing authority. It is the

responsibility of the employer to contact their accountant or

bookkeeper for return adjustment information and to provide any

power of attorney information.

PAYMENT

HISTORY

Analyzing the taxpayer’s payment history will assist in locating

unapplied payments or payments that have resulted in a refund.

PHONE

CONTACTS

Good communication requires the following skills:

SKILLS DESCRIPTION

Speak clearly Be precise and enunciate clearly.

Keep it simple

Communicate so the other person understands.

Avoid the use of legal or technical terms unless

it is absolutely necessary. Never use jargon or

EDD acronyms that the customer may not

understand.

Be objective Do not allow personal thoughts or opinions to

interfere with understanding the employer's

financial problems.

Do not presume

to know

Wait until there is sufficient information before

making a decision and giving a response.

Restate the conversation to ensure

understanding.

Stay focused Listen and understand what the taxpayer is

trying to explain.

Page 9 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

PHONE

CONTACTS

(cont’d.)

SKILLS DESCRIPTION

Balance the

communication

Effective communication requires one speaker

and one listener at a time. Each should have

ample time to speak or respond without

interruption.

Never argue Keep the mood pleasant and professional.

Summarize the

outcome of the

call

Confirm agreements that have been reached

and the dates and amounts that are due. Set

up any follow-up dates if documents are to be

provided.

Ask the right

questions

Knowing when and how to ask specific

questions is necessary.

Use option

thinking

Consider all available alternatives to move the

case forward to a rapid resolution.

OFFICE

MEETING

A positive attitude contributes noticeably to performance,

productivity, and good customer service. It is a skill that is

developed individually.

Learn to use the tools and resources available and consider all

options available.

Things to do before the taxpayer arrives:

•

Schedule interview room.

•

Complete all the steps in reviewing and analyzing the

account.

•

Review all of the documents that were previously submitted.

•

Prepare a list of questions.

•

Determine additional information needed to resolve report

delinquencies.

Page 10 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

PREPARATION

FOR THE FIELD

CALL

Be prepared to discuss the problems with the taxpayer at the

place or location of the field call.

Items to take:

•

Proper identification and business cards.

•

Contribution Receipt Book (DE 10).

•

Extra copies of forms the taxpayer may need.

•

GPS or a current map.

•

Laptop.

Things to do prior to leaving for the field call:

•

Prepare travel itinerary in accordance with your office

practices and policies.

•

Sign out per your office practices and policies.

•

Conduct a safety check of the vehicle to be used. If using a

state vehicle, make sure the travel log, and accident report

forms are in the glove compartment.

•

Comply with additional office procedures and seek advice

related to the business location.

RETURNING TO

THE OFFICE

Upon returning to the office, discuss any case issues or

problems with the manager.

Page 11 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 4 CONTACT EMPLOYER

COLLECTION

LETTERS

Some taxpayers will respond to:

•

Phone calls

•

Field visits

•

Letters

Each collection case requires individual treatment. Knowing

when to use each type of contact is a skill that is acquired

through experience.

The EDD has several form letters that may be used when

corresponding with a taxpayer. The appropriate letter should be

used. Every letter will contain the name of the representative or

other authorized person familiar with the case and the office

address and phone number.

Collection letters should be mailed as follows:

•

Ordinary mail: Use in most cases.

•

Certified mail: Use if proof of delivery is necessary.

•

Certified mail with return receipt: Use if it is suspected that

the taxpayer has moved and a receipt is needed to show

the address of delivery.

Page 12 of 12 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

ESCROW

Escrow is a contractual arrangement between parties, whereby

an independent, trusted third party receives and disburses money

or documents for the parties, with the timing of such disbursement

dependent on the fulfillment of conditions set by the parties.

Escrows are best known in the context of real estate, but are also

used for other financial transactions. The escrow process

guarantees that the property being purchased is free and clear of

encumbrances, including Employment Development Department

(EDD) liability.

The two most common types of escrows for the EDD collections

are the sale or refinance of real property and the sale of a

business.

The escrow company will contact the EDD to determine

the amount due and withhold money from the proceeds of the

sale to remit to the EDD.

The escrow holder is required to withhold sufficient money from

the proceeds of the escrow to cover any amounts due to the EDD.

