1

LEND LEASE

ACQUIRES

CROSBY GROUP

June 2005

Presenter: Greg Clarke, Group CEO

• Good afternoon, ladies and gentlemen – thank you for joining the call.

• The purpose of today’s session is to provide more information to round

out your understanding of our acquisition of Crosby announced earlier

today.

• Today we are providing:

– The background to the transaction

– How it fits into our UK Communities business

– Key metrics of the Crosby business

– The transaction financials; and

– Guidance on the likely outcomes for the Group.

• The transaction follows recent growth in our wholesale funds platform and

the completion of our acquisition of the rapidly growing Actus Lend Lease

business in the US.

• Let’s go to our agenda.

2

22

Agenda

¾ Overview

¾ Group Strategy

¾ UK Residential Market Dynamics

¾ Crosby Homes

¾ Strategic Fit and Synergies

¾ Integration Strategy

¾ Acquisition Metrics

¾ Summary

¾ Q&A

• After an overview of the transaction, I’ll take you through our Group

strategy.

• Some of you may have seen this before, but it’s worthwhile reviewing post

GPT’s internalisation.

• Then I would like to cover off the key drivers in the UK residential market

which support both our Communities and Retail strategy in the UK and the

acquisition of Crosby.

• I will then provide some insight into Crosby itself and how it operates, as

well as giving an overview on key projects.

• I’ll then ask Roger Burrows to talk to the financials of the transaction and

outcomes for the Group in terms of earnings accretion and our balance

sheet capacity for pursuing other initiatives in the future.

• This is intended as a high level presentation which will be followed up by a

management presentation post completion of the transaction and after

Lend Lease’s full year results announcement mid August.

3

33

Overview

¾ Acquisition of 100% economic interest in The Crosby Group plc for approximately

£261m (A$615m)

¾ Leading urban regeneration developer – high-quality management team, solid

earnings outlook and strong asset backing

¾ Strategic extension to Lend Lease’s UK Communities business platform

¾ Adds built-form product development, high-density dwelling construction to existing

community development capability

¾ Broadens scope for Lend Lease participation in major land development schemes,

Government sponsored affordable housing and urban regeneration projects, and

mixed-use retail / residential projects

¾ Earnings enhancing for Lend Lease

– Minor EPS accretion in FY06 (under AIFRS)

– Expected to be materially accretive thereafter

• As you know Lend Lease is well-positioned in the high-growth London and

South East UK residential markets.

• Crosby is a respected brand, with strong market positions in major

regional centres such as Birmingham, Manchester and Leeds.

• The acquisition supports our growth strategy, augments our existing

Communities business, enhances our skill base and broadens our offering

to the UK market.

• Perhaps more importantly, it provides us with the scale and national

footprint that we consider necessary to underpin our ability to partner with

Government and Government agencies.

• It brings specific skills in urban renewal and high-density residential to our

Communities business …

• A strong backlog of work for the next 4 years …

• And a sound business model that provides good visibility of earnings.

4

44

¾ Markets targeted are ‘deep’

¾ Lend Lease has advantaged positions and has secured a large pipeline for

growth (interest in projects with value circa $20b)

¾ Significant opportunities for consolidation

¾ Lend Lease’s balance sheet remains strong

Double digit earnings growth

¾ Protected positions come from integrated skills

¾ Strong Group synergies in terms of generating opportunities and developing

leading property skills (Lend Lease’s privatisation positions are an example)

¾ Boosts growth and returns for shareholders

Construction Management &

Investment Management

¾ Lend Lease should expand along sector (not business unit) lines

¾ Regional retail and master planned communities are the most attractive sectors

(including ‘mixed-use’ opportunities within these ‘footprints’)

¾ Lend Lease has leading skills in both sectors

Retail & Residential

¾ Must go beyond Australia (mature and small)

¾ Opportunities not ‘global’; UK & US the first focus

Inter national

‘A leading international retail and residential property group, supported by strong construction

management and investment management businesses delivering double digit earnings growth’

‘A leading international retail and residential property group, supported by strong construction

management and investment management businesses delivering double digit earnings growth’

Group Strategy

• To place the transaction in context, let’s walk you though Lend Lease’s

strategic ambitions:

– We want to capture growth opportunities internationally in specific

markets where we have established platforms

– We want to focus on retail and residential

– We will exploit integrated skill-set across construction management

and investment management

– Our overall aim is to generate double-digit earnings growth based on

participation in deep markets where we have established positions

– And we have a measured approach to maintain balance sheet

strength.

