5

10

15

20

25

1

2

3

4

6

7

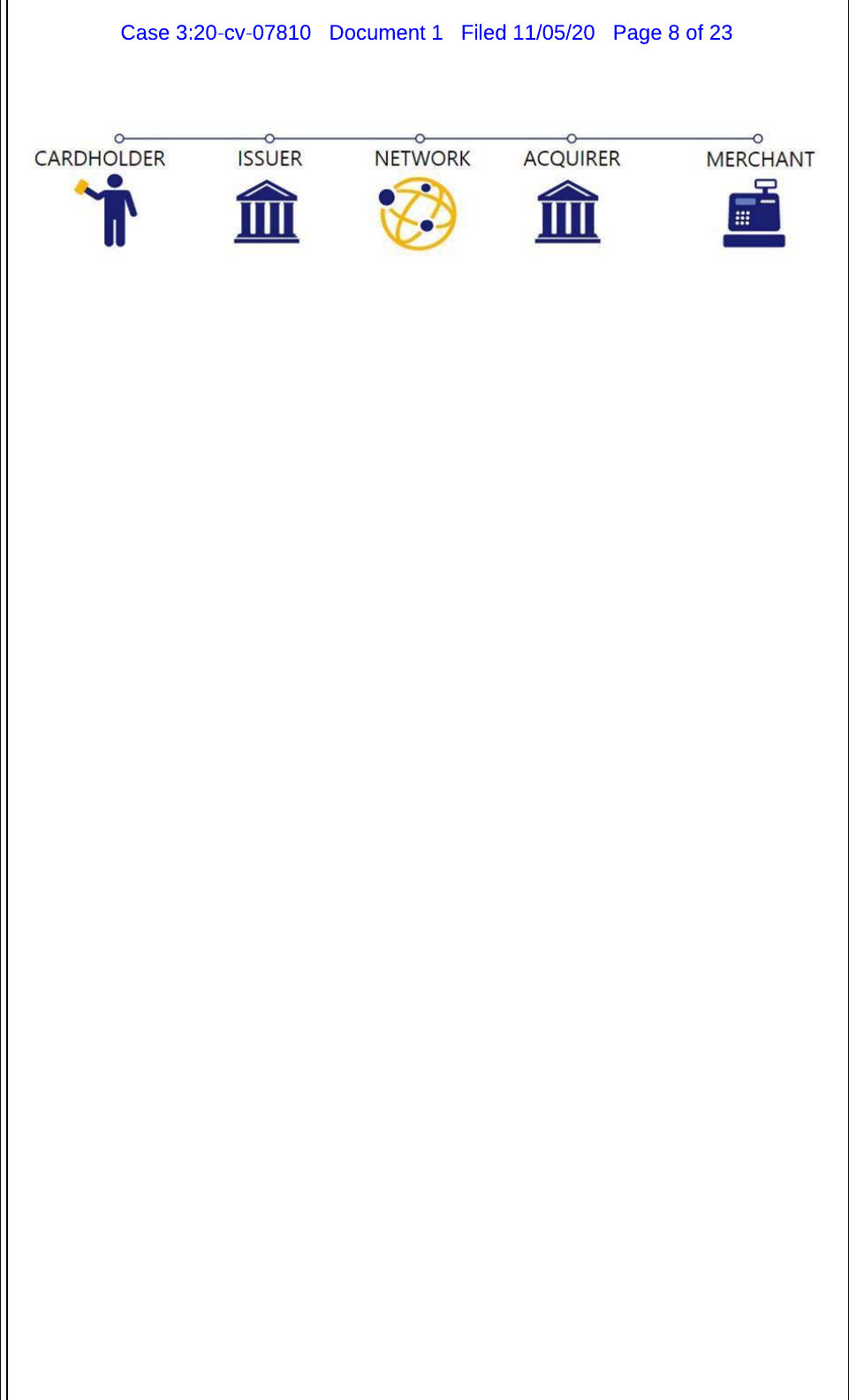

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

J

OHN

R

.

R

EAD (D

C B

ar #419373)

M

EAGAN K.

B

ELL

S

HAW (

C

A

B

ar #257875)

C

O

R

Y

BR

ADE

R

LEU

C

HTEN (NY

B

ar # 5118732)

S

A

R

AH H. LI

C

HT (D

C B

ar #1021541)

Un

it

ed

St

a

t

e

s

Depar

tm

en

t

of

J

u

sti

ce, An

tit

ru

st

D

i

v

isi

on

450

Fi

f

t

h

St

ree

t

, NW,

S

u

it

e 4000

Wa

s

h

i

ng

t

on, D

C

20530

Te

l

ephone

:

(202) 307-0468

F

ac

simil

e

:

(202) 514-7308

E-

m

a

il: j

ohn.read@u

s

do

j

.gov

[Add

iti

ona

l

coun

s

e

l list

ed on

si

gna

t

ure page]

A

tt

orney

s

for

Pl

a

i

n

ti

ff Un

it

ed

St

a

t

e

s

of A

m

er

i

ca

UN

I

TE

D

ST

A

TES

D

IST

R

I

C

T

C

O

UR

T

N

O

R

THE

RN D

IST

R

I

C

T O

F CA

LI

F

O

RN

I

A

S

AN FRANC

IS

C

O

D

I

V

ISIO

N

UNITED

S

TATE

S

O

F

A

M

E

R

I

C

A,

P

l

a

i

n

tiff

v.

C

a

s

e No.

:

C

O

MP

L

A

I

N

T

VI

S

A IN

C

. and

P

LAID IN

C

.,

De

f

endan

t

s

.

V

is

a

s

eek

s t

o buy

Pl

a

i

d – a

s its C

EO

s

a

i

d – a

s

an “

i

n

s

urance po

li

cy”

t

o neu

t

ra

li

ze a

“

t

hrea

t t

o our

im

por

t

an

t

U

S

deb

it

bu

si

ne

ss

.” V

is

a

is

a

m

onopo

list i

n on

li

ne deb

it t

ran

s

ac

ti

on

s

,

ex

t

rac

ti

ng b

illi

on

s

of do

ll

ar

s i

n fee

s

annua

ll

y fro

m m

erchan

ts

and con

s

u

m

er

s

.

Pl

a

i

d, a f

i

nanc

i

a

l

t

echno

l

ogy f

i

r

m

w

it

h acce

ss t

o

im

por

t

an

t

f

i

nanc

i

a

l

da

t

a fro

m

over 11,000 U.

S

. bank

s

,

is

a

t

hrea

t

t

o

t

h

is m

onopo

l

y

: it

ha

s

been deve

l

op

i

ng an

i

nnova

ti

ve new

s

o

l

u

ti

on

t

ha

t

wou

l

d be a

s

ub

stit

u

t

e

for V

is

a’

s

on

li

ne deb

it s

erv

i

ce

s

.