Failure to withhold may make the escrow holder liable for the full

amount of any Notice of State Tax Lien (DE 2181).

In addition to escrows, there are other situations where the EDD

may be contacted for a demand for payoff when there is a sale or

transfer of assets, such as:

• Liquor license

• Personal property

• Real property

• Surplus funds

Page 1 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

ESCROW

(cont’d.)

A DE 2181 is recorded in the county where the property is located

and/or filed with the Secretary of State (SOS).

This chapter covers the different types of demands for payment

that are requested from:

• Attorneys

• Banks

• County tax collectors

• Escrow companies

• IRS

• Business owners

• Private parties

• Reconveyance companies

• Title companies

• Trustees in bankruptcy

• Trustee services

Page 2 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

RESPONSIBILITY

FOR DEMAND

AND CLEARANCE

The responsibility of issuing a demand and clearance has been

divided as follows:

TYPE OF SALE OR

TRANSFER

RESPONSIBLE AREA

Business with a

liquor license

The Area Audit Office (AAO) issues escrow

clearances on the sale of businesses for

employers within their jurisdiction.

Special Procedures Section, Offset Group

(SPS, OG), processes the liquor license

demand/transfer if there is a hold on the

liquor license.

Business without a

liquor license

Audit issue escrow clearances on the sale

of businesses for employers within their

jurisdiction.

Excess funds

SPS

,

OG

Home equity loans

Special Procedures Section, Lien Group

(SPS, LG) - Full pay

Special Procedures Section, Special

Procedures Group (SPG, SPG) - Partial

pay

Surplus funds

SPS, OG - Full pay

SPS, SPG - Not paid in full

Liquor license

SPS, OG

Mortgage refinance

SPS,

LG

Personal property

SPS, LG - Full pay

SPS, SPG - Partial pay

Real property

SPS, LG

Page 3 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

RESPONSIBILITY

Field personnel who have case assignments may be requested to

assist in the escrow process.

FOR DEMAND

AND CLEARANCE

(cont’d.)

SALE OF A

BUSINESS

Section 1731 of the California Unemployment Insurance Code

(CUIC) provides that any person or entity that acquires an

employer’s business or substantially all of the assets shall

withhold in trust sufficient money or other property to cover the

employer's liability. The withholding shall continue until the

employer produces a certificate from the EDD stating that no

amounts are due.

Section 1732 of the CUIC provides that upon the request of the

seller or buyer, the EDD shall issue a statement showing the

amount due by the seller. If the EDD fails to issue the statement

within 30 days, it is equivalent to stating that there is no amount

due. However, if the EDD issues the statement, the buyer shall

withhold and pay to the EDD the amount due, not to exceed the

purchase price.

If the EDD issues a certificate stating that no amounts are due or

fails to issue an amount due statement within the 30-day period,

the seller is still responsible for any amount then or thereafter

determined to be due. However, the buyer is released from any

further liability on the seller’s account.

Section 1733 of the CUIC provides that any buyer that fails to

withhold money or other property from the sale or fails to pay the

amount withheld shall be personally liable for the employer’s

amount due up to but not exceeding the purchase price.

The EDD uses a Certificate of Release of Buyer (DE 2220) to

notify the buyer that they are released from any further liability on

the seller’s account.

Page 4 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

SALE OF A

BUSINE

SS

(cont’d.)

Escrow Notification

When staff receives written notification of a pending business

escrow, a copy of the notification should immediately be faxed to

the appropriate responsible area. Staff will inquire if sufficient

funds are available to satisfy the EDD liability and, if so, may not

initiate further collection activity.

Demand and Clearance

The AAO is responsible for issuing escrow clearances on the sale

of businesses. Escrow clearances are required when a business

is either partially sold or sold in its entirety. When there i s a partial

sale of a business, the demand for delinquent taxes will include

the total tax liability due from the seller.

The AAO will contact the assigned staff immediately upon receipt

of an escrow clearance demand. The assigned staff may be

asked for assistance on the account. The responsibility for the

issuance of the DE 2220 remains with the AAO.