• The acquisition is clearly consistent with this strategy and is underpinned

by a UK residential market with sound long-term fundamentals.

5

55

100

120

140

160

180

200

220

240

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

'000s

Housing Starts Net new households

Excess demand - 33k units p.a.

UK – housing starts v net new households

Source: ODPM, Scottish Executive 2004

¾ Long term undersupply of circa 33,000 p.a.

¾ Household formation has grown strongly, particularly smaller family units

¾ Lack of greenfield land together with infrastructure overload encourages high-density

development on brownfield sites

– Urban regeneration

UK Market Dynamics in Our Favour

Projected household growth (by region) 2001 to 2021

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

No

r

th

No

r

th West

Yorks & Humberside

East M

i

dl an d

s

West Midlands

East

London

South Eas t

South West

Region

Average annual new households

0%

5%

10%

15%

20%

25%

% total growth

Average annual new households Total % Growth

Source: ODPM

• As this slide shows, the UK market dynamics and public policy are working in our favour.

• Firstly, on the supply side, we need to recognise that the UK has suffered from a long-

term underinvestment in residential homes. This was highlighted in the recent UK

Government Barker review.

• The shortage has been fuelled by a number of factors. These include highly restrictive

planning, the decline in local authority housing construction and limited housing

association construction.

• This is set against the market fundamentals:

(1) Continuing population growth

(2) A continuing decline in average household size

(3) Stable affordability and house price trends, and

(4) Reduced barriers for residential investment property (sometimes called buy-to-let).

• The result is a 30,000 plus shortfall each year, notwithstanding 190,000 annual housing

starts.

• As well, there is a growing investor appetite for residential property which Crosby has

successfully tapped into.

• The Government is alive to the shortfall and issues of affordability.

• So there is great potential for the right product.

• I will elaborate a bit more on the UK policy drivers on the next slide.

6

66

¾ Need for increased housing supply (especially affordable)

¾ Recycling of brownfield land

¾ Focus on urban regeneration (no more Bluewaters / greenfield regionals)

– Lessening transport dependence

– Increased emphasis on mixed-use (retail / residential / commercial)

¾ Improving social infrastructure (schools and hospitals)

¾ Encouragement of residential investment vehicles

– REITs and SIPPs (“Self Invested Pension Plans”)

¾ Leads to opportunities in

– Mixed-use, residential-led schemes in existing urban areas

– Master planning / delivery to include private and social infrastructure (i.e. PFI)

– Sponsoring of REITs and other funds to invest in completed projects

UK Trends in Public Policy in Our Favour

• On the policy front, the signs are also good …

• Piecemeal development of land will not satisfy the shortfall.

• Hence the focus on brownfield sites (inner urban) ripe for regeneration:

– Inner urban regeneration places less demand on outlying

infrastructure provision

– This in turn provides the impetus for larger scale master-planned

development in brownfield settings.

• As well, from April 2006, the Government is allowing residential

investment property into self-invested super funds, or SIPPS as they are

known, and there is consideration of REITs which could provide further

investment support for the sector.

• We have the skills in master-planning.

• Crosby is well versed in maximising utility and appeal of brownfield sites.

• We have securitisation and funds management expertise.

• So, going forward, it looks like a great combination.

7

77

Master-planning

“Creation of Place”

Infrastructure Delivery

e.g. Greenwich & M11 Corridor

Current Core

Business

Key Worker

Housing

e.g. First Base JV

Medium-High

Density

Housing

Bovis Lend Lease

Supply Chain

Specialist

Community

Developme nt

Land

Management

Integrated

Delivery

Expansion

Complementary

Business Models

Asset / Fund

Management

Complementary to UK Communities Strategy

Expansion

Complementary

Business Models

• I’ll just say a few words here on how the acquisition complements our

existing platform.

• Our UK Communities business is focused on the creation of sophisticated

people-friendly places.