B

y acqu

i

r

i

ng

Pl

a

i

d, V

is

a wou

l

d e

limi

na

t

e a na

s

cen

t

co

m

pe

titi

ve

t

hrea

t t

ha

t

wou

l

d

li

ke

l

y re

s

u

lt i

n

s

ub

st

an

ti

a

l s

av

i

ng

s

and

m

ore

i

nnova

ti

ve on

li

ne deb

it s

erv

i

ce

s

for

-1-

C

O

M

P

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

m

erchan

ts

and con

s

u

m

er

s

.

F

or

t

he rea

s

on

s

d

is

cu

ss

ed be

l

ow,

t

he propo

s

ed acqu

isiti

on v

i

o

l

a

t

e

s

S

ec

ti

on 2 of

t

he

S

her

m

an Ac

t

, 15 U.

S

.

C

. § 2, and

S

ec

ti

on 7 of

t

he

Cl

ay

t

on Ac

t

, 15 U.

S

.

C

. § 18,

and

m

u

st

be

st

opped.

I

N

T

R

O

DUC

TIO

N

1. V

is

a

is

“everywhere you wan

t t

o be.”

1

I

ts

deb

it

card

s

are accep

t

ed by

t

he va

st

m

a

j

or

it

y of U.

S

.

m

erchan

ts

, and

it

con

t

ro

ls

approx

im

a

t

e

l

y 70% of

t

he on

li

ne deb

it t

ran

s

ac

ti

on

s

m

arke

t

. In 2019,

t

here were rough

l

y 500

milli

on V

is

a deb

it

card

s i

n c

i

rcu

l

a

ti

on

i

n

t

he Un

it

ed

St

a

t

e

s

. Tha

t s

a

m

e year, V

is

a proce

ss

ed approx

im

a

t

e

l

y 43 b

illi

on deb

it t

ran

s

ac

ti

on

s

,

i

nc

l

ud

i

ng

m

ore

t

han 10 b

illi

on on

li

ne

t

ran

s

ac

ti

on

s

. In 2019, V

is

a earned over $4 b

illi

on fro

m its

deb

it

bu

si

ne

ss

,

i

nc

l

ud

i

ng approx

im

a

t

e

l

y $2 b

illi

on fro

m

on

li

ne deb

it

.

2. A

m

er

i

can con

s

u

m

er

s i

ncrea

si

ng

l

y

m

ake purcha

s

e

s

on

li

ne, a

tt

rac

t

ed by

t

he

conven

i

ence of be

i

ng ab

l

e

t

o

s

hop any

tim

e, fro

m

anywhere, w

it

h fa

st

de

li

very. In recen

t

year

s

,

on

li

ne

t

ran

s

ac

ti

on

s

have exper

i

enced “exp

l

o

si

ve” grow

t

h, a

t

rend

t

ha

t

ha

s

on

l

y been acce

l

era

t

ed

by

t

he

C

OVID-19 pande

mi

c, w

it

h on

li

ne

s

a

l

e

s

grow

i

ng

m

ore

t

han 30% be

t

ween

t

he f

i

r

st

and

s

econd quar

t

er

s

of 2020.

3. A

m

er

i

can con

s

u

m

er

s

u

s

e deb

it

card

s t

o purcha

s

e hundred

s

of b

illi

on

s

of do

ll

ar

s

of

good

s

and

s

erv

i

ce

s

on

t

he

i

n

t

erne

t

each year.

M

any con

s

u

m

er

s

buy

i

ng good

s

and

s

erv

i

ce

s

on

li

ne

e

it

her prefer u

si

ng deb

it

or canno

t

acce

ss

o

t

her

m

ean

s

of pay

m

en

t

,

s

uch a

s

cred

it

.

B

ecau

s

e of

its

ub

i

qu

it

y a

m

ong con

s

u

m

er

s

,

m

erchan

ts

have no cho

i

ce bu

t t

o accep

t

V

is

a deb

it

de

s

p

it

e perenn

i

a

l

co

m

p

l

a

i

n

ts

abou

t t

he h

i

gh co

st

of V

is

a’

s

deb

it s

erv

i

ce.

4. V

is

a’

s m

onopo

l

y power

i

n on

li

ne deb

it is

pro

t

ec

t

ed by

si

gn

i

f

i

can

t

barr

i

er

s t

o en

t

ry

and expan

si

on. V

is

a connec

ts milli

on

s

of

m

erchan

ts t

o hundred

s

of

milli

on

s

of con

s

u

m

er

s i

n

t

he

Un

it

ed

St

a

t

e

s

. New cha

ll

enger

s t

o V

is

a’

s m

onopo

l

y wou

l

d

t

hu

s

face a ch

i

cken-and-egg

quandary, need

i

ng connec

ti

on

s

w

it

h

milli

on

s

of con

s

u

m

er

s t

o a

tt

rac

t t

hou

s

and

s

of

m

erchan

ts

and

need

i

ng

t

hou

s

and

s

of

m

erchan

ts t

o a

tt

rac

t milli

on

s

of con

s

u

m

er

s

. V

is

a’

s C

h

i

ef

Fi

nanc

i

a

l

Off

i

cer

ha

s

acknow

l

edged

t

ha

t

bu

il

d

i

ng an ex

t

en

si

ve ne

t

work

li

ke V

is

a’

s is

“very, very hard

t

o do” and

1

h

tt

p

s://

u

s

a.v

is

a.co

m/

.

-2-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

“

t

ake

s m

any year

s

of

i

nve

stm

en

t

,” bu

t

“[

i

]f you can do

t

ha

t

,

t

hen you can have a bu

si

ne

ss

[

li

ke

V

is

a’

s

]

t

ha

t

ha

s

a re

l

a

ti

ve

l

y h

i

gh

m

arg

i

n.” He exp

l

a

i

ned

t

ha

t

en

t

ry barr

i

er

s

are

s

o

si

gn

i

f

i

can

t t

ha

t

even we

ll

-funded co

m

pan

i

e

s

w

it

h

st

rong brand na

m

e

s st

rugg

l

e

t

o en

t

er on

li

ne deb

it

.

5.

M

a

st

ercard, V

is

a’

s

on

l

y

l

ong

st

and

i

ng r

i

va

l i

n on

li

ne deb

it s

erv

i

ce

s

, ha

s

a

m

uch

sm

a

ll

er

m

arke

t s

hare of around 25%.

F

or year

s

,

M

a

st

ercard ha

s

ne

it

her ga

i

ned

si

gn

i

f

i

can

t s

hare

fro

m

V

is

a nor re

st

ra

i

ned V

is

a’

s m

onopo

l

y.

