Leeds SHMA 2017 Page | 2

September 2017

Table of Contents

Executive summary ......................................................................................................................... 9

Introduction ........................................................................................................................ 9

The Housing Market Area ................................................................................................... 9

The current housing market .............................................................................................. 10

Objectively Assessed Housing Need (OAN) ....................................................................... 11

The need for all types of housing ...................................................................................... 12

Conclusion ......................................................................................................................... 15

1. Introduction ...................................................................................................................... 16

Background and objectives ............................................................................................... 16

National Planning Policy Framework (NPPF), Planning Practice Guidance (PPG) and

other requirements ........................................................................................................... 16

Definitions ......................................................................................................................... 17

Geography ......................................................................................................................... 19

Leeds strategic context ..................................................................................................... 19

Data analysis and presentation ......................................................................................... 21

Research methodology ..................................................................................................... 22

Report structure ................................................................................................................ 22

2. Defining the Housing Market Area ................................................................................... 24

Introduction ...................................................................................................................... 24

Leeds strategic context ..................................................................................................... 24

House prices and rates of change in house prices ............................................................ 25

Migration and self-containment ....................................................................................... 28

Commuting patterns ......................................................................................................... 30

Concluding comments ....................................................................................................... 31

3. Leeds housing market review .............................................. Error! Bookmark not defined.

Introduction ...................................................................................................................... 32

Property profile ................................................................................................................. 32

Tenure characteristics ....................................................................................................... 40

Key market drivers ............................................................................................................ 51

Current households in need .............................................................................................. 53

Homeless and previously homeless households .............................................................. 56

Relative affordability of housing options .......................................................................... 58

4. Housing market signals and past delivery ......................................................................... 63

Introduction ...................................................................................................................... 63

Market Signals ................................................................................................................... 63

Comparator areas.............................................................................................................. 66

Past trends in housing delivery ......................................................................................... 69

Leeds SHMA 2017 Page | 3

September 2017

Concluding comments ....................................................................................................... 71

5. Objectively Assessed Housing Need and Housing Requirement ...................................... 72

Introduction ...................................................................................................................... 72

Establishing the Housing Market Area .............................................................................. 73

LPEG model ....................................................................................................................... 73

PPG model ......................................................................................................................... 75

Objectively Assessed Housing Need ................................................................................. 83

From an OAN to a Housing Requirement ......................................................................... 84

DCLG consultation regarding the calculating of OAN ....................................................... 87

6. The need for all types of housing ...................................................................................... 88

Introduction ...................................................................................................................... 88

Dwelling mix and affordability .......................................................................................... 88

People wishing to build their own homes ........................................................................ 96

Family housing................................................................................................................... 97

Armed forces accommodation .......................................................................................... 97

Older people ...................................................................................................................... 97

Households with specific needs ...................................................................................... 102

7. Conclusion: policy and strategic issues ........................................................................... 104

The Housing Market Area ............................................................................................... 104

The current housing market ............................................................................................ 104

Objectively Assessed Housing Need, market signals and Housing Requirement ........... 104

The need for all types of housing .................................................................................... 105

Final comments ............................................................................................................... 105

Introduction to Technical Appendices ........................................................................................ 106

Technical Appendix A: Research methodology ........................................................................... 107

Overall approach ............................................................................................................. 107

Baseline dwelling stock information and survey sample errors ..................................... 107

Interviews with estate and letting agents ....................................................................... 108

Technical Appendix B: Housing policy review ............................................................................. 109

Introduction .................................................................................................................... 109

Legislative and policy background .................................................................................. 109

Emerging policy and legislation....................................................................................... 114

Overview of housing policy themes ................................................................................ 116

National housing reviews ................................................................................................ 123

Technical Appendix C: Housing need calculations ...................................................................... 125

Summary of contents ...................................................................................................... 125

Introduction .................................................................................................................... 126

Leeds SHMA 2017 Page | 4

September 2017

Stage 1: Current need .................................................................................................... 129

Stage 2: Future housing need ........................................................................................ 133

Stage 3: Affordable housing supply ................................................................................ 134

Stage 4: Estimate of annual housing need ..................................................................... 135

Total net imbalance ......................................................................................................... 136

Tenure and dwelling type profile of affordable dwellings .............................................. 137

Technical Appendix D: Monitoring and updating ....................................................................... 141

A framework for updating the housing needs model and assessment of affordable

housing requirements ..................................................................................................... 141

Introduction .................................................................................................................... 141

Updating of baseline housing needs and affordable housing requirements ................. 141

Concluding comments ..................................................................................................... 143

Technical Appendix E: National Planning Policy Framework and Planning Practice Guidance

Checklist 144

National Planning Policy Framework .............................................................................. 144

Planning Practice Guidance ............................................................................................. 144

List of Tables

Table ES1 Suggested dwelling mix by market and affordable dwellings based on OAN of

3789 each year ...................................................................................................... 12

Table 2.1 House prices in Leeds 2016 by sub-area ............................................................... 27

Table 2.2 House prices and price change in neighbouring areas, Yorkshire and the Humber

and England ........................................................................................................... 28

Table 2.3 Flows of residents (all moves) ............................................................................... 29

Table 2.4 Containment ratios ............................................................................................... 30

Table 2.5 Leeds 2011 Census commuting flows: workers (aged 16-74 years) ..................... 30

Table 3.1 Dwelling stock and occupancy by sub-area .......................................................... 32

Table 3.2 Property type and size of occupied dwellings across Leeds ................................. 33

Table 3.3 Age of dwelling ...................................................................................................... 36

Table 3.4 Dwelling stock condition in England and Leeds estimates ................................... 37

Table 3.5 Lower Quartile and median price and income required to be affordable ........... 40

Table 3.6 Profile of private rented sector in Leeds ............................................................... 46

Table 3.7 Private sector rental prices in Leeds 2010-2016 ................................................... 47

Table 3.8 Primary market drivers ......................................................................................... 51

Table 3.9 Projected population change, 2017 to 2033 ......................................................... 52

Table 3.10 Housing need in Leeds .......................................................................................... 54

Leeds SHMA 2017 Page | 5

September 2017

Table 3.11 Households in need by Affordable Housing Zone ................................................. 55

Table 3.12 Households in need by sub-area ........................................................................... 55

Table 3.13 Housing need by tenure ........................................................................................ 56

Table 3.14 Housing need by household type .......................................................................... 56

Table 3.15 Homeless decisions and acceptances 2009/10 to 2015/16 .................................. 57

Table 3.16 Characteristics of households previously homeless ............................................. 58

Table 3.17 Cost of alternative tenure options by sub-area .................................................... 59

Table 3.18 Annual income required for alternative tenure options by sub-area .................. 60

Table 3.19 Assumptions in assessing income required for alternative tenure options ......... 61

Table 4.1 Housing market signals 2005-2015 ....................................................................... 65

Table 4.2 Housing market signals in comparator districts, region and England 2010-2015 68

Table 4.3 Dwelling completions 2006/07 to 2015/16 .......................................................... 69

Table 5.1 Full Objectively Assessed Housing Need using the LPEG method ........................ 75

Table 5.2 Dwelling requirements under alternative scenarios using 2014-based and

alternative headship rates .................................................................................... 77

Table 5.3 Labour force and employment growth outcomes 2017-2033 .............................. 80

Table 5.4 Employment-led REM and Average employment growth outcomes 2017-2033 . 81

Table 5.5 Employment-led scenario Dwelling requirements under alternative scenarios

using 2014-based and alternative headship rates ................................................ 81

Table 5.6 Factors included in OAN calculation methods ...................................................... 87

Table 6.1 Overall market dwelling requirements compared with the current stock profile 89

Table 6.2 Comparison between current dwelling stock and market aspirations at sub-area

level ....................................................................................................................... 91

Table 6.3 Comparison between current dwelling stock and market expectations at sub-

area level ............................................................................................................... 92