• It is already successfully partnering with the public sector to secure long-

term land banks, such as the Greenwich Peninsula project in London.

• Where we bring value to these developments is through our disciplined

focus on master-planning and the provision of both hard and soft

infrastructure to create sustainable and desirable communities.

• The acquisition of Crosby, an established brownfield developer, provides

the opportunity to extend these skills, allowing us to participate in profit

streams from high-density built-form that we are not currently capturing.

• Over time, this may also generate new asset classes for Asset

Management and Investment Management.

8

88

¾ Leading UK residential-focused urban regeneration business operating in

Midlands and North of England

¾ 70-year history, strong brand recognition and respected management

¾ Since 2002, focus on inner urban regeneration, with major schemes in

Birmingham, Leeds and Manchester, operating at the premium end of the sector

¾ Crosby provides Lend Lease with complementary skills to its UK Residential

Communities business

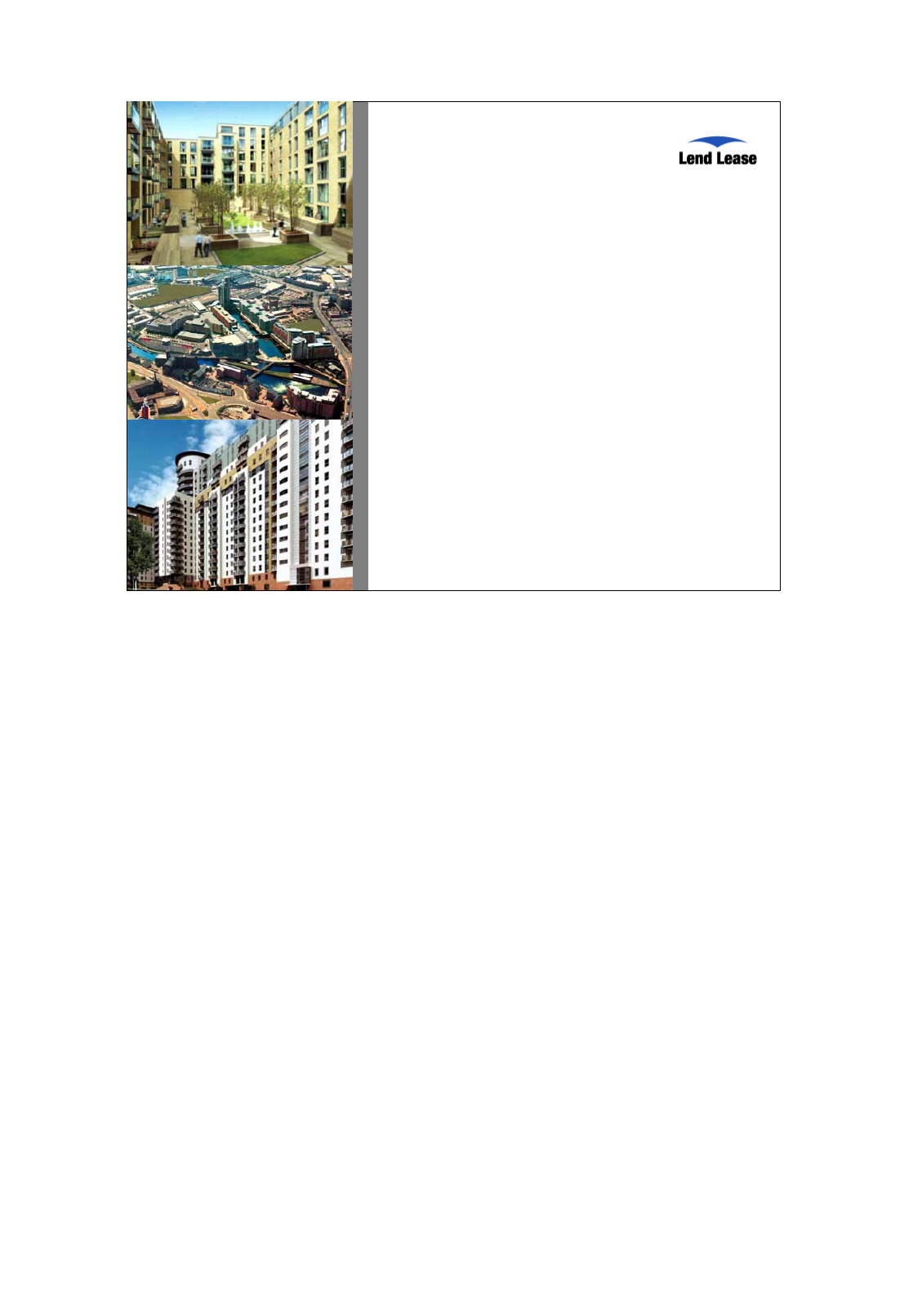

Overview – Crosby Homes

Southside, Central Birmingham Clarence Dock, Central Leeds

• So now lets look specifically at the Crosby business. Crosby is a leader in the highly

complex UK residential urban regeneration market.

• It’s got a substantial skill base and prudent approach to risk management, a strong

development pipeline and a sound business model that provides good visibility of earnings.

• It has good brand recognition (evidenced by repeat sales to residential investors) in its

core markets of the Midlands and the North of England.

• Originally a builder of executive homes, in 2002 a conscious decision was made to focus

on brownfield city centre sites, with the result that it is a more tightly managed and profit

focused business. Over recent years:

i. Staff numbers have been reduced by more than 50% from 325 to 120, focused in

three offices rather than 6

ii. Overheads have been reduced from £20 million to the current £13 million

iii. And the business is now concentrating on 14 large-scale high-density brownfield

sites with planning permission – as opposed to the 70 lower density sites under

development in 2002

iv. As a result, the business has achieved higher margins than the 15-20% found in

traditional housebuilding

v. And the focus on large scale projects has given it a competitive advantage over

smaller local competition (less able to fund these larger projects.

9

99

Strong Management Team