Statement of Amount Due

The AAO shall issue a Requirements for Certificate of Release of

Buyer Statement of Amounts Due Under Section 1732 of the

California Unemployment Insurance Code (DE 4874) showing the

amount of any contributions, interest, and penalties claimed to be

due. The DE 4874 should include all liabilities due as well as

estimated assessments, final or non-

final. Estimated assessments

should be issued for any missing returns, including periods not yet

delinquent. The DE 4874 is mailed to the escrow holder.

Page 5 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

SALE OF A

BUSINESS

(cont’d.)

Payments

The payment of any amount demanded in the DE 4874 shall be

submitted to the AAO as directed.

The amount due must be paid in the form of cash, cashier’s

check, money order, or escrow check. Checks written on the

seller’s checking account will delay the escrow clearance until the

check has cleared the account.

If any other enforced compliance is in effect, that action must be

terminated or modified after the funds are received. The AAO will

notify the assigned staff that funds have been received.

If sufficient funds are not available from the escrow process,

collections should continue against the seller.

Certificate of Release of Buyer

A request for clearance on behalf of a buyer is granted using a

DE 2220 when:

• The seller is registered and has

o No open delinquency case.

o No outstanding liabilities.

o No outstanding form delinquencies.

• The seller is not registered and

o The business has no employees.

o The business is a type that would not require employees.

• The seller is disposing of a portion of the business and

o A Notice of State Tax Lien (DE 2181) secures the full

amount of the EDD liability, and

o

The remaining portion of property is sufficient to secure the

EDD liability.

• The seller is not registered but

o The business is a type that would require employees, then

o The AAO will prepare an estimated amount due, and

o Send a demand to the escrow company using form

DE 4874.

Page 6 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

SALE OF A

BUSINESS

(cont’d.)

Additional Requirements

When the seller’s account has delinquent returns or missing

payments, the buyer is notified that additional conditions must be

met. A DE 4874, with instructions to withhold an amount equal to

the known delinquent taxes plus any estimated amounts, is sent

to the escrow holder with copies to each party. Additional

conditions may include:

• Missing reports:

o Payroll Tax Deposit (DE 88).

o Quarterly Contribution Return and Report of Wages

(DE 9).

o Quarterly Contribution Return and Report of Wages-

Continuation (DE 9C).

• Liability is due:

o A Notice of State Tax Lien covers all unpaid amounts.

o Liabilities are due that have not had a Notice of State Tax

Lien filed.

• A final return is due:

Final returns must be filed within 10 days of closure of the

business.

It is important to remember that the release of a buyer does not

release the seller if any liability is identified in the future.

File Retention

All escrow information will be retained by the AAOs for one year.

Page 7 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

EXCESS FUNDS

The EDD may be notified of excess funds from foreclosure

proceedings upon the real property of a taxpayer. Any entity

having a legal claim filed against the foreclosed property may file

a claim after the property has been sold. If funds remain over and

above the claim of the foreclosure, those having junior liens will

be paid from the excess funds according to their recording priority.

The SPS, OG receives a copy of all notices of default and all

notices of sale on properties having a Notice of State Tax Lien

recorded. Claim information is provided and completed by

SPS, OG.

HOME EQUITY

LOANS

When a taxpayer applies for a home equity loan requesting funds

from a financial institution based upon real property owned, the

request/demand is processed as outlined in the Real Property

section of this chapter.

SURPLUS FUNDS The IRS will seize and sell assets when their tax liens have not

been satisfied.

If there are surplus funds from the sale, the EDD may file a

demand for these funds. The SPS, OG prepares and monitors all

IRS surplus demands.

Page 8 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

LIQUOR LICENSE

When a business being sold has a liquor license, the following

actions will be performed:

• The SPS, OG will only process the liquor license

demand/transfer.

• The SPS, OG will contact the assigned staff to verify any

outstanding delinquencies and to confirm the amount to be

included in the demand.

• The AAOs will complete the escrow clearance process and

issue a DE 4874 for any outstanding delinquencies.

• When the AAO learns of a sale that involves both a business

and its liquor license, it determines the status of the liquor

license:

o If the liquor license is clear, the AAO will complete the

buyer release process.

o If the liquor license has a hold on it, the AAO will notify

SPS, OG.