Table 6.4 Net annual affordable housing imbalance by Affordable Housing Zone, property

size and designation 2017/18 to 2027/28 ............................................................ 93

Table 6.5 Affordable housing tenure options: existing and newly-forming households ..... 94

Table 6.6 Relative affordability of intermediate tenure prices ............................................ 94

Table 6.7 Suggested dwelling mix by market and affordable dwellings based on OAN of

3789 each year ...................................................................................................... 95

Table 6.8 Older persons’ housing options ............................................................................ 98

Table 6.9 Dwelling aspirations and expectations of households containing a HRP aged 65+99

Table 6.10 Future housing expectations (upsizing/downsizing) ............................................ 99

Table 6.11 Older persons’ dwelling requirements 2014 to 2035 ......................................... 100

Leeds SHMA 2017 Page | 6

September 2017

Table 6.12 Future market split of older persons’ accommodation by relative

deprivation/affluence of an area ........................................................................ 101

Table 6.13 Adaptations required either now or in next 5 years by age group ..................... 101

Table 6.14 Client groups accommodated in Social Rented sector in Leeds City 2010/11 to

2012/13 ............................................................................................................... 102

Table A1 Households surveyed, response rates and sample errors .................................. 107

Table C1 CLG Needs Assessment Summary for Leeds City Council ................................... 127

Table C2 CLG Needs Assessment Summary by Affordable Housing Zone ......................... 128

Table C3 Summary of current housing need across Leeds District ................................... 129

Table C4 Summary of current need by Affordable Housing Zone ..................................... 130

Table C5 Homeless decisions and acceptances 2009/10 to 2015/16 ................................ 131

Table C6 Lower quartile house prices by Housing Market Character Area ....................... 133

Table C7 Net annual affordable housing imbalance by Affordable Housing Zone, property

size and designation 2017/18 to 2026/27 .......................................................... 137

Table C8 Affordable housing tenure options: existing households in need ...................... 138

Table C9 Affordable housing tenure split .......................................................................... 138

Table C10 Affordable housing tenure options: newly-forming households ........................ 138

Table C11 Relative affordability of intermediate tenure prices .......................................... 139

Table C12 Property type preferences .................................................................................. 140

Table C13 Property type preferences by affordable housing zone ..................................... 140

List of Figures

Figure 2.1 Median house price trends 2005 to 2016: Leeds, North Yorkshire and England . 26

Figure 3.1 Property type by sub-area..................................................................................... 34

Figure 3.2 Property size by sub-area ...................................................................................... 35

Figure 3.3 Leeds tenure profile of occupied dwellings .......................................................... 38

Figure 3.4 Leeds tenure profile by sub-area .......................................................................... 39

Figure 3.5 Leeds City household income and housing costs comparison .............................. 62

Figure 4.1 Dwelling completions 2006/07 to 2015/16 compared with the annual target .... 70

Figure 4.2 Housing delivery test ............................................................................................. 71

Figure 5.1 Housing Needs Assessment for Leeds (based on PAS Guidance OAN advice note

July 2015 Figure 4.1) ............................................................................................. 86

Figure 6.1 Market development requirements compared with the current stock profile .... 89

Leeds SHMA 2017 Page | 7

September 2017

List of Maps

Map 1.1 Leeds location and geographical context.............................................................. 19

Map 1.2 Leeds City Region and local authority context ...................................................... 20

Map 1.3 Leeds sub-areas ..................................................................................................... 21

Map 2.3 Median house prices 2015 by sub-area ................................................................ 27

Map 3.1 Median rents 2016 by sub-area ............................................................................ 48

Leeds SHMA 2017 Page | 8

September 2017

Please note that in this report some of the tables include rounded figures. This can result in

some column or row totals not adding up to 100 or to the anticipated row or column ‘total’

due to the use of rounded decimal figures. We include this description here as it covers all

tables and associated textual commentary included. If tables or figures are to be used in-

house then we recommend the addition of a similarly worded statement being included as a

note to each table used.

This report takes into account the particular instructions and requirements of our client. It is not intended for and

should not be relied upon by any third party and no responsibility is undertaken to any third party.

arc

4

Limited accepts no responsibility or liability for, and makes no representation or warranty with respect to, the

accuracy or completeness of any third party information (including data) that is contained in this document.

Leeds SHMA 2017 Page | 9

September 2017

Executive summary

Introduction

The Leeds Strategic Housing Market Assessment (SHMA) (2017) provides the latest available

evidence to help to shape the future planning and housing policies of the area. The study will

help inform the production of the Council’s local plan and housing strategy. This research

provides an up-to-date analysis of the social, economic, housing and demographic situation

across the area.

The SHMA (2017) contains:

• A review of existing (secondary) data;

• Analysis of the findings of a household survey, completed by 5,383, representing a 19.3%

response rate;

• A consideration of the findings of interviews with estate and lettings agents;

• A consideration of research by Edge Analytics regarding Objectively Assessed Housing Need

(OAN);

• An assessment of housing need and affordable housing requirements; and

• Analysis of the housing needs of specific groups of people.

The findings from the study provide an up-to-date, robust and defensible evidence base for

policy development which conforms to the Government’s National Planning Policy Framework

(NPPF) and Planning Practice Guidance (PPG), Housing and economic development needs

assessments.

The Housing Market Area

Defining the housing market area

Leeds’s Housing Market Area (HMA) exhibits a degree of distinctiveness compared with

neighbouring areas as measured by median house price change 2000-2016 at a lower rate than

most neighbouring local authority areas and the Yorkshire and the Humber region as a whole.

The Leeds HMA is considered to be self-contained from the perspective of migration and in

terms of low levels of out-commuting by its working population but it has a significant

economic function that also draws commuters from the wider City Region.

Interactions with several neighbouring areas are recognised, research identifies relationships

with the northern part of Kirklees and with the Wharfedale part of Bradford. These local

authorities recognise that they operate as a wider functional area from an economic

perspective, but they do not consider Leeds as part of their respective Housing Market Areas

for the purposes of local planning policy.

In conclusion, although there are interactions with other areas, Leeds should be recognised as

an appropriate Housing Market Area for the purposes of local planning policy.

Leeds SHMA 2017 Page | 10

September 2017

The current housing market

The aim of the Leeds housing market review is to explore the housing market dynamics of

Leeds. The evidence is based upon household survey data, secondary data and information

from stakeholders.

The study finds that there are 337,302 households and 347,787 dwellings in Leeds City. With

8,578 vacant homes (of which 2,681 are long term vacant) and 2,038 are second homes. The

overall vacancy rate is around 2.5%, this compares with a vacancy rate of 2.6% across England.

Overall, the vast majority (70.4%) of properties are houses, 22.6% are flats/apartments and

maisonettes, 6.4% are bungalows, and 0.6% are other types of property including park

homes/caravans. Of all occupied properties, 14.90% have one bedroom/bedsit, 28.6% have

two bedrooms, 38.2% have three bedrooms and 18.3% have four or more bedrooms.

Regarding tenure, 57.7% of occupied dwellings are owner-occupied, some 29.9% of all

households (100,978) own outright and 27.7% of all households (93,482) have a mortgage.

19.9%. are private rented (including tied accommodation and student housing) and 22.5% are

affordable.

The mix of property size type and tenure varies greatly by sub-area. The size and type of

dwelling varies greatly within tenure. Some 21.7% of owner occupied homes are detached and

5.9% are flats, apartments and maisonettes, whereas, regarding the private rented sector 5.1%

are detached and 46.1% are flats and maisonettes.