Geoff Hutchinson

CEO, Crosby

Phil Darcy

Regional MD

Yorkshire

Keith Pepperdine

Regional MD

Midlands

Andrew Brady

Regional MD

North West

• Clearly, Crosby has a very strong management which is staying on board

and will continue to drive the business following the acquisition.

• The team will be led by Geoff Hutchinson, who has driven Crosby’s

brownfield regeneration strategy. He has a wealth of experience in the

sector and, before joining Crosby, was Managing Director of the largest

operating division of Beazer Homes, one of the UK’s largest home

builders until its acquisition by a competitor (Persimmon) in 2001.

• The rest of the team bring specialist skills in site acquisition, planning

approval, built-form design, project management and marketing and sales

which is essential in highly complex residential brownfield regeneration

projects.

• A strong team for Lend Lease going forward.

10

1010

¾ Total of 18 principal sites with backlog of 4,500 units remaining (including JVs)

¾ Of these, 14 have planning approval, 4 are in the planning process

¾ This represents 4 years’ backlog at current sales rate of over 1,100 units p.a.

¾ Modest land acquisitions in last 2 years in line with vendor’s cash realisation

strategy

¾ Most land acquisitions have been off-market, with success in increasing density

and optimising mix

¾ Gross profit margin at circa 25%

¾ Operating margin at circa 20%

– Traditional UK housebuilder margins are 15%-20%

¾ Land cost typically 10% of sales value

¾ Construction let under lump sum contracts – no in-house construction

Crosby Homes – Business Profile

• As I outlined before, Crosby has a number of high-quality brownfield developments.

• Today it has a total of 18 principal sites, with backlog of 4,500 units remaining

(including JVs).

• Of these, 14 have planning approval, 4 are in the planning process.

• This represents 4 years’ backlog at the current sales rate of over 1,100 units p.a.

• Crosby has remained active in the land market, both to trade on and to develop, albeit

at a lower level to ensure it retains its market positioning.

• In general, land has been acquired with planning or zoning approval (or high chance of

it); it is then optimised, and phased according to market demand. Individual site

stages take say 18 months to build and are typically part pre-sold.

– Of the backlog: 3,250 units have zoning, 1,250 are awaiting zoning.

• Land acquisitions have been largely off-market – from family trusts, non-residential

property companies / owner-occupiers and the public sector etc.

