Prepared by Steer Davies Gleave

Study on the prices and

quality of rail passenger

services

European Commission

Directorate General for Mobility

and Transport

Final Report

April 2016

Our ref: 22870601

Client ref: MOVE/B2/2015-126

Steer Davies Gleave has prepared this material for European Commission, Directorate General for

Mobility and Transport. The copyright of all the material belongs to the EU in accordance with article I.9

the public service contract between the European Commission (Directorate General for Mobility and

Transport) and Steer Davies Gleave. Nevertheless, the information and views set out in this report are

those of the author(s) and do not necessarily reflect the official opinion of the Commission. The

Commission does not guarantee the accuracy of the data included in this study. Steer Davies Gleave has

prepared this material using professional practices and procedures using information available to it at

the time and as such any new information could alter the validity of the results and conclusions made.

Steer Davies Gleave, the Commission or any person acting on the Commission’s behalf may not be held

responsible for the use which may be made of the information contained therein. Any person other than

Steer Davies Gleave or the Commission choosing to use any part of this material shall be deemed to

confirm their agreement to indemnify Steer Davies Gleave and the Commission for all loss or damage

resulting therefrom.

Study on the prices and

quality of rail passenger

services

European Commission

Directorate General for Mobility

and Transport

Final Report

April 2016

Our ref: 22870601

Client ref: MOVE/B2/2015-126

Prepared by:

Prepared for:

Steer Davies Gleave

28-32 Upper Ground

London SE1 9PD

European Commission Directorate

General for Mobility and Transport

Directorate-General for Mobility and

Transport, MOVE B2

Rue de Mot 28

B-1040, Brussels

Belgium

+44 20 7910 5000

www.steerdaviesgleave.com

April 2016

Contents

1 Introduction ....................................................................................................................... 1

Study background ......................................................................................................................... 1

Study objectives and methodology .............................................................................................. 1

Organisation of this report ........................................................................................................... 3

2 The passenger rail market in Europe ................................................................................... 4

European rail travel demand ........................................................................................................ 4

European rail fares ........................................................................................................................ 6

National institutional arrangements .......................................................................................... 19

National railway characteristics .................................................................................................. 27

3 Suburban fares and tickets................................................................................................ 34

Introduction ................................................................................................................................ 34

Suburban fares sampled ............................................................................................................. 34

Suburban fares setting and sharing revenue .............................................................................. 43

Fares structures .......................................................................................................................... 47

Discounts and reductions ........................................................................................................... 51

Smart cards ................................................................................................................................. 53

4 Other fares and tickets ..................................................................................................... 54

Introduction ................................................................................................................................ 54

Regional fares ............................................................................................................................. 54

Interurban fares at distances under 300 kilometres .................................................................. 59

Interurban fares at distances over 300 kilometres .................................................................... 62

Domestic high speed fares.......................................................................................................... 64

International fares ...................................................................................................................... 67

Setting fares ................................................................................................................................ 70

Discounts .................................................................................................................................... 73

Complexity .................................................................................................................................. 77

Clarity and sales channels ........................................................................................................... 78

5 Intermodal competition .................................................................................................... 83

Introduction ................................................................................................................................ 83

Competition with car .................................................................................................................. 84

April 2016

Competition with coach.............................................................................................................. 90

Competition with air ................................................................................................................... 95

Frequency and reliability ............................................................................................................ 98

Summary ..................................................................................................................................... 99

6 Intramodal competition ................................................................................................... 101

Introduction .............................................................................................................................. 101

Competition within an operator or group ................................................................................ 101

Competition for the market...................................................................................................... 104

Competition in the market ....................................................................................................... 109

Findings ..................................................................................................................................... 110

Summary ................................................................................................................................... 118

7 Quality and customer satisfaction .................................................................................... 120

Journey time and feasible day trips .......................................................................................... 121

Service frequency ..................................................................................................................... 127

Punctuality and reliability ......................................................................................................... 130

Station facilities ........................................................................................................................ 134

Customer satisfaction ............................................................................................................... 136

8 Conclusions ..................................................................................................................... 140

Introduction .............................................................................................................................. 140

Factors influencing rail demand ............................................................................................... 140

Summary of findings ................................................................................................................. 142

Conclusions on market liberalisation ....................................................................................... 143

Figures

Figure 2.1: Rail passenger-kilometres by Member State (2013) .................................................. 4

Figure 2.2: Propensity to travel by rail by Member State (2003-2013) ........................................ 5

Figure 2.3: Average annual growth in rail passenger-kilometres (2003-2013) ............................ 6

Figure 2.4: Harmonised Index of Consumer Prices: all transport (2005-2014) ............................ 7

Figure 2.5: Harmonised Index of Consumer Prices: rail transport/all transport (2005-2014) ..... 8

Figure 2.6: Trends in Anytime fares in Great Britain (nominal) .................................................. 10

Figure 2.7: Trends in Off-peak fares in Great Britain (nominal) ................................................. 10

April 2016

Figure 2.8: Trends in Advance fares in Great Britain (nominal) ................................................. 11

Figure 2.9: Rail fare trends in Sweden (2015 prices) .................................................................. 12

Figure 2.10: Rail fare trends in Finland ....................................................................................... 13

Figure 2.11: Fare revenue per passenger-kilometre (2012, excluding Luxembourg) ................ 14

Figure 2.12: Average annual change in revenue per passenger-kilometre (2007-2012) ........... 15

Figure 2.13: Average annual growth rate: peak return fare ....................................................... 17

Figure 2.14: Average annual growth rate: off-peak single ......................................................... 17

Figure 2.15: EU total rail operating costs, revenue and subsidy (2012) ..................................... 23

Figure 2.16: Passenger rail revenue as a proportion of total rail operating costs (2012) .......... 24

Figure 2.17: Average yield and network length .......................................................................... 29

Figure 2.18: Average yield and network density ........................................................................ 29

Figure 2.19: Average yield and urban population ...................................................................... 30

Figure 2.20: Average yield and population density .................................................................... 30

Figure 2.21: Average yield and propensity to travel by rail ........................................................ 31

Figure 2.22: Average yield and car ownership ........................................................................... 31

Figure 2.23: Average yield and GDP per capita .......................................................................... 32

Figure 3.1: Suburban fares: single .............................................................................................. 37

Figure 3.2: Suburban fares: multi-trip ........................................................................................ 37

Figure 3.3: Suburban fares: monthly or 30-day .......................................................................... 38

Figure 3.4: Suburban fares: variation of single and 30-day fares within Member States .......... 42

Figure 3.5: Suburban fares: types of zoning system ................................................................... 48

Figure 3.6: Suburban fares: capital cities with zones ................................................................. 50

Figure 4.1: Regional fares: peak single ....................................................................................... 56

Figure 4.2: Regional fares: off-peak return ................................................................................. 56

Figure 4.3: Regional fares: monthly or 30-day ........................................................................... 57

Figure 4.4: Interurban fares under 300 kilometres: peak single ................................................ 60

Figure 4.5: Interurban fares under 300 kilometres: off-peak return.......................................... 60

Figure 4.6: Interurban fares under 300 kilometres: monthly or 30-day .................................... 61

Figure 4.7: Interurban fares over 300 kilometres: peak single ................................................... 63

Figure 4.8: Interurban fares over 300 kilometres: off-peak return ............................................ 63

Figure 4.9: High speed fare: peak single ..................................................................................... 65

Figure 4.10: High speed fares: off-peak return .......................................................................... 66

April 2016

Figure 4.11: International fares: peak single .............................................................................. 68

Figure 4.12: International fares: off-peak return ....................................................................... 69

Figure 4.13: International and domestic rail fares over 300 kilometres: peak single ................ 70

Figure 4.14: Examples of discounts for children ......................................................................... 76

Figure 5.1: Rail and car costs: regional trips ............................................................................... 85

Figure 5.2: Rail and car costs: interurban trips under 300 kilometres ....................................... 85

Figure 5.3: Rail and car costs: interurban trips over 300 kilometres.......................................... 86

Figure 5.4: Rail and car costs: international trips ....................................................................... 86

Figure 5.5: Rail and car average speeds: regional trips .............................................................. 88

Figure 5.6: Rail and car average speeds: interurban trips under 300 kilometres ...................... 88

Figure 5.7: Rail and car average speeds: interurban trips over 300 kilometres ......................... 89

Figure 5.8: Rail and car average speeds: international trips ...................................................... 89

Figure 5.9: Rail and coach costs: interurban trips under 300 kilometres (lowest observed fare)

.................................................................................................................................................... 91

Figure 5.10: Rail and coach average speeds: interurban trips under 300 kilometres (lowest

observed fare) ............................................................................................................................. 92