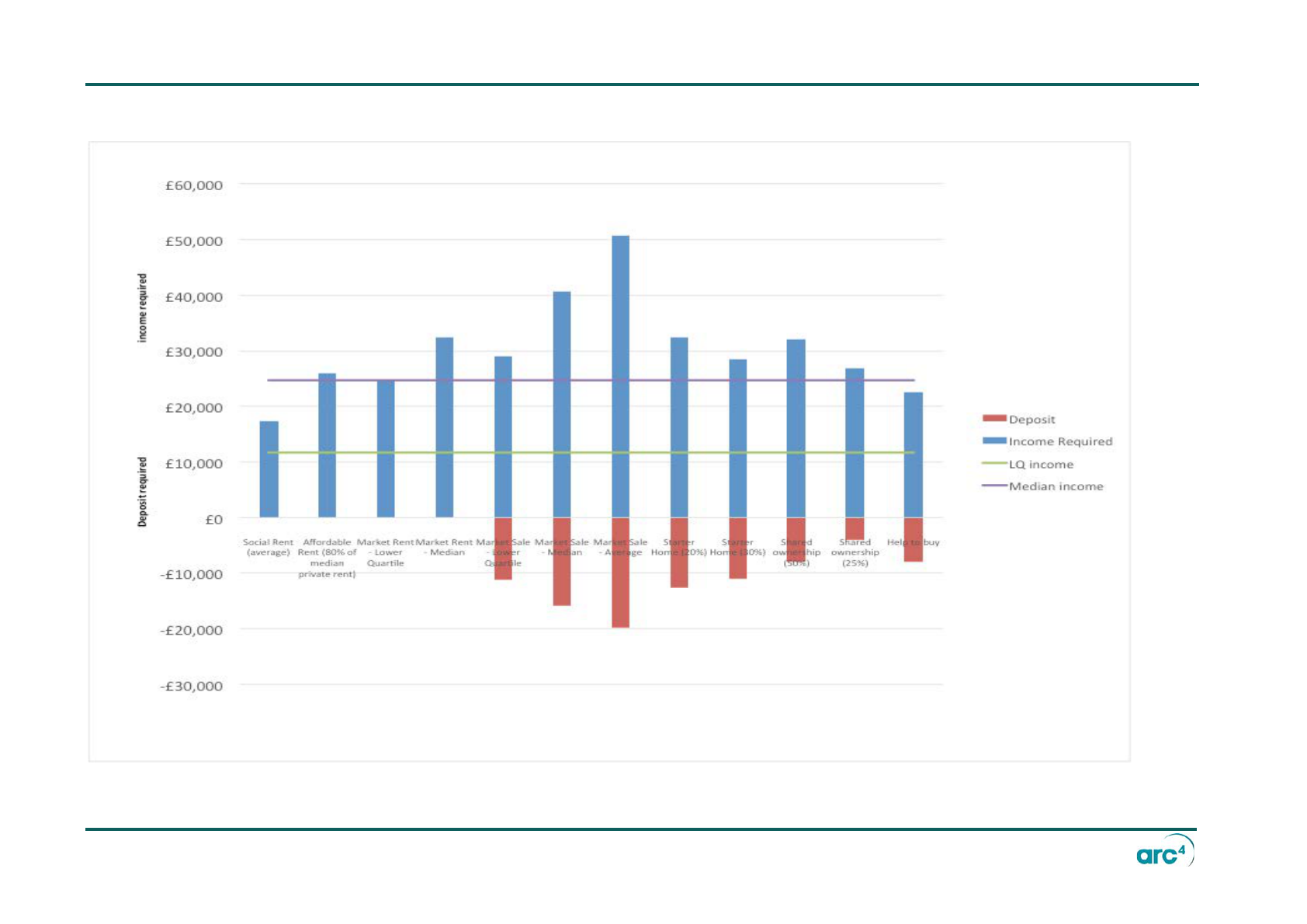

In 2016, median house prices across the city were £159,000 and lower quartile prices were

£110,000. For open market housing, the minimum indicative income required is £24,768 for

lower quartile or entry-level renting in the City as a whole. For lower quartile or entry-level

house prices (owner occupation) the minimum income required is £28,929.

Median rents across the city were £676 per month and lower quartile rents were £516 per

month.

Estate agents told us that housing markets in Leeds have largely recovered from the 2008

recession with sales showing increased demand over the past 3 years. Leeds has traditionally

been a strong housing market. It is currently seen as offering better returns on investment

than Manchester, for example, and is anecdotally better value than other surrounding cities

e.g. Sheffield and Hull, etc. We were told that the housing market in the city centre is distinctly

different than in other parts of Leeds as the market offer is almost entirely apartments. We

were told that until recently the market was investor led. Agents told us that the main drivers

of the market include the level of inward investment fuelling expectation around the city; and

the skilled nature of jobs that have been created in Leeds which has created a good fit

between income, borrowing levels and mortgage rates which normally equates to a lot of

potential in the market. The concern is the general undersupply of properties to let.

Letting agents told us that the rental market has remained relatively strong buoyed by

customers unable / unwilling to buy in the current market either due to affordability pressures

or lack of supply. The typical renter is professional; is single and wants their independence; a

couple or a small family ready to settle down but can’t afford the deposit; ex-students who

have finished studying and want to remain local; newly arrived employees of the growing

business sector who want to rent. Agents also report that a growing number of households are

selling their homes and choosing to rent as a lifestyle choice. Increasingly, landlords across the

Leeds SHMA 2017 Page | 11

September 2017

city are refusing to let properties to people on benefits. Where lets are made to households on

benefits, landlords insist on a guarantor who is in employment and able to meet the full rent

requirement in the event of a default.

According to our survey some 31,740 existing households are in housing need (9.4% of all

households). Reasons for housing need are mostly overcrowding, cost, a tenancy ending,

households sharing facilities or due to people having special needs. Although housing need is

evidenced across the city, housing need issues are most prevalent in the inner area and the

city centre, in the private rented sector and amongst lone parent, large family households and

student households.

The Household Survey identified 4,831 households who had been previously homeless or living

in temporary accommodation and had moved to their present accommodation in the past five

years. These were mostly single adults and lone parents, occurring in flats and maisonettes and

within the private rented sector.

Objectively Assessed Housing Need (OAN)

The National Planning Policy Framework (NPPF) requires that Local Planning Authorities (LPAs)

identify Objectively Assessed Housing Need (OAN) and that Local Plans translate those needs

into land provision targets. Paragraph 159 of the NPPF recognises that the objective

assessment of housing need must be one that meets household and population projections,

taking account of migration and demographic change; meets the need for all types of housing

including affordable, and caters for housing demand and the scale of housing supply necessary

to meet that demand. Government Planning Practice Guidance (PPG) recognises that

‘establishing future need for housing is not an exact science’ (paragraph 14), although it should

be informed by reasonable and proportionate evidence.

The SHMA firstly sets out the OAN calculation based on the approach set out in the Local Plan

Experts Group report. Secondly, an OAN calculation based on the Planning Practice Guidance

(PPG) is undertaken. The key difference between the approaches is that the second approach

introduces some economic factors into the calculation.

The SHMA concludes that the challenge for the council is to deliver an appropriate and

proportionate level of dwelling growth that supports economic growth and carefully takes into

account the current demographic profile of the district.

Key features of the OAN recommended in the SHMA report are:

• Demographic factors: a baseline of 2,534 is adjusted to 2,765 to take account of higher

rates of household formation amongst the 25-44 age group;

• A market signals uplift of 15% of the basic demographic requirement (380 dwellings each

year) is also recommended, which also takes into account underlying affordable housing

need as evidenced in the 2017 SHMA household survey;

• After considering several employment growth scenarios it is recommended that the OAN is

expressed as a range and that the total dwelling need is between 44,240 and 60,528 over

the Plan period 2017-2033.

Leeds SHMA 2017 Page | 12

September 2017

The need for all types of housing

Having established the Objectively Assessed Need for housing, the SHMA goes on to consider

the range of need for all types of housing as identified in PPG paragraph 21. The SHMA

considers the needs of different groups, including the private rented sector, people wishing to

build their own homes, family housing, housing for older people, households with specific

needs and student housing.

Dwelling mix and affordability

The NPPF (paragraph 159) states that local authorities should identify the scale and mix of

housing and the range of tenures that the local population is likely to need over the Plan

period.