• Typically, through the approval process, Crosby has been able to optimise site yield

and realise improved returns over original feasibilities. Green Quarter is an excellent

example of this – where the Crosby team acquired a site with an initial consent for 300

units and successfully negotiated an increase to 1,300 units. I’ll touch on this more

later.

11

1111

£200m

£240m £270m

£110m

0

200

400

600

800

1,000

1,200

1,400

1,600

Birmingham Manchester Leeds & York Other

Exchanged Reserved Available Not released

No. of

units

Approx

sales value

Current Projects – Unit Numbers and Sales Values

• This slide shows the value of projects by our main operating regions.

• The big projects are Clarence Dock (Leeds), Green Quarter (Manchester), and

Navigation Street and Southside in Birmingham. Prices range from £150k - £300k.

As I said earlier, we will talk in detail about this at the management presentation. But,

to give you some colour …

• All sites will have been developed by 2010 – all but 4 by 2008.

• Of the forecast apartment sales in 2005 / 06, over 75% have been pre-sold or

reserved. Of these, 70% have been sold into the investor market.

• 15% of reservations fail to proceed to exchange, and a negligible number of

exchanges fail to complete (typically less than 1%).

• There are some commercial units in the developments and these tend to be pre-sold

to investors, with the purchaser taking letting risk.

• Historically, Crosby has sold off the ground rents and outsourced ongoing property

management.

Joint Ventures

• Crosby is involved in a number of JVs, the main one being Hungate - 727 units in York

in which Crosby has a 33% interest alongside Land Securities and Evans of Leeds -

currently in planning process.

• At this stage it is probably appropriate to talk about the UK residential market.

12

1212

UK Residential Market

¾ Market fundamentals continue

to be attractive

¾ Private rental market in UK

11% v 21% in Australia

Privately

rented

11%

Home owners

71%

Social for rent

18%

UK Household Ownership

• The important factor to note is that there is significant potential for the buy-to-let

component in the UK. The Government, as we have said, is keen to stimulate

residential investment through changes in personal super and real estate investment

funds.

• At a macro level:

– The market fundamentals are attractive

– There is a recognised need to address long-term undersupply

– The economy is stable and growing

– Unemployment is low

– As are interest rates (and they are now predicted to fall rather than rise).

• Mortgage affordability is around 40% of household income which, although above the

long-term trend of 35%, is well below the 65% of the early 90s.

• Mortgage approvals, after hitting a low in November ’04, appear to have stabilised.

• Other trend data also indicate the market is normalising.

• Before leaving the Crosby overview, I will just take you through two of their large

brownfield urban regeneration projects which will give you a sense of their

capabilities.

13

1313

Urban Regeneration – Green Quarter, Manchester

Land acquired: 23 October 2000

Planning consent received: 15 September 2001

Start on site: 6 May 2003

No. of units: 1,357

Completed, exchanged, reserved: 604

Available / not released: 157 / 596

Total project value: £237m

Average unit price: £175k

• Green Quarter is a city centre urban regeneration project, about half way

through its development cycle.

• The site was originally a largely industrial area earmarked for

redevelopment.

• It is envisaged that upon completion the scheme will provide seven

residential blocks, offices and a hotel.

• The hotel and office site have been sold to a commercial developer.

• The development is approximately 500 metres to the north of

Manchester’s main retail core and transport nodes.

• As I mentioned, through the approval process Crosby negotiated an

increase in the original consent from 300 homes to 1,300.

• Of the 157 units available as at 3 May 2005, a further 96 have now been

reserved.

14

1414

Urban Regeneration – Clarence Dock, Leeds

Land acquired: 26 March 2002

Outline planning consent: 28 February 2000

Further planning consent: 1 October 2002

Start on site: 22 April 2002

No of units: 1,149

Completed, exchanged, reserved: 881

Available / not released: 13 / 255

Total project value: £242m

Average unit price: £210k

• Clarence Dock is a 15-acre landmark mixed-use development which is

being built around an existing canal basin.

• The site, which is 1 km from Leeds City Centre adjoining the River Aire,

was acquired from the British Waterways Board and incorporates the

Royal Armouries Museum.

• Clarence Dock is under development on a phased basis, and currently

has 2 blocks completed and 4 blocks started or due to start this year out

of 8.

