Business E-mail Compromise Survey Report

JPCERT Coordination Center

March 25, 2020

JPCERT Coordination Center

: JPCERT Coordination Center

DN : c=JP, st=Tokyo, l=Chuo-ku, o=Japan Computer

Emergency Response Team Coordination Center,

cn=JPCERT Coordination Center,

: 2020.06.10 09:27:13 +09'00'

Table of Contents

1. Introduction ......................................................................................................................................... 4

1.1. Overview .......................................................................................................................................... 4

1.2. Target audience ................................................................................................................................ 4

1.3. Aim of this report .............................................................................................................................. 4

2. What Is Business E-mail Compromise? .............................................................................................. 5

3. Business E-mail Compromise Survey ................................................................................................. 6

3.1. Survey overview ............................................................................................................................... 6

3.2. Survey results .................................................................................................................................. 7

3.2.1. Relevant countries and languages used ....................................................................................... 7

3.2.2. Categorization ............................................................................................................................... 8

3.2.3. Methods ...................................................................................................................................... 10

Forgery of invoices .............................................................................................................. 10

Timing of misrepresentation ................................................................................................ 11

Impersonation...................................................................................................................... 11

Account hijacking ................................................................................................................ 12

Possible involvement of parties familiar with internal affairs ................................................ 12

3.3. Losses incurred .............................................................................................................................. 13

3.4. Lessons learned from the survey results ........................................................................................ 14

3.4.1. Increasingly complicated structure .............................................................................................. 14

3.4.2. Existence of related incidents ...................................................................................................... 16

3.4.3. Difference of position ................................................................................................................... 16

3.5. Countermeasures ........................................................................................................................... 17

3.5.1. Operational approach .................................................................................................................. 17

System ................................................................................................................................ 17

Training ............................................................................................................................... 18

Review of payment process ................................................................................................ 18

3.5.2. Technological approach ............................................................................................................... 18

Detection function ................................................................................................................ 18

Monitoring for lookalike domains ......................................................................................... 19

4. Business E-mail Compromise Abroad ............................................................................................... 19

4.1. International efforts ......................................................................................................................... 19

4.2. Efforts made by financial institutions .............................................................................................. 20

4.3. Cases of arrest ............................................................................................................................... 20

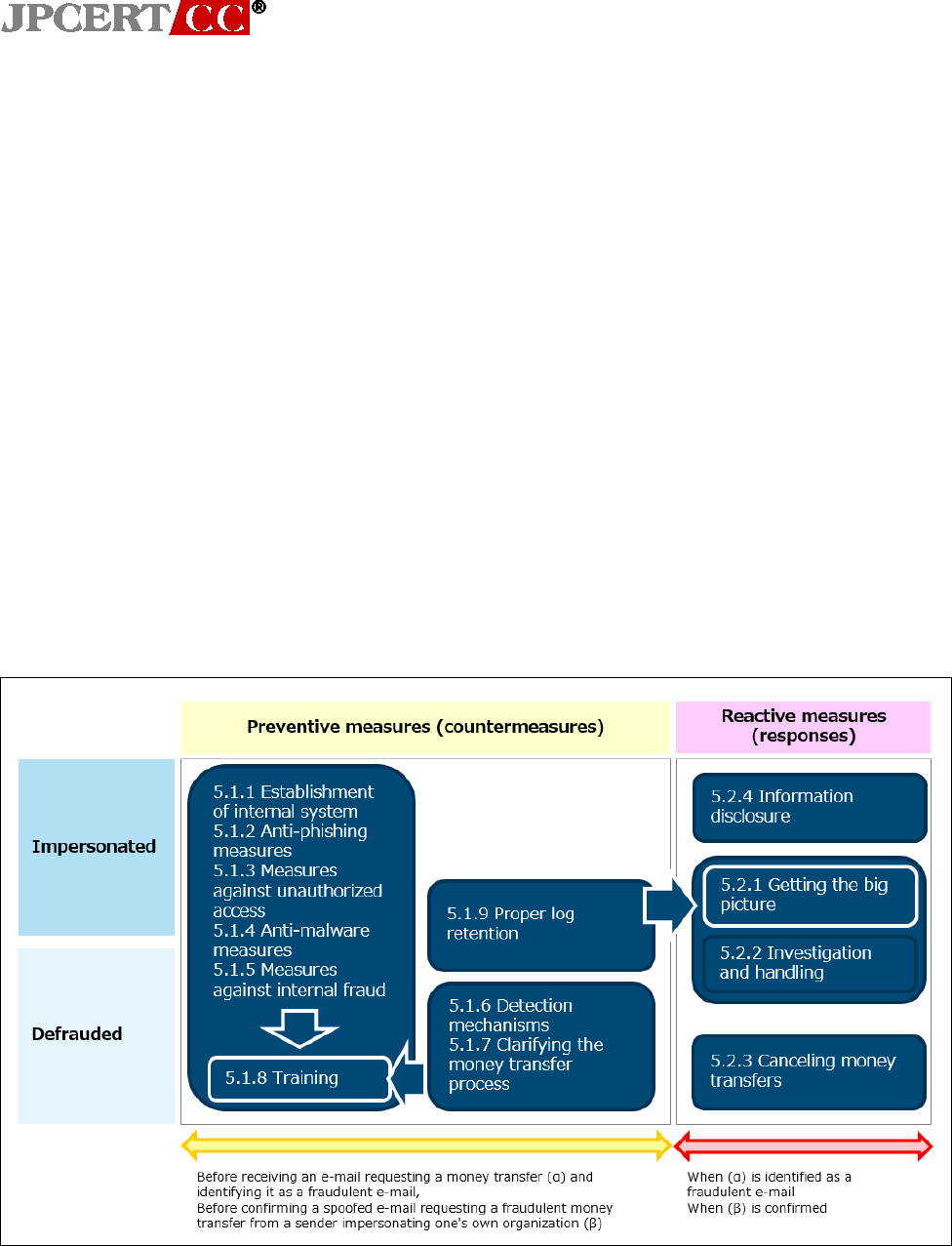

5. Countermeasures and Responses .................................................................................................... 22

5.1. Pre-incident measures (countermeasures) .................................................................................... 23

5.1.1. Establishment of internal system ................................................................................................. 23

5.1.2. Anti-phishing measures ............................................................................................................... 23

5.1.3. Measures against unauthorized access ...................................................................................... 23

5.1.4. Anti-malware measures ............................................................................................................... 23

5.1.5. Measures against internal fraud .................................................................................................. 24

5.1.6. Detection mechanisms ................................................................................................................ 24

5.1.7. Clarifying the money transfer process ......................................................................................... 27

5.1.8. Training ....................................................................................................................................... 27

5.1.9. Proper log retention ..................................................................................................................... 28

5.2. Reactive measures (responses) ..................................................................................................... 29

5.2.1. Getting the big picture ................................................................................................................. 29

5.2.2. Investigation and handling of prior incidents ............................................................................... 30

5.2.3. Canceling money transfers made in response to BEC ................................................................ 30

5.2.4. Information disclosure when impersonated in a BEC scheme .................................................... 30

6. Conclusion ........................................................................................................................................ 31

7. Acknowledgment ............................................................................................................................... 33

4

1. Introduction

1.1. Overview

This report summarizes the findings of a survey carried out by the JPCERT Coordination Center

(JPCERT/CC) to clarify the losses caused by Business E-mail Compromise (BEC), and what organizations

should do to protect themselves against this type of scam.