M

a

st

ercard’

s

par

ti

c

i

pa

ti

on

i

n

t

he on

li

ne deb

it m

arke

t

ha

s

no

t t

ran

sl

a

t

ed

i

n

t

o

l

ower pr

i

ce

s

for con

s

u

m

er

s

, and

t

h

is

appear

s

un

li

ke

l

y

t

o change.

F

or

exa

m

p

l

e, V

is

a ha

s l

ong-

t

er

m

con

t

rac

ts

w

it

h

m

any of

t

he na

ti

on’

s l

arge

st

bank

s t

ha

t

re

st

r

i

c

t t

he

s

e

bank

s

’ ab

ilit

y

t

o

iss

ue

M

a

st

ercard deb

it

card

s

. V

is

a a

ls

o ha

s

ha

mst

rung

sm

a

ll

er r

i

va

ls

by e

it

her

erec

ti

ng

t

echn

i

ca

l

barr

i

er

s

, or en

t

er

i

ng

i

n

t

o re

st

r

i

c

ti

ve agree

m

en

ts t

ha

t

preven

t

r

i

va

ls

fro

m

grow

i

ng

t

he

i

r

s

hare

i

n on

li

ne deb

it

, or bo

t

h.

6. The

s

e en

t

ry barr

i

er

s

, coup

l

ed w

it

h V

is

a’

s l

ong-

t

er

m

, re

st

r

i

c

ti

ve con

t

rac

ts

w

it

h

bank

s

, are near

l

y

i

n

s

ur

m

oun

t

ab

l

e,

m

ean

i

ng V

is

a rare

l

y face

s

any

si

gn

i

f

i

can

t t

hrea

ts t

o

its

on

li

ne

deb

it m

onopo

l

y.

Pl

a

i

d

is s

uch a

t

hrea

t

.

7.

Pl

a

i

d

is

un

i

que

l

y po

siti

oned

t

o

s

ur

m

oun

t t

he

s

e en

t

ry barr

i

er

s

and under

mi

ne

V

is

a’

s m

onopo

l

y

i

n on

li

ne deb

it s

erv

i

ce

s

.

Pl

a

i

d power

s s

o

m

e of

t

oday’

s m

o

st i

nnova

ti

ve

f

i

nanc

i

a

l t

echno

l

ogy (“f

i

n

t

ech”) app

s

,

s

uch a

s

Ven

m

o, Acorn

s

, and

B

e

tt

er

m

en

t

.

Pl

a

i

d’

s

t

echno

l

ogy a

ll

ow

s

f

i

n

t

ech

s t

o p

l

ug

i

n

t

o con

s

u

m

er

s

’ var

i

ou

s

f

i

nanc

i

a

l

accoun

ts

, w

it

h con

s

u

m

er

per

missi

on,

t

o aggrega

t

e

s

pend

i

ng da

t

a,

l

ook up ba

l

ance

s

, and ver

i

fy o

t

her per

s

ona

l

f

i

nanc

i

a

l

i

nfor

m

a

ti

on.

Pl

a

i

d ha

s

a

l

ready bu

ilt

connec

ti

on

s t

o 11,000 U.

S

. f

i

nanc

i

a

l i

n

stit

u

ti

on

s

and

m

ore

t

han 200

milli

on con

s

u

m

er bank accoun

ts i

n

t

he Un

it

ed

St

a

t

e

s

and grow

i

ng. The

s

e e

st

ab

lis

hed

connec

ti

on

s

po

siti

on

Pl

a

i

d

t

o overco

m

e

t

he en

t

ry barr

i

er

s t

ha

t

o

t

her

s

face

i

n a

tt

e

m

p

ti

ng

t

o

prov

i

de on

li

ne deb

it s

erv

i

ce

s

.

8. Wh

il

e

Pl

a

i

d’

s

ex

isti

ng

t

echno

l

ogy doe

s

no

t

co

m

pe

t

e d

i

rec

tl

y w

it

h V

is

a

t

oday,

Pl

a

i

d

is

p

l

ann

i

ng

t

o

l

everage

t

ha

t t

echno

l

ogy, co

m

b

i

ned w

it

h

its

ex

isti

ng re

l

a

ti

on

s

h

i

p

s

w

it

h bank

s

and con

s

u

m

er

s

,

t

o fac

ilit

a

t

e

t

ran

s

ac

ti

on

s

be

t

ween con

s

u

m

er

s

and

m

erchan

ts i

n co

m

pe

titi

on w

it

h

V

is

a. L

i

ke V

is

a’

s

on

li

ne deb

it s

erv

i

ce

s

,

Pl

a

i

d’

s

new deb

it s

erv

i

ce wou

l

d enab

l

e con

s

u

m

er

s t

o

pay for good

s

and

s

erv

i

ce

s

on

li

ne w

it

h

m

oney deb

it

ed fro

m t

he

i

r bank accoun

ts

. W

it

h

t

h

is

new

-3-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

on

line debit

service, Plaid intended to “steal[] share” and become a “formidable competitor to

Visa and

Mastercard.”

Competition from Plaid likely would drive down prices for online debit

transactions, chipping away at Visa’s monopoly and resulting in substantial savings to merchants

and consumers.

9. Visa feared that Plaid’s innovative potential – on its own or in partnership with

another company – would threaten Visa’s debit business. In evaluating whether to consider

Plaid as a potential acquisition target in March 2019, Visa’s Vice President of Corporate

Development and Head of Strategic Opportunities expressed concerns to his colleagues about the

threat Plaid posed to Visa’s established debit business, observing: “I don’t want to be IBM to

their Microsoft.” This executive analogized Plaid to an island “volcano” whose current

capabilities are just “the tip showing above the water” and warned that “[w]hat lies beneath,

though, is a massive opportunity – one that threatens Visa.” He underscored his point by

illustrating Plaid’s disruptive potential:

10. Several months later, Visa had the opportunity to acquire Plaid. While

conducting extensive due diligence, Visa’s senior executives became alarmed to learn about

Plaid’s plans to add a “meaningful money movement business by the end of 2021” that would

compete with Visa’s online debit services. This prompted Visa’s CEO to conclude that Plaid

was “clearly, on their own or owned by a competitor going to create some threat to our important

-4-

CO

M

PLAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

U

S

deb

it

bu

si

ne

ss

” and

t

o

t

e

ll

h

is CF

O

t

ha

t

purcha

si

ng

Pl

a

i

d wou

l

d be an “

i

n

s

urance po

li

cy

t

o

pro

t

ec

t

our deb

it

b

i

z

i

n

t

he U

S

.”