Figure 5.11: Rail and coach costs: international trips (lowest observed fare) ........................... 93

Figure 5.12: Rail and coach average speeds: international trips (lowest observed fare) .......... 94

Figure 5.13: Rail and air costs: interurban trips over 300 kilometres (lowest observed fare) ... 95

Figure 5.14: Rail and air average speeds: interurban trips over 300 kilometres (lowest observed

fare) ............................................................................................................................................ 96

Figure 5.15: Rail and air costs: international trips (lowest observed fare) ................................ 97

Figure 5.16: Rail and air average speeds: international trips (lowest observed fare) ................ 97

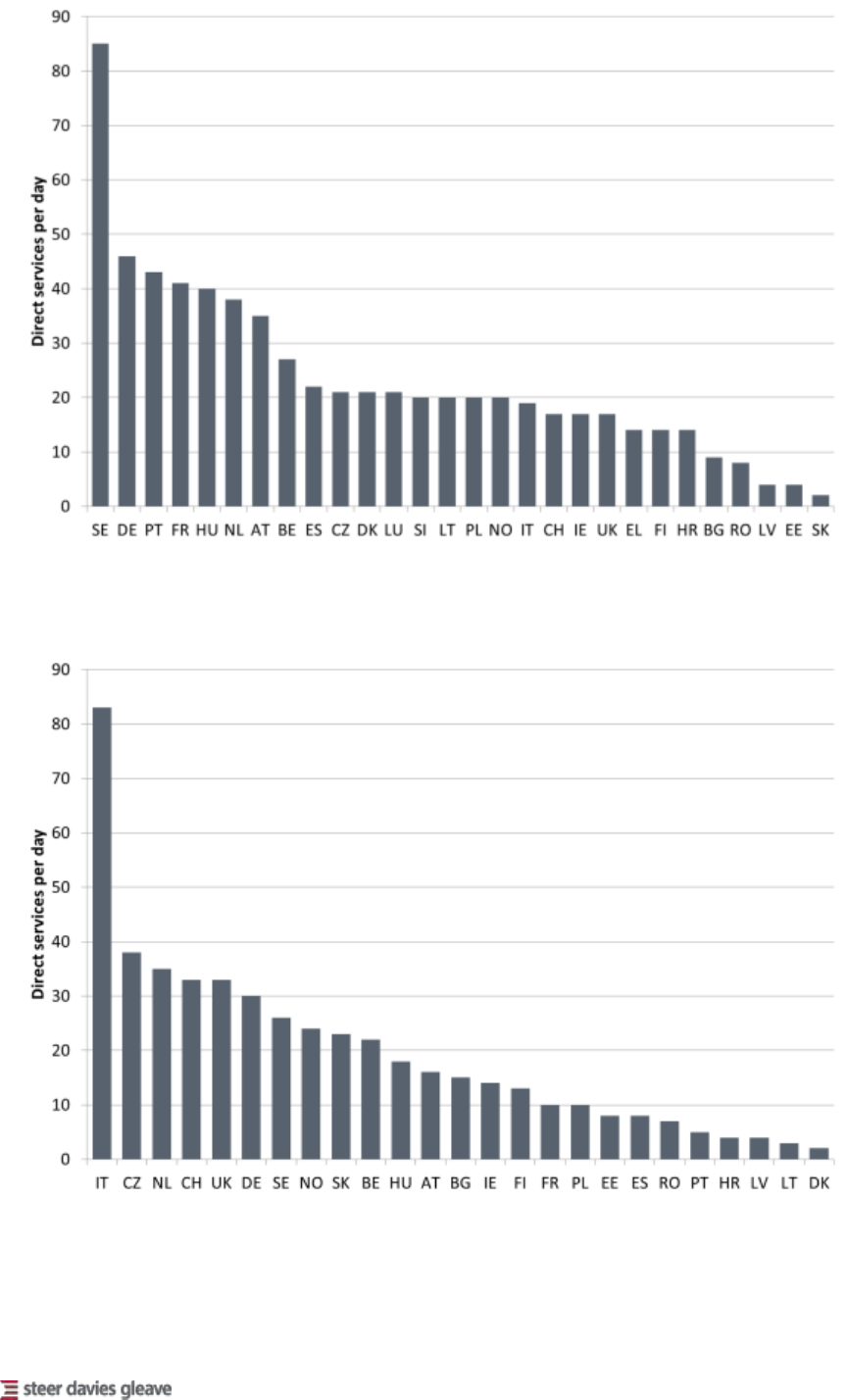

Figure 5.17:Direct air and rail services per weekday (interurban trips over 300 kilometres) .... 98

Figure 6.1: Izy’s service offer .................................................................................................... 104

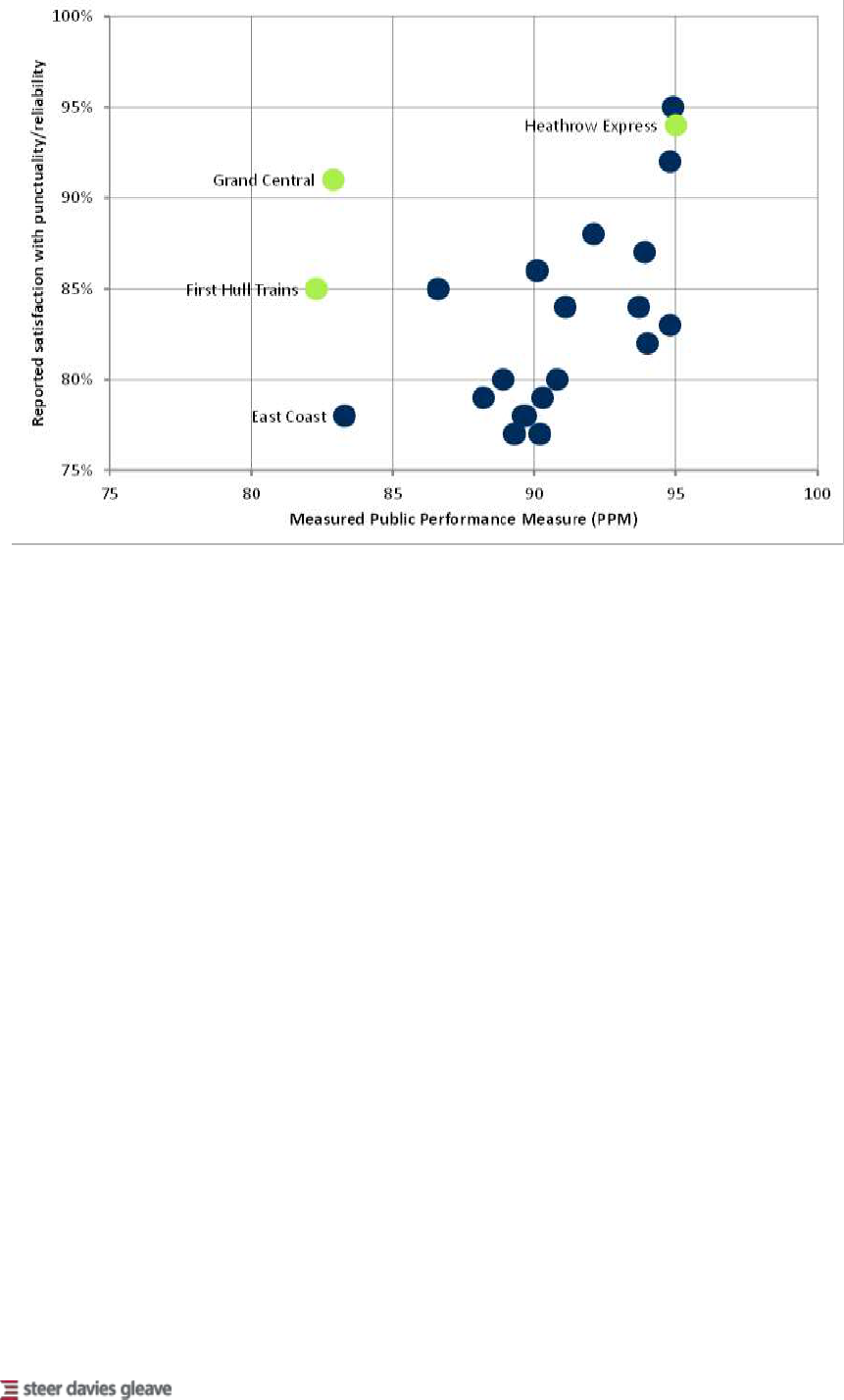

Figure 6.2: Market entry: incumbent and new entrant frequency and fares .......................... 114

Figure 6.3: Market entry: measured punctuality and reported satisfaction with punctuality. 116