• Of the commercial elements, the casino and hotel have been pre-sold and

the remaining units will include retail, leisure and office.

15

1515

Strategic Fit and Synergies

¾ Enhanced management capability in mixed-use, urban regeneration based on

established brand

¾ Increased capability in brownfield development

¾ Opportunity to develop residential fund management capability

¾ Synergies with existing business in

– Site selection and master planning

– Capturing residential development profits in-house

– Construction and supply chain

– Affordable housing – First Base

• From these two urban regeneration examples, you can clearly see the

relevance of the acquisition to Lend Lease. It takes us from being

“interesting” to being a scale player in urban regeneration, and gives us a

national platform for building our relationship with Government.

• We are acquiring a solid business in its own right with an excellent record

in inner urban renewal which is increasing in prominence, strong local

authority negotiating skills and transferable skill-sets.

• As a Group, this broadens our skill-set and gives us increased capability

for brownfield development.

• Longer term, it provides synergies with our UK Communities and Retail

businesses, given increased emphasis on town centre renewal often

including mandated residential components with retail development.

• We have a staged approach to integrating over the medium-longer term,

as you will see from the next slide …

16

1616

Medium Term Short Term

Integration Strategy

Approach to integration similar to Delfin

¾ Ensure business delivers on plan

¾ Supplement existing skill-sets

¾ Identify new growth opportunities

¾ Incorporate within Lend Lease Communities

¾ Full integration

• Our integration strategy mirrors the approach taken with Delfin when it

was purchased in 2001.

• The first objective will be to ensure that business delivers against its plan.

• Over time we will supplement Crosby’s management team and skill-sets to

provide capacity for growth.

• And like Delfin, over the medium term the Crosby business will be

gradually incorporated into our broader Communities business.

• Throughout this process we will identify opportunities to:

– Share and develop master planning and brownfield development

skills, and

– Realise opportunities in construction and in the affordable housing

and vertical residential development portfolios.

• Once the UK’s mooted REIT legislation is in place, we will be in a position

to use product as a platform to build a residential, mixed-use fund

management business.

• Roger will now take you through the financial metrics.

17

1717

¾ Acquisition cost approx. £261m (A$615m)

¾ 100% funded by UK debt

¾ Solid asset backing – price 1.4 times net tangible assets

¾ Purchase price equates to around 5.4 times expected FY06 EBIT

OR approx 7.7 times P/E

¾ Strong forward earnings outlook

¾ No surprises in due diligence; supported by Savills’ valuation

¾ Completion expected July 2005

Acquisition Metrics

Presenter: Roger Burrows, Group CFO

• As Greg has said, the acquisition cost is approximately £261 million,

subject to minor working capital adjustments between now and

completion.

• We will be funding the acquisition with UK denominated debt and …

• The purchase price compares favourably with the trading and

acquisition multiples of comparable companies in the UK.

• For example, comparable transactions in the sector have been at an

average of 6.5 times EBIT versus the 5.4 times we are paying.

• In addition, the purchase price at 1.4 times NTA is also well within the

range of comparable transactions.

• As further point of comparison, the acquisition P/E compares favourably

to that of Delfin when we acquired it in 2001.

• One of the main financial attractions is that the pre-sales and committed

income stream support a strong earnings outlook for Crosby.

• As Greg said earlier, it’s complementary to our strategy for the UK

market, and it’s in a sector where we have considerable knowledge.

• Completion is expected in early July.

18

1818

¾ FY05 EBIT approx. £41m (A$96m)

¾ Pre-sales backlog secures 50% first

2 years’ GPM

¾ Pre-sales secured by 10% deposits;