1.2. Target audience

This report targets the following readers.

Information system department (IT department) staff

Information security department (CSIRT) staff

Management members (mainly those in charge of system, accounting, risk, or legal department),

etc.

1.3. Aim of this report

BEC has become widely known since the Federal Bureau of Investigation (FBI) released information about

it in 2015, but losses linked to BEC scams continue to grow. According to the data on incidents reported to

the FBI's Internet Crime Complaint Center (IC3), the combined number of victims inside and outside the

US was 22,143 with losses amounting to approximately 3.1 billion US dollars ($3,086,250,090) from

October 2013 to May 2016, but the corresponding figures for the period from June 2016 to July 2019 surged

to 166,349 and 26.2 billion US dollars ($26,201,775,589), respectively.

In Japan, organizations such as Information-technology Promotion Agency, Japan (IPA), the National

Police Agency, and Trend Micro started releasing information about BEC to alert the public in 2017. Around

the end of 2017, losses incurred by Japanese organizations due to BEC scams were widely publicized,

and in 2018 businesses started receiving scam e-mails in Japanese, highlighting the need to be

increasingly vigilant against the BEC threat in Japan.

In light of these circumstances, JPCERT/CC decided to conduct a survey and interviews on BEC, thinking

it was necessary to clarify the actual nature of the threat and, based on its findings, disseminate information

about measures and responses that organizations in Japan should take in order to minimize losses related

to BEC.

This report provides information about specific actions that will be effective against BEC, considering how

this threat has developed and transitioned based on the survey results along with information publicly

available.

5

2. What Is Business E-mail Compromise?

Various organizations have provided information about BEC. While definitions vary, they all agree on its

general description: "a scam intended to trick businesses into making money transfers by sending spoof e-

mails impersonating suppliers or business partners."

IC3 started releasing alerts on BEC from around early 2015, and in January 2015, it described BEC as "a

sophisticated scam targeting businesses working with foreign suppliers and/or businesses that regularly

perform wire transfer payments."

1

Other types of e-mail scam include "romance scams" in which scammers

try to lure victims into a fake relationship and then later ask for money, and "lottery scams" in which

scammers ask the recipients to send them money saying they will notify lottery numbers in advance. It is

also known that criminal organizations that perpetrate BEC scams against businesses also commit

romance and lottery scams mainly targeting individual victims.

2

Although BEC is sometimes put in the

same category of scam as romance and other types of e-mail scam, this report will focus on BEC as it

differs from other e-mail scams in targets and methods used. In fact, statistics released by the FBI's IC3

tally the victims and losses for BEC and romance scams separately.

3

In this report, BEC refers to scams intended to trick businesses into making money transfers by sending

spoof e-mails impersonating suppliers or business partners. (The type of fraud known as phishing is not

included.)

1

Business E-mail Compromise

https://www.ic3.gov/media/2015/150122.aspx

2

281 Arrested Worldwide in Coordinated International Enforcement Operation Targeting Hundreds of Individuals in

Business Email Compromise Schemes

https://www.justice.gov/opa/pr/281-arrested-worldwide-coordinated-international-enforcement-operation-targeting-

hundreds

3

2018 Internet Crime Report

https://pdf.ic3.gov/2018_IC3Report.pdf

6

3. Business E-mail Compromise Survey

3.1. Survey overview

This survey was conducted in the form of a questionnaire prepared by JPCERT/CC to gather details

concerning individual cases of BEC, including failed attempts. The survey was carried out with the help of

12 organizations that supported the aim of the survey, including

Japan Foreign Trade Council ISAC and the

Japan Petrochemical Industry Association, and compiles the information submitted by 117 respondents. In

addition, JPCERT/CC visited six of the organizations that agreed to take the questionnaire and interviewed

key personnel to obtain further information about BEC incidents and measures currently in place to counter

BEC.

Survey Period July 8, 2019 to November 22, 2019

Survey Target

Japan Foreign Trade Council ISAC (supporting organization)

Japan Petrochemical Industry Association (supporting organization)

etc.

Method Questionnaire and face-to-face interviews

Survey Name Business E-mail Compromise (BEC) Survey

Survey Overview Survey of BEC incidents

observed and actions taken at each

organization, etc.

No. of Responding

Organizations

Questionnaire: 12; Interviews: 6

7

3.2. Survey results

3.2.1. Relevant countries and languages used

[Table 1] lists relevant countries (countries where

organizations involved in BEC incidents are

located) and languages used.

While relevant countries may depend on the

business model of the organization being surveyed,

many cases involved transactions with a location or

business partner in Asia.

English was by far the language most frequently

used, and Japanese was used in some cases.

[Table 1: Relevant countries and languages used]

Relevant

country

Cases Language

used

Cases

Japan 41 English 108

China 19 Japanese 8

United States 18 Chinese 2

India 11 Indonesian 1

Singapore 10 French 1

South Korea 7 Portuguese 1

Thailand 6

* Cases involving multiple locations and languages are counted

multiple times.

<Other relevant countries/region>

Indonesia, United Kingdom, Germany, Brazil, Vietnam, Malaysia, Australia, Sri

Lanka, Belgium, Mauritius, Turkey, the Philippines, Taiwan, UAE, Uzbekistan, Egypt,

Qatar, Sweden, Spain, Tunisia, Dubai, Haiti, Pakistan, Panama, Belarus, Myanmar,

Mexico, Laos, and Russia

8

3.2.2. Categorization

BEC incidents can be categorized using various approaches, but this report adopts an approach that

follows the "five types of Business E-mail Compromise"

4

defined by IPA.

[Table 2: IPA's "five types of Business E-mail Compromise" and types of incident identified]

IPA's "five types of Business E-mail Compromise" Categorization

Result

[Type 1] Forgery of an invoice from a business partner

Identified

E.g., Scammer sends a fake invoice (account for wiring money into) during the course of

exchanging e-mails on a business transaction

[Type 2] Impersonation of a business manager, etc.