MORTGAGE

REFINANCE

Taxpayers refinancing a mortgage on real property will need a

clear title. When a Notice of State Tax Lien has been recorded,

the lending institution will open an escrow and request a payoff

demand of the Notice of State Tax Lien or a subordination of the

Notice of State Tax Lien.

When assigned staff is made aware of a taxpayer’s refinance

action, advise the escrow holder to fax a demand request to

SPS, LG.

Page 9 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

PERSONAL

PROPERTY

Personal property is described as any property that is not

classified as real property. Usually, the transferring of personal

property is not handled through an escrow; however, the filing of a

Notice of State Tax Lien with the SOS will provide notice to the

buyer or a lender of delinquent tax liabilities.

When a Notice of State Tax Lien has been filed with the SOS, the

escrow will be processed by SPS, LG.

Personal property includes, but is not limited to:

• Aircraft

• Automobiles

• Boats

• Heavy equipment

• Mobile homes

• Office equipment

• Recreational vehicles

• Stock on hand

• Tangible assets

• Trucks

• Vessels

Page 10 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 5 ESCROWS

REAL PROPERTY

A title search will provide notice to an escrow holder or lender of a

Notice of State Tax Lien encumbering real property. All Notices of

State Tax Lien must be paid and released before title to the

encumbered property is cleared.

When the escrow holder or lender is processing an escrow with

respect to the encumbered property, they will send the EDD a

demand for a payoff amount or the release of the recorded liens.

In response to the request, SPS, LG will prepare either a demand

for the liability covered by the Notices of State Tax Lien, or a

status letter advising that the Notices of State Tax Lien have been

released. The 30-day limitation described in Section 1732 of the

CUIC does not apply to the sale of real property.

The demand request must be in writing and sent to:

Employment Development Department

Lien Group, MIC 92G

PO Box 826880

Sacramento, CA 94230-6880

Or

Fax: 1-916-464-2711

Correspondence regarding a demand related to real property and

covered by a Notice of State Tax Lien must be directed to

SPS, LG.

Page 11 of 11 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

INVOLUNTARY

COLLECTION

DETERMINATION

Involuntary collection action may be initiated immediately if any

of the following situations occur:

• A taxpayer fails to:

o Respond to Employment Development Department (EDD)

notices or correspondence after being contacted by an

EDD representative.

o Respond to phone calls.

o Provide requested information.

o Remain current on an installment agreement.

o Remain current on filing and paying quarterly requirements

(active employers).

o Make payments or payments are returned as

“non-sufficient funds” or “stop payment.”

o Negotiate an acceptable method of payment.

o Appear for an interview.

• A taxpayer is:

o In the process of liquidation of assets.

o Moving out of the state/country.

o Otherwise uncooperative or evasive regarding the

business entity.

• If:

o Bankruptcy appears imminent.

o A jeopardy assessment has been issued.

o It is necessary to protect the EDD’s interest.

o The taxpayer has a history of non-compliance.

o Assets are identified that were not disclosed by the

taxpayer.

o Statute of limitations is nearing expiration.

Care must be taken when deciding on the appropriate involuntary

collection action. Staff

must be able to distinguish between liability

that is due or delinquent.

Page 1 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

Involuntary actions can be taken using the following methods:

• Earnings Withholding Order for Taxes (EWOT), Jeopardy

Withholding Order for Taxes (JWOT)

• Interagency offsets

• Notice of Levy (NOL)