11. In

m

ak

i

ng

t

he ca

s

e

t

o buy

Pl

a

i

d

t

o V

is

a’

s B

oard of D

i

rec

t

or

s

, V

is

a’

s s

en

i

or

l

eader

s

h

i

p e

stim

a

t

ed a “po

t

en

ti

a

l

down

si

de r

is

k of $300-500

M i

n our U

S

deb

it

bu

si

ne

ss

” by 2024

s

hou

l

d

Pl

a

i

d fa

ll i

n

t

o

t

he hand

s

of a r

i

va

l

. V

is

a under

st

ood

t

ha

t

cou

l

d crea

t

e an “[e]x

ist

en

ti

a

l

r

is

k

t

o our U.

S

. deb

it

bu

si

ne

ss

” and

t

ha

t

“V

is

a

m

ay be forced

t

o accep

t l

ower

m

arg

i

n

s

or no

t

have a

co

m

pe

titi

ve offer

i

ng.”

12. On

J

anuary 13, 2020, V

is

a agreed

t

o acqu

i

re

Pl

a

i

d

i

n par

t t

o e

limi

na

t

e

t

h

is

ex

ist

en

ti

a

l

r

is

k and pro

t

ec

t its m

onopo

l

y

i

n on

li

ne deb

it

. V

is

a offered approx

im

a

t

e

l

y $5.3 b

illi

on

for

Pl

a

i

d, “an unpreceden

t

ed revenue

m

u

lti

p

l

e of over 50X” and

t

he

s

econd-

l

arge

st

acqu

isiti

on

i

n

V

is

a’

s

h

ist

ory.

R

ecogn

i

z

i

ng

t

ha

t t

he dea

l

“doe

s

no

t

hun

t

on f

i

nanc

i

a

l

ground

s

,” V

is

a’

s C

EO

j

u

sti

f

i

ed

t

he ex

t

raord

i

nary purcha

s

e pr

i

ce for

Pl

a

i

d a

s

a “

st

ra

t

eg

i

c, no

t

f

i

nanc

i

a

l

”

m

ove becau

s

e

“[o]ur U

S

deb

it

bu

si

ne

ss i

[

s

] cr

iti

ca

l

and we

m

u

st

a

l

way

s

do wha

t it t

ake

s t

o pro

t

ec

t t

h

is

bu

si

ne

ss

.”

13.

M

onopo

lists

canno

t

have “free re

i

gn

t

o

s

qua

s

h na

s

cen

t

, a

l

be

it

unproven,

co

m

pe

tit

or

s

a

t

w

ill

.” Un

it

ed S

t

a

t

e

s

v. M

i

c

r

o

s

o

ft

C

o

r

p., 253

F

.3d 34, 79 (D.

C

.

Ci

r. 2001).

Acqu

i

r

i

ng

Pl

a

i

d wou

l

d e

limi

na

t

e

t

he na

s

cen

t

bu

t si

gn

i

f

i

can

t

co

m

pe

titi

ve

t

hrea

t Pl

a

i

d po

s

e

s

,

fur

t

her en

t

rench

i

ng V

is

a’

s m

onopo

l

y

i

n on

li

ne deb

it

. A

s

a re

s

u

lt

, bo

t

h

m

erchan

ts

and con

s

u

m

er

s

wou

l

d be depr

i

ved of co

m

pe

titi

on

t

ha

t

wou

l

d dra

sti

ca

ll

y

l

ower co

sts

for on

li

ne deb

it t

ran

s

ac

ti

on

s

,

l

eav

i

ng

t

he

m

w

it

h few a

lt

erna

ti

ve

s t

o V

is

a’

s m

onopo

l

y pr

i

ce

s

. Thu

s

,

t

he acqu

isiti

on wou

l

d

un

l

awfu

ll

y

m

a

i

n

t

a

i

n V

is

a’

s m

onopo

l

y

i

n v

i

o

l

a

ti

on of

S

ec

ti

on 2 of

t

he

S

her

m

an Ac

t

.

14. V

is

a’

s

propo

s

ed acqu

isiti

on a

ls

o wou

l

d v

i

o

l

a

t

e

S

ec

ti

on 7 of

t

he

Cl

ay

t

on Ac

t

,

wh

i

ch wa

s

“de

si

gned

t

o arre

st t

he crea

ti

on of

m

onopo

li

e

s

‘

i

n

t

he

i

r

i

nc

i

p

i

ency,’” Un

it

ed S

t

a

t

e

s

v.

Gen. Dynam

i

c

s C

o

r

p., 415 U.

S

. 486, 505 n.13 (1974), and

simil

ar

l

y proh

i

b

its

a

m

onopo

list

fro

m

bo

lst

er

i

ng

its m

onopo

l

y

t

hrough an acqu

isiti

on

t

ha

t

e

limi

na

t

e

s

a na

s

cen

t

bu

t si

gn

i

f

i

can

t

co

m

pe

titi

ve

t

hrea

t

. The

S

upre

m

e

C

our

t

ha

s

exp

l

a

i

ned

t

ha

t

an acqu

isiti

on can v

i

o

l

a

t

e

S

ec

ti

on 7

when “

t

he re

l

a

ti

ve

si

ze of

t

he acqu

i

r

i

ng corpora

ti

on ha[

s

]

i

ncrea

s

ed

t

o

s

uch a po

i

n

t t

ha

t its

advan

t

age over

its

co

m

pe

tit

or

s t

hrea

t

en[

s

]

t

o be ‘dec

isi

ve.’” B

r

o

w

n Shoe

C

o. v. Un

it

ed S

t

a

t

e

s

,

-5-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

370 U.

S

. 294, 321 n.36 (1962). V

is

a a

l

ready ha

s

a dec

isi

ve

m

arke

t

po

siti

on

t

hrough

its

on

li

ne

deb

it m

onopo

l

y, and wou

l

d un

l

awfu

ll

y ex

t

end

t

ha

t

advan

t

age by acqu

i

r

i

ng

Pl

a

i

d.

F

or

t

he rea

s

on

s

s

e

t

for

t

h

i

n

t

h

is C

o

m

p

l

a

i

n

t

,

t

he propo

s

ed acqu

isiti

on

m

u

st

be en

j

o

i

ned.

JUR

IS

D

I

C

TIO

N

15. The Un

it

ed

St

a

t

e

s

br

i

ng

s t

h

is

ac

ti

on under

S

ec

ti

on 15 of

t

he

Cl

ay

t

on Ac

t

, a

s

a

m

ended, 15 U.

S

.

C

§ 25, and

S

ec

ti

on 4 of

t

he

S

her

m

an Ac

t

, 15 U.

S

.

C

. § 4,

t

o preven

t

and

re

st

ra

i

n V

is

a fro

m

v

i

o

l

a

ti

ng

S

ec

ti

on 2 of

t

he

S

her

m

an Ac

t

, 15 U.

S

.