Figure 6.4: Comparison of fares on routes with one or more operators ................................. 117

Figure 7.1: Regional trips: average effective speeds ................................................................ 121

Figure 7.2: Regional trips: longest day trip ............................................................................... 122

Figure 7.3: Interurban trips under 300 kilometres: average effective speed ........................... 123

Figure 7.4: Interurban trips under 300 kilometres: longest day trip ........................................ 124

Figure 7.5: Interurban trips over 300 kilometres: average effective speed ............................. 125

April 2016

Figure 7.6: Interurban trips over 300 kilometres: longest day trip .......................................... 125

Figure 7.7: Domestic high speed trips: average effective speed .............................................. 126

Figure 7.8: Domestic high speed trips: longest day trip ........................................................... 127

Figure 7.9: Regional trips: rail service frequency ..................................................................... 128

Figure 7.10: Interurban trips under 300 kilometres: rail service frequency ............................ 128

Figure 7.11: Interurban trips over 300 kilometres: rail service frequency ............................... 129

Figure 7.12: Domestic high speed trips: rail service frequency ................................................ 129

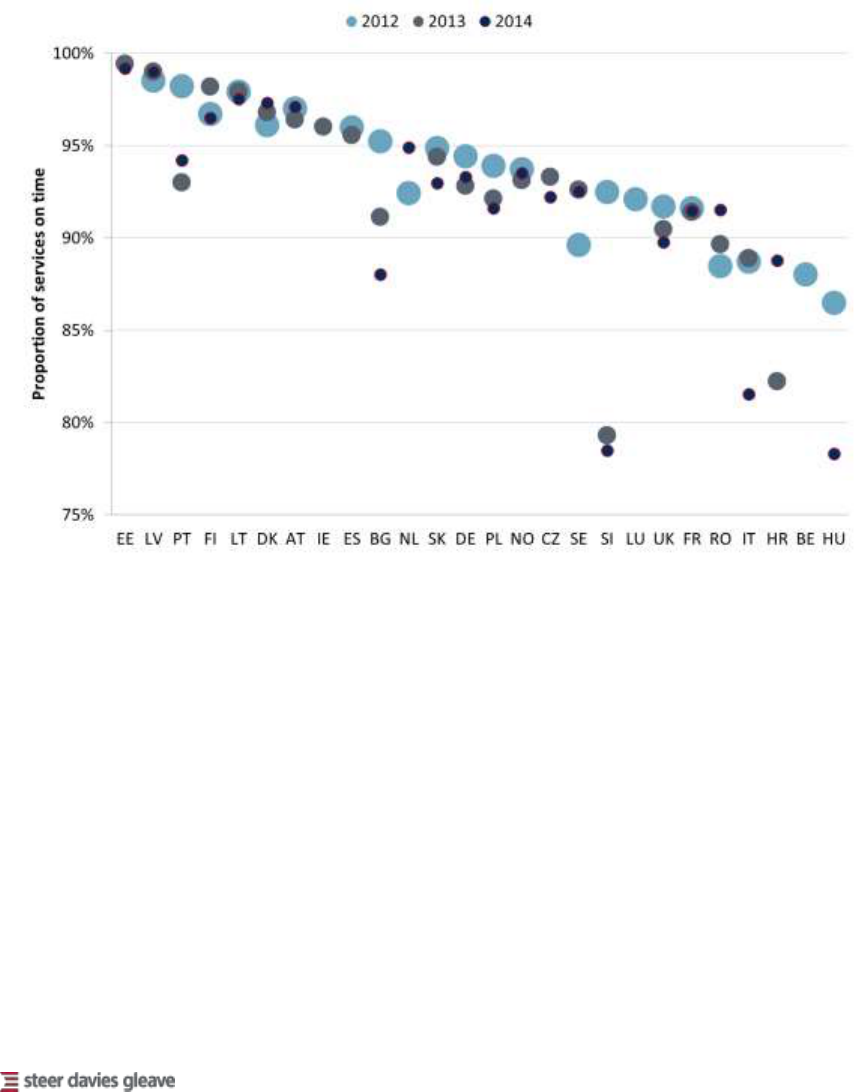

Figure 7.13: Punctuality of regional and local passenger services by Member State .............. 131

Figure 7.14: Punctuality of long-distance passenger services by Member State ..................... 132

Figure 7.15: Reliability of regional and local passenger services by Member State ................ 133

Figure 7.16: Reliability of long-distance passenger services by Member State ....................... 133

Figure 7.17: Eurobarometer scores: railway stations and rail services (2012-2013) ............... 137

Figure 7.18: Eurobarometer scores: ticketing attributes (2012-2013) ..................................... 138

Figure 7.19: Eurobarometer scores: frequency and punctuality and reliability (2012-2013) .. 139

Tables

Table 2.1: Fare and average yield: an example ............................................................................ 9

Table 2.2: Member States and routes in 2009 fares study for Passenger Focus ....................... 16

Table 2.3: Changes in the structure and level of fares (2005-2015) .......................................... 18

Table 2.4: Stakeholder responses on PSO contracts in provision of rail services ...................... 20

Table 2.5: Approaches to setting fares ....................................................................................... 21

Table 2.6: Stakeholder comments on developments in rail competition .................................. 26

Table 2.7: Member State characteristics and their influence on rail fares ................................ 28

Table 3.1: Suburban fares: stations selected for 10-kilometre radial journey in capital cities .. 35

Table 3.2: Suburban fares: fares found for 10-kilometre radial journey in capital cities ........... 36

Table 3.3: Suburban fares: multi-trip discount relative to full “cash” fare ................................ 39

Table 3.4: Suburban fares: personal and bearer tickets in London ............................................ 40

Table 3.5: Suburban fares: variation between cities within a State ........................................... 42

Table 3.6: Suburban fares: setting fares and sharing revenues ................................................. 45

Table 3.7: Suburban rail services between London terminals and Crystal Palace ..................... 47

Table 3.8: Suburban fares: capital cities with suburban rail networks ...................................... 49

April 2016

Table 3.9: Suburban fares: discounts available in different cities .............................................. 52

Table 4.1: Regional fares: sample of station pairs ...................................................................... 55

Table 4.2: Interurban trips under 300 kilometres: sample of station pairs ............................... 59

Table 4.3: Interurban trips over 300 kilometres: sample of station pairs .................................. 62

Table 4.4: Domestic high-speed trips: sample of station pairs .................................................. 65

Table 4.5: Domestic and international long-distance fares ........................................................ 67

Table 4.6: Other international routes ......................................................................................... 68

Table 4.7: Approaches to setting fares ....................................................................................... 70

Table 4.8: Setting other fares and sharing revenues .................................................................. 72

Table 4.9: Discounts: tickets combining travel, social and group characteristics ...................... 74

Table 4.10: Discounts: examples of how discounts may be set ................................................. 74

Table 4.11: Relationships between fares and sales channels..................................................... 78

Table 4.12: Transparency and clarity: information criteria and scoring..................................... 79

Table 4.13: Transparency and clarity: online ticket sales channels ............................................ 80

Table 5.1: Modal competition: data collection for competitor modes ...................................... 83

Table 6.1: Intramodal competition ........................................................................................... 101

Table 6.2: Intramodal competition through low cost services ................................................. 103

Table 6.3: Intramodal competition for the market .................................................................. 104

Table 6.4: Liberalisation: market entry by domestic open access operators ........................... 110

Table 6.5: Liberalisation: market entry and effects in the UK, Italy and the Czech Republic ... 111

Table 6.6: Liberalisation: routes, incumbents and new entrants for comparison ................... 114

Table 6.7: Corridors with more than one operator and comparator corridors ........................ 117

Table 7.1: Quality: analysis by market sector ........................................................................... 120

Table 7.2: Quality: services defined as on time in RMMS ........................................................ 130

Table 7.3: Quality: station facilities scoring system ................................................................. 134

Table 7.4: Quality: online information on station facilities ...................................................... 135

Table 8.1: Factors affecting travel demand .............................................................................. 141

Table 8.2: Rail fares and service quality (regional) ................................................................... 143

Table 8.3: Domestic coach market regulatory frameworks ..................................................... 220

April 2016 | 1

1 Introduction

Study background

Under Article 15 of Directive 2012/34/EU establishing a single European railway area (the 1.1

Recast Directive), the European Commission (the Commission) is required to monitor

developments in rail transport across the European Union and to report on these to the

European Parliament and the Council. Accordingly, the Commission collects a wide range of

information on the rail sector of each Member State through the annual Rail Market

Monitoring Survey (RMMS). All European Union Member States except Cyprus and Malta

(which do not have railways), together with Norway, submit RMMS questionnaire responses.