Table 6.5 below provides our recommendation on the potential dwelling tenure, type and size

split for housing delivery in Leeds. This assumes that 25% of homes delivered are affordable

based on past trends in affordable delivery.

Table ES1 Suggested dwelling mix by market and affordable dwellings based on OAN of 3789

each year

Overall dwelling size mix

Market

Affordable

Total

Overall tenure split

75%

25%

100%

House 1-2 Bed

613

243

856

House 3+ Bed

996

116

1,112

House 4+ Bed

491

59

549

Bungalow

167

83

250

Flat/Apartment

539

446

985

Other

37

0

37

Total

2,843

946

3,789

Source: arc4

People wishing to build their own homes

The 2017 Household Survey identified 812 households planning to move in the next five years

who would like to move into a self/custom-build property. The Household Survey identified

the characteristics of households considering self/custom-build:

• 43.7% lived in affordable housing, 43.0% in private rented housing and only 13.2% were

owner occupiers;

• 43.7% were couples with one or two children, 35.8% were singles under 65, 18.2% were

couples under 65 (no children) and 2.2% were couples over 65;

• 33.6% had an income of less than £15,600 per annum and 50.0% had an income of more

than £49,400 per year; and

Leeds SHMA 2017 Page | 13

September 2017

• 43.0% would like a two-bedroom property and 52.5% would like a property with four or

more bedrooms;

• All households considering self/custom build stated an open market tenure preference, but

additionally one third stated a preference for intermediate tenures and one-third stated a

preference for affordable renting. Therefore, self/custom build could have a role in

delivering affordable housing.

The level of demand for self/custom build should be monitored closely by the Council.

Family housing

Families (that is couples and lone parents with children including adult children living at home)

account for around 30.5% of households across Leeds. Of this number, 70.8% are couples with

children and 29.2% are lone parents with children (2017 Household Survey data).

Overall 73.8% of families live in owner-occupied dwellings, 15.5% live in the private rented

sector and 10.7% live in affordable dwellings. 24.3% of all families live in the North Leeds sub-

area.

The evidence shows that lone parent families are more likely to live in unsuitable housing or

experience homelessness especially if they reside in the private rented sector.

Armed forces accommodation

The 2011 Census identified that 691 residents in Leeds City are employed in the Armed Forces.

Of these, 95.2% lived in a household and 4.8% live in a communal establishment.

More recent records identify 80 Ministry of Defence personnel living within Leeds, which

represents 0.6% of the total for the region of Yorkshire and the Humber (12,320).

Older people

A major strategic challenge is to ensure a range of appropriate housing provision, adaptation

and support for the area’s older population. PPG paragraph 21 states that ‘the need to provide

housing for older people is critical given the projected increase in the number of households

aged 65 and over accounts for over half of new households’.

The number of people across Leeds City area aged 65 or over is projected to increase from

121,700 in 2017 to 158,500 by 2033 (a 30.2% increase) according to the ONS 2014-based

population projections.

The 2017 Household Survey identifies the following key findings:

• 23.6% of households across Leeds are either singles or couples aged 65 years or over;

• 54.4% live in owner-occupied properties, 8.4% live in the private rented sector and 37.2%

live in affordable accommodation;

• 21.6% of all older households live in the North Leeds sub-area, 19.7% in Inner Area and

15.9% in Outer West;

Leeds SHMA 2017 Page | 14

September 2017

• 77.3% want to stay in their own homes with help and support when needed;

• 14.3% would consider buying a property on the open market;

• Sheltered accommodation and Extra Care housing are identified as further options;

• Around 11.0% of older households would consider co-housing; and

• 43.8% of households are planning to downsize.

Of all older person households (HRP aged 65+), 3.4% intend to move in the next five years and

a further 11.5% stated that they would like to move but are unable to. Of households who are

unable to move, reasons stated included cannot afford to (32.1%), lack of suitable property in

the area wanted (21.8%) and lack of suitable property of the type wanted (14.2%).

A key feature of the survey is to understand the aspirations and expectations of older people:

• 54.5% would like to move to a bungalow, and 53.4% expect to;

• 23.1% would like move into a flat and 15.7% expect to;

• 62.1% would like a one or two-bedroom property and 72.8% expect to.

Information from Housing Learning and Information Network (LIN) estimates that over the

period 2014 to 2035, there is expected to be a 75% increase in the requirement for older

persons’ specialist provision. However, when the current (2014) supply of accommodation is

compared with change in demand to 2035, data would suggest a need to increase the current

level of provision for older people, particularly the provision of enhanced sheltered housing

and Extra Care 24/7 support.

The Household Survey asked respondents whether they need adaptations to their home,

either now or in the next five years. In respect of the 65+ cohort, the adaptations considered

most important included adaptations to bathrooms (16.0%), internal handrails (11.6%) and

better heating (9.7%).

This evidence suggests a need to continue to diversify the range of older persons’ housing

provision. Additionally, providing a wider range of older persons’ accommodation has the

potential to free-up larger family accommodation.

Households with specific needs

The evidence shows that single homeless people with support needs (an average of 1,036 per

year) and older people with support needs (an average of 550 per year) are the main groups

provided for.

The need for accessible dwellings has been explored and it is recommended that the Council

seeks, as a minimum, 17.5% of new dwellings to be accessible dwellings and, in addition, a

minimum of 5% to be wheelchair accessible.

Black, Asian and Minority Ethnic households

The 2011 Census reports that 91.0% of residents are White British and the next largest ethnic

group is White Other (including Irish and Gypsies and Travellers) (4.7%), Asian/Asian British

(1.8%), Black/Black British (0.7%) Mixed/Multiple Ethnic (1.5%), and other groups (0.2%).

Leeds SHMA 2017 Page | 15

September 2017

The 2017 Household Survey identified that 89.7% of households are White British, 2.5% White

Other, 2.3% Asian/Asian British, 1.7% White Central and Eastern European, 1.3% Black/Black

British, 1.2% Mixed/Multiple Ethnic and 1.3% other groups.

The 2011 Census identified 652 residents across 257 households who stated that they had

Gypsy or Irish Traveller ethnicity. 43 of these households lived in a caravan or other

mobile/temporary structure with the remainder in bricks and mortar (house, bungalow, flat or

maisonette).

The January 2017 DCLG Caravan Count identified a total of 122 Gypsy and Traveller caravans,

84 on local authority-owned sites and 38 on unauthorised sites. No Travelling Showpeople

caravans were identified.

A Gypsy and Traveller Accommodation Assessment was carried out in 2014 which identified a

current authorised residential provision of 48 pitches (41 on local authority sites and 7 on

private sites). A total need for 62 pitches up to 2027/28 was identified.

Conclusion

The evidence presented in this SHMA suggests that there are three main policy areas that

require special attention from both a planning policy and social policy perspective:

• The challenge of enabling the quantity and mix of housing that needs to be delivered;

• The challenge of ensuring that the housing and support needs of older people are met

going forward;

• The challenge of driving up the quality of the private rented sector and increasing the

sustainability of tenancies.

Leeds SHMA 2017 Page | 16

September 2017

1. Introduction

Background and objectives

This Strategic Housing Market Assessment (SHMA) for Leeds City Council (the Council)

has been commissioned to provide an up-to-date evidence base to help shape the

future planning and housing policies and strategies for the area.

The SHMA satisfies the requirements of the National Planning Policy Framework (NPPF,

March 2012) and National Planning Practice Guidance (NPPG), Housing and economic

development needs assessments (last updated February 2016), which replace previous

guidance including the DCLG Strategic Housing Market Assessment Guidance (Version

2, 2007).

The SHMA includes a review of the Housing Market Area definition, Objectively

Assessed Housing Need, Housing Market Signals and Duty to Co-operate matters. The

SHMA takes into account latest legislative requirements and updated population and

employment data.

National Planning Policy Framework (NPPF), Planning Practice

Guidance (PPG) and other requirements

The NPPF and PPG, Housing and economic development needs assessments, provide the

planning policy context for this SHMA. The key sections which need to be taken into

account in the SHMA are now summarised.