Identified

E.g., Scammer impersonates a business manager and gets the victim to transfer money

into a fake bank account

[Type 3] Fraudulent use of a compromised e-mail account

Identified

E.g., Scammer hijacks an e-mail account and commits fraud on a business partner

[Type 4] Impersonation of an external third party with authority

Not identified

E.g., Scammer pretends to be a lawyer acting on the instructions of the president or other

such person and requests money to be transferred

[Type 5] Acquisition of information by fraudulent means, apparently in preparation for a scam

Identified

E.g., Scammer impersonates an executive or HR department staff and obtains employee

information to be used for committing fraud

Of the five types defined by IPA, incidents falling under four types excluding type 4 ("Impersonation of an

external third party with authority") were identified. The most common type was type 1 ("Forgery of an

invoice from a business partner"), making up approximately 75% of the total. The next most common type

was type 2 ("Impersonation of a business manager, etc."), with impersonated positions including CEO and

CFO. There were also some cases combining multiple types, such as a fraudster gaining access to the e-

mail account of an officer and using it to have money transferred into a fake bank account.

4

Cases of Business E-mail Compromise (BEC) and Security Alert (Follow-up Report) (Japanese)

https://www.ipa.go.jp/files/000068781.pdf

9

It is also important to mention about the existence of

impersonated organizations. Reports and articles

currently published on BEC often focus on organizations

whose money has been stolen (or nearly been stolen).

However, it must be noted that while there are

organizations that have received scam e-mails, there are

also organizations that have been impersonated. As

shown in [Figure 1], this trend is clearly visible

among the cases identified in the survey as well, and

there were nearly as many organizations that received a

scam e-mail as those that were impersonated.

[Figure 1: Difference in position with respect to BEC]

the difference in position with respect to BEC will be key

to considering countermeasures and responses.

10

3.2.3. Methods

Forgery of invoices

Of the "five types of Business E-mail Compromise," the most

common type was type 1 ("Forgery of an invoice from a

business partner"). There were also many cases in which

invoices used in actual transactions were falsified and used to

perpetrate BEC scams. The survey asked if there was an

attachment in each case, and if there was, what file format was

used and the date and time the file was created. The results

showed that PDF files were used in 90% of the cases, and that

many of the files were created using free conversion software [Figure 2: Attachment file types]

or conversion websites. Also, in some cases the date and time

created recorded in the document properties are in a different

time zone from the relevant country, so this information can

also be used to spot BEC.

[Table 3: Examples of software and websites used to convert attachment files to PDF]

PDF Conversion Software

PDF Conversion Websites

3-Heights™ Document Converter

Convert-JPG-to-PDF.net

Adobe Acrobat

Zamzar

Excel for Office 365

Online PDF-Converter

GPL Ghostscript

pdf-tools.com

Microsoft Word

Sejda SDK

Quartz PDF Context

PDFill FREE PDF Tools

PDFlib

RAD PDF management tool

SAMBox

Skia/PDF

11

Some of the falsified invoices contained signs of

forgery, such as something odd in the billing

details and indications that text boxes were simply

copied and pasted. If examined carefully, these

signs could have been identified and losses

prevented.

E-mails asking to have money wired into a

different account by replacing a legitimate invoice

with a forged one, for example, often have a

reason attached for the change. The table to the

right lists the reasons given for why the account

needs to be changed in the cases identified in the survey. Although they all look legitimate, it must be noted

that these were reasons given in actual cases of BEC. Many of the cases reported in this survey used

"annual audit" as a reason that the normal account could not be used.

Timing of misrepresentation

Attackers tend to give instructions to

change the account during the process

between issuing an invoice and making a

payment by sending a forged invoice and

other means. BEC has occurred during the

course of concluding a new business

contract as well. Some respondents have

claimed that such cases are difficult to spot

since, unlike with existing business

transactions, they offer no opportunity for

noticing any irregularity through

comparison with an existing account and so

on.

Impersonation

Of the "five types of Business E-mail Compromise," the next most common type was type 2 ("Impersonation

of a business manager, etc."). As discussed in 3.2.2. Categorization, the survey found cases in which CEO

and CFO were impersonated, but there was also a case using a new approach in which the attacker

impersonated a business manager and a secretary. In this case, a person identifying him/herself as a

[Table 4: Reasons given for account change]

<Reasons for account change>

Account cannot be used due to an annual audit

Main account is under inspection due to a tax

issue

Financial records are being created for the main

account to issue a check

Foreign exchange rates are being adjusted due

to system reform

Bank merger, etc.

[Table 5: Timing of misrepresentation]

Timing of Misrepresentation

Before issuing an invoice

13

Misrepresentation during the process before

issuing an invoice

When issuing an invoice

33

Misrepresentation during the process of issuing an

invoice

Before transferring money

29

Misrepresentation during the process between

issuing an invoice and transferring money

After transferring money

3

Misrepresentation after transferring money

Other

28

Misrepresentation that occurred regardless of the

payment process

12

secretary first sent an e-mail saying the CEO will give instructions on a business transaction the next day,

and that he/she (the secretary) will be absent that day. The next day, someone impersonating the CEO

gave instructions to send money. As businesses have become increasingly concerned about and wary of

BEC, it is assumed that the attacker impersonated multiple actors to gain the confidence of the victim.

Impersonation is not limited to type 2 ("Impersonation of a business manager, etc."). There were also many

type 1 ("Forgery of an invoice from a business partner") cases in which scammers impersonated an officer

or employee of the same organization as the victim. Attackers employ the same impersonation methods

used to date, such as using lookalike domains with a different top-level domain (TLD) or altered character

strings.

Account hijacking

The questionnaire also asked about the e-mail services used by the perpetrators of BEC scams to send e-

mails. While there were some cases in which an account created with a free e-mail service was used to

carry out attacks, a number of cases involved fraudulent use of hijacked e-mail accounts as defined in type

3 ("Fraudulent use of a compromised e-mail account") of the "five types of Business E-mail Compromise."

In the survey, none of the cases involved a breach of an account set up with an e-mail service administered

by the organization in question. However, there were breaches of accounts using free e-mail services, as

well as cloud-based e-mail services introduced independently by overseas office. Interview respondents

listed brute force attacks and the use of credentials stolen by means of phishing or malware as reasons for

the breaches of accounts.

Possible involvement of parties familiar with internal affairs

Some of the cases attempted BEC scams using

information that only related parties can know.

Examples include "A. Case in which amounts

extremely close to the approval limit were requested

repeatedly" and "B. Case in which the same

organization was targeted for BEC (received a scam

e-mail) after suffering losses in an impersonation

scam" (see the figure below). In some cases,

attackers do collect preliminary information before

perpetrating BEC scams. However, given that some

BEC scams are carried out using information

external parties cannot possibly know, such as the approval limit of payment amounts and details of multiple

transactions, the possibility of involvement of parties familiar with internal affairs cannot be denied.

A. Case in which amounts extremely close to the

approval limit were requested repeatedly

13

B. Case in which the same organization was targeted for BEC (received a scam e-mail) after suffering losses

in an impersonation scam

[Figure 3: Cases in which parties familiar with internal affairs could be involved]

3.3. Losses incurred

In the cases surveyed, scammers basically requested

money transfers denominated in a foreign currency,

but a majority of the cases were identified as BEC

scams before incurring any actual losses.