In preparing reports on the rail sector, the Commission must include information on fares and 1.2

service quality. These are key determinants of the competitiveness of rail services relative to

other transport modes, and it is important for policy makers to understand how they are

influenced by policy at the Union, national and regional level. However, given the wide range

of fares and services offered, a reflection partly of the different fare setting and subsidy

policies prevailing in different Member States (and in different regions within individual

Member States), it is difficult to obtain comparable information through the RMMS.

Against this background, the Commission has initiated this study on the prices and quality of 1.3

rail passenger services. Steer Davies Gleave was awarded the contract to undertake the study

in October 2015 and this Final Report sets out the findings and conclusions.

Study objectives and methodology

Study objectives

The study is intended to investigate the rail service offer, defined in terms of fare levels and 1.4

service quality, to passengers across the European Union and to assess how this has been

influenced by policy in different Member States. The Commission is particularly interested in

how the prices and service offer have evolved and vary in different States. It is also concerned

with the impact of market liberalisation and competition, and policy in relation to services

operated as Public Service Obligations (PSO services) under contract between a transport

authority and a railway undertaking.

A key objective is therefore to determine how far policy in each of these areas has influenced 1.5

the attractiveness of rail services in different markets, more specifically suburban, regional and

long-distance services operating on routes on the main European rail network. The findings

are expected to inform the Commission’s Fifth Report on Rail Market Monitoring, to be

published during the first half of 2016.

The study covers all 26 Member States of the European Union which have operating railways, 1.6

plus Norway and Switzerland. For simplicity, in this report the term Member State is taken to

April 2016 | 2

apply to all of these countries, notwithstanding that Norway and Switzerland are not members

of the Union

1

.

Overview of methodology

In view of the multiplicity of fares and services available, it has not been possible to undertake 1.7

a comprehensive study of the rail service offer across the European Union. However, we

sought to ensure that the results of our analysis are representative of the passenger

experience in different Member States and of the influence of policy on the fares and service

quality offered to them. Accordingly, our methodology included the following elements:

Review of trends in yield and fare data: where data are available, we reviewed historical

trends in fares and yields to determine how these developed over the last decade.

Review of national and rail sector characteristics: we investigated the impact of factors

such as rail network length, degree of urbanisation and income levels on yields, providing

context for the more detailed investigation of fares policy and fare levels in different

countries that provided the main focus for the study.

Desk research by Member State: we carried out desk research into the rail service offer in

each Member State, and prepared case studies of 12 of them. This work included a

review of various websites, covering railway undertakings, infrastructure managers and

other rail sector organisations. It allowed us to identify developments in fares policy and

sales and distribution channels, including applications of new technology to help buy

tickets, and to assess the extent of innovation in rail markets more generally.

Assessment of station facilities: based on a review of website information, we

investigated the services and facilities available at a major station located in the capital of

each Member State, assessing aspects of service quality such as provision of ticket

facilities, train information and assistance for persons with reduced mobility (PRMs).

Review of data from RMMS and the ERADIS database: to inform the case studies and our

broader understanding of service quality, we also reviewed and analysed data from

RMMS and from reports on service quality submitted by rail operators and included in the

European Railway Agency Database of Interoperability and Safety (ERADIS). This enabled

us to assess the service offer in each Member State by reference to measures such as

punctuality and customer satisfaction.

Sampling of rail fares: we sampled fares systematically for a selection of services, covering

all Member States and suburban, regional, long-distance domestic and international

markets. This enabled a comparison of fares within and between countries, taking

account of the influence of factors such as type of fare and booking horizon (the period

between booking and travel).

Sampling of fares offered by competitive modes: building on the analysis of rail fares, we

identified the cost of car travel, and coach and airline fares for equivalent origin-

destination pairs, to determine how effectively rail competes with these modes on a

range of shorter and longer distance routes across the European Union.

Stakeholder engagement: we carried out extensive stakeholder engagement through

interviews with, or written responses from a total thirty-three stakeholders including

railway undertakings, transport ministries, regulatory bodies, passenger representative

1

Norway is a member of the European Economic Area and Switzerland is a member of the European

Free Trade Area. Both comply with aspects of European railway law.

April 2016 | 3

bodies and a number of pan-European organisations

2

. These responses informed our

understanding of rail policy, notably in relation to the provision of services operated as

Public Service Obligations (PSOs) and the introduction of on-rail competition.

Review of the impact of on-rail competition: we investigated a number of examples of on-

rail competition in the Czech Republic, Italy and the UK, identifying impacts on the

behaviour of new entrant and incumbent operators and comparative fare and service

quality levels.

Review of the impact of national rail policies: drawing on the stakeholder responses and

published information, we compared the ways in which fare levels and service quality are

determined in different Member States and different markets, contrasting the importance

of administered fares, PSO specifications and the availability of public subsidy in some

markets with the effect of commercial incentives and competition in others.

To supplement the core research team, we also engaged a broader team of staff with country-1.8

specific transport sector experience across all Member States. In addition to providing their

own knowledge and experience, our country experts assisted with data collection and

stakeholder contacts, and reviewed the outputs of the desk research and stakeholder

engagement exercises.

Based on our findings, we sought to draw conclusions about the overall competitiveness of rail 1.9

relative to other modes in different markets, and about the impact of different rail policies on

the attractiveness of rail services from the perspective of passengers.

Organisation of this report

The remainder of this report is organised as follows:

1.10

Chapter 2 provides an overview of the passenger rail market in Europe, the institutional

arrangements that govern rail policy and the characteristics of the national networks.

Chapter 3 provides our analysis of suburban fares and tickets.

Chapter 4 provides our analysis of other fares and tickets.

Chapter 5 discusses competition between rail and car, coach and air transport.

Chapter 6 discusses competition between rail operators, whether for or in the market.

Chapter 7 examines quality and customer satisfaction.

Chapter 8 synthesises and draws conclusions on the preceding analysis.

The following additional information is provided in appendices: 1.11

Appendix A, our country case studies

Appendix B, a statistical analysis of national railway characteristics

Appendix C, a case study on fares between Exeter and Fareham

Appendix D, background on factors influencing travel demand

Appendix E, a summary of the extent of coach market liberalisation

Appendix F, a glossary of terms

2

This represents a response rate of 22% of the 150 organisations contacted.

April 2016 | 4

2 The passenger rail market in Europe

European rail travel demand

Over the ten years to 2013, and as reported to Eurostat, passenger rail demand in the 2.1

European Union (EU28) increased by 61.8 billion passenger-kilometres to 424 billion

passenger-kilometres. This represents an average growth rate of 1.6% per annum and

suggests that in 2013 rail had a 7.4% share of all surface transport including private car, bus

and coach, rail, tram and metro.

Figure 2.1 shows how the largest markets for rail travel are in large and high-income Western 2.2

European Member States.

Figure 2.1: Rail passenger-kilometres by Member State (2013)

Source: Steer Davies Gleave analysis of Eurostat data

April 2016 | 5

Many rail services in these large high-income Member States are not part of a Public Service 2.3

Obligation (PSO) agreement

3

, except in the UK where the PSO operator (franchisee) may have

offered to pay a premium to operate the service. Across the European Union, however, two

thirds (or 280 billion passenger-kilometres) of the estimated travel by rail in 2013 was made

on PSO services.

Figure 2.2 shows how estimated rail travel per inhabitant varies by a factor of ten between the 2.4

Member States which have railways. In 2013, estimated rail travel per head of population was

typically over 1,000 kilometres per year in Western and Northern Member States and less than

100 kilometres in Lithuania and Greece.

Figure 2.2: Propensity to travel by rail by Member State (2003-2013)

Source: Steer Davies Gleave analysis of Eurostat data

Growth in rail use over the ten years to 2013 also varied significantly by Member State, as 2.5

shown in Figure 2.3.

3

Public Service Obligations are defined in Regulation (EC) 1370/2009 to mean requirements defined or

determined by a competent authority in order to ensure public passenger transport services in the

general interest that an operator, if it were considering its own commercial interests, would not assume

or would not assume to the same extent or under the same conditions without reward.

April 2016 | 6

Figure 2.3: Average annual growth in rail passenger-kilometres (2003-2013)

Source: Steer Davies Gleave analysis of Eurostat data

The largest increases in rail passenger-kilometres, with average annual growth of at least 2%,

2.6

were in EU15 Member States: the UK, Luxembourg, Austria, Sweden, the Netherlands,

Belgium, Germany, France and Estonia.

A decline in rail patronage over the ten years to 2013 was reported in eleven Member States, 2.7

with average rates of decline of over 6% in Romania, 4% in Lithuania and Greece and 3% in

Bulgaria. In Bulgaria, the decline may result from the consolidation activity required by its

Railway Reform Programme. In Greece, it may be due to the contraction of state funding

required as part of the wider fiscal austerity packages implemented from 2010.