The NPPF (paragraph 159) states that Local Planning Authorities should have a clear

understanding of housing needs in their area and they should prepare a Strategic

Housing Market Assessment to assess their full housing needs, working with

neighbouring authorities where housing market areas cross administrative boundaries.

The SHMA should identify the scale and mix of housing and the range of tenures that

the local population is likely to need over the Plan period that:

• Meets household and population projections, taking account of migration and

demographic change;

• Addresses the need for all types of housing, including affordable housing and the

needs of different groups in the community (such as, but not limited to families

with children, older people, people with disabilities, service families and people

wishing to build their own homes); and

• Caters for housing demand and the scale of housing supply necessary to meet this

demand.

PPG (paragraph 2) sets out that ‘the primary objective of identifying need is to identify

the future quantity of housing needed, including a breakdown by type, tenure, and size.’

PPG (paragraph 8) states that housing needs should be assessed in relation to the

relevant functional area i.e. Housing Market Area and this may identify smaller sub-

markets with specific features and it may be appropriate to investigate these

specifically in order to create a detailed picture of local need. It is also important to

Leeds SHMA 2017 Page | 17

September 2017

recognise that there are 'market segments' i.e. not all housing types have the same

appeal to different occupants.

The NPPF (paragraph 47) makes it clear that local planning authorities should ‘use their

evidence base to ensure that their Local Plan meets the full objectively assessed needs

for market and affordable housing’. The SHMA Update 2017 will provide robust

evidence to help the Council ‘plan for a mix of housing based on current and future

demographic trends, market trends and the needs of different groups in the community’

and will ‘identify the size, type tenure and range of housing that is required in particular

locations, reflecting local demand’ (NPPF paragraph 50).

The NPPF and the Localism Act 2011 both introduced the Duty to Co-operate as a

replacement for Regional Spatial Strategy (RSS). Section 110 of the Localism Act

requires local authorities to co-operate with other local authorities in maximising the

effectiveness with which strategic matters within development plan documents are

prepared. The provision of housing development is a strategic priority and the Council

will have to ensure that they are legally compliant with the Localism Act at Examination.

The Duty to Co-operate applies to all local planning authorities, working with

neighbouring authorities and other bodies, including Local Enterprise Partnerships, on

strategic priorities. It also means collaborating on the evidence critical to understanding

the needs of your area, and the wider economic and Housing Market Areas, including

through the preparation of a Strategic Housing Market Assessment.

Technical Appendix E provides a checklist of how the SHMA satisfies the requirements

of the NPPF and PPG.

Definitions

PPG (paragraph 3) provides a broad definition of need for housing:

‘…the scale and mix of housing and the range of tenures that is likely to be needed in the

housing market area over the Plan period – and should cater for the housing demand of

the area and identify the scale of housing supply necessary to meet that demand.’

Affordable housing need is defined in PPG (paragraph 22) as:

‘…the number of households and projected households who lack their own housing or

live in unsuitable housing and who cannot afford to meet their housing needs in the

market.’

For the purposes of this study, the term housing need refers to:

‘…the housing that households are willing and able to buy or rent, either from their own

resources or with assistance from the state’

1

.

Definitions relating to affordable housing are set out in the National Planning Policy

Framework (March 2012):

1

Planning Advisory Service Objectively Assessed Need and Housing Targets Technical Advice Note June 2014

Leeds SHMA 2017 Page | 18

September 2017

• Affordable Housing: Social Rented, Affordable Rented and Intermediate housing,

provided to eligible households whose needs are not met by the market. Eligibility is

determined with regard to local incomes and local house prices. Affordable housing

should include provisions to remain at an affordable price for future eligible

households or for the subsidy to be recycled for alternative affordable housing

provision.

• Social Rented housing is owned by local authorities and private Registered

Providers (as defined in Section 80 of the Housing and Regeneration Act 2008), for

which guideline target rents are determined through the national rent regime. It

may also be owned by other persons and provided under equivalent rental

arrangements to the above, as agreed with the local authority or with the Homes

and Communities Agency.

• Affordable Rented housing is let by local authorities or private Registered Providers

of social housing to households who are eligible for Social Rented housing.

Affordable rent is subject to rent controls that require a rent of no more than 80%

of the local market rent (including service charges, where applicable).

• Intermediate housing is homes for sale and rent provided at a cost above Social

rent, but below market levels subject to the criteria in the Affordable housing

definition above. These can include shared equity (shared ownership and equity

loans), other low cost homes for sale and Intermediate rent, but not Affordable

Rented housing.

• Homes that do not meet the above definition of affordable housing, such as “low

cost market” housing, may not be considered as affordable housing for planning.

These definitions of affordable housing are correct at the time of publication of this

report (mid-2017), although revisions to the NPPF are anticipated. Additionally, councils

are required to provide Starter Homes under the provisions of the Housing and

Planning Act 2016

2

. The Government has outlined the key characteristics of Starter

Homes

3

and the Housing and Planning Act 2016 officially introduced Starter Homes into

legislation, defined in Section 2 of the Act as:

• new dwellings available for purchase by ‘qualifying first-time buyers’ only; these are

defined as people who don’t already own a home and who are aged 23-40; and

• to be sold at a discount of at least 20% of their market value, and always for less

than the price cap (currently set to £450,000 in Greater London; £250,000 outside

London).

Many of the details relating to Starter Homes are to be specified in forthcoming

regulations (secondary legislation), which is still awaited following consultation in

2016

4

.

2

The Government consulted on proposals to change the NPPF (December 2015) including the definitions of affordable housing

3

National Planning Practice Guidance, paragraph 002, Reference ID 55-002-20150318

4

DCLG Starter Homes Regulations: Technical Consultation was published in March 2016

Leeds SHMA 2017 Page | 19

September 2017

Geography

Map 1.1 illustrates the geographical context of Leeds City, located within the County of

West Yorkshire and in the region of Yorkshire and the Humber. Located at the

intersection of the M1 and M62 motorways, Leeds is on the east coast mainline railway,

two hours from London Kings Cross.

Map 1.1 Leeds location and geographical context

Leeds strategic context

Following the abolition of regional planning bodies and their associated strategies and

targets, the last few years have seen ‘Local Enterprise Partnerships’ (LEPs) established

across England to help empower locally-driven economic growth at a strategic level. In

addition, ‘Combined Authorities’ (CA) have been established in several urban areas to

assist in strategic collaboration. In some cases, this has included devolution and the

election of regional mayors.

The Leeds City Region Enterprise Partnership (LEP) is a partnership between local

authorities and businesses whose aim is to “unlock the Leeds City Region’s vast

Leeds SHMA 2017 Page | 20

September 2017

economic potential by enabling businesses and enterprise to thrive”

5

. The Leeds City

Region is made up of ten local authority areas with Leeds City at the heart. This is

shown in Map 1.2.

The West Yorkshire Combined Authority (WYCA) is made up of the five metropolitan

districts of Leeds, Bradford, Calderdale, Kirklees and Wakefield.

The WYCA and the LEP are supported by an officer organisation that undertakes the

Boards’ policies and actions. The bodies have a joint vision for economic growth in the

Leeds City Region. As part of their strategic function, the WYCA and LEP have been

involved with a range of housing research, which forms the evidence base for housing

policy decisions at the strategic level. Relevant aspects of this strategic research will be

referenced in this SHMA for Leeds City.

Map 1.2 Leeds City Region and local authority context

5

http://www.the-lep.com/

Leeds SHMA 2017 Page | 21

September 2017

Data analysis and presentation

Data has been presented for the following 11 sub-areas within Leeds City, as illustrated

by Map 1.3:

• Aireborough,

• City Centre,

• East Leeds,

• Inner Area,

• North Leeds,

• Outer North East,

• Outer North West,

• Outer South,

• Outer South East,

• Outer South West, and

• Outer West.