• Warrants

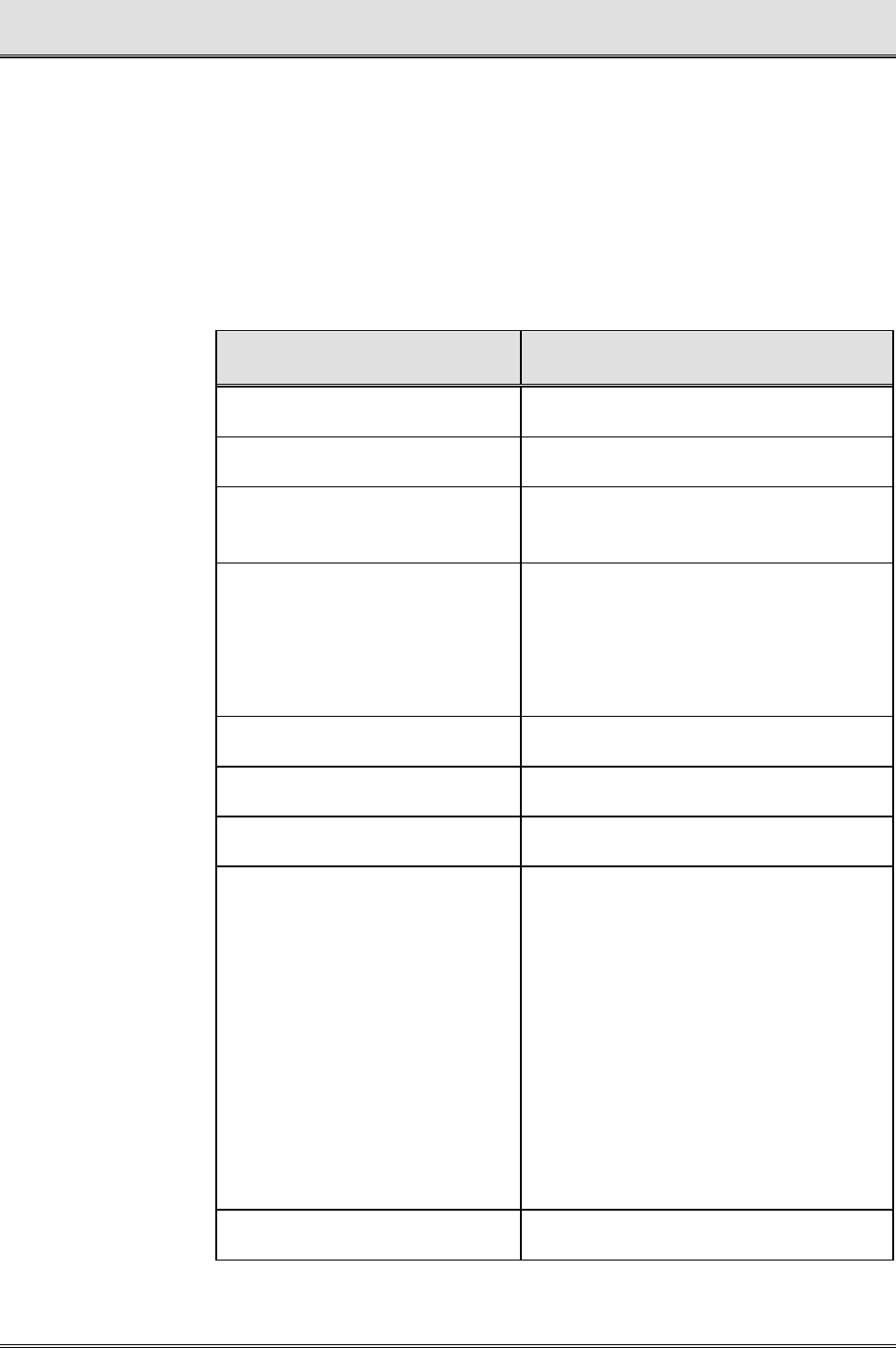

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Accounts receivable NOL – effective for one year

Aircraft Warrant

Assets requiring an

execution sale

Warrant

Assignee for benefit

of creditors

NOL on the assignee to secure

dividends that may be payable to

the taxpayer, if the assignment has

been recently terminated and there

are funds to be returned.

Automobile Warrant

Bank account NOL

Boat/trailer Warrant

Bonds:

1. Surety

2. United States

(U.S.) Savings

3. Security deposits

by other agencies

1. Claims filed by Special

Procedures Section,

Special Procedures Group

(SPS, SPG)

2. Not attachable

3. Offset

Campaign funds NOL

Page 2 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Cash in possession of

taxpayer

Warrant

Cash in possession of

third party

NOL

Cemetery plot, land held

for sale

Warrant

Cemetery plot, taxpayer’s

family/spouse

Not attachable

Certificate of deposit –

matured

NOL

Church – bank account NOL

Commissions plus salary EWOT/JWOT

Commissions – straight NOL if individual is treated as

an independent contractor

EWOT if individual is treated as

an employee

Community property –

other than wages

Issue an NOL or Warrant

depending on type of asset

When enforcement is being taken

against the community property of

a spouse who is not a taxpayer or

is not personally responsible for

the liability, the NOL or Warrant

must explain this fact.