C

. § 2, and Defendan

ts

fro

m

v

i

o

l

a

ti

ng

S

ec

ti

on 7 of

t

he

Cl

ay

t

on Ac

t

, 15 U.

S

.

C

. § 18. Th

is C

our

t

ha

s s

ub

j

ec

t m

a

tt

er

j

ur

is

d

i

c

ti

on

over

t

h

is

ac

ti

on under

S

ec

ti

on 15 of

t

he

Cl

ay

t

on Ac

t

, 15 U.

S

.

C

§ 25,

S

ec

ti

on 4 of

t

he

S

her

m

an

Ac

t

, 15 U.

S

.

C

. § 4, and 28 U.

S

.

C

. §§ 1331, 1337.

16. Defendan

ts

V

is

a and

Pl

a

i

d are engaged

i

n

i

n

t

er

st

a

t

e co

mm

erce and

i

n ac

ti

v

iti

e

s

s

ub

st

an

ti

a

ll

y affec

ti

ng

i

n

t

er

st

a

t

e co

mm

erce. V

is

a and

Pl

a

i

d

s

e

ll

on

li

ne deb

it

and da

t

a aggrega

ti

on

s

erv

i

ce

s t

hroughou

t t

he Un

it

ed

St

a

t

e

s

. They are engaged

i

n a regu

l

ar, con

ti

nuou

s

, and

s

ub

st

an

ti

a

l

f

l

ow of

i

n

t

er

st

a

t

e co

mm

erce, and

t

he

i

r

s

a

l

e

s

have had a

s

ub

st

an

ti

a

l

effec

t

on

i

n

t

er

st

a

t

e co

mm

erce.

17. Th

is C

our

t

ha

s

per

s

ona

l j

ur

is

d

i

c

ti

on over each Defendan

t

.

B

o

t

h V

is

a and

Pl

a

i

d

are corpora

ti

on

s t

ha

t t

ran

s

ac

t

bu

si

ne

ss

w

it

h

i

n

t

h

is

D

ist

r

i

c

t t

hrough, a

m

ong o

t

her

t

h

i

ng

s

,

t

he

i

r

s

a

l

e

s

of on

li

ne deb

it t

ran

s

ac

ti

on

s

and da

t

a aggrega

ti

on

s

erv

i

ce

s

.

V

E

NU

E

18. Venue

is

proper

i

n

t

h

is

d

ist

r

i

c

t

under

S

ec

ti

on 12 of

t

he

Cl

ay

t

on Ac

t

, 15 U.

S

.

C

.

§ 22 and 28 U.

S

.

C

. § 1391.

B

o

t

h Defendan

ts

are headquar

t

ered and

t

ran

s

ac

t

bu

si

ne

ss i

n

t

h

is

j

ud

i

c

i

a

l

D

ist

r

i

c

t

.

I

N

T

RAD

IST

R

I

C

T

A

SSIG

NM

E

N

T

19. A

ssi

gn

m

en

t t

o

t

he

S

an

F

ranc

is

co D

i

v

isi

on

is

proper. Th

is

ac

ti

on ar

is

e

s i

n

S

an

F

ranc

is

co

C

oun

t

y becau

s

e a

s

ub

st

an

ti

a

l

par

t

of

t

he even

ts t

ha

t

gave r

is

e

t

o

t

he c

l

a

ims

occurred

i

n

S

an

F

ranc

is

co.

Pl

a

i

d’

s

headquar

t

er

s

and pr

i

nc

i

pa

l

p

l

ace of bu

si

ne

ss is l

oca

t

ed

i

n

S

an

F

ranc

is

co.

V

is

a’

s

headquar

t

er

s

are

i

n

S

an

M

a

t

eo

C

oun

t

y

;

V

is

a ha

s

off

i

ce

s i

n

S

an

F

ranc

is

co and

is

bu

il

d

i

ng

new headquar

t

er

s i

n

S

an

F

ranc

is

co.

-6-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

D

E

F

E

NDAN

TS

AND

THE

PR

O

P

OSE

D AC

Q

U

ISITIO

N

20. V

is

a Inc.

is

a De

l

aware co

m

pany headquar

t

ered

i

n

F

o

st

er

Cit

y,

C

a

li

forn

i

a. V

is

a

is

a g

l

oba

l

pay

m

en

ts

co

m

pany

t

ha

t

opera

t

e

s t

he

l

arge

st

deb

it

ne

t

work

i

n

t

he Un

it

ed

St

a

t

e

s

. V

is

a

prov

i

de

s

a

t

wo-

si

ded

t

ran

s

ac

ti

on

s

p

l

a

t

for

m t

ha

t

au

t

hor

i

ze

s

, c

l

ear

s

, and

s

e

ttl

e

s

deb

it t

ran

s

ac

ti

on

s

be

t

ween bu

si

ne

ss

e

s

, con

s

u

m

er

s

, and bank

s

. V

is

a repor

t

ed revenue

s

of approx

im

a

t

e

l

y $23 b

illi

on

i

n f

is

ca

l

year 2019,

i

nc

l

ud

i

ng $10.3 b

illi

on

i

n

t

he Un

it

ed

St

a

t

e

s

.

21.

Pl

a

i

d Inc.

is

a De

l

aware co

m

pany headquar

t

ered

i

n

S

an

F

ranc

is

co,

C

a

li

forn

i

a.

Pl

a

i

d opera

t

e

s t

he

l

ead

i

ng f

i

nanc

i

a

l

da

t

a aggrega

ti

on p

l

a

t

for

m i

n

t

he Un

it

ed

St

a

t

e

s

. I

ts

t

echno

l

ogy a

ll

ow

s

con

s

u

m

er

s t

o connec

t t

he

i

r bank accoun

t i

nfor

m

a

ti

on

t

o f

i

n

t

ech app

s

, wh

i

ch

enab

l

e

s

f

i

n

t

ech

s t

o aggrega

t

e con

s

u

m

er

s

pend

i

ng da

t

a,

l

ook up accoun

t

ba

l

ance

s

, and ver

i

fy o

t

her

per

s

ona

l

f

i

nanc

i

a

l i

nfor

m

a

ti

on w

it

h con

s

u

m

er per

missi

on.

Pl

a

i

d’

s

revenue

s

have been grow

i

ng

rap

i

d

l

y and were a

lm

o

st

$100

milli

on

i

n 2019.

22. On

J

anuary 13, 2020, Defendan

ts

announced

t

ha

t

V

is

a wou

l

d acqu

i

re a

ll

of

Pl

a

i

d’

s

vo

ti

ng

s

ecur

iti

e

s

for con

si

dera

ti

on va

l

ued a

t

approx

im

a

t

e

l

y $5.3 b

illi

on.