How these cases were identified and the reasons

losses were avoided are described below.

(1) The person who was exchanging e-mails noticed

that it was a BEC scam

(2) Money could not be transferred because the

specified account was frozen or for some other

reason

(3) The person involved noticed that it was a scam

after receiving a reminder from the business partner and was able to cancel the money transfer

In most cases, persons involved notice the scam during the course of exchanging e-mails, and as soon as

they feel anything suspicious, they check with the counterparty using a means of communication other than

e-mail (phone, messaging app, etc.) and avoid losses.

[Figure 4: Timing in which losses were avoided]

14

Examples of clues drawn from the

survey results are listed in the table

to the right. Unnatural local

language is a level of language that

local staff feel unnatural and may

be difficult for people like overseas

representatives to notice.

While losses were avoided in many cases, there were also cases in which losses amounting to millions or

even tens of millions of yen were incurred. Amounts of losses vary because the amounts requested differ

depending on the details of transaction. This suggests that attackers who perpetrate BEC scams fully

understand the transaction details.

In some cases, the account where money was sent was later frozen, and a portion of the losses was

returned according to the balance of the account. There were also some cases in which losses could be

recovered by filing a crime insurance claim. However, there are issues as well. One is complicated

procedures for recovering losses. To prove losses in a BEC scam, many documents need to be submitted

to banks, insurance companies, and so on. In addition, when an overseas financial institution is involved,

the necessary procedures often must be handled in the local language and may entail other complexities,

adding considerably to the burden. Another issue is the timing of reversal. If losses are returned in the next

accounting period, the returned amount will be treated as proceeds on the books. There appears to be

cases in which losses cannot be recovered for this reason.

The total amount (converted into yen) requested in the BEC scams reported in this survey, regardless of

whether losses were incurred, was approximately 2.4 billion yen.

3.4. Lessons learned from the survey results

The following lessons were learned through this survey.

■ BEC scams do not always take place only between the attacker and the affected organization; there

are also cases involving multiple organizations and/or persons

■ Some BEC incidents occur in connection with a preceding incident

■ Measures against BEC must address the risk of being impersonated as well as being tricked

3.4.1. Increasingly complicated structure

Many of the reports and articles currently published on BEC discuss cases occurring on a one-to-one basis,

such as between two different companies or between an officer and employee.

While many of the cases reported in this survey were on a one-to-one basis, there were also cases that

involved multiple persons and/or organizations on one side or both sides. Here are some examples.

[Table 6: Examples of clues that helped detect scams during the

course of exchanging e-mails]

<Examples of clues>

Request for payment already made, invoice that looks unnatural

Request for money transfer to an unfamiliar region

Frozen bank account

Unnatural local language, etc.

15

C. Case involving another group organization

Overview

■ Occurred during a transaction process between

a local subsidiary (country S) and an external U

■ Payment from the external U to the local

subsidiary (country S) was stolen

Method

■ The attacker impersonated the local subsidiary

(country S) and

instructed another local

subsidiary (country T) to request the external U

to change the account

■ The local subsidiary (country T) requested the

external U to change the account

■ The external U sent a payment to a fake account

Key

points

■ Communication between the local subsidiary

(country T) and external U was legitimate

■ Confidence was gained using another group

organization

D. Case handled through brokers

Overview

■ Occurred during a transaction process

between business company N and supplier P

■ Payment is made through brokers

■ Payment from broker R to a shipowner was

stolen

Method

■ The attacker impersonated the shipowner and

set up a fake payment account

■ Broker R sent a payment to the fake account

Key

points

■ No direct contract between business company

N and supplier P

■ Multiple organizations are involved without any

direct contract, so how to split the losses is at

issue

[Figure 5: Examples of cases in which multiple persons and/or organizations were involved]

These were cases in which multiple persons and/or organizations were involved, with third parties

intervening in the transaction process and, as a result, BEC occurring between organizations with no direct

contractual relationships.

Such structural relationships may make it difficult to identify causes and require considerable effort to

16

resolve legal issues like the proportion of losses to be borne. In any case, when thinking about BEC, it is

necessary to keep in mind that multiple actors and organizations may be involved, instead of thinking in

terms of a simple structure of a perpetrator and victim.

3.4.2. Existence of related incidents

As a rule, it is difficult for anyone other than the persons in charge or other related parties to obtain the

details of a transaction between organizations. However, there were many cases in which the attacker

appeared to have known the transaction details in advance, as suggested, for example, by the broad range

of payment amounts requested from tens of thousands of yen to hundreds of millions of yen, or the fact

that a forged invoice was received immediately after a legitimate invoice was sent.

One organization found in an internal survey that a user had accessed a phishing site and entered the

credentials of the e-mail service immediately before the BEC scam came to light, which it believed led to

the leakage of transaction details. Another organization found in an internal investigation conducted later

that it had been infected with malware.

In both cases, the acts in question took place before the BEC scam was uncovered. When faced with an

incident, a victim tends to focus on the event unfolding before their eyes, and be oblivious of why the

attacker has the transaction details or how they came by the e-mail account information. However, it is

important to be aware of the possibility that information obtained in a prior security incident may have been

exploited to perpetrate a BEC scam.

If a security incident such as a breach of account or information leakage occurs at your own organization

or at a related party, it is recommended that appropriate steps be taken to urge vigilance against BEC by

issuing a security alert within the organization, in view of the possibility that the leaked information may be

used in a BEC scam.

3.4.3. Difference of position

Another point that should be kept in mind is that while you could become a victim, one could also be helping

the perpetrator. In cyber security incidents, infrastructure of one’s own organization could be used as a

springboard for carrying out cyber attacks. Likewise, any organization can unwittingly become an

accomplice in BEC scams as well. At the same time, this is a problem that is easy to be overlooked as

organizations tend to prioritize their own defenses and fail to implement countermeasures in a timely

manner.

As stated in 3.2.2 Categorization, in this survey there were nearly as many organizations that received

scam e-mails as those that were impersonated. Given that BEC is a type of scam connected with business

transactions, the organization that incurred financial losses (defrauded organization) might file a civil action

against the impersonated organization and seek compensation for damages. In considering measures

against BEC, it is necessary to address not just the risk of incurring losses by paying money to fraudsters,

but also the risk of being impersonated in view of a possible claim for damages from the affected

17

organization, and to be prepared in case such a claim is made.

3.5. Countermeasures

So far, the specific methods used, characteristics, and losses incurred that came to light through the survey

have been discussed. The interviews also asked about measures taken against BEC, and roughly two

types of approach have been found: operational and technological. This section will discuss measures

implemented by organizations from these perspectives.