Consigned property –

taxpayer’s

Warrant

Consignment sales –

proceeds

NOL

Contracts payable to

taxpayer

NOL

Page 3 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Denti-Cal payments

NOL

Disability Insurance (DI)

benefits

Not attachable for taxes – can be

offset for a benefit overpayment

Equipment: Warrant

•

Sale of Equipment

1. No escrow

2. With escrow

1. Warrant or NOL

2. Issue a demand to clear the

Notice of State Tax Lien

Escrow funds:

1. Amounts covered by

a Notice of State

Tax Lien

2. Amounts not

covered by a Notice

of State Tax Lien

1. Issue a demand to clear

the Notice of State Tax

Lien

2. NOL

Financial institution

accounts:

•

Banks

•

Credit Unions

•

Savings and Loans

NOL

Funds held by Trustees

in bankruptcy

Not attachable, unless they

are funds to be returned to

the taxpayer, then use NOL

Furniture and fixtures –

commercial

Warrant

Furniture and fixtures –

personal and residence

Not attachable

Page 4 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Horse racing purse NOL

Individual Retirement

Account (IRA)

Not attachable

Inheritance Warrant

Insurance dividends NOL

Insurance proceeds –

business:

•

Errors and Omissions

•

Malpractice Insurance

•

Fire Insurance

•

Interruption of Business

•

Personal Injury

Warrant if proceeds are

for personal property

damage

Interest NOL

Lien on cause Refer to SPS, SPG

Life insurance policy –

loan cash value

Warrant

Liquor – unopened Warrant

Lottery – proceeds/winnings Offset

Machinery Warrant

Medi-Cal payments Offset

Mobile home – dealer sales Warrant

Motor vehicles –

on-road/off-road

Warrant

Page 5 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Partnership property

Warrant – Partnership property is

not subject to levy for the

individual debt of one of the

partners incurred either prior to

the formation or after the

dissolution of a partnership.

Payments for services

rendered to state agencies

Offset

Perishable items Warrant – Requires special

consideration for storage, board,

care and maintenance, or

immediate sale.

Personal property in

warehouse

Warrant

Personal property

being sold

•

Warrant prior to the sale.

•

NOL to the buyer.

Progress payments

(continuing periodic

payments to taxpayer)

•

Warrant – effective for

two years.

•

NOL – effective for one year.

Promissory note

Warrant

Property in custody of

the law

Property that is no longer required

for security and is to be returned

to the taxpayer is subject to

attachment (i.e., bail posted for a

charge that has been cleared,

property used as evidence, etc.).

See property types in this table for

the method of attachment.

Prosthetic and orthopedic

devices – for taxpayer’s

personal use

Not attachable

Page 6 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Real property:

• Land

• Taxpayer’s personal

residence, including a

mobile home

• Rental

Warrant

Recreational equipment Warrant

Refunds from other state

agencies

Offset

Rent NOL to each tenant

Retirement funds Not attachable

Rolling stock Warrant

Safe deposit box Warrant with drilling instructions.

Sales tax deposit Not attachable unless being

refunded, then offset prior to

refund to the taxpayer.

Security deposits Offset

Stock NOL

Stock in trade Warrant

Surplus funds from third-

party sale

NOL

Tangible personal property Warrant

Page 7 of 9 DE 83 Rev. 1 (4-18)

(INTERNET)

CHAPTER 6 INVOLUNTARY COLLECTION DETERMINATION

TYPE OF

INVOLUNTARY

ACTION

(cont’d.)

IF IDENTIFIED ASSET IS METHOD OF ATTACHMENT

Trailer(s):

•

Camping

•

Freight

•

Motor home

•

Utility

•

Vehicle transport

Warrant

Trusts – family NOL or Warrant

Trusts – held for a

third party

Not attachable:

•

Federal regulations prohibit

the attachment of payroll

withholding.

•

Special bond deposits for