B

AC

KG

R

O

UND

23. A deb

it t

ran

s

ac

ti

on

i

nvo

l

ve

s

a

m

u

lti

-

st

ep proce

ss t

ha

t

re

s

u

lts i

n

t

he

t

ran

s

fer of

fund

s

fro

m

a con

s

u

m

er’

s

bank accoun

t i

n

t

o a

m

erchan

t

’

s

bank accoun

t

u

si

ng

t

he con

s

u

m

er’

s

bank accoun

t

creden

ti

a

ls

. When a con

s

u

m

er

m

ake

s

an on

li

ne purcha

s

e u

si

ng

t

he

i

r deb

it

card

creden

ti

a

ls

(

i

.e. a deb

it

card nu

m

ber, exp

i

ra

ti

on da

t

e, and

C

VV

/C

V

C

nu

m

ber on

t

he back of a

deb

it

card), a deb

it t

ran

s

ac

ti

on w

it

hdraw

s

fund

s

fro

m t

he con

s

u

m

er’

s

bank accoun

t

. The on

li

ne

m

erchan

t

u

s

e

s t

he con

s

u

m

er’

s

creden

ti

a

ls t

o

s

end a reque

st t

o

t

he

m

erchan

t

’

s

bank (

t

he

“acqu

i

r

i

ng” bank or “acqu

i

rer”), wh

i

ch

i

n

t

urn u

s

e

s t

he deb

it

ne

t

work

t

o

s

end a reque

st t

o

t

he

con

s

u

m

er’

s

bank (

t

he “

iss

u

i

ng bank” or “

iss

uer”)

t

o conf

i

r

m

whe

t

her

t

he

iss

uer w

ill

au

t

hor

i

ze

t

he

t

ran

s

ac

ti

on. The

iss

uer w

ill t

yp

i

ca

ll

y au

t

hor

i

ze

t

he

t

ran

s

ac

ti

on

i

f

t

here

is

a

s

uff

i

c

i

en

t

accoun

t

ba

l

ance

t

o fund

t

he

t

ran

s

ac

ti

on. If

t

he

t

ran

s

ac

ti

on

is

au

t

hor

i

zed,

t

he con

s

u

m

er’

s

bank p

l

ace

s

a

ho

l

d on

t

he con

s

u

m

er’

s

fund

s

.

-7-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

24. Deb

it

ne

t

work

s

– V

is

a,

M

a

st

ercard, and a handfu

l

of

sm

a

ll

er ne

t

work

s

– opera

t

e

t

he

s

y

st

e

ms t

ha

t t

ran

smit t

he

s

e

m

e

ss

age

s

. Once

t

he con

s

u

m

er’

s iss

u

i

ng bank au

t

hor

i

ze

s t

he

t

ran

s

ac

ti

on,

t

he deb

it

ne

t

work a

ls

o guaran

t

ee

s t

he fund

s t

o

t

he

m

erchan

t

. Deb

it

ne

t

work

s

t

yp

i

ca

ll

y do no

t iss

ue card

s

d

i

rec

tl

y

t

o con

s

u

m

er

s

or e

st

ab

lis

h card-accep

ti

ng

s

erv

i

ce

s

w

it

h

m

erchan

ts

. The deb

it

ne

t

work

s t

yp

i

ca

ll

y con

t

rac

t

w

it

h

t

he acqu

i

r

i

ng and

iss

u

i

ng bank

s

, wh

i

ch

i

n

t

urn con

t

rac

t

w

it

h

m

erchan

ts

and con

s

u

m

er

s

, re

s

pec

ti

ve

l

y. The deb

it

ne

t

work a

ls

o c

l

ear

s

and

over

s

ee

s t

he

i

n

t

erbank

s

e

ttl

e

m

en

t

proce

ss

by aggrega

ti

ng a

ll t

ran

s

ac

ti

on

s

each day for each bank

i

n

its s

y

st

e

m

, ne

tti

ng ou

t

app

li

cab

l

e fee

s

, and prov

i

d

i

ng da

il

y

s

e

ttl

e

m

en

t

repor

ts t

o

t

he bank

s

.

W

it

h few excep

ti

on

s

,

t

he deb

it

ne

t

work

s

are no

t t

he

ms

e

l

ve

s

bank

s

and do no

t m

ove

m

oney

;

ra

t

her,

t

he ne

t

work

s

’

s

e

ttl

e

m

en

t

repor

ts

are u

s

ed by

t

he bank

s t

o

t

ran

s

fer fund

s

a

m

ong

t

he

ms

e

l

ve

s

,

t

yp

i

ca

ll

y u

si

ng a w

i

re

s

erv

i

ce ava

il

ab

l

e on

l

y

t

o bank

s

.

A. V

is

a

is

a Mo

n

o

p

o

lis

t

in Onlin

e De

bi

t

S

erv

i

ce

s

25. V

is

a

is

a

m

onopo

list

a

m

ong prov

i

der

s

of on

li

ne deb

it s

erv

i

ce

s

, w

it

h a durab

l

e

m

arke

t s

hare of approx

im

a

t

e

l

y 70%.

26. V

is

a’

s

nex

t

c

l

o

s

e

st

r

i

va

l is M

a

st

ercard, wh

i

ch

is

around one-

t

h

i

rd

t

he

si

ze of V

is

a

i

n on

li

ne deb

it

.

M

a

st

ercard ha

s

no

t

con

st

ra

i

ned V

is

a’

s m

onopo

l

y power by forc

i

ng

it t

o

l

ower

pr

i

ce

s t

o

m

erchan

ts

and con

s

u

m

er

s

.

M

erchan

ts t

ha

t

accep

t

deb

it

pay

m

en

ts

have no cho

i

ce bu

t t

o

accep

t

V

is

a. In con

t

ra

st t

o cred

it

card

s

,

m

o

st

con

s

u

m

er

s

carry on

l

y one deb

it

card. A con

s

u

m

er

w

it

h a V

is

a deb

it

card canno

t

u

s

e a

M

a

st

ercard deb

it

card

t

o w

it

hdraw fund

s

fro

m t

he

s

a

m

e

check

i

ng accoun

t

.

27. V

is

a ha

s s

ecured

l

ong-

t

er

m

con

t

rac

ts

w

it

h

m

any of

t

he

l

arge

st

f

i

nanc

i

a

l

i

n

stit

u

ti

on

s i

n

t

he Un

it

ed

St

a

t

e

s

, for

ti

fy

i

ng

t

he barr

i

er

s t

ha

t

he

l

p

m

a

i

n

t

a

i

n

its m

onopo

l

y. The

s

e

con

t

rac

ts limit t

he

s

e f

i

nanc

i

a

l i

n

stit

u

ti

on

s

’ ab

ilit

y

t

o

iss

ue deb

it

card

s

fro

m M

a

st

ercard, V

is

a’

s

on

l

y

m

ean

i

ngfu

l

co

m

pe

tit

or for card

iss

uance. V

is

a under

st

and

s t

ha

t M

a

st

ercard ha

s littl

e ab

ilit

y

-8-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

t

o d

is

p

l

ace V

is

a’

s

re

l

a

ti

on

s

h

i

p

s

w

it

h

t

ho

s

e f

i

nanc

i

a

l i

n

stit

u

ti

on

s

and con

s

equen

tl

y

littl

e ab

ilit

y

t

o

grow

its s

hare of con

s

u

m

er

s

’ wa

ll

e

ts

.