The divergence in growth rates with EU13 Member States also reflects a broad range of 2.8

exogenous and endogenous factors. For example, increased access to car ownership and

higher car use in new Member States will suppress rail demand. Conversely, the opening of

new infrastructure or services, such as the West Coast Main Line upgrade works in the UK

(2008) and the HSL-Zuid line in the Netherlands (2009) will support rail demand and encourage

modal shift.

European rail fares

Each year millions of fares are calculated and marketed by a wide range of national, regional, 2.9

local and urban authorities and operators. However, databases of historic fares may not be

saved or made available to third-parties. Nevertheless, we identified a number of sources of

data providing some indication of historical trends, although each source is subject to some

caveats. More specifically, the data sources identified to investigate changes in fares through

time include the following:

April 2016 | 7

Harmonised Index of Consumer Prices (HICP) can be disaggregated to allow some analysis

of how rail fares in individual Member States have changed relative to average prices

across all transport modes.

Historical fares data at the national level are published by the UK Office of Rail and Road.

National average yield data can be calculated from time-series data on passenger revenue

and passenger kilometres reported in Eurostat.

Fares data collected for the 2009 Comparisons between fares and ticketing in Britain and

continental Europe study by Steer Davies Gleave for Passenger Focus (now Transport

Focus, the representative body for rail passengers in Great Britain) includes information

on 2009 fare levels that can be compared with 2015.

Information that has been obtained from stakeholder engagement.

We discuss each of these sources below. 2.10

Harmonised Index of Consumer Prices (HICP)

Figure 2.4 uses data from the HICP to illustrate inflation across all transport modes from 2005 2.11

to 2014.

Figure 2.4: Harmonised Index of Consumer Prices: all transport (2005-2014)

Source: Steer Davies Gleave analysis of Eurostat HICP data

The dominance of private car travel in the index means that these figures are heavily affected 2.12

by volatility in the price of crude oil and improvements in fleet efficiency. They are also

influenced, in some part, by the strength of the economy in each Member State, including the

perceived quality of macroeconomic policy.

Figure 2.5 uses disaggregate HICP data to consider the relationship between the price of rail 2.13

and the “all modes” average shown in Figure 2.4. In this chart, a value greater than zero

suggests that rail travel is becoming more expensive than a basket of transport services

April 2016 | 8

(private and public) across all modes. A value less than zero suggests that rail travel is

becoming cheaper.

Figure 2.5: Harmonised Index of Consumer Prices: rail transport/all transport (2005-2014)

Source: Steer Davies Gleave analysis of Eurostat HICP data

In all but two Member States (Belgium and Sweden), rail travel appears to be becoming more 2.14

expensive relative to other modes. While across the European Union (together with Norway

and Switzerland) the divergence is modest (approximately 1% per year), there are some

notable outliers (Estonia and Latvia) where rail travel appears to be becoming considerably

more expensive than other modes. In Estonia this may be due to the reduction in Russian

freight transit traffic which previously cross-subsidised passenger journeys.

At this level of disaggregation, the reliability of conclusions based on HICP data is limited. The 2.15

HICP aims to be representative of the developments in the prices of all goods and services

available for purchase within the euro area for the purposes of directly satisfying consumer

needs. It measures the average change over time in the prices paid by households for a

specific, regularly updated basket of consumer goods and services. As part of a large bundle of

goods that is weighted to produce whole-economy inflation estimates, HICP therefore relies

upon a small sample of rail products which may not be representative of the rail market in

general, and many individuals or households will experience different fares depending upon

the corridor and type of ticket bought

4

.

4

On average, the prices of around 700 products are collected every month in different outlets and in

approximately 1,600 different towns and cities across the euro area.

April 2016 | 9

National fares data

The UK Office of Rail and Road publishes time series data on rail fares. We investigated the 2.16

availability of similar data for other Member States and identified Sweden as the only country

which provided a similar time series on advertised fares at the point of sale, rather than

average yields which reflect changes in the mix of fares that are bought.

It is important to distinguish between fare and average yield, in particular, if the calculation of 2.17

average yields includes multiple ticket types. Average yield may not always provide a reliable

proxy for changes in fares since passengers may change their travelling habits in response to

fare changes. Table 2.1 provides a stylised example of the distinction between fare and

average yield.

Table 2.1: Fare and average yield: an example

Class of travel

Indicator

Scenario 1

Scenario 2

First Class

Fare (1)

€50

€75

Journeys (2)

100

50

Revenue (3) = (1)x(2)

€5,000

€3,750

Second Class

Fare (4)

€20

€20

Journeys (5)

500

525

Revenue (6) = (4)x(5)

€10,000

€10,500

Average yield (7) = ((3)+(6))/((2)+(5))

€25

€24.78

In Scenario 1, a train has fares of €50 in First Class and €20 in Second Class. With 100 2.18

passengers travelling in First and 500 in Second, this generates an average yield of €25.

In Scenario 2, the First Class fare increases to €75. This reduces the demand for First Class to 2.19

50 passengers, 25 of whom choose to travel in Second Class instead, and the remaining 25 no

longer travel by rail, but may use alternative modes, make a different trip, or choose not to

travel at all.

The result of changing from Scenario 1 to Scenario 2 is that, while the First Class fare has risen 2.20

and the Second Class fare has not changed, the average yield has fallen from €25.00 to €24.78.

Due to the way in which it incorporates elements of behavioural change, care must be taken 2.21

when interpreting average yield data that covers multiple ticket types or fare levels.

The Office of Rail and Road time series data on rail fares take the form of indices for different

2.22

fare types for each the main categories of PSC (franchise) in the UK. These are calculated each

year in January, the month in which fares increases permitted under the regulatory

mechanism in the franchise agreements are applied. Separate indices are calculated for

Anytime, Off-peak, Super-off peak, Advance and season fares. Figure 2.6 to Figure 2.8 inclusive

show trends in anytime, off-peak and advance fares for each franchise category from 2004 to

2015. Note that the data covers services operating in the privatised rail industry in Great

Britain and hence does not include fares in Northern Ireland.

April 2016 | 10

Figure 2.6: Trends in Anytime fares in Great Britain (nominal)

Source: UK Office of Rail and Road

Figure 2.7: Trends in Off-peak fares in Great Britain (nominal)

Source: UK Office of Rail and Road

April 2016 | 11

Figure 2.8: Trends in Advance fares in Great Britain (nominal)

Source: UK Office of Rail and Road

The figures indicate a steady annual increase in the real value of most fares over the period as 2.23

a whole, in the range of between 1% and 2% per annum for Anytime and Off-peak fares. The

apparent substantial reduction in Advance fares on London and Southeast services in 2009

may reflect the major reclassification of fares that occurred in that year. If so, Figure 2.8 may

illustrate a more general issue concerning discontinuities in data sets even where these appear

to allow analysis of long term trends.

In Sweden, the Royal Institute of Technology (KTH) has produced a report which describes the 2.24

changes in rail fares and patronage in Sweden between 1990 and 2015. Some key findings are

summarised below

5

.

5

KTH Sweden (2015) Development of supply and prices on Swedish railway lines 1990-2015

April 2016 | 12

Figure 2.9: Rail fare trends in Sweden (2015 prices)

Source: The Royal Institute of Technology (KTH Sweden)

Figure 2.9 illustrates considerable variation in Swedish rail fares (per 10 km) over the past 25 2.25

years. The price of SJ Express’ highest fare has grown steadily year on year, whilst the lowest

priced SJ Express fare decreased dramatically between 1990 and 2008 and has almost levelled

off since. This is indicative of SJ’s pricing policy, which has been strongly influenced by the

introduction of yield management (a policy that tends to increase the range of fares paid). The

prices of other, specific rail products have remained broadly fixed in real terms, with the

exception of the RPTA Monthly pass which has grown steadily and has almost doubled since

1990. The downward trend observed on SJ services from 2014 can be partly explained by the

complete market liberalisation of Swedish railways in 2010

6

. This has introduced some

competition on the network and has pushed SJ to lower its fares.

The Finnish Transport Agency also provided an extract of time-series fares data which is 2.26

reported in Figure 2.10 below.

6

Deregulation started on October 1

st

2010, however, train paths needed to be submitted by April 2010

for the timetable that came into place in 2011, which corresponded with train operation year 2012.

April 2016 | 13

Figure 2.10: Rail fare trends in Finland

Source: Statistics Finland

Figure 2.10 shows a steady increase in in the cost of a 200km trip between 2002 and 2012. 2.27

Between 2012 and 2015 the sample trip was changed to Helsinki to Tampere by IC2, however,

the trend observed is similar. Since the data only represent a trip type, it is not possible to

infer whether fares on average followed the same pattern.