3.5.1. Operational approach

System

To prevent losses from BEC, it is necessary to detect the scam. In many cases, a company's IT support

desk or other department responsible for IT troubles is in charge of handling reports and consultations

related to BEC incidents since they stem from e-mail. When there is no specified contact point, these

reports and consultations are directed to the sales department, accounting department, or elsewhere as

determined by the user. There is a concern that these BEC cases could be buried among other matters

and go unnoticed.

Organizations that handle BEC effectively often have separate contact points for reports and consultations

concerning IT troubles and e-mails, and regularly share information about BEC with general affairs, legal,

accounting, sales, and other related departments so that relevant information is channeled into

departments responsible for handling BEC.

[Example 1] System that separates reporting and

consultation channels

[Example 2] System that ensures all BEC scams are

identified

[Figure 6: Systems of organizations that handle BEC effectively (examples)]

18

Training

The survey revealed that many organizations provide training described in reports currently published on

BEC.

Every organization that provides training includes it in the training on suspicious e-mails with an eye on

targeted attacks and cyber attacks.

Some organizations provide company-wide training through e-learning while regularly sharing with users

information that requires their attention, such as insights gained through BEC scam e-mails received by

the organization. There are also organizations where legal, financial, and IT departments jointly conduct

group training targeting managers with authority to approve payments, and provide knowledge about IT

and information from multiple perspectives such as laws and regulations of foreign countries, payment flow,

and clues for spotting scams.

Responses on the effects of these initiatives differ for each organization. Organizations that provide group

training have seen some effects, so they are planning to make it available to the entire company in the form

of video content. On the other hand, some organizations, while showing understanding for the necessity of

training, also claimed that initiatives that rely on users are not sufficient, and are focusing on creating a

system that ensures information about incidents is quickly reported.

Review of payment process

Review of payment process has been discussed as a common countermeasure by various public

institutions and security vendors, and some organizations have actually reviewed their processes.

Specifically, they added checks by the accounting department in addition to the sales department to

enhance the payment process.

3.5.2. Technological approach

Detection function

As mentioned in the discussion on the operational approach, BEC scams need to be detected in order to

be prevented. To this end, establishing a system to help recipients identify scams and a simple reporting

scheme will be effective. One organization uses a pop-up function to alert recipients when they have

received an e-mail from a domain that they have not received an e-mail from in the past three months.

Another organization provides a button in the inbox of its e-mail system that enables recipients of suspicious

e-mails to report them with a simple push of a button, making the reporting process hassle-free.

19

Monitoring for lookalike domains

BEC scams often use a domain that closely resembles a legitimate domain ("lookalike domain") for the e-

mail sender address. The use of lookalike domains is not a problem unique to BEC, but one organization

uses a paid service as a countermeasure to monitor the registration status of domains that closely resemble

its own and, when a lookalike domain is identified, send an alert across the company and applying filters

on the e-mail system. According to this organization, a lookalike domain is created in about two days on

average after a legitimate domain is created, and the sheer number of lookalike domains generated each

day makes the effort to counter them endless. As mentioned in 3.2.3.3 Impersonation, there is a wide

variety of patterns for creating lookalike domains, such as using a different TLD or modifying character

strings, so it is understandable that this countermeasure is unlikely to be highly effective.

4. Business E-mail Compromise Abroad

This section discusses the situation surrounding the BEC threat outside Japan and efforts made to combat

it. Various communities have been formed among many organizations and countries in an ongoing effort

to reduce losses linked to BEC. This effort is mainly popular in the United States, where losses from BEC

are growing each year. In a number of publicized cases, individuals suspected of involvement in BEC

schemes have been prosecuted and arrested thanks to cooperation between financial institutions and law

enforcement agencies.

4.1. International efforts

In December 2015, an e-mail group called "The Business Email Compromise List" was founded to fight the

BEC threat.

5

The e-mail group was originally launched with the aim of sharing information about the BEC

threat and analyzing its methods. Later, as the membership grew, it also started engaging in activities to

protect victims.

6

In October 2018, Ronnie Tokazowski, founder and administrator of The BEC List, received

the M3AAWG JD Falk Award in recognition of the group's achievements.

7

Members use the information obtained from the e-mail group to help prevent BEC at their own organizations,

and these include law enforcement agencies, e-mail service providers that have the ability to suspend e-

mail accounts, and financial institutions involved in transferring money. The list of cooperating members

includes security vendors as well, since there are also reported cases of BEC incidents in which the attacker

used malware or other means to steal information from the target organization before requesting fraudulent

money transfers. As it is difficult for a single organization, industry, or even country to combat the threat of

BEC alone, it would be desirable to further promote various forms of cooperation between countries and

5

How Do You Fight a $12B Fraud Problem? One Scammer at a Time

https://krebsonsecurity.com/tag/bec-mailing-list/

6

“Under the Radar” Industry Group Fighting BEC Phishing Receives 2018 M3AAWG JD Falk Award

https://www.m3aawg.org/Rel-FalkAward-2018

7

SilverTerrier: 2018 Nigerian Business Email Compromise Update

https://unit42.paloaltonetworks.com/silverterrier-2018-nigerian-business-email-compromise/

20

organizations.

4.2. Efforts made by financial institutions

In the US, financial institutions are required to report suspicious transactions that may be associated with

criminal activities to the Department of the Treasury through a system called Suspicious Activity Reporting

(SAR), which is used to collect information about suspicious transactions.

8

Reported information is

forwarded to the Department of the Treasury's Financial Crimes Enforcement Network (FinCEN) and used

by FinCEN and law enforcement agencies to conduct criminal investigations. These efforts enable FinCEN

and law enforcement agencies to cooperate and, in some cases, recover funds. In particular, funds are

often successfully recovered if reported within 24 hours of payment. FinCEN requests US-based financial

institutions to report the following information about BEC schemes to facilitate investigation.

[Table 7: Information about BEC schemes that FinCEN requests US-based financial institutions to report]

Transaction Details Scheme details

(1)

Dates and amounts of suspicious

transactions

(1) Relevant e-

mail addresses and associated IP

addresses with their respective timestamps

(2)

Sender's identifying information,

account number, and financial

institution

(2) Description and timing of suspicious e-mail

communications and involved parties

(3)

Beneficiary's identifying information,

account number, and financial

institution

(3) Description of related cyber-events

(a) E-mail autoforwarding

(b) Inbox sweep rules or sorting rules

(4)

Correspondent and intermediary

financial institutions' information, if

applicable

(c) A malware attack

(d) Authentication protocol that was compromised

4.3. Cases of arrest

In 2018, the FBI cooperated with the law enforcement agencies and private organizations in a number of

countries in a large-scale effort to dismantle international BEC schemes. This operation—named Operation

WireWire—was carried out over a period of six months and resulted in 74 arrests in the US, Nigeria,

Canada, Mauritius, Poland, and other countries.