28.

M

erchan

ts

are charged

t

wo

t

ype

s

of fee

s

by V

is

a and

its

par

t

ner bank

s

, bo

t

h

s

e

t

by

V

is

a

: t

he “ne

t

work” fee

s

V

is

a co

ll

ec

ts t

o proce

ss t

he

t

ran

s

ac

ti

on, and

t

he “

i

n

t

erchange” fee

s t

ha

t

V

is

a co

m

pe

ls m

erchan

ts t

o pay

t

he bank

s t

ha

t iss

ue V

is

a-branded deb

it

card

s

. Taken

t

oge

t

her,

t

he deb

it

ne

t

work and

i

n

t

erchange fee

s t

ha

t

V

is

a and

its

par

t

ner bank

s

co

ll

ec

t

co

st

U.

S

.

m

erchan

ts

and con

s

u

m

er

s m

ore

t

han $6 b

illi

on per year.

29. Wh

il

e con

s

u

m

er

s

do no

t

pay V

is

a d

i

rec

tl

y

t

o u

s

e

its

pay

m

en

t

ne

t

work – and

re

l

a

ti

ve

l

y few earn

si

gn

i

f

i

can

t

reward

s

on V

is

a deb

it t

ran

s

ac

ti

on

s

– con

s

u

m

er

s i

nd

i

rec

tl

y pay for

V

is

a’

s t

ran

s

ac

ti

on fee

s i

n

t

he pr

i

ce of

t

he good

s

and

s

erv

i

ce

s t

hey buy fro

m m

erchan

ts

. In

t

h

is

way, V

is

a’

s

exce

ssi

ve deb

it

fee

s

opera

t

e a

s

a

t

ax on

m

erchan

ts t

ha

t is

pa

ss

ed on

t

o con

s

u

m

er

s

and burden

s t

he en

ti

re econo

m

y.

30.

R

ecogn

i

z

i

ng

t

he burden

im

po

s

ed by h

i

gh deb

it

fee

s

and

t

he barr

i

er

s t

o

co

m

pe

titi

on

i

n

t

he

m

arke

t

for deb

it t

ran

s

ac

ti

on

s

,

C

ongre

ss s

ough

t t

o “correc

t t

he

m

arke

t

defec

ts

t

ha

t

were con

t

r

i

bu

ti

ng

t

o h

i

gh and e

s

ca

l

a

ti

ng fee

s

” w

it

h

t

he Durb

i

n A

m

end

m

en

t

of

t

he 2010

Dodd-

F

rank Wa

ll St

ree

t R

efor

m

and

C

on

s

u

m

er

P

ro

t

ec

ti

on Ac

t

,

P

ub. L. No. 111-203, 124

St

a

t

.

1376 (2010). The Durb

i

n A

m

end

m

en

t

a

im

ed

t

o reduce h

i

gh fee

s

charged by deb

it

ne

t

work

s

w

it

h

a regu

l

a

t

ory cap and

i

ncrea

s

e

t

he nu

m

ber of

m

ean

i

ngfu

l

deb

it

co

m

pe

tit

or

s

.

31.

B

u

t t

he Durb

i

n A

m

end

m

en

t

cap

s

on

l

y

i

n

t

erchange fee

s t

ha

t

accrue

t

o V

is

a’

s l

arge

iss

u

i

ng bank

s

, and doe

s

no

t

regu

l

a

t

e

t

he ne

t

work fee

s t

ha

t

accrue

t

o V

is

a. A

s

a re

s

u

lt

, V

is

a ha

s

re

s

ponded by

im

po

si

ng new fee

s

on

m

erchan

ts t

ha

t

under

mi

ne

t

he effec

ti

vene

ss

of

t

he Durb

i

n

A

m

end

m

en

t

’

s

fee cap

s

. Even af

t

er enac

tm

en

t

of

t

he Durb

i

n A

m

end

m

en

t

, V

is

a e

stim

a

t

e

s t

ha

t it

earn

s

an 88% opera

ti

ng

m

arg

i

n fro

m its

ne

t

work fee

s

on deb

it

pay

m

en

ts

,

ill

u

st

ra

ti

ng

its

durab

l

e

m

onopo

l

y power.

32. The Durb

i

n A

m

end

m

en

t

a

ls

o requ

i

re

s

V

is

a and

M

a

st

ercard deb

it

card

s t

o

i

nc

l

ude

a fea

t

ure

t

ha

t

a

ll

ow

s m

erchan

ts t

o proce

ss t

ran

s

ac

ti

on

s

u

si

ng one of

t

he

s

o-ca

ll

ed “

P

IN” deb

it

ne

t

work

s

. The

s

e

sm

a

ll

er

P

IN ne

t

work

s

,

s

uch a

s

Acce

l

,

St

ar, NY

C

E, and

P

u

ls

e, have

s

o

m

e

m

ean

i

ngfu

l

pre

s

ence for

i

n-per

s

on deb

it t

ran

s

ac

ti

on

s

, bu

t

have ye

t t

o overco

m

e

t

he barr

i

er

s t

o

-9-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

en

t

ry for on

li

ne

t

ran

s

ac

ti

on

s

. Th

is is i

n par

t

becau

s

e V

is

a ha

s

erec

t

ed

t

echno

l

og

i

ca

l

barr

i

er

s

(

s

uch a

s

V

is

a’

s t

oken

i

za

ti

on

s

erv

i

ce, wh

i

ch w

it

hho

l

d

s

e

ss

en

ti

a

l

da

t

a fro

m P

IN ne

t

work

s

) and

en

t

ered

i

n

t

o re

st

r

i

c

ti

ve agree

m

en

ts t

ha

t

d

isi

ncen

ti

v

i

ze

t

he u

s

e of

P

IN ne

t

work

s

. A

s

a re

s

u

lt

,

m

erchan

ts

do no

t

u

s

e

P

IN ne

t

work

s i

n any

si

gn

i

f

i

can

t

vo

l

u

m

e

t

o proce

ss

on

li

ne

t

ran

s

ac

ti

on

s

, and

i

n

st

ead pay h

i

gher fee

s t

o u

s

e V

is

a and

M

a

st

ercard ne

t

work

s

.