default rate negligible

¾ Construction costs locked in via

lump-sum contracts

¾ Authority risk mitigated – majority of

sites have already secured planning

permissions

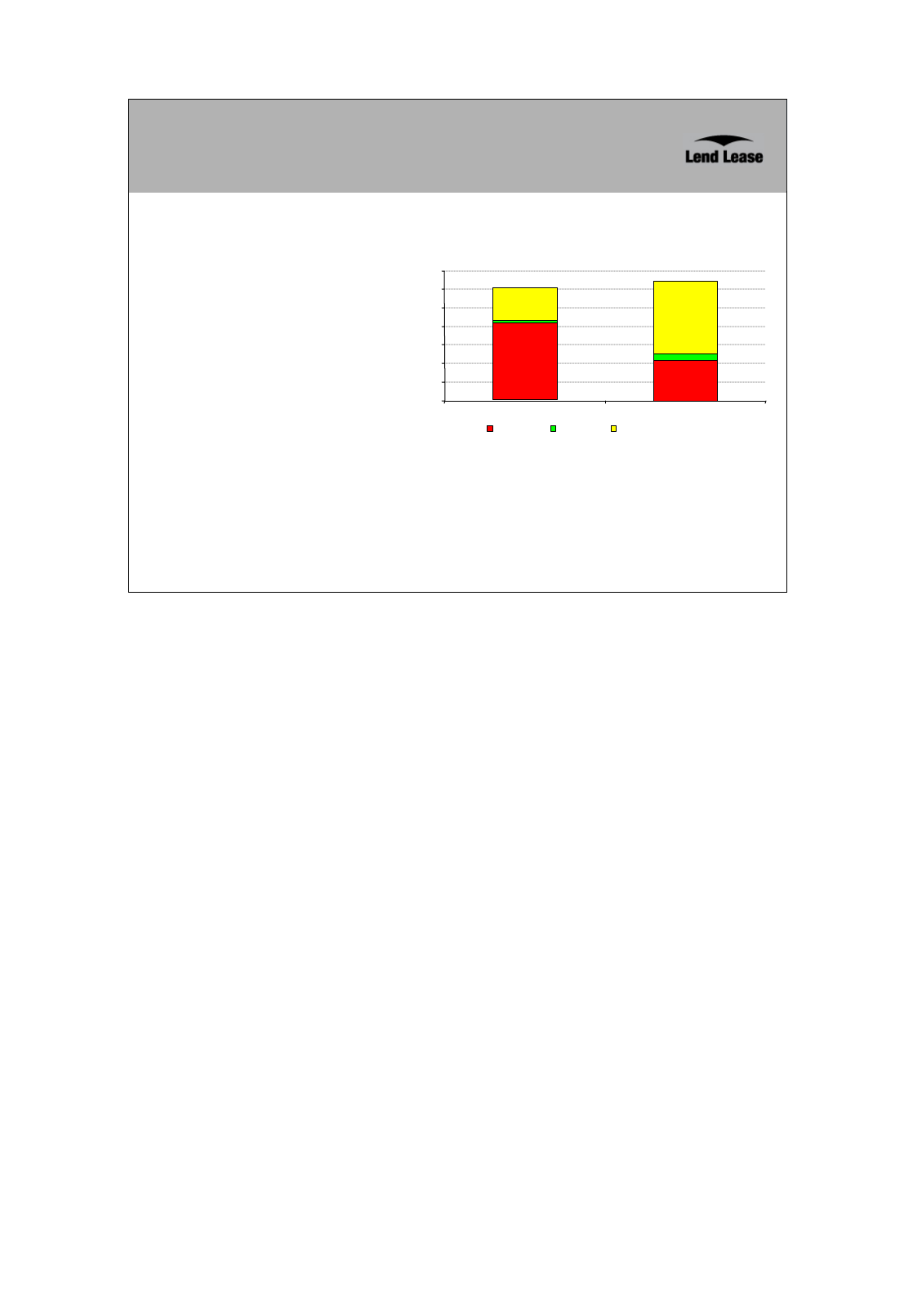

Crosby – Solid Earnings Outlook

34%

Exchanged Reserved Available / not yet released

Gross profit margin secured

(1 )

2006 / 07

2005 / 06

70%

(1)

Based on Crosby forecast, before adjusting for AIFRS and Lend Lease

accounting policies

34%

• Turning now to the earnings outlook, the pre-sales and committed income

stream support a strong and robust earnings outlook for Crosby.

• For example, the pre-sales backlog secures around 50% of Crosby’s

Gross Profit Margin – or GPM – for the next two years.

• As the slide shows, 70% of 2006 earnings are secured by pre-sales …

• As are 34% of 2007 earnings.