9

In Operation reWired, undertaken a year later in 2019, a

total of 281 arrests were made, including in Japan. In a different case reported the same year, the Tokyo

8

Updated Advisory on Email Compromise Fraud Schemes Targeting Vulnerable Business Processes

https://www.fincen.gov/sites/default/files/advisory/2019-07-16/Updated BEC Advisory FINAL 508.pdf#page=9

9

International Business E-Mail Compromise Takedown

https://www.fbi.gov/news/stories/international-bec-takedown-061118

21

Metropolitan Police Department cooperated with the FBI in an investigation that resulted in the arrest of

Japanese nationals suspected of helping an international criminal organization perpetrate a BEC scam.

Cooperation with law enforcement agencies is essential to exposing cases of fraud like these. With respect

to the threat of BEC as well, it is hoped that further cooperation between law enforcement agencies and

private organizations will lead to more arrests and deterrence of criminal activities through announcement

of arrests.

22

5. Countermeasures and Responses

BEC scams are difficult to prevent only with countermeasures implemented by the IT department. The

accounting department which is responsible for transferring money must identify suspicious payment

requests and ask the requesting party for confirmation. If a business partner incurs losses due to a BEC

scheme in which the name of a department or individual of one's own company was used, the IT department

may be able to prove the absence of negligence on the part of the company by analyzing logs and other

data. In this manner, BEC must be handled as an issue for the entire organization by combining the

technical knowledge and skills provided by the IT department with actions taken by relevant departments

according to their functions.

This chapter discusses measures against BEC in terms of preventive measures (countermeasures) and

reactive measures (responses).

While each organization has a different definition for incidents, this report categorizes preventive and

reactive measures according to their timing, that is, whether they are taken before or after receiving an e-

mail requesting a money transfer and identifying it as a fraudulent e-mail, or before or after confirming a

spoofed e-mail requesting a fraudulent money transfer from a sender impersonating one's own organization.

[Figure 7: BEC countermeasures and responses]

23

5.1. Pre-incident measures (countermeasures)

5.1.1. Establishment of internal system

If the internal system and escalation rules for responding to confirmed or suspected cases of BEC are

established, the organization can respond rapidly. With a shared awareness of the possibility of a BEC

attack, organizations should establish a system that facilitates collaboration between the accounting

department which requests financial institutions to make money transfers, IT department which is

responsible for e-mail and system operation, legal department which responds when a case involves legal

issues, and sales department which undertakes negotiations with outside business partners. As the survey

results show, most BEC schemes occur outside Japan, so organizations should also have a communication

system set up and tested with overseas locations.

5.1.2. Anti-phishing measures

Organizations using Office 365 or other web-based e-mail services are at risk for having credentials stolen

through phishing. When credentials are stolen and e-mail accounts are hijacked, attackers will be able to

obtain full knowledge of communication with business partners based on past e-mail exchanges, and send

e-mails masquerading as the account holder. Users should be trained and educated on how to identify

phishing and prevent credentials from getting stolen.

10

5.1.3. Measures against unauthorized access

Authentication of e-mail accounts may be breached by a brute force attack or other means. To prevent e-

mail accounts from getting hijacked, measures to enhance authentication such as the use of strong

passwords, prohibition of reusing passwords, and introduction of multi-factor authentication are

recommended for e-mail services.

5.1.4. Anti-malware measures

There were some cases in which attackers used malware with a function for collecting information to steal

relevant information from the target organization as a preparatory step for making a fraudulent money

transfer request. For this reason, organizations must have measures in place to prevent malware infections

and, in case of an infection, to detect malware communications with external servers.

10

Anti-phishing Guidelines (Japanese)

https://www.antiphishing.jp/report/pdf/antiphishing_guide.pdf

24

5.1.5. Measures against internal fraud

As discussed in "3.2.3.5 Possible involvement of parties familiar with internal affairs," the possibility of

involvement of parties familiar with internal affairs cannot be denied in BEC scams in which attackers make

repeated requests to different targets for varying amounts of payment. Parties familiar with internal affairs

include officers, employees, former officers/employees, and business partners. When devising

countermeasures, organizations should consider cases of both unintentional involvement and involvement

as the main culprit or an accomplice.

Measures against cases of unintentional involvement include ensuring employees are fully aware that they

must not leak internal information to outside parties, and restricting access rights so that only users who

need to access or work with necessary information may do so. As for involvement in BEC schemes as the

main culprit or an accomplice, it is not realistic to expect individuals who engage in such practices to act

on their conscience. Therefore, organizations should show their stance toward internal fraud through penal

provisions and so on, make it difficult to conduct criminal acts by restricting employees from bringing their

own devices and storage media or by monitoring access logs, and reduce the reward that can be gained

by engaging in criminal acts.

The "Guidelines for the Prevention of Internal Improprieties in Organizations"

11

published by IPA sets forth

basic policies as well as specific measures including technological management, securing evidence, and

follow-up measures. Please read it through when devising countermeasures.

As for former officers and employees, who rarely stay in touch with the organization once they have retired,

it is desirable to take measures as much as possible while the individuals are employed. In addition to

having them sign a written pledge and quickly deleting unnecessary IDs, more in-depth measures such as

checking the operation logs of retiring employees for any improper removal of information are effective.

Since the handling at the time of retirement may be more uncertain overseas than in Japan due to

difference of customs, organizations should maintain active involvement with regard to overseas locations,

for example, by requesting submittal of evidence indicating implementation of countermeasures targeting

retirees.

5.1.6. Detection mechanisms

Although it would be possible to prevent losses from BEC scams if e-mails requesting fraudulent money

transfers could be blocked and kept from reaching their intended recipients, most of them do not have any

malware attached or contain any fraudulent URL and therefore cannot be mechanically removed or blocked

using anti-virus software or other such means. Moreover, many scam e-mails are extremely sophisticated

and made to look like legitimate business e-mails, making them difficult to filter as spam.

To detect BEC scam e-mails that reach an organization and prevent losses, it might help recipients

11

Guidelines for the Prevention of Internal Improprieties in Organizations

https://www.ipa.go.jp/files/000045873.pdf

25

recognize e-mails requesting fraudulent money transfers by visually alerting them using system functions,

such as attaching a warning to e-mails sent from a free e-mail address, or displaying a message when an

e-mail is received from a domain not used in recent transactions.

In addition to technological measures, an approach from the aspect of operational processes would also

be effective. In light of the fact that BEC scams take place in the course of a business process, having

relevant personnel compare the process with the proper business process might facilitate identification of

suspicious details. Specifically, it would be effective to create a check sheet that lists the details of a past

transaction and the transaction instructed in an e-mail, and check for any differences. From the perspective

of detecting BEC at an early stage, it is important for check sheets to be created and verified by recipients

of billing e-mails and secondary reviewers.