National average yield data

A further potential source of national time-series data on rail fares is passenger revenue and 2.28

passenger-kilometre data reported at national level. Again, where available, this data is not

subject to many of the shortcomings of HICP data, providing a more comprehensive picture of

rail travel across all routes and ticket-types. However, we examined the source information on

which these data are based and are aware that they may be inaccurate for a number of

reasons:

Reported passenger revenue data may exclude revenue associated with gross cost Public

Service Contracts (PSCs), or not allocated to rail by a competent authority, particularly in

urban areas

7

.

Reported passenger revenue reflects the number of passengers who pay each fare, but

this will change not only with underlying demand but also when fares are changed

relative to the passengers’ willingness to pay (as illustrated in Table 2.1). Changes in the

average fare paid by passengers will not be the same as changes in the average fare set

by competent authorities or operators.

7

In recent but unpublished work for the Commission on the implementation of Regulation 1370/2007,

we found the revenue for multimodal urban and suburban travel was rarely identified or allocated to a

mode.

April 2016 | 14

Reported passenger-kilometres are estimated, and in other studies we found that these

estimates are sometimes based on assumptions, such as that there is a fixed average trip

length.

Despite the shortcomings described above, Figure 2.11 highlights the disparity in average 2.29

yields (fare revenue per passenger-kilometre) between States.

Figure 2.11: Fare revenue per passenger-kilometre (2012, excluding Luxembourg)

Source: Study on the Cost and Contribution of the Rail Sector (Steer Davies Gleave, 2015).

Note: fare revenue data is not available for Croatia.

Note: for ease of presentation the reported €0.58 per passenger-kilometre in Luxembourg has been excluded.

However, this high average yield is difficult to reconcile with our findings of low individual fares (see Chapter 4).

As might be expected, the highest average yields are found in high-income EU15 Member 2.30

States with well-developed, high-quality passenger networks. Fares in Sweden are a notable

exception to this general observation, where average fares are broadly half those charged in

neighbouring Denmark and Finland.

The observed difference in average yield may reflect the proportion of industry costs covered, 2.31

through necessity or design, by subsidies. As we discuss later (see Figure 2.16), the operating

cost recovery from fare revenue in Western European Member States is typically higher than

elsewhere in the EU. However, in some markets fares may be low, even if railway undertakings

seek to maximise revenues, because of either low incomes or competition from other modes

8

.

Figure 2.12 shows the average annual change in average yield (measured as fare revenue per 2.32

passenger-kilometre) between 2007 and 2012 for a sample of Member States.

8

In some Member States, particularly where services are poor, there is evidence of rail being

considered an ‘inferior good’. In economics terminology, an inferior good is one for which demand falls

when consumer income rises.

April 2016 | 15

Figure 2.12: Average annual change in revenue per passenger-kilometre (2007-2012)

Source: Study on the Cost and Contribution of the Rail Sector (Steer Davies Gleave, 2015).

Note: average annual change calculated as a compound annual growth rate (CAGR).

In the majority of cases, average yields have risen, although the average rate of increase 2.33

varied considerably. The very high increases in average yield in Greece may be a result of large

reductions in the number of passenger services on offer and consequent reductions in rail use.

Only the most profitable services, typically those with higher average yields, have been

retained at the expense of less profitable routes and services.

As noted previously, these outcomes are likely to reflect a number of factors, not least the 2.34

potential for passengers to trade down to a cheaper product when faced with a fare increase

(as illustrated in Table 2.1) and external factors such as the economic slowdown which began

in 2007. For example, despite well-documented increases in UK rail fares, average yields fell

between 2007 and 2012. This is probably due to passengers shifting from First Class and

unrestricted (“open”) tickets to Standard Class and yield-managed advance purchase

(“Advance”) tickets

9

. The transfer of some high-yield London suburban services from a

national net cost to a municipal gross cost PSC may also have affected reported average yield.

Comparison with fares data obtained from previous work

In our previous work for Passenger Focus (see paragraph 2.9), we identified a range of fares 2.35

available in 2009 on specific routes within a limited number of States

10

, as shown in Table 2.2

below. In each case we sought to compare 2009 and 2016 fares of each type.

9

Due to the way in which the data presented in Figure 2.12 has been constructed, some of the change

in average yield may also be due to a fall in the value of the pound relative to the euro over the same

period, leading to an apparent fall in revenues when converted to euros.

10

Comparisons between fares and ticketing in Britain and continental Europe (SDG, 2009)

April 2016 | 16

Table 2.2: Member States and routes in 2009 fares study for Passenger Focus

State

Origin

Destination

Germany

Hamburg

Berlin

Spain

Valencia

Madrid

France

Paris

Marseille

Italy

Milan

Rome

The Netherlands

Leeuwarden

Rotterdam

Poland

Krakow

Warsaw

Sweden

Malmö

Gothenburg

Source: Comparisons between fares and ticketing in Britain and continental Europe (Steer Davies Gleave, 2009)

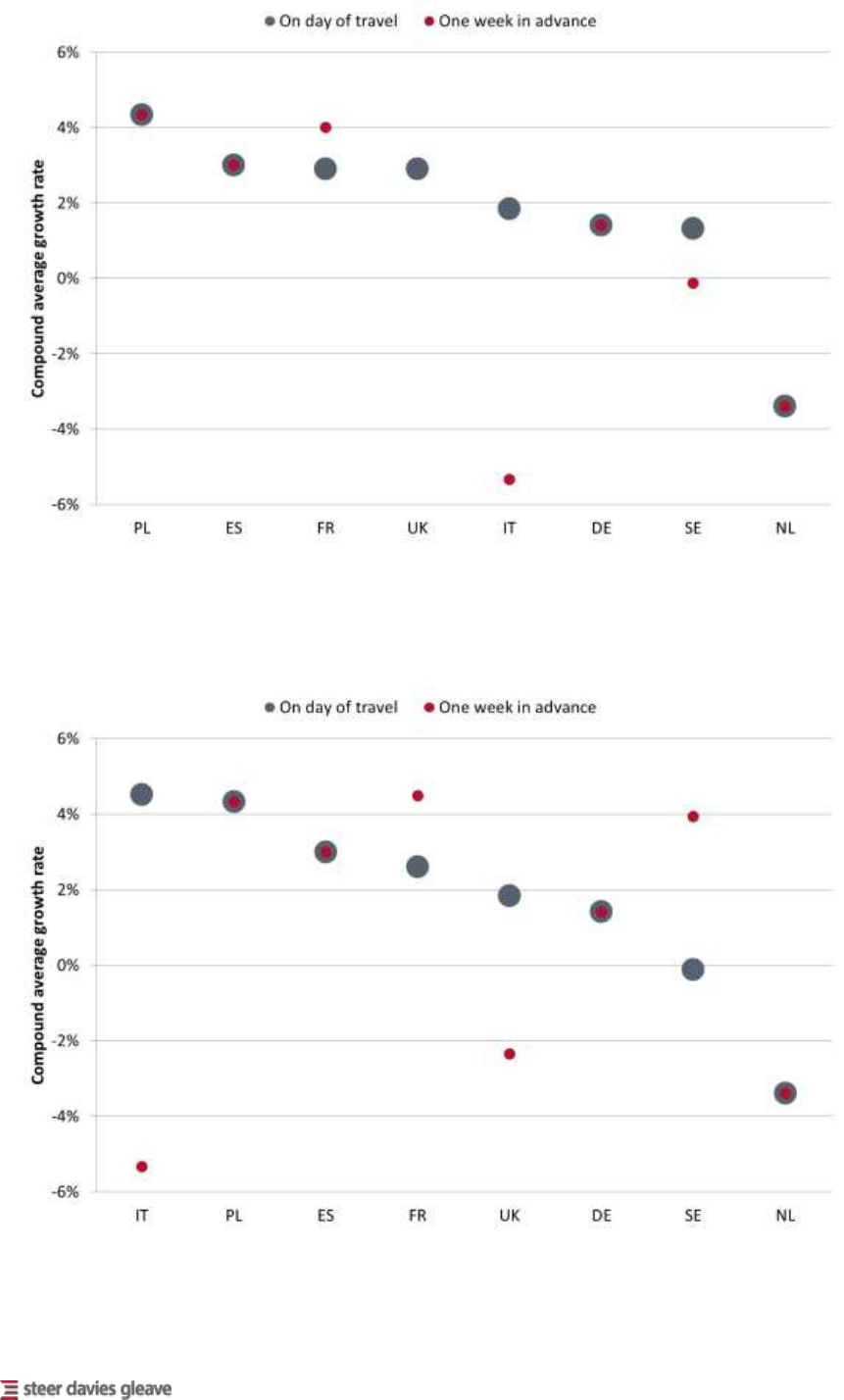

Figure 2.13 and Figure 2.14 overleaf show compound average growth rates for two ticket 2.36

types booked on the day of travel and a week ahead. In each case, the growth rate represents

an average annual change in the real ticket price.