Map 1.3 Leeds sub-areas

Leeds SHMA 2017 Page | 22

September 2017

Research methodology

Regarding the overall methodological approach to assessing housing need, PPG

(paragraph 5) states that, ‘there is no one methodology approach or use of a particular

dataset(s) that will provide a definitive assessment of development need. But the use of

this standard methodology set out in this guidance is strongly recommended because it

will ensure that the assessment findings are transparently prepared. Local planning

authorities may consider departing from the methodology, but they should explain why

their particular local circumstances have led them to adopt a different approach where

this is the case. The assessment should be thorough but proportionate, building where

possible on existing information sources outlined within the guidance’.

PPG (paragraph 14) comments that, ‘establishing future need for housing is not an exact

science. No single approach will provide a definitive answer. Plan makers should avoid

expending significant resources on primary research (information that is collected

through surveys, focus groups or interviews etc. and analysed to produce a new set of

findings) as this will in many cases be a disproportionate way of establishing an

evidence base. They should instead look to rely predominantly on secondary data (e.g.

Census, national surveys) to inform their assessment which are identified within the

guidance.’

To deliver the SHMA 2017, a multi-method approach has been adopted, comprising:

• A review of primary data obtained through a survey of 333,207 households across

the Leeds City Council area. The 2017 Household Survey involved a total of 27,867

households contacted and 5,383 questionnaires returned, representing a 19.3%

response rate overall. The number of questionnaires returned was well in excess of

the 1,500 specified in former Government guidance;

• A consideration of the findings of a stakeholder consultation and interviews with

estate and lettings agents;

• A review of relevant secondary data including the 2011 Census, house price data,

private rental data, Housing Association CORE lettings data, CLG Statistics and

Housing Register information;

• A consideration of research by Edge Analytics regarding Objectively Assessed

Housing Need (OAN); and

• Analysis of housing need and affordable housing requirements.

Further details of the research methodology are set out in Technical Appendix A.

Report structure

The Leeds SHMA 2017 report is structured as follows:

• Chapter 2 considers the definition of the Housing Market Area for Leeds;

• Chapter 3 provides a review of the current housing market;

• Chapter 4 looks at housing market signals;

• Chapter 5 considers the Objectively Assessed Housing Need;

Leeds SHMA 2017 Page | 23

September 2017

• Chapter 6 looks at the need for all types of housing and includes an analysis of

overall type/size mix, affordable housing need, overall tenure mix and the needs of

different groups; and

• Chapter 7 concludes the report with a summary of findings and a consideration of

strategic and policy issues.

The report includes technical appendices, which provide detailed material that

underpins the core outputs of the SHMA. The technical appendix material includes:

• Research methodology (Appendix A);

• Housing policy review (Appendix B);

• Affordable housing need calculations (Appendix C);

• Monitoring and updating (Appendix D); and

• Conformity to NPPF and PPG checklist (Appendix E).

Leeds SHMA 2017 Page | 24

September 2017

2. Defining the Housing Market Area

Introduction

PPG (paragraph 8) states that, ‘[housing] needs should be assessed in relation to the

relevant functional area i.e. Housing Market Area… Establishing the assessment area

may identify smaller sub-markets with specific features and it may be appropriate to

investigate these specifically in order to create a detailed picture of local need. It is also

important to recognise that there are 'market segments' i.e. not all housing types have

the same appeal to different occupants.’

PPG (paragraph 10) defines a Housing Market Area as, “a geographical area defined by

household demand and preferences for all types of housing, reflecting the key functional

linkages between places where people live and work. It might be the case that housing

market areas overlap”.

PPG (paragraph 11) suggests that Housing Market Areas can be broadly defined by

using three different sources of information as follows:

• House prices and rates of change in house prices;

• Household migration and search patterns; and

• Contextual data (for example travel to work area boundaries, retail and school

catchment areas).

In relation to migration and search patterns (the second bullet point, above), PPG

(paragraph 11) further comments that, “migration flows and housing search patterns

reflect preferences and the trade-offs made when choosing housing with different

characteristics. Analysis of migration flow patterns can help to identify these

relationships and the extent to which people move house within an area. The findings

can identify the areas within which a relatively high proportion of household moves

(typically 70 per cent) are contained. This excludes long distance moves (e.g. those due

to a change of lifestyle or retirement), reflecting the fact that most people move

relatively short distances due to connections to families, friends, jobs, and schools”.

In line with PPG, this SHMA reviews relevant data to establish the extent of the Leeds

Housing Market Area. Firstly, this chapter considers existing analysis on Housing Market

Areas, and then analyses house price, migration and commuting data.

Leeds strategic context

The Leeds City Region Housing Market Areas Study (July 2016) was undertaken for the

LEP and WYCA by the Centre for Urban and Regional Development Studies (CURDS) at

Newcastle University, in conjunction with Nathaniel Lichfield and Partners (NLP).

The core task for the study was to undertake new analyses defining housing market

areas (HMAs) with data from the 2011 Census, updating the National Housing and

Planning Advisory Unit (NHPAU) HMA definitions that CURDS had previously produced

using 2001 Census data.

Leeds SHMA 2017 Page | 25

September 2017

The study found that two Strategic HMAs cover West Yorkshire. Compared with the

previous NPHAU research:

• the Bradford Strategic HMA is now smaller;

• the Leeds Strategic HMA includes all of Calderdale, Kirklees and part of Wharfedale;

• the Leeds Strategic HMA has ‘lost’ the majority of Barnsley local authority area;

• the Leeds Strategic HMA has ‘gained’ Tadcaster and the northern part of Harrogate

local authority area to encompass Ripon.

The study found that there are only three Local HMAs within West Yorkshire and

findings relating to the Leeds Local HMA include:

• The previous NHPAU Leeds Local HMA north-south split is not replicated in the new

analysis;

• The Local Leeds HMA ‘gained’ parts of North Kirklees and Wharfedale from

Bradford;

• Leeds northern boundary with Harrogate is less permeable and Wetherby’s

allocation is volatile;

• Leeds:Bradford is a mostly impermeable boundary, but has ‘weakened’ in the

Wharfedale part of Bradford local authority area;

• Leeds:Wakefield is a mostly impermeable boundary, apart from in relation to the

wider strategic reach of Leeds.

House prices and rates of change in house prices

PPG (paragraph 11) states that,

‘Housing market areas can be identified by assessing patterns in the relationship

between housing demand and supply across different locations. This analysis uses house

prices to provide a ‘market-based’ reflection of housing market area boundaries. It

enables the identification of areas which have clearly different price levels compared to

surrounding areas. The findings provide information about differences across the area in

terms of the price people pay for similar housing, market ‘hotspots’, low demand areas

and volatility.’

Figure 2.1 shows how the median house price over the period 2000 to 2016 has

changed in Leeds, the region (Yorkshire and the Humber) and England.

Since 2000, the median house price in Leeds has increased 148.4% from £64,000 to

£159,000. The median price in Leeds has tracked below the national median, but has

been consistently higher than the regional median. As with England as a whole, the

fastest rate of median house price growth was experienced between 2000 (£64,000)

and 2007 (£146,428), followed by a period of fluctuation between 2008 and 2011.

House prices have risen since 2011, from £140,000 (2011) to £159,000 (2016).

Leeds SHMA 2017 Page | 26

September 2017

Figure 2.1 Median house price trends 2005 to 2016: Leeds, North Yorkshire and England

Source: Data produced by Land Registry © Crown copyright 2017

The lower quartile house price in Leeds has increased from £44,500 in 2000 to £110,000

during 2016, an increase of 147.2%.