26

[Table 8: Check items for detecting BEC]

Existing Transaction

(Normal)

E-mail Subject to

Investigation

Anomaly

(1) Requesting party

Sender's organization XXX Co., Ltd. XXX Co., Ltd. □

Sender's name Mr./Ms. ABC Mr./Ms. ABC □

Sender's phone number (xx) xxxx-xxxx (xx) xxxx-xxxx □

Recipient's e-mail address

tantou@△△△cert.or.jp tantou@△△△cert.or.jp

□

Sender's e-mail address

* Taken from the e-mail header due

to possibility of forgery

abc@□□□tech.com abc@□□□tach.com ■

(2) Payment and account information

Payment amount 7,800,000 yen (incl. tax) 7,800,000 yen (incl. tax) □

Financial institution XXX Bank YYY Bank ■

Payment recipient account

information (location)

AAA Branch (Country A) BBB Branch (Country B) ■

Account number xxx-xxxxxxxx yyy-yyyyyyy ■

(3) Related information

■ Time zone

Date/time e-

mail was

sent

+0900 UTC +0100 UTC ■

Date/time attachment

was created

+0900 UTC +0100 UTC ■

(4) Notes and findings

The payment recipient's financial institution, account information, and sender's e-mail address are

different from those used in the existing transaction.

The information security department has confirmed that the dates and times the e-mail was sent and

the attachment file was created are in a different time zone from the existing transaction.

It appears that a third party is impersonating XXX Co., Ltd. and requesting the recipient to make a

money transfer.

Since the third party is impersonating Mr./Ms. ABC of XXX Co., Ltd. and requesting payment of the

same amount of money as before (7,800,000 yen, including tax), there is a possibility that the third party

has obtained information about the existing transaction.

Both e-mail addresses need to be checked for a possible breach.

tantou@△△△cert.or.jp

abc@□□□tech.com

27

5.1.7. Clarifying the money transfer process

E-mails requesting fraudulent money transfers use various techniques to "trick" the recipient. The text is

often written in a way that unsettles the recipient, for example, by claiming that payment is needed urgently

to rush the recipient, or impersonating a superior or executive to pressure the recipient. To prevent being

tricked into sending money by such tactics, it is necessary to incorporate a system that enables secondary

review from an objective standpoint into the company's money transfer process. It goes without saying that

money transfers should always be processed well ahead of the schedule.

5.1.8. Training

Generally, security measures do not achieve sufficient results due to a lack of awareness on the part of the

users, lack of understanding of specific steps for implementing the measures, and so on. To put users on

the alert, and have them learn the way to address the threat, repeated training is needed.

As for measures against BEC, it is important to alert the users of the possibility of getting involved in a

scam, and have them understand the key points that they should look out for to avoid being tricked by

highlighting some of the typical methods used.

The table below lists some telltale signs that help identify BEC scam e-mails according to findings from this

survey.

[Table 9: Telltale signs that help identify e-mails and messages related to BEC]

□

Routine e-mail sent from an e-mail address different from the one used before

□

Routine e-mail sent during different hours or with different text (wording, expressions,

etc.) from previous messages

□

E-mail is received near the end of business hours or right before the weekend, and

requests an irregular handling at a rush

□

First e-mail received from a company with no past dealings

□

E-mail received from a superior or executive giving instructions, with no prior contact by

a means other than e-mail

□

Money transfer is being requested to an account never used before

By highlighting telltale signs like these along with actual case examples, it is possible to cultivate skills for

identifying BEC. Moreover, by requiring the use of the check sheet discussed in "5.1.6 Detection

mechanisms" when the personnel who receive e-mails from outside the company requesting money

transfers request the responsible department to send money, it is possible to raise the detection rate of

BEC.

Even e-mails like those shown in Table 9 could be legitimate business e-mails unrelated to BEC, it is

desirable to suspect BEC then check with the other party using a means other than e-mail (e.g., by phone

28

or in person). While such measures may take time and effort, the other party will most likely show

understanding as rational precaution. It must also be ensured through training that, when checking by

phone, the relevant personnel use a phone number obtained by exchanging name cards or other means,

not the contact number given in the e-mail requesting a money transfer.

5.1.9. Proper log retention

During the course of incident handling, operation logs and other records are checked to understand the

situation or as part of the investigation. BEC is no exception. If e-mail and system logs are not properly

retained, it may not be possible to identify the cause or understand the situation. In one case, for example,

the audit logs of e-mail accounts were not properly recorded, so only recent login history was available,

and the evidence of an account breach by an attacker could not be confirmed. In another case, the recipient

deleted a suspicious e-mail, making subsequent investigation difficult.

12

In impersonated cases, retention of e-mail and system logs are important from the perspective of dealing

with external parties as well. When the defrauded organization claims compensation for damages, it is up

to the impersonated organization to prepare evidence to counter the claim.

If one's own organization was tricked into transferring money and wishes to request cancellation of the

money transfer, the financial institution may request grounds for cancellation (e.g., data proving that the

transaction in question was made in connection with a BEC scam). Accordingly, data such as e-mail and

system logs might later be necessary to understand the situation or negotiate with external parties, so it is

desirable to establish rules for retention and properly retain relevant data.

Specifically, e-mail logs and e-mail account audit logs including login history should be obtained, given that

BEC takes place via e-mail. It is also recommended that communication logs of proxy servers, firewalls,

and so on and operation logs such as Active Directory be obtained, assuming that other incidents may be

related.

Note that it might be necessary to configure settings to output logs, and it is also necessary to secure a

place for storing logs. Retention period is another issue that must be considered along with the storage

location. Given that losses from BEC come to light when an outstanding payment is pointed out, the

investigation covers a relatively short time period. However, when investigation of related incidents is taken

into account, logs must be examined for a considerable period of time.

JPCERT/CC recommends that logs be retained for at least one year taking advanced cyber attacks (APT

attacks) into account, based on its experience supporting incident response. A similar retention period

would be appropriate for BEC as well.

13

12

Incident Response Casefile – A successful BEC leveraging lookalike domains

https://research.checkpoint.com/2019/incident-response-casefile-a-successful-bec-leveraging-lookalike-domains/

13

How to Use and Analyze Logs in Dealing with Advanced Cyber Attacks (Japanese)

https://www.jpcert.or.jp/research/apt-loganalysis.html

Preparing for Advanced Persistent Threats (APT): A Process Guide for Companies and Organizations (Japanese)

https://www.jpcert.or.jp/research/apt-guide.html

29

5.2. Reactive measures (responses)

5.2.1. Getting the big picture

When an e-mail requesting a fraudulent money transfer is identified, or when a spoofed e-mail requesting

a fraudulent money transfer from a sender impersonating one's own organization is confirmed, the following

matters must be sorted out with the aim of obtaining an accurate understanding of the situation and

clarifying actions to be taken.