• These pre-sales are secured by 10% deposits, which historically have had

a negligible default rate.

• Our due diligence showed that both construction costs and planning risks

have been appropriately managed.

• I’ll take a few moments to outline the earnings outcomes for the Group.

.

19

1919

Impact on Lend Lease Earnings

¾ Short-term earnings affected by

AIFRS adjustments

– Pre-sold units reflected at sale

value on balance sheet post

acquisition

¾ Minor earnings accretion in FY06

post AIFRS adjustments and funding

costs

¾ Less significant AIFRS adjustment on

FY07 earnings

¾ Full earnings accretion post FY07

– Underlying Crosby earnings add 10

to 15% (net of funding costs) to

Lend Lease earnings

2005 / 06

2006 / 07

Gross profit margin secured

(1 )

Exchanged Reserved Available / not yet released

70%

34%

(1)

Based on Crosby forecast, before adjusting for AIFRS and Lend Lease

accounting policies

• Crosby generated EBIT of around £41 million for the 2005 financial year.

• However, as a result of accounting adjustments under the new

international accounting standards, or AIFRS, there will be a lower

earnings benefit for Lend Lease in the short term.

• This is due to the requirement under AIFRS to reflect the pre-sold units at

sale value on the balance sheet post acquisition, as opposed to at cost.

• For the 2006 financial year, around 70% of Crosby’s GPM will be affected

by this adjustment.

• Therefore, the net earnings of Crosby within Lend Lease’s result for FY06

are expected to be only marginally above the funding costs for the

acquisition.

• Clearly, with a much lower level of pre-sales of around 34% for 2007, the

impact of AIFRS on Lend Lease’s result will be significantly reduced in

that year.

• Irrespective of the AIFRS accounting adjustments, it is important to note

that Crosby’s cashflows – which underpin the acquisition – are

unaffected.

• Post 2007, the full earnings accretion from Crosby will flow to Lend

Lease’s results.

20

2020

Lend Lease Remains in Strong Financial Position

¾ Gross gearing moves from 17% to approx. 25% of total tangible assets

(assuming existing debt refinanced)

¾ Interest coverage comfortably above target minimum of 6 times

¾ Balance sheet capacity retained for investment in Retail and Residential

Communities businesses

• Following this transaction, the Group remains in a strong financial position.

• Gross gearing will move to around 25% of total tangible assets.

• Just as important, we expect interest coverage to remain comfortably

above our target of a minimum 6 times.

• So, in summary, it is an attractive acquisition that brings a robust earnings

stream with a solid outlook, and doesn’t constrain our capacity to

undertake further growth initiatives in our core businesses.

• On that note, I’ll now hand you back to Greg to sum up.

21

2121

Summary

¾ Acquiring a leading urban regeneration developer with solid earnings outlook and

strong asset backing

¾ Positive market metrics underpin Crosby earnings outlook

¾ Strategic extension to the Lend Lease land management model in the UK

¾ Extends vertical profit participation – land development, built-form development, high

density dwelling construction and estate management

¾ Potential supply chain synergies with Bovis Lend Lease

¾ Widens scope for Lend Lease participation in major mixed-use residential-led urban

regeneration projects

¾ Mildly earnings accretive 2005 / 2006

¾ Material earnings enhancing for Lend Lease from 2006 / 2007

¾ Group well-positioned to achieve strategic ambitions

• In summary, Lend Lease is very well-positioned in the high-growth London and

South East UK residential markets, and Crosby has strong market positions in

major regional centres.

• The acquisition supports our growth strategy, augments our existing Communities

business, enhances our skill base and broadens our offering to the UK market.

• Crosby has a strong brand and is a clear fit with our Master Planned Urban

Communities business, increasing its scale and footprint.

• It is a leader in the highly complex UK urban regeneration market.

• It has a substantial skill base …

• A prudent approach to risk management …

• A strong development pipeline …

• And a sound business model that provides good visibility of earnings.

• The UK has a stable and growing economy.

• There is a recognised undersupply of new housing, and the Government has

introduced initiatives which support residential investment and enhance home

affordability.

• And we are comfortable with the market dynamics and fundamentals.

• Thank you for your time.