B

. Pay-

b

y-

B

a

nk is

a New Form of

Onlin

e De

bi

t

S

erv

i

ce t

h

at

Th

reate

ns

V

is

a’

s

Mo

n

o

p

o

l

y

33.

F

or

t

he f

i

r

st tim

e

i

n

m

any year

s

, a new

t

ype of pay

m

en

ts s

erv

i

ce

is

po

is

ed

t

o

t

ake

s

hare away fro

m

V

is

a’

s

on

li

ne deb

it

bu

si

ne

ss

.

P

ay-by-bank

is

a for

m

of on

li

ne deb

it t

ha

t

u

s

e

s

a

con

s

u

m

er’

s

on

li

ne bank accoun

t

creden

ti

a

ls

(

i

.e. a con

s

u

m

er’

s

on

li

ne bank

i

ng u

s

erna

m

e and

pa

ss

word) – ra

t

her

t

han deb

it

card creden

ti

a

ls

–

t

o

i

den

ti

fy and ver

i

fy

t

he u

s

er, bank, accoun

t

nu

m

ber and ba

l

ance, and fac

ilit

a

t

e pay

m

en

ts t

o

m

erchan

ts

d

i

rec

tl

y fro

m t

he con

s

u

m

er’

s

bank

accoun

t

.

34.

P

ay-by-bank deb

it s

erv

i

ce

s

are a

l

ready w

i

de

l

y ava

il

ab

l

e

i

n o

t

her coun

t

r

i

e

s

. A

pay-by-bank p

l

a

t

for

m

fac

ilit

a

t

e

s

con

s

u

m

er-

t

o-bu

si

ne

ss

pay

m

en

ts

by prov

i

d

i

ng equ

i

va

l

en

t

end-

t

o-

end func

ti

ona

lit

y a

s t

he V

is

a deb

it

ne

t

work

: it

au

t

hor

i

ze

s

pay

m

en

t

fro

m

a con

s

u

m

er’

s

bank

accoun

t

, fac

ilit

a

t

e

s

co

mm

un

i

ca

ti

on

s

w

it

h

t

he con

s

u

m

er’

s

bank

t

o c

l

ear

t

he

t

ran

s

ac

ti

on, and

prov

i

de

s s

e

ttl

e

m

en

t s

erv

i

ce

s

by

i

n

iti

a

ti

ng a pay

m

en

t t

o

t

he

m

erchan

t

’

s

f

i

nanc

i

a

l i

n

stit

u

ti

on.

P

ay-

by-bank deb

it s

erv

i

ce

s

can co

m

p

l

e

t

e

t

h

is

f

i

na

l t

ran

s

fer of fund

s

u

si

ng Au

t

o

m

a

t

ed

Cl

ear

i

ng Hou

s

e

(“A

C

H”) or ano

t

her

l

ow-co

st

a

lt

erna

ti

ve

t

o V

is

a’

s

deb

it

ne

t

work.

35. A

C

H enab

l

e

s s

e

ttl

e

m

en

t

of

t

ran

s

ac

ti

on

s t

hrough

m

oney

t

ran

s

fer

s

over a ne

t

work

m

anaged by

t

wo u

tilit

y-

li

ke opera

t

or

s

, one run by

t

he

F

edera

l R

e

s

erve and

t

he o

t

her opera

t

ed by

The

Cl

ear

i

ng Hou

s

e, wh

i

ch

is

owned by a con

s

or

ti

u

m

of bank

s

. A pay-by-bank deb

it t

ran

s

ac

ti

on

u

si

ng A

C

H

s

e

ttl

e

m

en

t is

u

s

ua

ll

y

m

uch

l

e

ss

expen

si

ve

t

han a deb

it t

ran

s

ac

ti

on proce

ss

ed by a

card ne

t

work

li

ke V

is

a.

36.

B

ank

s t

yp

i

ca

ll

y charge

m

erchan

ts

f

l

a

t

ra

t

e

s

rang

i

ng fro

m t

wo ($0.02)

t

o

t

wen

t

y-

f

i

ve cen

ts

($0.25) for A

C

H

t

ran

s

ac

ti

on

s

, wherea

s

V

is

a deb

it t

ran

s

ac

ti

on

s t

yp

i

ca

ll

y co

st t

wen

t

y-

t

wo cen

ts

($0.22) p

l

u

s

a percen

t

age of

t

he overa

ll

va

l

ue of

t

he

t

ran

s

ac

ti

on, wh

i

ch can be

-10-

C

O

MP

LAINT

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

si

gn

i

f

i

can

t

.

F

or exa

m

p

l

e,

m

erchan

ts

and con

s

u

m

er

s t

yp

i

ca

ll

y pay rough

l

y

t

h

i

r

t

y-n

i

ne cen

ts

($0.39)

t

o proce

ss

a $60 deb

it t

ran

s

ac

ti

on (

t

he average on

li

ne deb

it t

ran

s

ac

ti

on

si

ze)

t

hrough

V

is

a’

s

ne

t

work, co

m

pared

t

o a

s littl

e a

s t

wo cen

ts

($0.02)

t

hrough A

C

H, a 95%

s

av

i

ng

s

.

B

y

harne

ssi

ng

t

he

s

e

s

av

i

ng

s

u

si

ng

its

be

st

-

i

n-c

l

a

ss t

echno

l

ogy and ex

isti

ng re

l

a

ti

on

s

h

i

p

s

w

it

h bank

s

and con

s

u

m

er

s

,

Pl

a

i

d

st

and

s t

o

s

ave

m

erchan

ts

and con

s

u

m

er

s

hundred

s

of

milli

on

s

of do

ll

ar

s

per year

i

n deb

it

fee

s

.

C. P

l

a

id is

U

niqu

e

l

y

Si

t

u

ate

d

to C

h

a

ll

e

n

ge V

is

a

37.

Pl

a

i

d’

s t

echno

l

ogy curren

tl

y prov

i

de

s

an ea

s

y

i

n

t

erface for f

i

n

t

ech app

s t

o co

ll

ec

t

con

s

u

m

er

s

’ f

i

nanc

i

a

l

da

t

a, w

it

h con

s

u

m

er per

missi

on. When a con

s

u

m

er

si

gn

s

up w

it

h a

Pl

a

i

d-

s

uppor

t

ed f

i

n

t

ech app and prov

i

de

s

her bank

l

og-

i

n creden

ti

a

ls

,

Pl

a

i

d u

s

e

s t

ho

s

e creden

ti

a

ls t

o

acce

ss t

he con

s

u

m

er’

s

f

i

nanc

i

a

l i

n

stit

u

ti

on and ob

t

a

i

n

t

he con

s

u

m

er’