1) Big picture

As recent cases of BEC sometimes involve multiple persons and/or organizations on one side or both

sides, get the big picture of the incident by identifying all the actors and clarifying how they relate to

each other. Using a relationship diagram to visualize the relationships will not only make it easier to

understand the situation, but it will also help prevent misunderstanding between personnel.

2) Organization's position

After grasping the big picture, determine whether one's own organization received a BEC scam e-mail

or was impersonated. In the former case, check if any money transfer was made. If yes, immediately

take steps to cancel the money transfer linked to BEC as described later in 5.2.3. In the latter case as

well, check if any money transfer was made by the defrauded party. If yes, immediately instruct the

party to cancel the money transfer to the financial institution. The impersonated organization should

check the sending domain of the spoofed e-mail regardless of whether the business partner made any

money transfer, and see if it is the domain the organization uses for business operations. It should also

make preparations for information disclosure (see "5.2.4 Information disclosure when impersonated in

a BEC scheme"). If an e-mail requesting a fraudulent money transfer was sent from an e-mail address

with the domain used for business operations, it is highly likely that an e-mail account of the organization

had been breached, so the steps described in "5.2.2 Investigation and handling of prior incidents" should

be initiated.

3) Existence of internal information

Check if information used for carrying out a BEC scam includes information that only a business partner

or internal staff can know. If such information is included, there is a possibility that the attacker may

have viewed e-mails, or information may have leaked due to other incidents, so the steps described in

"5.2.2 Investigation and handling of prior incidents" should be initiated.

These steps should be undertaken by checking e-mail logs and the content of the e-mail requesting a

money transfer, and by interviewing the e-mail recipient. If the check sheet discussed in "5.1.6 Detection

Using Logs to Detect Attacks Against Active Directory and Countermeasures (Japanese)

https://www.jpcert.or.jp/research/AD.html

30

mechanisms" is used regularly, it can be used to understand the situation with efficiency as relevant

information is already compiled.

5.2.2. Investigation and handling of prior incidents

Once the situation is understood, take necessary steps such as changing the passwords of relevant e-mail

accounts assuming they are compromised. In particular, if the e-mail contains details concerning internal

information unique to the organization such as internal rules, there is a possibility that the attacker has

already obtained information about the organization. In that case, the attacker may have viewed past e-

mail exchanges, so the accounts of relevant persons at the organization and business partner need to be

checked for a possible breach of account. If e-mail accounts have been compromised, account settings

need to be reviewed in addition to changing passwords as e-mail forwarding, removal of received e-mails,

and other such settings may have been added. Incident response such as identifying the cause of account

breach and information leakage (e.g., phishing, unauthorized access, and malware infection) should be

undertaken.

5.2.3. Canceling money transfers made in response to BEC

It might be possible to cancel money transfers by making a request to the relevant financial institution. If a

money transfer was requested to a financial institution unaware that it was a BEC scam, it is recommended

that the financial institution be contacted immediately. To cancel the money transfer, the financial institution

might request submittal of information proving the existence of a BEC scheme, investigation results as well

as retained e-mails and logs should be prepared.

5.2.4. Information disclosure when impersonated in a BEC scheme

When it is revealed through external notification or inquiry that one’s own organization has been

impersonated in a BEC attempt, it is vital to disclose relevant facts as quickly as possible to prevent the

spread of damages assuming the possibility that similar attempts are being made against a wide range of

organizations. The information to be disclosed should include specific details such as the sender’s e-mail

address (extracted from the e-mail log considering the possibility of forgery) and payment recipient’s

account information (bank name, branch name, account number, account holder’s name), so that

organizations that received the information may use it to conduct investigation and alert their employees.

Information may be disclosed, for example, by sending individual notifications to business partners by e-

mail or other means, or issuing an alert on the website.

31

6. Conclusion

This survey helped clarify the losses incurred in connection with BEC, countermeasures implemented, and

three points that should be noted with regard to BEC, namely, that multiple actors and/or organizations may

be involved, that there may be a prior related incident, and that a victim may also be a perpetrator. To

prevent losses from BEC, organizations should act with these points in mind.

Countermeasures must address the risk of being impersonated as well as being tricked. One of the

organizations that participated in this survey monitors the registration status of domains that resemble its

domain as a measure against spoofing. This approach entails considerable operation costs, and its

effectiveness including feasibility depends on the organization's resources. Protecting accounts from

attackers by means of common security measures against phishing, unauthorized access, and malware is

also an effective way to address the risk of being impersonated. In addition, organizations are advised to

retain e-mail and system logs in a proper manner in case they become victims of a BEC scam. E-mail and

system logs not only serve as evidence in case an organization is impersonated, but they also can be used

in internal investigation and negotiations with external parties when defrauded.

As BEC scam e-mails do not always contain elements that can be filtered by a system, it is difficult to block

them before they reach the organization. To prevent being tricked under these circumstances, it would be

effective to create a mechanism for detecting e-mails that are not expected to be received. As discussed

in this report, possible detection methods include displaying a warning when an e-mail is received from a

free e-mail address and other system-based support. However, it is also important to approach this risk

with operational measures, such as having personnel familiar with the transaction details or personnel

responsible for processing payments perform a secondary check. This means that BEC is a problem to be

addressed not just by the IT department alone but by the organization as a whole. Perhaps, one may even

go further and say that BEC, which causes damage to an organization through financial losses, is a

management issue that requires management's active involvement.

This report was prepared with the aim of helping reduce losses linked to BEC, which is affecting an

increasing number of Japanese organizations. The report focuses on specific measures that organizations

should take when engaging in a business transaction. We hope that this report will be used by organizations

planning to implement measures against BEC and address its threat by ensuring the abovementioned

points are covered. As for organizations that already have countermeasures in place, it might offer hints for

improvements through comparison with existing measures.

Given the nature of BEC, which is a criminal act and fraud committed with the aim of stealing money, and

its sophisticated techniques, efforts on the part of target organizations alone are not sufficient to reduce it.

To prevent BEC-related losses, law enforcement agencies, e-mail providers, and financial institutions will

also need to cooperate by inhibiting criminal acts through crackdowns on attackers and other efforts,

32

suspending fraudulent e-mail accounts used to carry out BEC scams, and freezing bank accounts. We

hope that public institutions and private organizations in Japan will join hands and set up an environment

for combating BEC, like The Business Email Compromise List overseas. Once we have set up such an

environment, we would like to ask our readers to share information and make active use of it.

33

7. Acknowledgment

In closing, we would like to thank the organizations and their representatives who offered valuable input by

taking part in the survey questionnaire and interviews. We also offer thanks to Mr. Motohiko Sato of Itochu

Corporation, who serves on JPCERT/CC's expert committee, Mr. Nozomi Matsuzaka and Ms. Tomoko

Takeuchi of IPA, and Mr. Kenzo Masamoto of Macnica Networks for their invaluable help in writing and

editing this report.