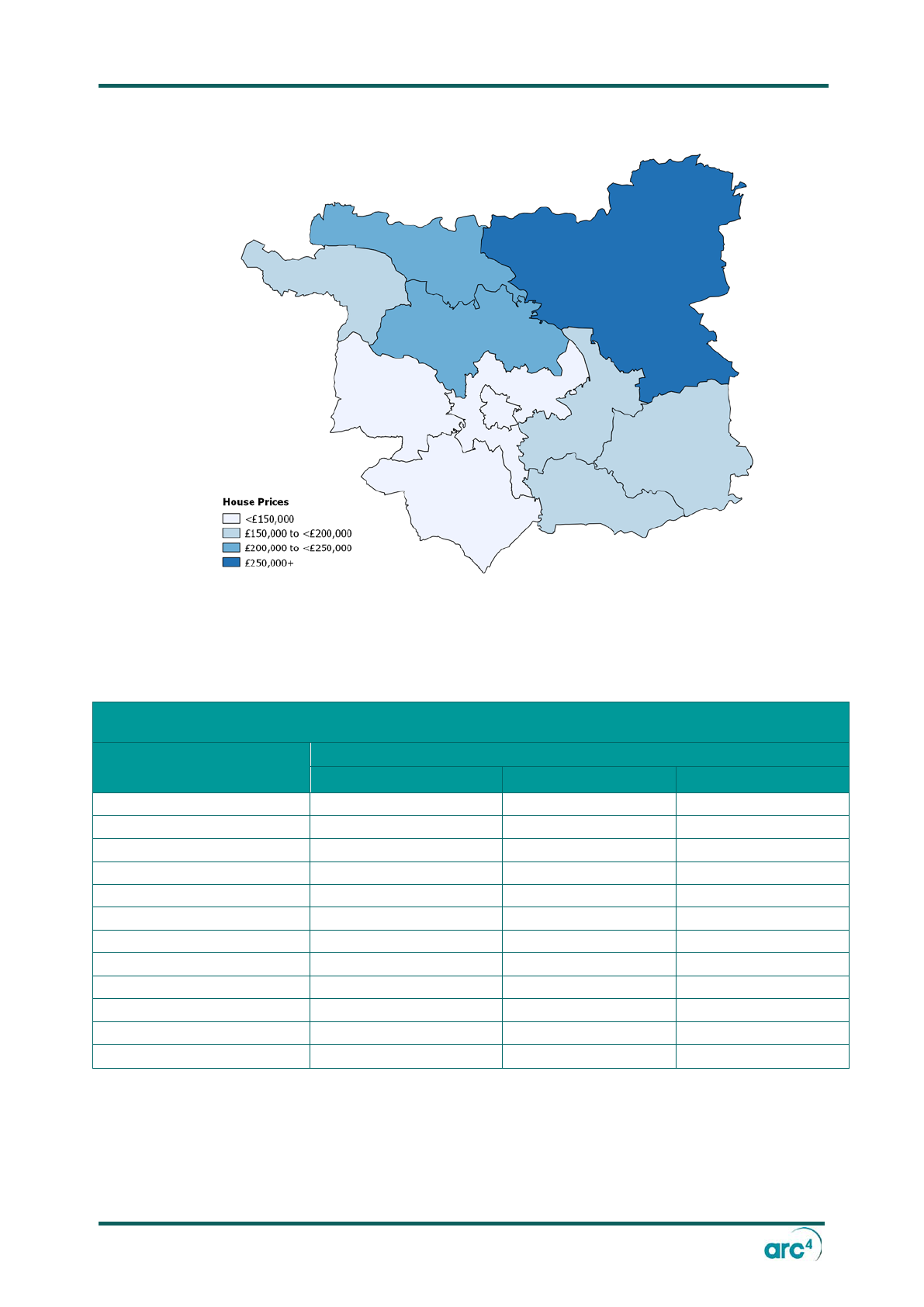

The distribution of house prices (2016) across the City of Leeds is illustrated by Map 2.3

and Table 2.1. Map 2.3 shows median house prices by sub-area and indicates relatively

lower prices in the Inner Area and higher prices in Outer North East, Outer North West

and North Leeds. Table 2.1 sets out lower quartile, median and upper quartile house

prices by sub-area and reflects this spatial pattern.

0

50,000

100,000

150,000

200,000

250,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Median House Price (£)

Yorkshire and Humber

England

Leeds

Leeds SHMA 2017 Page | 27

September 2017

Map 2.3 Median house prices 2015 by sub-area

Source: Data produced by Land Registry © Crown copyright 2017

Table 2.1 House prices in Leeds 2016 by sub-area

Sub-Area

Price (£)

Lower Quartile (25%)

Median (£)

Upper Quartile (£)

Aireborough

158,000

198,000

279,000

City Centre

103,000

135,750

179,000

East Leeds

125,000

160,000

210,000

Inner Area

73,000

96,000

135,000

North Leeds

152,375

211,250

287,350

Outer North East

207,000

298,250

434,525

Outer North West

170,100

242,250

334,998

Outer South

129,000

160,000

228,500

Outer South East

127,000

160,000

189,995

Outer South West

98,000

134,000

180,000

Outer West

104,000

135,000

175,000

Leeds Total

112,500

159,000

230,000

Source: Data produced by Land Registry © Crown copyright 2017

Leeds SHMA 2017 Page | 28

September 2017

Table 2.2 considers how Leeds median prices and change over the period 2000-2016

compare with neighbouring areas, the region and England. This analysis demonstrates

that the median price increase in Leeds has been lower than most neighbouring local

authority areas and the Yorkshire and the Humber region. However, percentage change

has been greater than that for England as a whole.

Table 2.2 House prices and price change in neighbouring areas, Yorkshire and the Humber

and England

Location

Year

% change 2000-2016

2000

2016

York

£75,500

£215,000

184.8

Harrogate

£90,500

£255,000

181.8

Craven

£69,950

£189,475

170.9

Calderdale

£48,000

£130,000

170.8

Selby

£65,000

£175,000

169.2

Yorkshire and Humber

£56,000

£145,000

158.9

Kirklees

£53,000

£135,000

154.7

Bradford

£49,500

£125,000

152.5

Barnsley

£44,000

£110,000

150.0

Leeds

£64,000

£159,000

148.4

England

£82,000

£202,000

146.3

Wakefield

£53,500

£131,500

145.8

Source: Data produced by Land Registry © Crown copyright 2017

Migration and self-containment

In relation to migration, PPG (paragraph 11) states:

‘Migration flows and housing search patterns reflect preferences and the trade-offs

made when choosing housing with different characteristics. Analysis of migration flow

patterns can help to identify these relationships and the extent to which people move

house within an area. The findings can identify the areas within which a relatively high

proportion of household moves (typically 70 per cent) are contained. This excludes long

distance moves (e.g. those due to a change of lifestyle or retirement), reflecting the fact

that most people move relatively short distances due to connections to families, friends,

jobs, and schools.’

That said, previous CLG guidance recognised that ‘rural areas typically have less locally

self-contained migration patterns, reflecting the influence of long-distance movers who

are opting for lifestyle change or retirement.’

6

Data reported in the 2011 Census provides evidence from which the degree of self-

containment of Leeds can be derived. PAS guidance recommends that migration data

are tested against the PPG criterion for self-containment, that at least 70% of all

6

DC Advice Note: Identifying sub-regional housing market areas 2007

Leeds SHMA 2017 Page | 29

September 2017

migration excluding long-distance migration should be contained within the HMA. A

suitable test are two migration containment ratios:

• Supply side (origin): moves within the area divided by all moves whose origin is in

the area, excluding long-distance moves; and

• Demand side (destination): moves within the area divided by all moves whose

destination is in the area, excluding long-distance migration.

Table 2.3 presents the relevant migration data for Leeds. This illustrates that 69.2% of

all residents moving in the year preceding the Census originated from within Leeds. Of

the total 108,802 moving residents, 69.2% originated in Leeds, 2.6% from Bradford,

1.5% from Wakefield, 1.4% from Kirklees, 5.8% from elsewhere in Yorkshire and the

Humber, 5.0% from the North West and 14.6% from elsewhere in the UK. Excluding

long-distance moves and only analysing the 87,542 movements from within Yorkshire

and the Humber, 85.9% originated within Leeds, 3.2% from Bradford, 1.9% from

Wakefield, 1.7% from Kirklees and 7.1% from elsewhere in the region.