They illustrate the variation between Member States, markets (defined by ticket types), and 2.37

booking horizons. While it is not possible to generalise on the basis of the evidence shown, we

note that:

France, Poland and Spain appear to have applied significant fare increases in both peak

and off-peak markets;

the benefits of buying tickets a week in advance rather than on the day have increased

significantly in Italy, possibly reflecting a sharper commercial focus following the

introduction of on-rail competition (Milan-Rome is one of only a few corridors with on-rail

competition, and may not be typical);

the benefits of buying tickets a week in advance have fallen in France as the price

differential with tickets bought on the day of travel has narrowed;

in the Netherlands, there has been a substantial fall in real fares across a range of routes

which may, in part, be due to the introduction of the OV Chipkaart card and the

associated restructuring of fares; and

in Poland, Spain, Germany and the Netherlands, fare changes were similar for each ticket

type and booking horizons.

April 2016 | 17

Figure 2.13: Average annual growth rate: peak return fare

Source: Steer Davies Gleave analysis (based partly on data from 2009 study for Passenger Focus).

Note: analysis is based on the corridors described in Table 2.2. It was not possible to identify a directly comparable

advance fare for the UK, because of ticket reclassification in 2009 and subsequent changes to ticket restrictions.

Figure 2.14: Average annual growth rate: off-peak single

Source: Steer Davies Gleave analysis (based partly on data from 2009 study for Passenger Focus).

Note: analysis is based on the corridors described in Table 2.2

April 2016 | 18

Information from stakeholders

While none of the stakeholder responses included quantitative information on trends in fares, 2.38

several provided information on some of the underlying causes of changes in fare levels.

Table 2.3 below summarises responses to specific questions for each of the Member States 2.39

where information has been provided. Note that it has been compiled on the basis of

information provided by a mix of stakeholders, including transport ministries, regulatory

bodies and train service operators. Where different responses were received from

stakeholders within the same Member State, the study team reached a judgement based on

the advice of country experts. The question relating to PSO and non-PSO services was not sent

to Member States for which the column is shaded grey.

Table 2.3: Changes in the structure and level of fares (2005-2015)

Member State

Significant changes

in the last ten

years?

Do fares depend

on whether the

service is PSO or

non-PSO?

Were changes

driven by

intramodal

competition?

Were changes

driven by

intermodal

competition?

BE

Belgium

n/a

BG

Bulgaria

CZ

Czech Republic

DK

Denmark

DE

Germany

IE

Ireland

IT

Italy

EL

Greece

ES

Spain

n/a

n/a

HR

Croatia

HU

Hungary

NO

Norway

AT

Austria

PL

Poland

PT

Portugal

RO

Romania

SK

Slovakia

FI

Finland

SE

Sweden

SI

Slovenia

UK

United Kingdom

Source: Steer Davies Gleave analysis of stakeholder responses

As the table shows, the majority of Member States have changed either the structure or level 2.40

of fares (or both) over the last 10 years. In many cases, significant changes have been driven

by competition with other modes, at least in part, and intramodal competition has an effect

on fare setting in some. Almost all Member States to which the question was submitted

confirmed that the level and/or structure of fares depended on whether the service in

April 2016 | 19

question was operated under a PSO contract. The approach to provision of PSO services in

different countries is discussed further below.

Further examination of the responses highlighted a number of reasons for introducing 2.41

changes, some commercial and others policy-driven. In particular, we note the following:

In Bulgaria, off-peak fare reductions have been introduced on regional services to

promote off-peak travel.

In Austria, Italy, Finland and Romania, fares on some routes have been changed in

response to competition. For example, yield management systems have been introduced

in Italy to support fare-setting on routes on which there is competition from low-cost

airlines, although we could not confirm that they are used where there is on-rail

competition. In Austria, yield management has been introduced on the Vienna-Salzburg

route, on which there is competition between rail operators. Elsewhere, for example in

the Czech Republic, Portugal, Sweden and the UK, yield management has been

introduced purely to increase revenues on commercial interurban services.

In Hungary, fare increases have been introduced explicitly to cover the costs of new long-

distance rolling stock.

Smartcards have been introduced in a number of Member States. For example, in Ireland

smartcards have been introduced in Dublin to attract passengers and to monitor travel

behaviour, with a view to offering passengers tailored information about services.

National public transport smartcards have been introduced in Denmark (Rejsekort) and

the Netherlands (OV Chipkaart).

In Finland, Greece and Romania, discounts have been introduced to promote rail travel

and encourage patronage.

National institutional arrangements

Use of PSO contracts

To provide context for the fares analysis, we examined the extent to which Member States 2.42

rely on PSO contracts for the provision of rail services, and on the different approaches to their

procurement. We identified Member States making direct awards of contracts and others

awarding them through competitive procurement procedures, as well as a number using both

approaches.

Table 2.4 overleaf summarises our findings. 2.43

April 2016 | 20

Table 2.4: Stakeholder responses on PSO contracts in provision of rail services

Member State

PSO award

PSO contract

type

Types of service covered by PSO

Direct

Tender

Gross cost

Net cost

Urban

Interurban

Suburban

Regional

Interregional

High speed

BE

Belgium

BG

Bulgaria

CZ

Czech Republic

DK

Denmark

DE

Germany

IE

Ireland

IT

Italy

EL

Greece

ES

Spain

HR

Croatia

HU

Hungary

NO

Norway

AT

Austria

PL

Poland

PT

Portugal

RO

Romania

SK

Slovakia

FI

Finland

SE

Sweden

SI

Slovenia

UK

United Kingdom

Source: Steer Davies Gleave analysis of stakeholder responses

We did not seek information from all Member States on the types of service covered by PSO 2.44

contracts, and in some cases received different answers from the transport ministry and the

corresponding regulatory authority.

For example, in one Member State the ministry reported that some PSO contracts on the 2.45

state-owned network are directly awarded, while the regulatory authority indicated that all

services were competitively tendered

11

. This inconsistency may, in part, reflect recent market

developments. For example, central contracts for the state-owned rail operator which

provides the majority of the long-distance and regional services, were extended by a further

10 years in 2009. However, a number of tendering opportunities are emerging and a number

of private sector bidders are preparing accordingly.

11

As before, where divergent responses were received from stakeholders within the same Member

State, the study team reached a judgement based on the advice of country experts.

April 2016 | 21

Our more detailed review of the responses highlighted the following: 2.46

only Poland makes exclusive use of gross cost contracts

12

;

PSO contracts with national operators tend to be net cost, as in the Czech Republic and

Hungary, but there is variation in the allocation of revenue risk at the regional level;

even where contracts are gross cost, with operators taking little or no revenue risk,

operators may nevertheless face significant financial risk as a result of contractual

incentive mechanisms in the form of reward or penalty schemes (as in Sweden); and

national legislation providing for competitive tendering of PSO contracts does not

guarantee the application of competitive procurement procedures, as in Spain where

Renfe, the incumbent national operator, continues to benefit from a direct award.

Fares on PSO services

As already noted, a number of stakeholders have confirmed that the structure and/or level of 2.47

fares can depend on whether services are commercial or operated under PSO contracts.

However, we could not categorise either services or fares as “PSO” or “non-PSO”:

There is rarely any indication of whether a train is operated under a PSO, unless it is a

suburban service specified by the local competent authority or there is a national PSO

13

.

PSO fares may be administered (as in many suburban areas), regulated (as in some

Member States), or left to the market (as with many fares in Sweden and Great Britain).

National operators may operate both “PSO” and “non-PSO” services but choose, or be

required, to have a common fare structure.

A competent authority or “PSO” operator may set or regulate fares that all operators

must accept. This means that fares which operators are in principle free to set may be

“quasi-regulated” by the regulated or administered fare which they must accept.

An individual train service may include both “PSO” and “non-PSO” station calls.

A station pair may be served by both “PSO” and “non-PSO” services.

Where possible, however, in later chapters of this report we have identified whether fares 2.48

appear to be administered, regulated or constrained only by reference to the market, as

summarised in Table 2.5.

Table 2.5: Approaches to setting fares

Approach

Body setting fare

Operator may vary fare

Lower

Higher

Administered

Fares are set by a national, regional, local or municipal authority,

and there is no deviation from the specified fares.

Regulated

Fares are set subject to constraints, typically an upper limit on

individual fares or in a “basket” of fares.

No, or only

in basket

Market

Fares are set by the rail operator and not subject to regulation,

but may be constrained or “quasi-regulated” by other rail fares.

Source: Steer Davies Gleave analysis

12

Gross cost contracts require the contracting authority to take revenue risk, with bidders paid a fixed

fee per unit or period, and therefore incentivised to minimise costs subject to meeting contract

obligations.

13

National PSO arrangements only appear to be in place in Estonia, Ireland, Greece and Luxembourg,

where all domestic passenger rail journeys are made on PSO services.

April 2016 | 22

In practice, while we also found that the various websites we used to research the fares may 2.49

offer one or more fares, they do not always name them, list all the fares available and any

differences in their validity, or say how they are calculated. For example, it was rarely possible

to infer:

what authority or operator had set the fare;

the reasons for any variation in fares between trains;

whether different fares had different validities or conditions of use; or

the highest or lowest fares that might be charged.

Variation in prices between individual trains might be due, inter alia, to: 2.50

different service quality or stopping patterns;

market pricing in response to competition;

differential pricing by time of day;

discounts on certain trains available only a certain period in advance;

special offers; or

active yield management in response to forecast and emerging bookings on each train.

The study timescale constrained us to carry out research late in 2015, and we found that some 2.51

“month ahead” fares quoted for travel in 2016 were higher than those quoted for travel in

2015. Where this was the case, we assumed that this was due to general annual fares rises,

rather than any of the factors listed above.

The impact of subsidies on revenues

While PSO services are not necessarily subsidised, many rely on financial support from

2.52

national, regional or local transport authorities, whether they are operated under net or gross

cost contracts. As noted above, it is not possible to categorise either individual services or

individual fares as PSO or non-PSO, and any estimate of the extent to which PSO services rely

on fare revenue rather than public subsidy is therefore problematic. It is nevertheless possible

to estimate the contribution of fare revenue to the overall costs of the rail industry in a given

Member State. This provides an understanding of the policy and political framework in which

fares are set. We note, for example, that in the UK, where fare revenue as a proportion of

costs has been steadily increasing in recent years, there is now strong political pressure to

restrain annual fare increases, notwithstanding ongoing public sector funding constraints.

The overall operating cost of railways in the European Union reported in 2012 was around 2.53

€110 billion, as shown in Figure 2.15 below

14

. This figure covers all European Union Member

States with a railway except Croatia, for which full data was not available. On average, the mix

of infrastructure and operator costs is approximately 30:70. This ratio reflects both the

underlying cost structure of the EU rail industry, and the way in which it is financed. In those

Member States which make significant subsidy payments to infrastructure managers, track

access charges are typically lower and hence the operating costs of freight and passenger

operators are lower. Alternatively, if subsidies are channelled through operators delivering

14

Operating costs include the provision of both passenger and freight services and the operation and

maintenance of fixed infrastructure. As far as possible capital expenditure on rolling stock replacement,

infrastructure renewal and enhancements is excluded. The figures are likely to mask significant

differences in input and output trends, and in costs, revenues and subsidies, between different Member

States. Moreover, aggregate analysis of this kind cannot identify hidden costs such as maintenance

backlogs in some Member States.

April 2016 | 23

public service obligations, track access charges are typically higher and hence operator costs

make up a larger proportion of the total. In countries with more rail freight, the proportion of

total costs accounted for by the infrastructure manager is greater.

Figure 2.15: EU total rail operating costs, revenue and subsidy (2012)

Source: Study on the Cost and Contribution of the Rail Sector, Steer Davies Gleave, 2015.

Roughly 60% of costs are covered by fare box and freight revenue (40% passenger and 20% 2.54

freight) and a further 30% by subsidy. The remaining 10% (around €11 billion) is a residual

balancing item that is likely to include freight income not captured at the Member State level

(data was not available for all Member States) and other sources of income such as property

rents and retail revenue.

This analysis, originally undertaken for the Study on the Cost and Contribution of the Rail 2.55

Sector, has been further developed as Figure 2.16. The figure illustrates the extent to which

passenger revenue from fares covers total rail sector operating costs (incurred by freight and

passenger railway undertakings, and infrastructure managers) by Member State. As this

analysis relies upon a range of “top-down” assumptions applied to aggregate rail industry

data, the results should be considered as indicative of broad trends and not representative at

the Member State level.

The distribution of cost coverage is highly skewed, with only the large passenger rail networks 2.56

in Germany and the UK recovering more than 60% of operating and maintenance costs

through passenger fare revenue. This may, in part, be due to exogenous factors such as

population distribution and density, and factors such as policy initiatives to reduce the

taxpayer burden of rail sector funding and track access charging regimes. The remaining

Western European Member States typically recover 25-40% of operating costs through fares.

April 2016 | 24

Cost coverage from fares is lowest among Eastern European Member States, where 2.57

approximately 5-15% of total operating costs are met by fare revenues. This similarly reflects a

range of factors which vary by country, but which may include the cost burdens imposed by

legacy networks with high fixed costs, lower service frequencies and uncompetitive journey

times, lower network densities and lower fares. It also reflects the relative importance of, and

the share of costs incurred by, rail freight traffic as in the Baltic States, which are

predominantly freight rail networks. Poland is a notable outlier, where 37% of operating costs

are met by income from fares.

Figure 2.16: Passenger rail revenue as a proportion of total rail operating costs (2012)

Source: Steer Davies Gleave analysis of data collected for the Study on the Cost and Contribution of the Rail Sector.

On the basis of the evidence presented in Figure 2.16 it is not possible to assess the proportion 2.58

of passenger rail costs covered by the passengers themselves since it is not possible to allocate

all network costs to either passenger or freight traffic. In Sweden, for example, infrastructure

charges are very low and do not cover the full marginal cost of running services over the

network. Central government subsidy paid directly to the infrastructure manager means that

many infrastructure costs are common and cannot be allocated to passenger or freight.

The development of competition

A previous study by Steer Davies Gleave on the Fourth Railway Package in 2012 included a 2.59

review of the extent of competition in the market (on-rail) and competition for the market (in

the form of competitive tendering for rail concessions) at the time. It noted:

the well-established structural and regulatory frameworks in Sweden and the UK, which

provide for competition for the market while allowing some on-rail competition on

specific routes;

the emergence of new entrants offering commercial services competing with those

provided by incumbent national operators in a number of Member States; and

April 2016 | 25

growing use of competitive tendering in some Member States, notably Germany.

At the same time, the study highlighted various barriers to entry, including access to stations 2.60

and key facilities such as maintenance depots, that appeared to be hindering the further

development of competition. The analysis indicated that measures proposed for the Fourth

Railway Package legislation, in particular those covered by the governance pillar, would help to

address these and deliver substantial customer benefits.

While the Fourth Railway Package has not yet been adopted, the level of competition in rail 2.61

passenger markets across the European Union has developed since 2012. Table 2.6, which is

limited to information from stakeholders who responded to our call for evidence, summarises

the current situation regarding competition in the market for rail services

15

.

Table 2.6 ignores competition for the rail market through competitive tendering and the 2.62

introduction of differentiated rail products by existing operators, which are often lower cost

and serve new and emerging markets. Recent examples include Ouigo (SNCF) services in

France in 2013 and Izy (Thalys) services between Paris and Brussels in 2016

16

.

As already highlighted in Table 2.3, a significant number of Member States have indicated that 2.63

both intermodal and intramodal competition have affected rail fares on one or more routes

within their national networks over the last ten years.

15

Member States are omitted from Table 2.6 if no stakeholder response was provided: this does not

imply that intermodal competition or on-rail competition have had no influence on the rail market.

16

Izy services will operate on conventional rather than high speed lines in France to reduce

infrastructure costs, will have no buffet, and will offer digital-only ticket sales. Ten tickets for each

service will be available for €10, but will not guarantee the passenger a seat.

April 2016 | 26

Table 2.6: Stakeholder comments on developments in rail competition

Member State

Intermodal competition

On-rail competition

BE

Belgium

BG

Bulgaria

Fares on routes subject to road competition can

be 30% lower

CZ

Czech

Republic

Road competition on the Prague-Brno route

Competition on a few routes

DK

Denmark

Formal cooperation between rail operators and

regional traffic agencies regarding rail and bus

fares

Private coach competition

Multiple operators, but coordinated fares

DE

Germany

Coach competition permitted from 2013

Competition on price between long-distance

and regional services, and some open access

long-distance operators

IE

Ireland

IT

Italy

Competition on routes served by low-cost airlines

Competition on HS services.

55% of tickets are discounted, compared to

20% in 2012.

EL

Greece

ES

Spain

Coach competition limited to national concessions

FI

Finland