Table 2.4 summarises the containment ratios that apply to the origin and destination of

moving residents. In line with PPG guidance, this excludes long-distance migration

(which in this case is taken as moves from outside Yorkshire and the Humber). Based on

these criteria, the origin containment ratio is 85.95% and the destination is 85.92%. This

indicates a high level of self-containment in terms of population migration.

Table 2.3 Flows of residents (all moves)

Origin/

Destination

Supply Side (Origin)

Demand Side (Destination)

All Moves

Excluding

Long

Distance

Moves

All Moves

Excluding

Long

Distance

Moves

Number

%

%

Number

%

%

Leeds

75,242

69.2

85.9

75,242

71.8

85.9

Bradford

2,831

2.6

3.2

2,563

2.4

2.9

Wakefield

1,672

1.5

1.9

1,773

1.7

2.0

Kirklees

1,522

1.4

1.7

1,825

1.7

2.1

Harrogate

823

0.8

0.9

1,097

1.0

1.3

Sheffield

809

0.7

0.9

761

0.7

0.9

East Riding of Yorkshire

664

0.6

0.8

609

0.6

0.7

York

653

0.6

0.7

727

0.7

0.8

Elsewhere Y&H

3,326

3.1

3.8

2,976

2.8

3.4

North West

5,388

5.0

3,739

3.6

London

2,570

2.4

3,669

3.5

East Midlands

2,605

2.4

1,731

1.7

Elsewhere UK

10,697

9.8

8,066

7.7

Total

108,802

100.0

100.0

104,778

100.0

100.0

Base (excluding long-distance moves)

87,542

87,573

Source: 2011 Census

Leeds SHMA 2017 Page | 30

September 2017

Table 2.4 Containment ratios

Origin

Moves within the area

All moves originating in the

area

Containment

Ratio

75,242 87,542 85.95%

Destination

Moves within the area

All moves whose

destination is in the area

Containment

Ratio

75,242 87,573 85.92%

Source: 2011 Census

Commuting patterns

The 2011 Census provides an analysis of travel to work patterns and the extent to which

residents in Leeds travel to other areas, together with details of how many people

commute into the City area. Table 2.5 presents this data and indicates that 83.1% of

people who live in Leeds work in the City; by comparison, 68.9% of workers in Leeds live

in the City. This indicates a clear net inward movement of workers and illustrates the

strength of Leeds as an economic centre within the region.

Table 2.5 Leeds 2011 Census commuting flows: workers (aged 16-74 years)

Where do people who live in Leeds work?

Live

Work

Number

%

Leeds

Leeds

266,323

83.1

Bradford

16,957

5.3

Wakefield

12,682

4.0

Kirklees

6,950

2.2

Other

17,565

5.4

Workers

320,477

100.0

Where to people who work in Leeds live?

Live

Work

Number

%

Leeds

Leeds

236,326

68.9

Bradford

27,508

8.0

Wakefield

21,568

6.3

Kirklees

19,725

5.7

Other

38,147

11.1

Jobs

343,274

100.0

Source 2011 Census

In terms of defining market areas, PPG does not suggest an appropriate self-

containment figure. However, the ONS provides a definition of Travel to Work areas as

follows:

‘The current criterion for defining TTWs is that generally at least 75% of an area’s

resident workforce in the area and at least 75% of the people who work in the area also

Leeds SHMA 2017 Page | 31

September 2017

live in the area…however, for areas with a working population in excess of 25,000, self-

containment rates as low as 66.7% are accepted’

7

On this basis, it is concluded that Leeds can be considered to be highly self-contained in

terms of the travel-to-work patterns of its own resident working population; however,

it has a wider economic function within the City Region which draws a significant

number of commuters into the City administrative area.

Concluding comments

The purpose of this chapter has been to consider the general housing market context of

Leeds and its inter-relationships with other areas. This reflects the requirements of PPG

(paragraph 11). By reviewing house prices, migration and travel to work patterns, the

extent to which Leeds is a self-contained Housing Market Area can be determined. PPG

establishes that areas within which a relatively high proportion of household moves

(typically 70%) are contained can be defined as a self-contained Housing Market Area.

Leeds’s Housing Market Area exhibits a degree of distinctiveness compared with

neighbouring areas as measured by median price change 2000-2016 at a lower rate

than most neighbouring local authority areas and the Yorkshire and the Humber region

as a whole. Percentage growth has been slightly greater than that for England as a

whole.

Regarding migration, analysis of the 2011 Census data identifies containment ratios of

85.95% (origin) and 85.92% (destination). From a migration perspective, Leeds is

therefore considered to be self-contained.

Regarding travel to work, 83.1% of employees living in Leeds also work Leeds, indicating

low levels of out-commuting to work elsewhere. However, there is a higher amount of

in-commuting, with 68.9% of Leeds’ workforce living in the City administrative area,

while 8.0% travel in from Bradford, 6.3% from Wakefield and 5.7% from Kirklees. From

a travel-to-work perspective it is therefore concluded that Leeds is self-contained in

terms of its own working population but has a significant economic function that also

draws commuters from the wider City Region.

Interactions with several neighbouring areas are recognised, as also highlighted in the

Leeds City Region research that has been undertaken at the strategic level to update

the NHPAU research (using 2011 Census information). This research particularly

identifies relationships with the northern part of Kirklees and with the Wharfedale part

of Bradford. These local authorities recognise that they operate as a wider functional

area from an economic perspective, but they do not consider Leeds as part of their

respective Housing Market Areas for the purposes of local planning policy.

In conclusion, although there are interactions with other areas, Leeds should be

recognised as an appropriate Housing Market Area for the purposes of local planning

policy.

7

https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/articles/commutingtoworkchangestot

raveltoworkareas/2001to2011

Leeds SHMA 2017 Page | 32

September 2017

3. Leeds housing market review

Introduction

The purpose of this chapter is to explore the housing market dynamics of Leeds. This

includes a review of the current stock profile along with an analysis of the tenure

characteristics. It also considers the key housing market drivers, a consideration of

housing need and the affordability of different tenure options.

Property profile

This study assumes a total of 337,302 households

8

and 347,787 dwellings in Leeds City.

With 8,578 vacant homes (of which 2,681 are long term vacant) and 2,038 are second

homes

9

. The overall vacancy rate is around 2.5%, this compares with a vacancy rate of

2.6% across England

10

. Data by sub-area is set out in Table 3.1.

Table 3.1 Dwelling stock and occupancy by sub-area

Sub-area

Total Dwellings

Second Homes

Total Vacant

(empty/

unoccupied)

Vacant %

Aireborough

15,495

91

382

4.5

City Centre

11,676

68

288

3.4

East Leeds

19,956

117

492

5.7

Inner Area

75,264

441

1,856

21.6

North Leeds

74,155

435

1,829

21.3

Outer North East

17,725

104

437

5.1

Outer North West

9,671

57

239

2.8

Outer South

12,914

76

319

3.7

Outer South East

16,700

98

412

4.8

Outer South West

43,456

255

1,072

12.5

Outer West

50,775

298

1,252

14.6

Leeds Total

347,787

2,038

8,578

2.5

Source: 2017 household survey data and 2015/2016 Council Tax data

Property size and type

Table 3.2 reviews the profile of occupied dwelling stock by size and type across Leeds.

Overall, the vast majority (70.4%) of properties are houses, 22.6% are flats/apartments

and maisonettes, 6.4% are bungalows, and 0.6% are other types of property including

park homes/caravans. Of all occupied properties, 14.9% have one bedroom/bedsit,

8

Household survey 2017

9

Council Tax 2015/2016

10

2015 CLG Dwelling and Vacancy data

Leeds SHMA 2017 Page | 33

September 2017

28.6% have two bedrooms, 38.2% have three bedrooms and 18.3% have four or more